Dassault Systemes Boston Consulting Group Matrix

See the Bigger Picture

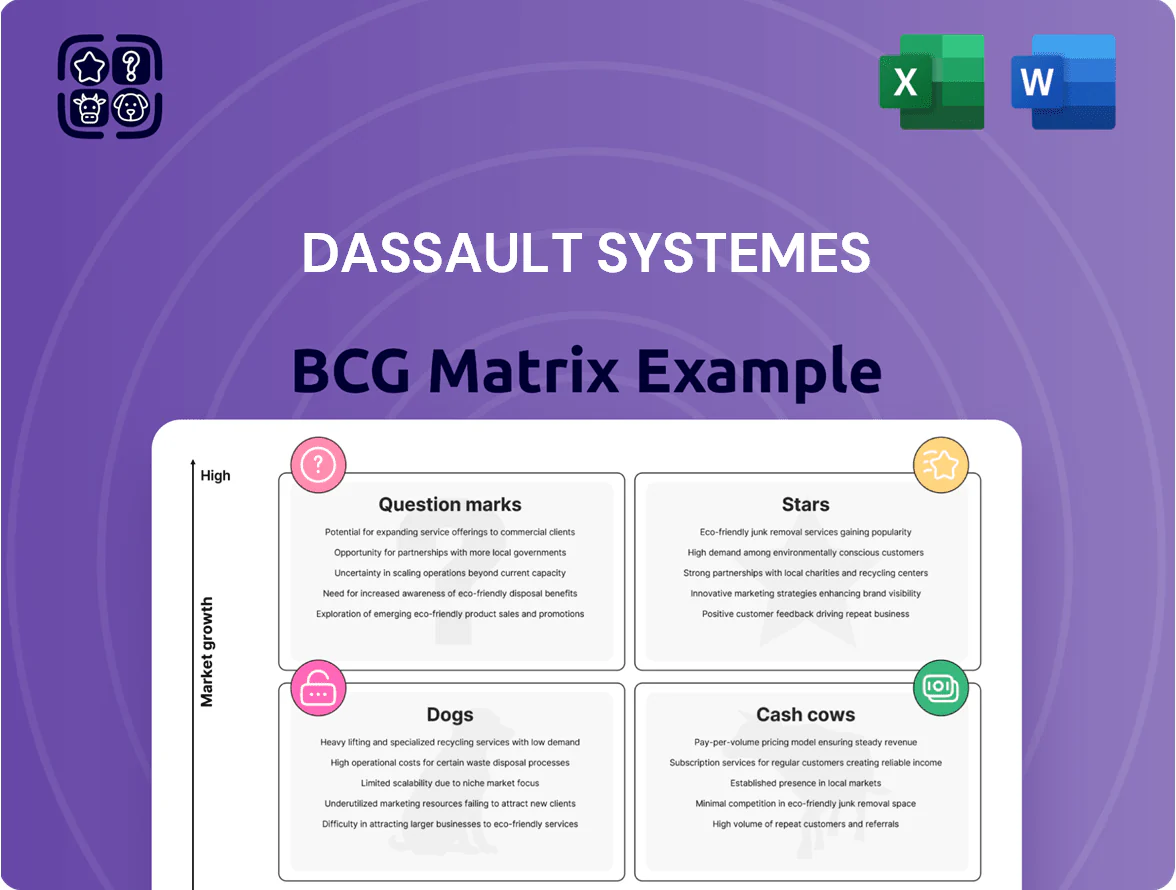

Dassault Systèmes’ BCG Matrix preview highlights how its product portfolio maps across market growth and relative share, hinting at which offerings are Stars, Cash Cows, Question Marks, or Dogs and what strategic moves may be warranted; this snapshot is ideal for a quick read but not a substitute for deep analysis. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel deliverables that translate insights into actionable investment and product decisions.

Stars

3DEXPERIENCE Cloud Platform

3DEXPERIENCE Cloud is Dassault Systèmes’ star: FY2025 cloud revenue rose 32% year-over-year, driving group cloud revenue to roughly €2.9bn and pushing ARR toward €3.5bn by end-2025.

The platform gained share as industries digitize, offering integrated design, simulation, and collaboration across PLM workflows—helping win deals in aerospace, automotive, and life sciences.

High growth requires heavy capex and OPEX for cloud infra and security; FY2025 R&D plus cloud spend climbed ~18% to support scale.

Despite high cash burn to scale, 3DEXPERIENCE Cloud is central to Dassault’s shift to SaaS, underpinning long-term recurring revenue and margin expansion.

SIMULIA Simulation Software

SIMULIA holds a top share in the specialized simulation market (~28% in 2024 according to IDC), with that segment growing ~11% CAGR through 2025 as firms cut physical prototypes.

In 2025, AI-driven generative design features drove new aerospace and high-tech deals, lifting SIMULIA-related revenue growth to ~16% YoY and increasing bookings in digital twin projects.

High revenue masks heavy R&D spend—estimated >12% of SIMULIA revenue—needed for advanced physics solvers and automation, keeping it a Star in the BCG matrix.

SIMULIA is core to Dassault Systèmes’ value: it enables high-value virtual twin experiences that differentiate the company from traditional CAD-only vendors.

Industrial Innovation Segment

Industrial Innovation Segment, led by ENOVIA and DELMIA, grew 6% in 2025 and holds a top position in the global PLM (product lifecycle management) market, with Dassault Systèmes’ PLM revenues up 5.8% to €4.9bn in FY2025.

It links design to manufacturing across the value chain, dominating transportation and mobility where DELMIA/ENOVIA deployments account for ~28% of segment billings.

Continued promotion and global placement are needed to counter aggressive industrial-software rivals like Siemens and PTC, preserving market share.

As these markets mature, the segment’s high share and steady growth set ENOVIA/DELMIA to become future cash cows for Dassault Systèmes.

Aerospace and Defense Solutions

Dassault Systèmes holds near-monopoly leadership in aerospace and defense, with sector software revenue up 9% in Q4 2025, driven by demand for specialized Industry Solution Experiences for next-gen aircraft and defense systems.

Rapid shift to sovereign AI and sustainable aviation forces heavy reinvestment so Dassault stays first-to-market with advanced virtual twins used by major global OEMs, maintaining pricing power and high margins.

- Q4 2025 software growth: 9%

- Near-monopolistic market position

- High reinvestment for sovereign AI, sustainable aviation

- Virtual twins prioritized by major OEMs

Subscription-Based Software Revenue

The shift from perpetual licenses to subscription drove a high-growth, high-share revenue stream for Dassault Systèmes, rising 11% in 2025 and contributing roughly 62% of software revenue, marking it as a Star in the BCG matrix because it redefines value capture in an expanding PLM and 3D software market.

It currently consumes cash as upfront payments convert to recurring cycles—CAPEX-to-OPEX timing—yet subscription ARR growth (up ~11%) shows rapid adoption and is becoming the dominant delivery model.

Sustaining subscription momentum is critical to meet long-term targets: stabilize cash flow conversion, improve gross margin over time, and hit 2026 fiscal goals tied to recurring revenue scale.

- 2025 subscription growth: +11%

- Share of software revenue: ~62%

- Status: Star—high growth, high market share

- Risk: short-term cash consumption; reward: stabilized recurring cash

Dassault: Cloud & SIMULIA Drive FY25 Growth — Cloud €2.9bn, Subscriptions 62%

3DEXPERIENCE Cloud, SIMULIA, and subscription PLM are Stars: FY2025 cloud revenue +32% to ~€2.9bn, SIMULIA ~16% YoY growth, PLM revenues €4.9bn (+5.8%), subscriptions ~62% of software revs (+11%). Heavy R&D/cloud spend (R&D+cloud +18%) keeps cash burn high but secures recurring ARR and market share.

| Metric | 2025 |

|---|---|

| Cloud rev | €2.9bn (+32%) |

| SIMULIA growth | +16% YoY |

| PLM rev | €4.9bn (+5.8%) |

| Subscriptions | 62% (+11%) |

| R&D+cloud spend | +18% |

What is included in the product

Comprehensive BCG Matrix review of Dassault Systèmes’ portfolio with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Dassault Systèmes business unit in a BCG quadrant for fast strategic prioritization.

Cash Cows

CATIA Design Software

CATIA remains Dassault Systèmes’ dominant cash cow, driving most revenue with an estimated 65% share of global aerospace and automotive OEM CAD seats as of Q4 2025; the product operates in a mature market growing ~5% annually and sustains operating margins above 40%. Low incremental CAPEX for this legacy platform frees substantial free cash flow—roughly €1.2–1.5 billion annually in recent years—to fund R&D in AI and cloud offerings.

SOLIDWORKS Mainstream Innovation

SOLIDWORKS, serving mainstream engineering and SMBs, generated about 24% of Dassault Systèmes’ 2025 total revenue (roughly €2.0–2.2 billion of €9.0 billion), driven by a very high installed base and steady renewals.

In 2025 it stayed a stable market leader, prioritizing user-requested enhancements over risky expansions, maintaining strong ARR and low churn under 8%.

Promotion and placement costs remain low versus revenue, making SOLIDWORKS a reliable cash source that funds 3DEXPERIENCE development for smaller enterprises.

ENOVIA Collaborative Management

ENOVIA Collaborative Management holds a leading share in the mature PLM market—estimated >25% global share among large OEMs in 2024—and provides data management and collaboration for multi-year industrial programs.

Growth has stabilized near low-single digits, yet ENOVIA yields high operating margins (circa 30% in FY2024) because it is deeply embedded in client workflows.

Minimal incremental infrastructure spend is needed, so ENOVIA reliably funds dividends and debt service, contributing steady free cash flow—roughly €400–500M annual EBIT contribution in 2024.

It remains a core, cash-generating asset within Dassault Systèmes’ portfolio, supporting balance-sheet strength and recurring revenue stability.

Recurring Maintenance Revenue

Maintenance and support for Dassault Systèmes’ legacy installed base is a high-share, low-growth cash cow that delivered steady recurring revenue in 2025, sustaining margins while cloud transition accelerated.

This stable stream underwrote R&D and cloud investments, acting as a financial safety net and helping the company keep a cash conversion rate near 82% in 2025.

- High-share, low-growth unit

- Resilient recurring revenue in 2025

- Funds cloud and high-growth bets

- Supports ~82% cash conversion

Industrial Equipment Sector Solutions

Dassault Systèmes’ Industrial Equipment solutions are a Cash Cow: in 2025 they held a high global market share in a mature market, delivering predictable, high cash inflows with low incremental sales investment.

These products’ strong competitive edge supported stable revenue in 2025, offsetting cyclical downturns in automotive and funding administrative costs and strategic R&D.

- High market share in 2025; steady revenue

- Low reinvestment need; high cash conversion

- Offsets automotive volatility

- Funds admin and R&D

Dassault Systèmes’ 2025 cash engines: CATIA, SOLIDWORKS, ENOVIA fuel high-margin FCF

CATIA, SOLIDWORKS, ENOVIA, maintenance/support, and Industrial Equipment were Dassault Systèmes cash cows in 2025, delivering ~€1.2–1.5B FCF from CATIA, ~€2.0–2.2B revenue from SOLIDWORKS (24% of €9.0B), ENOVIA ~€400–500M EBIT, ~82% cash conversion, high margins (CATIA >40%, ENOVIA ~30%), low reinvestment needs funding cloud/AI R&D.

| Product | 2025 KPI | Role |

|---|---|---|

| CATIA | €1.2–1.5B FCF; >40% OM | Primary cash generator |

| SOLIDWORKS | €2.0–2.2B rev; 24% of rev | Stable recurring cash |

| ENOVIA | €400–500M EBIT; ~30% OM | Embedded PLM cash |

| Maintenance | ~82% cash conversion | Low-growth recurring |

What You’re Viewing Is Included

Dassault Systemes BCG Matrix

The file you’re previewing on this page is the exact Dassault Systèmes BCG Matrix report you’ll receive after purchase — fully formatted, free of watermarks, and ready for presentation or analysis. This preview mirrors the final deliverable, crafted with strategic precision and up-to-date market insights, so there are no surprises when it arrives in your inbox. Once bought, the editable, print-ready document is immediately available for use in planning, pitching, or client work.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Dassault Systèmes’ BCG Matrix preview highlights how its product portfolio maps across market growth and relative share, hinting at which offerings are Stars, Cash Cows, Question Marks, or Dogs and what strategic moves may be warranted; this snapshot is ideal for a quick read but not a substitute for deep analysis. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel deliverables that translate insights into actionable investment and product decisions.

Stars

3DEXPERIENCE Cloud Platform

3DEXPERIENCE Cloud is Dassault Systèmes’ star: FY2025 cloud revenue rose 32% year-over-year, driving group cloud revenue to roughly €2.9bn and pushing ARR toward €3.5bn by end-2025.

The platform gained share as industries digitize, offering integrated design, simulation, and collaboration across PLM workflows—helping win deals in aerospace, automotive, and life sciences.

High growth requires heavy capex and OPEX for cloud infra and security; FY2025 R&D plus cloud spend climbed ~18% to support scale.

Despite high cash burn to scale, 3DEXPERIENCE Cloud is central to Dassault’s shift to SaaS, underpinning long-term recurring revenue and margin expansion.

SIMULIA Simulation Software

SIMULIA holds a top share in the specialized simulation market (~28% in 2024 according to IDC), with that segment growing ~11% CAGR through 2025 as firms cut physical prototypes.

In 2025, AI-driven generative design features drove new aerospace and high-tech deals, lifting SIMULIA-related revenue growth to ~16% YoY and increasing bookings in digital twin projects.

High revenue masks heavy R&D spend—estimated >12% of SIMULIA revenue—needed for advanced physics solvers and automation, keeping it a Star in the BCG matrix.

SIMULIA is core to Dassault Systèmes’ value: it enables high-value virtual twin experiences that differentiate the company from traditional CAD-only vendors.

Industrial Innovation Segment

Industrial Innovation Segment, led by ENOVIA and DELMIA, grew 6% in 2025 and holds a top position in the global PLM (product lifecycle management) market, with Dassault Systèmes’ PLM revenues up 5.8% to €4.9bn in FY2025.

It links design to manufacturing across the value chain, dominating transportation and mobility where DELMIA/ENOVIA deployments account for ~28% of segment billings.

Continued promotion and global placement are needed to counter aggressive industrial-software rivals like Siemens and PTC, preserving market share.

As these markets mature, the segment’s high share and steady growth set ENOVIA/DELMIA to become future cash cows for Dassault Systèmes.

Aerospace and Defense Solutions

Dassault Systèmes holds near-monopoly leadership in aerospace and defense, with sector software revenue up 9% in Q4 2025, driven by demand for specialized Industry Solution Experiences for next-gen aircraft and defense systems.

Rapid shift to sovereign AI and sustainable aviation forces heavy reinvestment so Dassault stays first-to-market with advanced virtual twins used by major global OEMs, maintaining pricing power and high margins.

- Q4 2025 software growth: 9%

- Near-monopolistic market position

- High reinvestment for sovereign AI, sustainable aviation

- Virtual twins prioritized by major OEMs

Subscription-Based Software Revenue

The shift from perpetual licenses to subscription drove a high-growth, high-share revenue stream for Dassault Systèmes, rising 11% in 2025 and contributing roughly 62% of software revenue, marking it as a Star in the BCG matrix because it redefines value capture in an expanding PLM and 3D software market.

It currently consumes cash as upfront payments convert to recurring cycles—CAPEX-to-OPEX timing—yet subscription ARR growth (up ~11%) shows rapid adoption and is becoming the dominant delivery model.

Sustaining subscription momentum is critical to meet long-term targets: stabilize cash flow conversion, improve gross margin over time, and hit 2026 fiscal goals tied to recurring revenue scale.

- 2025 subscription growth: +11%

- Share of software revenue: ~62%

- Status: Star—high growth, high market share

- Risk: short-term cash consumption; reward: stabilized recurring cash

Dassault: Cloud & SIMULIA Drive FY25 Growth — Cloud €2.9bn, Subscriptions 62%

3DEXPERIENCE Cloud, SIMULIA, and subscription PLM are Stars: FY2025 cloud revenue +32% to ~€2.9bn, SIMULIA ~16% YoY growth, PLM revenues €4.9bn (+5.8%), subscriptions ~62% of software revs (+11%). Heavy R&D/cloud spend (R&D+cloud +18%) keeps cash burn high but secures recurring ARR and market share.

| Metric | 2025 |

|---|---|

| Cloud rev | €2.9bn (+32%) |

| SIMULIA growth | +16% YoY |

| PLM rev | €4.9bn (+5.8%) |

| Subscriptions | 62% (+11%) |

| R&D+cloud spend | +18% |

What is included in the product

Comprehensive BCG Matrix review of Dassault Systèmes’ portfolio with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Dassault Systèmes business unit in a BCG quadrant for fast strategic prioritization.

Cash Cows

CATIA Design Software

CATIA remains Dassault Systèmes’ dominant cash cow, driving most revenue with an estimated 65% share of global aerospace and automotive OEM CAD seats as of Q4 2025; the product operates in a mature market growing ~5% annually and sustains operating margins above 40%. Low incremental CAPEX for this legacy platform frees substantial free cash flow—roughly €1.2–1.5 billion annually in recent years—to fund R&D in AI and cloud offerings.

SOLIDWORKS Mainstream Innovation

SOLIDWORKS, serving mainstream engineering and SMBs, generated about 24% of Dassault Systèmes’ 2025 total revenue (roughly €2.0–2.2 billion of €9.0 billion), driven by a very high installed base and steady renewals.

In 2025 it stayed a stable market leader, prioritizing user-requested enhancements over risky expansions, maintaining strong ARR and low churn under 8%.

Promotion and placement costs remain low versus revenue, making SOLIDWORKS a reliable cash source that funds 3DEXPERIENCE development for smaller enterprises.

ENOVIA Collaborative Management

ENOVIA Collaborative Management holds a leading share in the mature PLM market—estimated >25% global share among large OEMs in 2024—and provides data management and collaboration for multi-year industrial programs.

Growth has stabilized near low-single digits, yet ENOVIA yields high operating margins (circa 30% in FY2024) because it is deeply embedded in client workflows.

Minimal incremental infrastructure spend is needed, so ENOVIA reliably funds dividends and debt service, contributing steady free cash flow—roughly €400–500M annual EBIT contribution in 2024.

It remains a core, cash-generating asset within Dassault Systèmes’ portfolio, supporting balance-sheet strength and recurring revenue stability.

Recurring Maintenance Revenue

Maintenance and support for Dassault Systèmes’ legacy installed base is a high-share, low-growth cash cow that delivered steady recurring revenue in 2025, sustaining margins while cloud transition accelerated.

This stable stream underwrote R&D and cloud investments, acting as a financial safety net and helping the company keep a cash conversion rate near 82% in 2025.

- High-share, low-growth unit

- Resilient recurring revenue in 2025

- Funds cloud and high-growth bets

- Supports ~82% cash conversion

Industrial Equipment Sector Solutions

Dassault Systèmes’ Industrial Equipment solutions are a Cash Cow: in 2025 they held a high global market share in a mature market, delivering predictable, high cash inflows with low incremental sales investment.

These products’ strong competitive edge supported stable revenue in 2025, offsetting cyclical downturns in automotive and funding administrative costs and strategic R&D.

- High market share in 2025; steady revenue

- Low reinvestment need; high cash conversion

- Offsets automotive volatility

- Funds admin and R&D

Dassault Systèmes’ 2025 cash engines: CATIA, SOLIDWORKS, ENOVIA fuel high-margin FCF

CATIA, SOLIDWORKS, ENOVIA, maintenance/support, and Industrial Equipment were Dassault Systèmes cash cows in 2025, delivering ~€1.2–1.5B FCF from CATIA, ~€2.0–2.2B revenue from SOLIDWORKS (24% of €9.0B), ENOVIA ~€400–500M EBIT, ~82% cash conversion, high margins (CATIA >40%, ENOVIA ~30%), low reinvestment needs funding cloud/AI R&D.

| Product | 2025 KPI | Role |

|---|---|---|

| CATIA | €1.2–1.5B FCF; >40% OM | Primary cash generator |

| SOLIDWORKS | €2.0–2.2B rev; 24% of rev | Stable recurring cash |

| ENOVIA | €400–500M EBIT; ~30% OM | Embedded PLM cash |

| Maintenance | ~82% cash conversion | Low-growth recurring |

What You’re Viewing Is Included

Dassault Systemes BCG Matrix

The file you’re previewing on this page is the exact Dassault Systèmes BCG Matrix report you’ll receive after purchase — fully formatted, free of watermarks, and ready for presentation or analysis. This preview mirrors the final deliverable, crafted with strategic precision and up-to-date market insights, so there are no surprises when it arrives in your inbox. Once bought, the editable, print-ready document is immediately available for use in planning, pitching, or client work.