First Bank SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

First Bank’s resilient retail franchise, expanding digital offerings, and strong capital position drive steady growth, though regulatory shifts and competitive pressure from fintechs pose clear risks; our full SWOT unpacks these dynamics with financial context and strategic takeaways. Purchase the complete SWOT analysis to receive a professionally formatted, editable report and Excel deliverable—ideal for investors, advisors, and executives planning next steps.

Strengths

Dominant Puerto Rico Market Position

First BanCorp holds roughly 30% deposit share in Puerto Rico (2024 FDIC data), giving a stable, low-cost core deposit base versus mainland peers and strong brand recognition that supports ROA resilience—2024 net interest margin was 3.1% and deposits funded ~85% of assets.

Robust Capital and Liquidity Ratios

As of year-end 2025, First Bank reported a Common Equity Tier 1 (CET1) ratio of 12.8%, a Total Capital ratio of 15.6%, and a liquidity coverage ratio (LCR) of 140%, all comfortably above U.S. well-capitalized buffers, providing a sturdy buffer against downturns.

These capital and liquidity levels support continued quarterly dividends (2025 dividend yield ~3.1%) and permit measured loan growth, with loan-to-deposit at 82% ensuring short-term obligations are easily met.

Diversified Revenue Streams

First Bank has woven wealth management and insurance into its offer, lifting non-interest income to 32% of total revenue in FY2024 (up from 24% in 2019), which cuts reliance on net interest margin and cushions earnings against rate swings. These fee and premium streams helped ROA rise to 1.25% in 2024, and customer retention climbed 6 percentage points as cross-sell rates hit 28%—boosting profitability and stickiness.

Efficient Operational Structure

First BanCorp tightened costs: efficiency ratio improved from 62% in 2021 to 54% in 2024, driven by branch consolidation and headcount-light back-office automation, boosting pre-provision operating margin by ~180 bps over that period.

Saved capital funds digital spend—$120m invested in 2024 into mobile/online platforms—raising transaction-per-customer and lowering branch transaction costs.

- Efficiency ratio: 54% (2024)

- Operating margin +180 bps (2021–2024)

- Digital capex: $120m (2024)

- Branch count reduced, productivity ↑

Strong Commercial Lending Expertise

The bank’s focused commercial and industrial lending in Florida and Puerto Rico drives superior underwriting and local risk pricing; as of 2025 YTD commercial loans represent 62% of total loans and C&I NPAs remain low at 0.45% versus peer median 1.2%.

Deep local knowledge and repeat borrower relationships kept net charge-offs under 0.15% in 2024, supporting a high-quality loan book through recent regional stress.

- 62% commercial loan mix (2025 YTD)

- 0.45% C&I non-performing assets (2025)

- Net charge-offs 0.15% (2024)

First BanCorp: Dominant PR Deposits, Strong Capital & 3.1% NIM Fueling Growth

First BanCorp’s strengths: ~30% Puerto Rico deposit share (2024 FDIC), deposits fund ~85% of assets, NIM 3.1% (2024); CET1 12.8%, Total Capital 15.6%, LCR 140% (2025); non-interest income 32% (2024), ROA 1.25% (2024); efficiency 54% (2024), digital capex $120m (2024); C&I loans 62% (2025 YTD), C&I NPAs 0.45% (2025).

| Metric | Value |

|---|---|

| PR deposit share | ~30% (2024) |

| NIM | 3.1% (2024) |

| CET1 | 12.8% (2025) |

| LCR | 140% (2025) |

| Non-interest income | 32% (2024) |

| Efficiency ratio | 54% (2024) |

| Digital capex | $120m (2024) |

| C&I mix | 62% (2025 YTD) |

What is included in the product

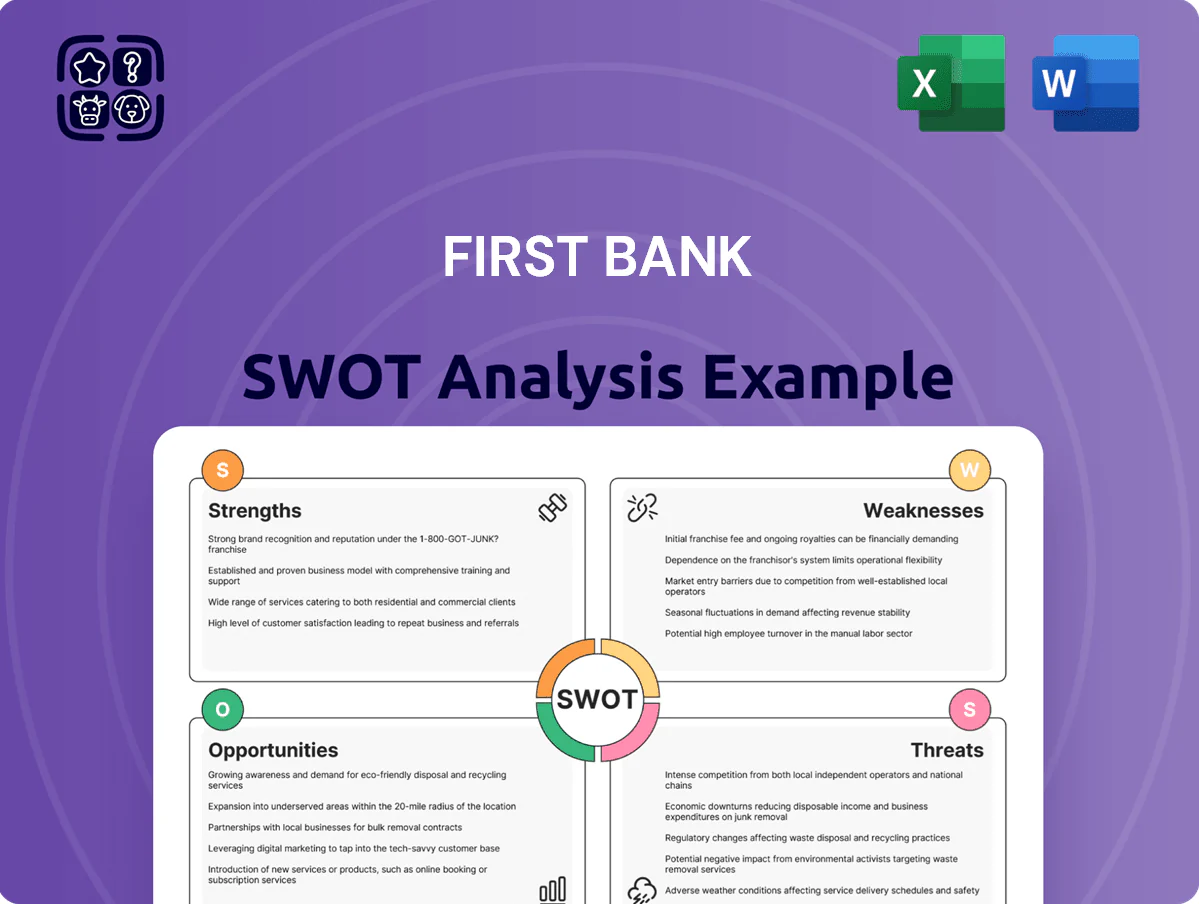

Provides a clear SWOT framework for analyzing First Bank’s business strategy, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping future performance.

Delivers a concise SWOT matrix for First Bank to expedite strategic alignment and quick stakeholder-ready summaries.

Weaknesses

High Geographic Concentration

A significant majority of First BanCorp’s assets and loans remain concentrated in Puerto Rico—about 80% of net loans and 75% of deposits as of FY2024—making the bank highly vulnerable to localized economic shifts. This limited geographic diversification leaves it exposed to island-specific risks like a 2023 GDP contraction of 1.3% and hurricane damage, which hit net income and credit metrics harder than for national peers. Any Puerto Rico downturn therefore directly and disproportionately affects overall financial performance.

Vulnerability to Natural Disasters

Operating mainly in the Caribbean and Florida exposes First Bank to frequent hurricanes; NOAA recorded 18 named storms in 2023 and 7 major hurricanes in 2024, raising physical and operational risk.

Storms can halt branches, damage collateral and spike charge-offs; after Hurricane Ian (2022) regional banks saw nonperforming loans jump 0.4–0.9 percentage points.

Disaster recovery and elevated insurance premiums cost the bank materially; industry catastrophe reinsurance expenses rose ~15% in 2024, squeezing margins.

Interest Rate Sensitivity

First Bank’s net interest margin (NIM) is highly sensitive to Federal Reserve rate moves; a 100bp Fed hike in 2022 roughly cut peer regional NIMs by ~15-25bps, illustrating earnings volatility for similar banks.

Repricing mismatches between assets and liabilities can compress margins during rapid cycles; if loan yields reprice slower than deposit costs, NIM can fall by dozens of basis points within quarters.

Managing this sensitivity requires complex, costly hedges—swaps and caps—whose fees and mark-to-market swings trimmed bank sector pre-tax income by up to 10% in volatile 2022–2023 periods.

Limited Scale vs National Competitors

First BanCorp, with $20.4 billion in assets at year-end 2024, lacks the R&D scale of U.S. money-center banks that spend billions on fintech—JPMorgan Chase spent $13.2B on tech in 2024—making it harder to build cutting-edge digital features fast.

That scale gap limits appeal to younger, tech-first customers; mobile-native cohorts (18–34) expect rapid feature rollout and personalization.

First BanCorp often uses third-party vendors, slowing customization and time-to-market compared with in-house teams.

- Assets: $20.4B (2024)

- Peer tech spend: JPM 2024 tech $13.2B

- Dependency: third-party vendors slow customization

Historical Credit Quality Volatility

Despite stable CET1 of 10.8% and NPLs at 1.9% in 2024, First BanCorp faced sharp credit deterioration during Puerto Rico’s 2016 fiscal crisis and 2017–2018 recession, raising investor wariness and pressuring valuation and cost of capital.

Maintaining pristine credit needs tight underwriting and stress testing, which can slow loan growth during recoveries; historically, loan-loss provisions spiked to 150–200 bps in crisis years.

- 2024 CET1 10.8%

- NPLs 1.9% (2024)

- Provisions 150–200 bps in crises

Puerto Rico-focused bank: high hurricane, credit and tech risks despite $20.4B assets

Concentrated Puerto Rico exposure (≈80% loans, 75% deposits, $20.4B assets in 2024) raises GDP, hurricane, and credit risk; hurricanes (18 named storms 2023; 7 major in 2024) spike charge-offs and recovery costs; NIM volatility from Fed moves and repricing mismatches; tech scale gap vs peers (JPM tech $13.2B 2024) slows digital rollout; CET1 10.8% and NPLs 1.9% heighten investor caution.

| Metric | Value |

|---|---|

| Assets (2024) | $20.4B |

| Loans in PR | ~80% |

| Deposits in PR | ~75% |

| CET1 (2024) | 10.8% |

| NPLs (2024) | 1.9% |

| Peer tech spend (JPM, 2024) | $13.2B |

| Named storms (2023) | 18 |

| Major hurricanes (2024) | 7 |

Same Document Delivered

First Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is not a sample but the real, editable analysis you'll download post-purchase. Purchase unlocks the entire in-depth version, ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

First Bank’s resilient retail franchise, expanding digital offerings, and strong capital position drive steady growth, though regulatory shifts and competitive pressure from fintechs pose clear risks; our full SWOT unpacks these dynamics with financial context and strategic takeaways. Purchase the complete SWOT analysis to receive a professionally formatted, editable report and Excel deliverable—ideal for investors, advisors, and executives planning next steps.

Strengths

Dominant Puerto Rico Market Position

First BanCorp holds roughly 30% deposit share in Puerto Rico (2024 FDIC data), giving a stable, low-cost core deposit base versus mainland peers and strong brand recognition that supports ROA resilience—2024 net interest margin was 3.1% and deposits funded ~85% of assets.

Robust Capital and Liquidity Ratios

As of year-end 2025, First Bank reported a Common Equity Tier 1 (CET1) ratio of 12.8%, a Total Capital ratio of 15.6%, and a liquidity coverage ratio (LCR) of 140%, all comfortably above U.S. well-capitalized buffers, providing a sturdy buffer against downturns.

These capital and liquidity levels support continued quarterly dividends (2025 dividend yield ~3.1%) and permit measured loan growth, with loan-to-deposit at 82% ensuring short-term obligations are easily met.

Diversified Revenue Streams

First Bank has woven wealth management and insurance into its offer, lifting non-interest income to 32% of total revenue in FY2024 (up from 24% in 2019), which cuts reliance on net interest margin and cushions earnings against rate swings. These fee and premium streams helped ROA rise to 1.25% in 2024, and customer retention climbed 6 percentage points as cross-sell rates hit 28%—boosting profitability and stickiness.

Efficient Operational Structure

First BanCorp tightened costs: efficiency ratio improved from 62% in 2021 to 54% in 2024, driven by branch consolidation and headcount-light back-office automation, boosting pre-provision operating margin by ~180 bps over that period.

Saved capital funds digital spend—$120m invested in 2024 into mobile/online platforms—raising transaction-per-customer and lowering branch transaction costs.

- Efficiency ratio: 54% (2024)

- Operating margin +180 bps (2021–2024)

- Digital capex: $120m (2024)

- Branch count reduced, productivity ↑

Strong Commercial Lending Expertise

The bank’s focused commercial and industrial lending in Florida and Puerto Rico drives superior underwriting and local risk pricing; as of 2025 YTD commercial loans represent 62% of total loans and C&I NPAs remain low at 0.45% versus peer median 1.2%.

Deep local knowledge and repeat borrower relationships kept net charge-offs under 0.15% in 2024, supporting a high-quality loan book through recent regional stress.

- 62% commercial loan mix (2025 YTD)

- 0.45% C&I non-performing assets (2025)

- Net charge-offs 0.15% (2024)

First BanCorp: Dominant PR Deposits, Strong Capital & 3.1% NIM Fueling Growth

First BanCorp’s strengths: ~30% Puerto Rico deposit share (2024 FDIC), deposits fund ~85% of assets, NIM 3.1% (2024); CET1 12.8%, Total Capital 15.6%, LCR 140% (2025); non-interest income 32% (2024), ROA 1.25% (2024); efficiency 54% (2024), digital capex $120m (2024); C&I loans 62% (2025 YTD), C&I NPAs 0.45% (2025).

| Metric | Value |

|---|---|

| PR deposit share | ~30% (2024) |

| NIM | 3.1% (2024) |

| CET1 | 12.8% (2025) |

| LCR | 140% (2025) |

| Non-interest income | 32% (2024) |

| Efficiency ratio | 54% (2024) |

| Digital capex | $120m (2024) |

| C&I mix | 62% (2025 YTD) |

What is included in the product

Provides a clear SWOT framework for analyzing First Bank’s business strategy, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping future performance.

Delivers a concise SWOT matrix for First Bank to expedite strategic alignment and quick stakeholder-ready summaries.

Weaknesses

High Geographic Concentration

A significant majority of First BanCorp’s assets and loans remain concentrated in Puerto Rico—about 80% of net loans and 75% of deposits as of FY2024—making the bank highly vulnerable to localized economic shifts. This limited geographic diversification leaves it exposed to island-specific risks like a 2023 GDP contraction of 1.3% and hurricane damage, which hit net income and credit metrics harder than for national peers. Any Puerto Rico downturn therefore directly and disproportionately affects overall financial performance.

Vulnerability to Natural Disasters

Operating mainly in the Caribbean and Florida exposes First Bank to frequent hurricanes; NOAA recorded 18 named storms in 2023 and 7 major hurricanes in 2024, raising physical and operational risk.

Storms can halt branches, damage collateral and spike charge-offs; after Hurricane Ian (2022) regional banks saw nonperforming loans jump 0.4–0.9 percentage points.

Disaster recovery and elevated insurance premiums cost the bank materially; industry catastrophe reinsurance expenses rose ~15% in 2024, squeezing margins.

Interest Rate Sensitivity

First Bank’s net interest margin (NIM) is highly sensitive to Federal Reserve rate moves; a 100bp Fed hike in 2022 roughly cut peer regional NIMs by ~15-25bps, illustrating earnings volatility for similar banks.

Repricing mismatches between assets and liabilities can compress margins during rapid cycles; if loan yields reprice slower than deposit costs, NIM can fall by dozens of basis points within quarters.

Managing this sensitivity requires complex, costly hedges—swaps and caps—whose fees and mark-to-market swings trimmed bank sector pre-tax income by up to 10% in volatile 2022–2023 periods.

Limited Scale vs National Competitors

First BanCorp, with $20.4 billion in assets at year-end 2024, lacks the R&D scale of U.S. money-center banks that spend billions on fintech—JPMorgan Chase spent $13.2B on tech in 2024—making it harder to build cutting-edge digital features fast.

That scale gap limits appeal to younger, tech-first customers; mobile-native cohorts (18–34) expect rapid feature rollout and personalization.

First BanCorp often uses third-party vendors, slowing customization and time-to-market compared with in-house teams.

- Assets: $20.4B (2024)

- Peer tech spend: JPM 2024 tech $13.2B

- Dependency: third-party vendors slow customization

Historical Credit Quality Volatility

Despite stable CET1 of 10.8% and NPLs at 1.9% in 2024, First BanCorp faced sharp credit deterioration during Puerto Rico’s 2016 fiscal crisis and 2017–2018 recession, raising investor wariness and pressuring valuation and cost of capital.

Maintaining pristine credit needs tight underwriting and stress testing, which can slow loan growth during recoveries; historically, loan-loss provisions spiked to 150–200 bps in crisis years.

- 2024 CET1 10.8%

- NPLs 1.9% (2024)

- Provisions 150–200 bps in crises

Puerto Rico-focused bank: high hurricane, credit and tech risks despite $20.4B assets

Concentrated Puerto Rico exposure (≈80% loans, 75% deposits, $20.4B assets in 2024) raises GDP, hurricane, and credit risk; hurricanes (18 named storms 2023; 7 major in 2024) spike charge-offs and recovery costs; NIM volatility from Fed moves and repricing mismatches; tech scale gap vs peers (JPM tech $13.2B 2024) slows digital rollout; CET1 10.8% and NPLs 1.9% heighten investor caution.

| Metric | Value |

|---|---|

| Assets (2024) | $20.4B |

| Loans in PR | ~80% |

| Deposits in PR | ~75% |

| CET1 (2024) | 10.8% |

| NPLs (2024) | 1.9% |

| Peer tech spend (JPM, 2024) | $13.2B |

| Named storms (2023) | 18 |

| Major hurricanes (2024) | 7 |

Same Document Delivered

First Bank SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is not a sample but the real, editable analysis you'll download post-purchase. Purchase unlocks the entire in-depth version, ready for immediate use.