TAL Education Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and tech disruption shape TAL Education Group’s growth and risks with our concise PESTLE snapshot—perfect for investors and strategists needing fast, actionable context; purchase the full analysis to unlock detailed insights, scenario impacts, and ready-to-use recommendations.

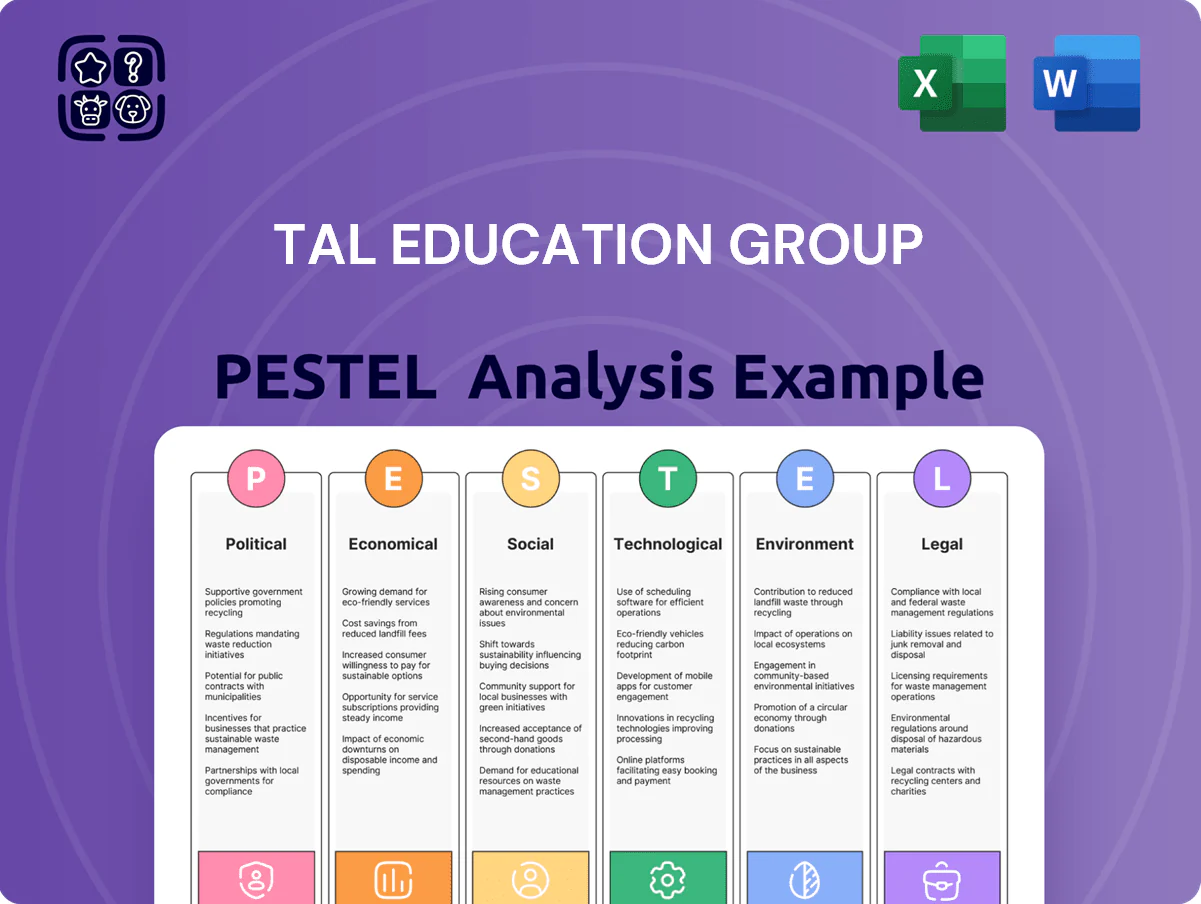

Political factors

Strict Government Oversight of Private Education

The Chinese government maintains tight control over private tutoring via the Double Reduction policies; after the July 2021 overhaul, by late 2025 regulatory stability had formed but authorities continue to monitor the sector to prevent renewed academic pressure on 200+ million K-12 students.

This environment forces TAL to align operations with Communist Party goals on equity and social welfare, affecting revenue streams: TAL reported adjusted FY2024 revenues of roughly RMB 12.3 billion, down from peak pre-regulation levels.

Geopolitical Tensions Affecting US-Listed Entities

State Support for Vocational and Non-Academic Learning

The Chinese government’s post-2021 education policy prioritizes vocational and holistic skills over exam-focused tutoring; TAL shifted accordingly, expanding arts, coding, and STEM enrichment—these non-academic segments contributed to a reported revenue recovery, with TAL’s Q3 2024 net revenue rising 18% year-over-year to RMB 5.2 billion, underscoring reliance on continued state backing for market access and legitimacy.

Data Sovereignty and National Security Policies

Political emphasis on data security has increased oversight of how edtech firms handle student and parent data; China's Personal Information Protection Law and Data Security Law impose strict controls that affect TAL's mainland operations, where K12 online revenue was RMB 6.2 billion in FY2023.

TAL must navigate rules on cross-border data transfer and algorithmic transparency for personalized learning; regulators have fined or restricted firms for breaches, making compliance essential to avoid sanctions that could jeopardize licenses and revenue streams.

- Strict laws: China PIPL and Data Security Law

- FY2023 K12 online revenue: RMB 6.2 billion

- Risk: license loss, fines, market access limits

Local Government Implementation Variance

National education reforms after 2021 reshape the sector, but provincial and municipal authorities enforce rules unevenly, causing operational differences for TAL across China.

Local enforcement affects TAL's ~1,000+ learning centers (2024 estimate) and regional revenue mixes—provinces with stricter rules show slower center openings and lower local enrollment rates.

Navigating these political nuances is vital for site selection, staffing, and compliance costs, which can materially impact regional margins and expansion pace.

- Uneven enforcement across provinces

- ~1,000+ learning centers (2024 est.) impacted

- Regional enforcement alters revenue and margins

- Critical for site selection and compliance planning

TAL pivots to non‑exam growth under tight regulation—FY24 revenue RMB12.3bn, Q3 +18%

Post-Double Reduction, TAL operates under strict state oversight—FY2024 revenue ~RMB 12.3bn, K‑12 online FY2023 ~RMB 6.2bn—with continued US‑China tensions (ADR investor share <15% in 2024) and heavy data-security compliance (PIPL, DSL) shaping market access, regional enforcement variability (≈1,000+ centers, 2024 est.) and pivot to non-exam offerings (Q3 2024 net revenue RMB 5.2bn, +18% YoY).

| Metric | Value |

|---|---|

| FY2024 revenue | RMB 12.3bn |

| K‑12 online FY2023 | RMB 6.2bn |

| Q3 2024 net revenue | RMB 5.2bn (+18% YoY) |

| US investor ADR share 2024 | <15% |

| Learning centers 2024 (est.) | ≈1,000+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect the TAL Education Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and trends to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for TAL Education Group that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market opportunities.

Economic factors

Impact of China's Macroeconomic Growth Deceleration

By late 2025 China GDP growth slowed to about 4.5% annualized, prompting middle-class households to tighten spending; household consumption growth fell to roughly 3.8% y/y in 2025 versus 5.5% in 2021.

With disposable income growth moderating and youth enrollment rates dipping, TAL’s premium tutoring segments face pricing pressure as parents prioritize cost-effective options.

The company must reconcile margin targets—operating margin was near 12% in 2024—with a more price-sensitive customer base, likely requiring product mix shifts and cost optimization.

Shifting Household Education Expenditure

Despite slowing GDP growth—6.3% in 2024 vs 8.1% pre-COVID—Chinese households still prioritize education, with per-student family spending on extracurriculars rising to an estimated CNY 12,400 in 2024 (up ~9% YoY), reflecting a shift from core tutoring to enrichment and skills training.

TAL faces a competitive pivot as K12 academic tutoring revenue fell sharply after 2021 reforms, so management is reallocating resources to after-school enrichment, where the private market was valued at ~CNY 220 billion in 2024.

Consequently, TAL’s future topline depends on capturing a larger share of the rising enrichment wallet amid price sensitivity and regulatory constraints, with 2025 guidance indicating a strategic focus on vocational, STEAM, and online subscription products to stabilize margins.

Labor Market Dynamics and Teacher Compensation

The post-2021 contraction left an estimated surplus of 200,000+ tutors in China; many shifted to tech, K‑12 live tutoring, or vocational training by 2024, easing short-term hiring but increasing competition for specialized instructors. TAL must balance higher pay for non-academic course experts—market median hourly rates for professional tutors rose ~18% in 2023–24—against margins, as personnel costs typically exceed 40% of revenue in education services.

Expansion into International Markets

TAL has scaled international operations to diversify risk, targeting Southeast Asia and North America where supplemental education demand grew ~6–8% CAGR in 2021–24; international revenue contributed under 10% of consolidated sales in 2024.

Macroeconomic strength in target regions affects enrollment and pricing power; a 5–10% currency swing versus RMB can erase margins, while localized marketing and compliance raised customer-acquisition costs by an estimated 15–25% in pilot markets.

- International revenue <10% of 2024 sales

- Southeast Asia/NA demand ~6–8% CAGR (2021–24)

- Currency moves ±5–10% materially impact margins

- Localized CAC up ~15–25% in pilots

Cost of Digital Transformation and Infrastructure

The capital intensity of TALs digital transformation is high: TAL reported technology and content investments of RMB 5.8 billion in FY2023 and continued heavy spend into 2024 to scale cloud, servers and AI for its hybrid model, pressuring margins as digital-native rivals expand with lower legacy costs.

Careful capex allocation is critical to convert these expenditures into long-term efficiency gains rather than permanent operating overhead, given cloud/AI running costs and estimated industry server/cloud growth of 15–20% p.a. through 2025.

- RMB 5.8bn tech/content spend in FY2023

- Cloud/server/AI costs rising ~15–20% p.a. industry-wide

- Risk: capex that raises opex if not efficiency-linked

TAL pressured by slowing China demand, rising tutor pay and FX volatility

Slowing China GDP (≈4.5% in 2025) and softer household consumption (≈3.8% y/y 2025) pressure TAL’s premium K12 pricing; enrichment spending rose to ~CNY12,400 per student in 2024 as K12 revenue contracted post-2021. TAL’s 2024 operating margin ~12% faces headwinds from higher tutor pay (+18% 2023–24) and RMB ±5–10% FX swings; international revenue <10% of 2024 sales.

| Metric | Value |

|---|---|

| China GDP 2025 | ≈4.5% |

| Household consumption 2025 | ≈3.8% y/y |

| Per-student extracurricular 2024 | CNY12,400 |

| Op. margin 2024 | ~12% |

| Tutor pay rise 2023–24 | ~18% |

| Intl revenue 2024 | <10% |

What You See Is What You Get

TAL Education Group PESTLE Analysis

The preview shown here is the exact TAL Education Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

No placeholders or teasers: the content, layout, and insights visible in this preview are exactly what you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and tech disruption shape TAL Education Group’s growth and risks with our concise PESTLE snapshot—perfect for investors and strategists needing fast, actionable context; purchase the full analysis to unlock detailed insights, scenario impacts, and ready-to-use recommendations.

Political factors

Strict Government Oversight of Private Education

The Chinese government maintains tight control over private tutoring via the Double Reduction policies; after the July 2021 overhaul, by late 2025 regulatory stability had formed but authorities continue to monitor the sector to prevent renewed academic pressure on 200+ million K-12 students.

This environment forces TAL to align operations with Communist Party goals on equity and social welfare, affecting revenue streams: TAL reported adjusted FY2024 revenues of roughly RMB 12.3 billion, down from peak pre-regulation levels.

Geopolitical Tensions Affecting US-Listed Entities

State Support for Vocational and Non-Academic Learning

The Chinese government’s post-2021 education policy prioritizes vocational and holistic skills over exam-focused tutoring; TAL shifted accordingly, expanding arts, coding, and STEM enrichment—these non-academic segments contributed to a reported revenue recovery, with TAL’s Q3 2024 net revenue rising 18% year-over-year to RMB 5.2 billion, underscoring reliance on continued state backing for market access and legitimacy.

Data Sovereignty and National Security Policies

Political emphasis on data security has increased oversight of how edtech firms handle student and parent data; China's Personal Information Protection Law and Data Security Law impose strict controls that affect TAL's mainland operations, where K12 online revenue was RMB 6.2 billion in FY2023.

TAL must navigate rules on cross-border data transfer and algorithmic transparency for personalized learning; regulators have fined or restricted firms for breaches, making compliance essential to avoid sanctions that could jeopardize licenses and revenue streams.

- Strict laws: China PIPL and Data Security Law

- FY2023 K12 online revenue: RMB 6.2 billion

- Risk: license loss, fines, market access limits

Local Government Implementation Variance

National education reforms after 2021 reshape the sector, but provincial and municipal authorities enforce rules unevenly, causing operational differences for TAL across China.

Local enforcement affects TAL's ~1,000+ learning centers (2024 estimate) and regional revenue mixes—provinces with stricter rules show slower center openings and lower local enrollment rates.

Navigating these political nuances is vital for site selection, staffing, and compliance costs, which can materially impact regional margins and expansion pace.

- Uneven enforcement across provinces

- ~1,000+ learning centers (2024 est.) impacted

- Regional enforcement alters revenue and margins

- Critical for site selection and compliance planning

TAL pivots to non‑exam growth under tight regulation—FY24 revenue RMB12.3bn, Q3 +18%

Post-Double Reduction, TAL operates under strict state oversight—FY2024 revenue ~RMB 12.3bn, K‑12 online FY2023 ~RMB 6.2bn—with continued US‑China tensions (ADR investor share <15% in 2024) and heavy data-security compliance (PIPL, DSL) shaping market access, regional enforcement variability (≈1,000+ centers, 2024 est.) and pivot to non-exam offerings (Q3 2024 net revenue RMB 5.2bn, +18% YoY).

| Metric | Value |

|---|---|

| FY2024 revenue | RMB 12.3bn |

| K‑12 online FY2023 | RMB 6.2bn |

| Q3 2024 net revenue | RMB 5.2bn (+18% YoY) |

| US investor ADR share 2024 | <15% |

| Learning centers 2024 (est.) | ≈1,000+ |

What is included in the product

Explores how external macro-environmental factors uniquely affect the TAL Education Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and trends to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

A concise, visually segmented PESTLE summary for TAL Education Group that can be dropped into presentations or shared across teams to quickly align on external risks, regulatory shifts, and market opportunities.

Economic factors

Impact of China's Macroeconomic Growth Deceleration

By late 2025 China GDP growth slowed to about 4.5% annualized, prompting middle-class households to tighten spending; household consumption growth fell to roughly 3.8% y/y in 2025 versus 5.5% in 2021.

With disposable income growth moderating and youth enrollment rates dipping, TAL’s premium tutoring segments face pricing pressure as parents prioritize cost-effective options.

The company must reconcile margin targets—operating margin was near 12% in 2024—with a more price-sensitive customer base, likely requiring product mix shifts and cost optimization.

Shifting Household Education Expenditure

Despite slowing GDP growth—6.3% in 2024 vs 8.1% pre-COVID—Chinese households still prioritize education, with per-student family spending on extracurriculars rising to an estimated CNY 12,400 in 2024 (up ~9% YoY), reflecting a shift from core tutoring to enrichment and skills training.

TAL faces a competitive pivot as K12 academic tutoring revenue fell sharply after 2021 reforms, so management is reallocating resources to after-school enrichment, where the private market was valued at ~CNY 220 billion in 2024.

Consequently, TAL’s future topline depends on capturing a larger share of the rising enrichment wallet amid price sensitivity and regulatory constraints, with 2025 guidance indicating a strategic focus on vocational, STEAM, and online subscription products to stabilize margins.

Labor Market Dynamics and Teacher Compensation

The post-2021 contraction left an estimated surplus of 200,000+ tutors in China; many shifted to tech, K‑12 live tutoring, or vocational training by 2024, easing short-term hiring but increasing competition for specialized instructors. TAL must balance higher pay for non-academic course experts—market median hourly rates for professional tutors rose ~18% in 2023–24—against margins, as personnel costs typically exceed 40% of revenue in education services.

Expansion into International Markets

TAL has scaled international operations to diversify risk, targeting Southeast Asia and North America where supplemental education demand grew ~6–8% CAGR in 2021–24; international revenue contributed under 10% of consolidated sales in 2024.

Macroeconomic strength in target regions affects enrollment and pricing power; a 5–10% currency swing versus RMB can erase margins, while localized marketing and compliance raised customer-acquisition costs by an estimated 15–25% in pilot markets.

- International revenue <10% of 2024 sales

- Southeast Asia/NA demand ~6–8% CAGR (2021–24)

- Currency moves ±5–10% materially impact margins

- Localized CAC up ~15–25% in pilots

Cost of Digital Transformation and Infrastructure

The capital intensity of TALs digital transformation is high: TAL reported technology and content investments of RMB 5.8 billion in FY2023 and continued heavy spend into 2024 to scale cloud, servers and AI for its hybrid model, pressuring margins as digital-native rivals expand with lower legacy costs.

Careful capex allocation is critical to convert these expenditures into long-term efficiency gains rather than permanent operating overhead, given cloud/AI running costs and estimated industry server/cloud growth of 15–20% p.a. through 2025.

- RMB 5.8bn tech/content spend in FY2023

- Cloud/server/AI costs rising ~15–20% p.a. industry-wide

- Risk: capex that raises opex if not efficiency-linked

TAL pressured by slowing China demand, rising tutor pay and FX volatility

Slowing China GDP (≈4.5% in 2025) and softer household consumption (≈3.8% y/y 2025) pressure TAL’s premium K12 pricing; enrichment spending rose to ~CNY12,400 per student in 2024 as K12 revenue contracted post-2021. TAL’s 2024 operating margin ~12% faces headwinds from higher tutor pay (+18% 2023–24) and RMB ±5–10% FX swings; international revenue <10% of 2024 sales.

| Metric | Value |

|---|---|

| China GDP 2025 | ≈4.5% |

| Household consumption 2025 | ≈3.8% y/y |

| Per-student extracurricular 2024 | CNY12,400 |

| Op. margin 2024 | ~12% |

| Tutor pay rise 2023–24 | ~18% |

| Intl revenue 2024 | <10% |

What You See Is What You Get

TAL Education Group PESTLE Analysis

The preview shown here is the exact TAL Education Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

No placeholders or teasers: the content, layout, and insights visible in this preview are exactly what you’ll download immediately after payment.