2CRSI Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

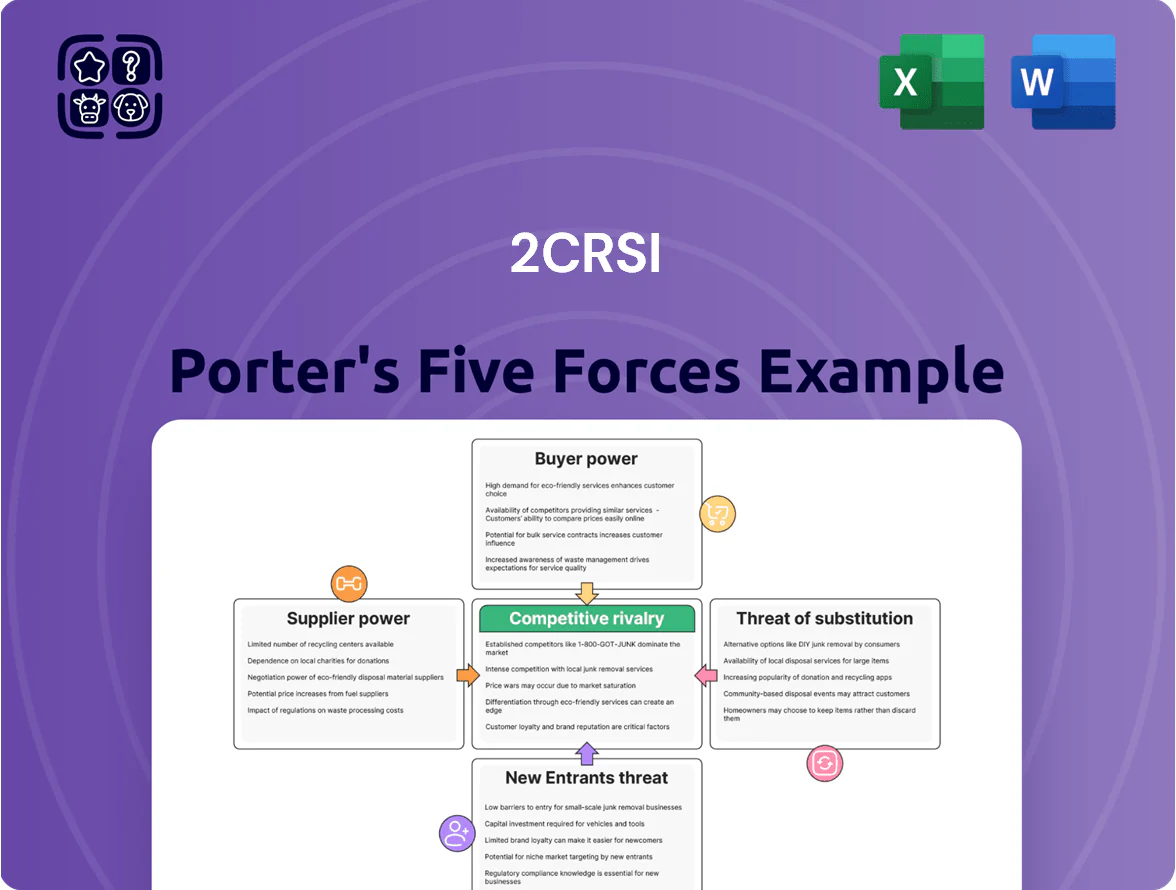

2CRSI faces mixed pressures: moderate supplier leverage for specialized components, strong buyer demands for cost and customization, and growing rivalry in HPC and edge servers—while barriers to entry and substitutes exert variable threat levels. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore 2CRSI’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Tier 1 Semiconductor Manufacturers

The primary components for 2CRSI servers—GPUs and CPUs—are concentrated among Nvidia, AMD, and Intel, which controlled roughly 85% of AI-capable GPU/CPU market share in 2025; their specialized silicon and constrained wafer capacity give them major pricing power. 2CRSI is effectively a price taker as suppliers allocate supply to large cloud and hyperscaler customers, with spot GPU prices up ~30% year-over-year in 2025, pressuring margins.

Specialized Component Scarcity

Beyond CPUs, 2CRSI depends on specialized cooling and high-speed networking parts—often custom or from niche suppliers—giving vendors leverage; a 2024 supply-chain survey showed 42% of data‑center component shortages were in cooling/networking.

Disruptions can delay deliveries by 6–12 weeks and raise component costs 8–15%, so 2CRSI needs multi‑year contracts and strategic partnerships to secure parts for its bespoke servers.

Impact of Proprietary Technology Moats

Suppliers of proprietary software and firmware in 2CRSI’s storage and server stacks hold high bargaining power, able to set licensing fees and update cadences that shape 2CRSI’s roadmap; in 2025 enterprise AI software license CAGR hit ~22%, pushing vendor leverage.

These partners can force recurring royalties and mandatory upgrades, raising gross margin pressure—2CRSI’s gross margin sensitivity to COGS swings could exceed 200–300 bps if license costs rise 10%.

By 2026, as integrated AI stacks (inference+management) become standard, dependency on specialized vendors increases procurement risk and operating cost volatility, making supplier relationships a strategic constraint for 2CRSI.

Raw Material Price Volatility

In 2025, 2CRSI faces raw material price volatility as rare earths and high-grade copper—key for high-performance servers—are constrained by geopolitics and green-energy demand; copper jumped ~25% in 2024 and select rare earths rose 30–50% year-on-year.

Suppliers wield high bargaining power: limited producers and tight markets let them pass costs to 2CRSI with little negotiation room, squeezing margins and forcing price-adjustments or redesigns.

- Copper +25% in 2024

- Rare earths +30–50% YoY

- Green-energy demand ups competition for minerals

- Limited supplier base → low negotiation leverage

Switching Costs for Engineering Integration

Once 2CRSI integrates a supplier's architecture into custom servers, switching costs become prohibitive—redesigning motherboards and thermal systems demands large R&D outlays and months of validation, often 6–18 months and €1–3M per platform based on industry benchmarks.

This technical lock-in boosts supplier leverage in renewals and price talks, effectively raising supplier bargaining power and risking 3–7% margin compression if prices rise.

- 6–18 months redesign time

- €1–3M typical R&D cost

- 3–7% potential margin hit

Suppliers’ dominance spikes costs—multi‑year contracts needed to protect 2CRSI margins

Suppliers hold high bargaining power: Nvidia/AMD/Intel ~85% share in AI-capable silicon (2025), spot GPU prices +30% YoY, copper +25% (2024), rare earths +30–50% YoY; switching costs 6–18 months and €1–3M per platform, causing 3–7% potential margin hit—2CRSI must use multi-year contracts and partnerships to mitigate supply-driven cost and timing risk.

| Metric | Value |

|---|---|

| AI silicon share (2025) | ~85% |

| Spot GPU price change (2025 YoY) | +30% |

| Copper (2024) | +25% |

| Rare earths YoY | +30–50% |

| Redesign time | 6–18 months |

| R&D cost/platform | €1–3M |

| Potential margin hit | 3–7% |

What is included in the product

Tailored Porter’s Five Forces analysis for 2CRSi that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, plus disruptive risks and strategic levers to protect market share and profitability.

Clear, one-sheet Porter's Five Forces for 2CRSI—instantly spot competitive pressures and make faster strategic decisions.

Customers Bargaining Power

Concentration of Hyperscale Buyers

Large cloud providers and mega data centers account for roughly 40–55% of enterprise server demand and can push hard on price; their volume buys let them extract discounts of 15–30% on rack-scale orders, squeezing 2CRSI margins. These buyers run formal RFPs and reverse auctions, forcing 2CRSI to compete on cost and customization to win multi‑year deals. By end‑2025, further consolidation—top 5 owners controlling an estimated 60% of hyperscale capacity—amplifies institutional bargaining power and pricing pressure on vendors like 2CRSI.

Demand for Customization as a Leverage Point

2CRSI’s bespoke, high-performance servers for AI and edge computing reduce customers’ price leverage: buyers with specific technical specs face few substitutes, so they can’t easily push down prices. In 2025 the AI server market’s custom segment grew ~18% YoY, letting niche vendors hold ~15–25% gross margins versus 5–12% for commodity OEMs. Large-volume buyers still exert volume power, but customization narrows that gap.

Low Switching Costs for Standardized Hardware

For 2CRSI’s standardized server and storage lines, switching costs are low: studies show 68% of enterprise buyers prioritize price and performance-per-watt over vendor lock-in, so a competitor offering similar efficiency at 5–15% lower price can capture next-cycle orders. This forces 2CRSI to raise R&D (it spent €7.2m in 2024) and expand after-sales SLAs to retain customers and protect margins.

Price Sensitivity in the Mid-Market Segment

Small and mid-sized enterprises (SMEs) and research labs face tight capex limits and prioritize total cost of ownership—upfront price plus energy and maintenance—when buying 2CRSI servers.

In 2025, with euro area rates around 3.5% and industrial electricity averaging €0.22/kWh, these buyers push for better financing, longer warranties, or energy-efficient models to reduce lifecycle costs.

- SME capex pressure

- Focus on TCO: purchase + energy

- 2025: ~3.5% rates, €0.22/kWh energy

- Leverage: finance, warranties, efficiency

Information Symmetry and Market Transparency

Customers now use public benchmarks and component price indices (e.g., DRAM spot prices down 18% in 2025) to infer 2CRSI’s manufacturing margins, shrinking information asymmetry and weakening the firm’s unilateral pricing power.

Buyers routinely demand line-item cost breakdowns for custom engineering, citing market component markups typically 10–25%, forcing 2CRSI to justify any premium or risk losing bids.

- Benchmark access up; DRAM −18% (2025)

- Component markups usually 10–25%

- Buyers ask for BOM-level cost justifications

Hyperscalers consolidate to 60% by 2025—price cuts squeeze commodity margins; AI servers hold premium

Large cloud players (40–55% demand) drive price cuts (15–30% discounts) and consolidate to ~60% hyperscale by 2025, squeezing margins; bespoke AI/edge servers keep 15–25% gross margins vs 5–12% commodity, limiting buyer leverage; standardized lines face low switching costs (68% buyers price-focused), forcing €7.2m R&D and richer SLAs; DRAM −18% (2025) raises BOM scrutiny and demand for financing/warranties.

| Metric | Value |

|---|---|

| Hyperscale share (2025) | ~60% |

| Cloud demand | 40–55% |

| Discounts on racks | 15–30% |

| AI server margins | 15–25% |

| Commodity margins | 5–12% |

| DRAM spot (2025) | −18% |

| 2CRSI R&D (2024) | €7.2m |

Preview Before You Purchase

2CRSI Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for 2CRSi you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

2CRSI faces mixed pressures: moderate supplier leverage for specialized components, strong buyer demands for cost and customization, and growing rivalry in HPC and edge servers—while barriers to entry and substitutes exert variable threat levels. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore 2CRSI’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Tier 1 Semiconductor Manufacturers

The primary components for 2CRSI servers—GPUs and CPUs—are concentrated among Nvidia, AMD, and Intel, which controlled roughly 85% of AI-capable GPU/CPU market share in 2025; their specialized silicon and constrained wafer capacity give them major pricing power. 2CRSI is effectively a price taker as suppliers allocate supply to large cloud and hyperscaler customers, with spot GPU prices up ~30% year-over-year in 2025, pressuring margins.

Specialized Component Scarcity

Beyond CPUs, 2CRSI depends on specialized cooling and high-speed networking parts—often custom or from niche suppliers—giving vendors leverage; a 2024 supply-chain survey showed 42% of data‑center component shortages were in cooling/networking.

Disruptions can delay deliveries by 6–12 weeks and raise component costs 8–15%, so 2CRSI needs multi‑year contracts and strategic partnerships to secure parts for its bespoke servers.

Impact of Proprietary Technology Moats

Suppliers of proprietary software and firmware in 2CRSI’s storage and server stacks hold high bargaining power, able to set licensing fees and update cadences that shape 2CRSI’s roadmap; in 2025 enterprise AI software license CAGR hit ~22%, pushing vendor leverage.

These partners can force recurring royalties and mandatory upgrades, raising gross margin pressure—2CRSI’s gross margin sensitivity to COGS swings could exceed 200–300 bps if license costs rise 10%.

By 2026, as integrated AI stacks (inference+management) become standard, dependency on specialized vendors increases procurement risk and operating cost volatility, making supplier relationships a strategic constraint for 2CRSI.

Raw Material Price Volatility

In 2025, 2CRSI faces raw material price volatility as rare earths and high-grade copper—key for high-performance servers—are constrained by geopolitics and green-energy demand; copper jumped ~25% in 2024 and select rare earths rose 30–50% year-on-year.

Suppliers wield high bargaining power: limited producers and tight markets let them pass costs to 2CRSI with little negotiation room, squeezing margins and forcing price-adjustments or redesigns.

- Copper +25% in 2024

- Rare earths +30–50% YoY

- Green-energy demand ups competition for minerals

- Limited supplier base → low negotiation leverage

Switching Costs for Engineering Integration

Once 2CRSI integrates a supplier's architecture into custom servers, switching costs become prohibitive—redesigning motherboards and thermal systems demands large R&D outlays and months of validation, often 6–18 months and €1–3M per platform based on industry benchmarks.

This technical lock-in boosts supplier leverage in renewals and price talks, effectively raising supplier bargaining power and risking 3–7% margin compression if prices rise.

- 6–18 months redesign time

- €1–3M typical R&D cost

- 3–7% potential margin hit

Suppliers’ dominance spikes costs—multi‑year contracts needed to protect 2CRSI margins

Suppliers hold high bargaining power: Nvidia/AMD/Intel ~85% share in AI-capable silicon (2025), spot GPU prices +30% YoY, copper +25% (2024), rare earths +30–50% YoY; switching costs 6–18 months and €1–3M per platform, causing 3–7% potential margin hit—2CRSI must use multi-year contracts and partnerships to mitigate supply-driven cost and timing risk.

| Metric | Value |

|---|---|

| AI silicon share (2025) | ~85% |

| Spot GPU price change (2025 YoY) | +30% |

| Copper (2024) | +25% |

| Rare earths YoY | +30–50% |

| Redesign time | 6–18 months |

| R&D cost/platform | €1–3M |

| Potential margin hit | 3–7% |

What is included in the product

Tailored Porter’s Five Forces analysis for 2CRSi that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, plus disruptive risks and strategic levers to protect market share and profitability.

Clear, one-sheet Porter's Five Forces for 2CRSI—instantly spot competitive pressures and make faster strategic decisions.

Customers Bargaining Power

Concentration of Hyperscale Buyers

Large cloud providers and mega data centers account for roughly 40–55% of enterprise server demand and can push hard on price; their volume buys let them extract discounts of 15–30% on rack-scale orders, squeezing 2CRSI margins. These buyers run formal RFPs and reverse auctions, forcing 2CRSI to compete on cost and customization to win multi‑year deals. By end‑2025, further consolidation—top 5 owners controlling an estimated 60% of hyperscale capacity—amplifies institutional bargaining power and pricing pressure on vendors like 2CRSI.

Demand for Customization as a Leverage Point

2CRSI’s bespoke, high-performance servers for AI and edge computing reduce customers’ price leverage: buyers with specific technical specs face few substitutes, so they can’t easily push down prices. In 2025 the AI server market’s custom segment grew ~18% YoY, letting niche vendors hold ~15–25% gross margins versus 5–12% for commodity OEMs. Large-volume buyers still exert volume power, but customization narrows that gap.

Low Switching Costs for Standardized Hardware

For 2CRSI’s standardized server and storage lines, switching costs are low: studies show 68% of enterprise buyers prioritize price and performance-per-watt over vendor lock-in, so a competitor offering similar efficiency at 5–15% lower price can capture next-cycle orders. This forces 2CRSI to raise R&D (it spent €7.2m in 2024) and expand after-sales SLAs to retain customers and protect margins.

Price Sensitivity in the Mid-Market Segment

Small and mid-sized enterprises (SMEs) and research labs face tight capex limits and prioritize total cost of ownership—upfront price plus energy and maintenance—when buying 2CRSI servers.

In 2025, with euro area rates around 3.5% and industrial electricity averaging €0.22/kWh, these buyers push for better financing, longer warranties, or energy-efficient models to reduce lifecycle costs.

- SME capex pressure

- Focus on TCO: purchase + energy

- 2025: ~3.5% rates, €0.22/kWh energy

- Leverage: finance, warranties, efficiency

Information Symmetry and Market Transparency

Customers now use public benchmarks and component price indices (e.g., DRAM spot prices down 18% in 2025) to infer 2CRSI’s manufacturing margins, shrinking information asymmetry and weakening the firm’s unilateral pricing power.

Buyers routinely demand line-item cost breakdowns for custom engineering, citing market component markups typically 10–25%, forcing 2CRSI to justify any premium or risk losing bids.

- Benchmark access up; DRAM −18% (2025)

- Component markups usually 10–25%

- Buyers ask for BOM-level cost justifications

Hyperscalers consolidate to 60% by 2025—price cuts squeeze commodity margins; AI servers hold premium

Large cloud players (40–55% demand) drive price cuts (15–30% discounts) and consolidate to ~60% hyperscale by 2025, squeezing margins; bespoke AI/edge servers keep 15–25% gross margins vs 5–12% commodity, limiting buyer leverage; standardized lines face low switching costs (68% buyers price-focused), forcing €7.2m R&D and richer SLAs; DRAM −18% (2025) raises BOM scrutiny and demand for financing/warranties.

| Metric | Value |

|---|---|

| Hyperscale share (2025) | ~60% |

| Cloud demand | 40–55% |

| Discounts on racks | 15–30% |

| AI server margins | 15–25% |

| Commodity margins | 5–12% |

| DRAM spot (2025) | −18% |

| 2CRSI R&D (2024) | €7.2m |

Preview Before You Purchase

2CRSI Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for 2CRSi you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to use.