Dassault Systemes Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

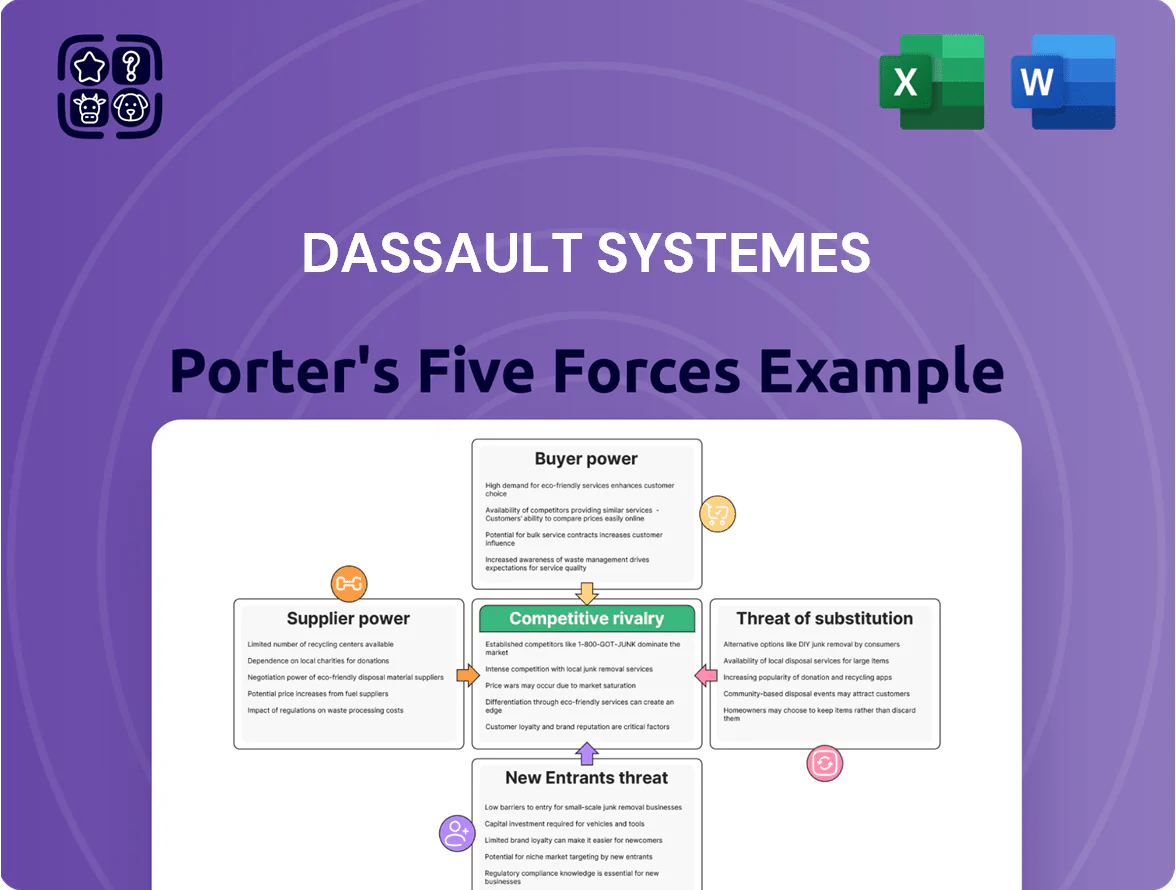

Dassault Systèmes faces intense rivalry from legacy PLM vendors and agile SaaS entrants, while high switching costs and broad partner ecosystems moderate buyer leverage; supplier power and substitute threats vary across industries served.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dassault Systèmes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

As Dassault Systèmes shifts 3DEXPERIENCE to cloud, reliance on hyperscalers AWS, Microsoft Azure, and Google Cloud raises supplier power because of specialized compute for simulation and 3D; hyperscalers held ~65% global cloud market in 2024 (Gartner).

Dassault’s scale—€5.8B revenue in FY2024—and multi-cloud deals let it negotiate better prices and SLAs than smaller ISVs, lowering supplier risk.

By late 2025 Dassault invested in European sovereign cloud projects (e.g., partnerships with OVHcloud and Atos), cutting US-provider dependency and regulatory exposure.

Scarcity of Specialized Software Engineering Talent

The pool of engineers skilled in multi-physics simulation, AI, and geometric kernels is very tight; global demand outpaces supply and raises supplier power over pay and remote-work terms. These specialists are key human-capital suppliers for Dassault Systèmes, pushing salary premiums—industry surveys showed 15–30% higher total compensation in 2024 for such skills. Dassault counters with heavy academic partnerships (over 200 university collaborations by 2025) to pipeline talent into its proprietary ecosystems, helping moderate R&D cost inflation while securing expertise.

Dependency on Specialized Hardware Vendors

High-end engineering apps need specialized hardware like professional GPUs and VR/AR peripherals from suppliers such as NVIDIA, which held ~80% data center GPU market share in 2024, giving suppliers pricing and roadmap leverage over Dassault Systèmes’ software performance; Dassault counters this by forming deep technical alliances and joint engineering (co-optimization agreements signed regularly, e.g., NVIDIA and Dassault collaborations in 2023–2025), creating mutual dependency that tempers pure supplier bargaining power.

Licensing of Third-Party Geometric Kernels

Dassault owns the CGM kernel but some integrated products still used third-party geometric solvers and translators, giving niche suppliers temporary leverage—single-source math solvers can force licensing fees or slow integrations.

Since 2015 Dassault has acquired or developed many such components (example: 2014 Spatial assets earlier, 2017 acquisitions), cutting estimated licensing expense by an estimated mid-single-digit percent of R&D annually and lowering supplier disruption risk.

Strategic Data and Content Partners

Suppliers of niche industry data—like aerospace material properties or life-science clinical datasets—wield high bargaining power because substitutes are rare and validation is costly; Medidata’s 2019 acquisition by Dassault Systèmes for $5.8B (closed 2020) exemplifies how Dassault internalized such critical data sources to reduce supplier leverage.

Dassault: €5.8B scale mitigates supplier power vs hyperscalers & NVIDIA dominance

Supplier power is moderate: hyperscalers held ~65% cloud market (Gartner 2024) and NVIDIA ~80% data‑center GPU share (2024), raising leverage; Dassault’s €5.8B FY2024 scale, multi‑cloud deals, European cloud partnerships (OVHcloud/Atos by 2025), 200+ university ties, Medidata acquisition (2020, $5.8B) and CGM ownership cut risks and licensing costs (mid single‑digit % R&D savings).

| Metric | Value |

|---|---|

| FY2024 revenue | €5.8B |

| Cloud market (hyperscalers) | ~65% (2024) |

| Data‑center GPU share | ~80% (NVIDIA, 2024) |

| Univ. partnerships | 200+ (2025) |

| Medidata deal | $5.8B (2020) |

| R&D licensing saving | mid single‑digit % |

What is included in the product

Tailored exclusively for Dassault Systèmes, this Porter's Five Forces analysis uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats to evaluate pricing power and strategic resilience.

Compact, one-sheet Porter's Five Forces for Dassault Systèmes—clarify competitive pressures quickly and tailor threat levels as M&A, PLM shifts, or cloud adoption evolve.

Customers Bargaining Power

High Switching Costs for Enterprise Clients

Large aerospace and automotive clients face huge costs and risks switching PLM providers—implementing Dassault Systèmes’ 3DEXPERIENCE across design-to-manufacturing creates deep lock-in; vendors estimate migration can cost tens to hundreds of millions and take 12–36 months. This structural dependency cuts buyers’ leverage on prices, letting Dassault raise subscription and maintenance fees with limited churn; by end-2025, customer stickiness remains its strongest defense in core markets.

Consolidation of Global Industrial Giants

Consolidation in aerospace and defense concentrates revenue: in 2024 Boeing and Airbus accounted for an estimated 18–25% of Dassault Systèmes’ industry bookings, giving megacustomers scale to demand tailored features and discounts.

Those buyers exert strong bargaining power via volume and long procurement cycles, often pushing for integration with supplier PLM ecosystems.

Dassault reduces dependence by expanding into Life Sciences and Infrastructure; by FY2024, non-aerospace sectors made up roughly 46% of revenue, limiting single-group financial leverage.

Price Sensitivity in the SMB and Mid-Market

SMB and mid-market buyers show high price sensitivity and lower switching costs than enterprises; 2024 surveys suggest ~62% of SMBs prioritize subscription price when choosing CAD/PLM tools.

Many evaluate SolidWorks against lower-cost or cloud-native rivals (Onshape, Fusion 360) offering simpler subscriptions; cloud CAD growth hit ~28% YoY in 2023–24.

Dassault introduced flexible licensing and modular cloud packages in 2022–24, enabling tiered capture of SMB spend while preserving premium enterprise pricing.

Demand for Open Standards and Interoperability

Modern customers push for open standards and interoperability to avoid vendor lock-in, raising buyer power as platforms must offer APIs and join standards bodies; 2024 surveys show 68% of industrial software buyers rank interoperability as a top-three purchase driver.

Dassault Systemes responds by joining standards initiatives and exposing APIs but positions 3DEXPERIENCE as the orchestration hub, turning interoperability demand into a lock-in advantage—3DEXPERIENCE-related revenue grew ~12% in FY2024, supporting this strategy.

- 68% of buyers prioritize interoperability (2024 survey)

- 3DEXPERIENCE revenue +12% FY2024

- APIs and standards reduce switching for core workflows

Influence of Sustainability and Regulatory Compliance

Corporate buyers now favor software that supports strict ESG targets and carbon reporting; 72% of Fortune 500 firms had formal Scope 3 reduction targets by 2024, increasing demand for life-cycle assessment (LCA) and material-selection features.

That shift boosts customer bargaining power to demand sustainability features, so Dassault Systèmes embedded environmental-impact simulation into CAD and PLM workflows (2023–2025 releases), preserving premium pricing and lowering churn to green-tech rivals.

- 72% Fortune 500 with Scope 3 targets (2024)

- Dassault added LCA/sustainability modules in 2023–2025

- Feature integration reduces switch to niche green vendors

Dassault: Pricing power with big clients; 3DEXPERIENCE +12%, ESG & APIs curb churn

Customers have moderate-to-high bargaining power: large aerospace/auto clients face high switching costs (migration 12–36 months, $10M–$200M), giving Dassault pricing power; SMBs remain price-sensitive (≈62% prioritize price). 2024: 3DEXPERIENCE revenue +12%, non-aero revenue ~46%. Interoperability (68% buyers) and ESG (72% Fortune 500 Scope 3) drive feature demands, but integrated LCA and APIs limit churn.

| Metric | Value (2024) |

|---|---|

| 3DEXPERIENCE rev growth | +12% |

| Non-aero revenue | ≈46% |

| SMBs price priority | ≈62% |

| Interoperability priority | 68% |

| Fortune 500 Scope 3 | 72% |

Same Document Delivered

Dassault Systemes Porter's Five Forces Analysis

This preview shows the exact Dassault Systèmes Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples.

The document displayed is the final, professionally formatted analysis covering competitive rivalry, threat of new entrants, supplier and buyer power, and threat of substitutes.

Once you buy, you’ll get instant access to this identical file, ready to download and use for due diligence, strategy, or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Dassault Systèmes faces intense rivalry from legacy PLM vendors and agile SaaS entrants, while high switching costs and broad partner ecosystems moderate buyer leverage; supplier power and substitute threats vary across industries served.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dassault Systèmes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

As Dassault Systèmes shifts 3DEXPERIENCE to cloud, reliance on hyperscalers AWS, Microsoft Azure, and Google Cloud raises supplier power because of specialized compute for simulation and 3D; hyperscalers held ~65% global cloud market in 2024 (Gartner).

Dassault’s scale—€5.8B revenue in FY2024—and multi-cloud deals let it negotiate better prices and SLAs than smaller ISVs, lowering supplier risk.

By late 2025 Dassault invested in European sovereign cloud projects (e.g., partnerships with OVHcloud and Atos), cutting US-provider dependency and regulatory exposure.

Scarcity of Specialized Software Engineering Talent

The pool of engineers skilled in multi-physics simulation, AI, and geometric kernels is very tight; global demand outpaces supply and raises supplier power over pay and remote-work terms. These specialists are key human-capital suppliers for Dassault Systèmes, pushing salary premiums—industry surveys showed 15–30% higher total compensation in 2024 for such skills. Dassault counters with heavy academic partnerships (over 200 university collaborations by 2025) to pipeline talent into its proprietary ecosystems, helping moderate R&D cost inflation while securing expertise.

Dependency on Specialized Hardware Vendors

High-end engineering apps need specialized hardware like professional GPUs and VR/AR peripherals from suppliers such as NVIDIA, which held ~80% data center GPU market share in 2024, giving suppliers pricing and roadmap leverage over Dassault Systèmes’ software performance; Dassault counters this by forming deep technical alliances and joint engineering (co-optimization agreements signed regularly, e.g., NVIDIA and Dassault collaborations in 2023–2025), creating mutual dependency that tempers pure supplier bargaining power.

Licensing of Third-Party Geometric Kernels

Dassault owns the CGM kernel but some integrated products still used third-party geometric solvers and translators, giving niche suppliers temporary leverage—single-source math solvers can force licensing fees or slow integrations.

Since 2015 Dassault has acquired or developed many such components (example: 2014 Spatial assets earlier, 2017 acquisitions), cutting estimated licensing expense by an estimated mid-single-digit percent of R&D annually and lowering supplier disruption risk.

Strategic Data and Content Partners

Suppliers of niche industry data—like aerospace material properties or life-science clinical datasets—wield high bargaining power because substitutes are rare and validation is costly; Medidata’s 2019 acquisition by Dassault Systèmes for $5.8B (closed 2020) exemplifies how Dassault internalized such critical data sources to reduce supplier leverage.

Dassault: €5.8B scale mitigates supplier power vs hyperscalers & NVIDIA dominance

Supplier power is moderate: hyperscalers held ~65% cloud market (Gartner 2024) and NVIDIA ~80% data‑center GPU share (2024), raising leverage; Dassault’s €5.8B FY2024 scale, multi‑cloud deals, European cloud partnerships (OVHcloud/Atos by 2025), 200+ university ties, Medidata acquisition (2020, $5.8B) and CGM ownership cut risks and licensing costs (mid single‑digit % R&D savings).

| Metric | Value |

|---|---|

| FY2024 revenue | €5.8B |

| Cloud market (hyperscalers) | ~65% (2024) |

| Data‑center GPU share | ~80% (NVIDIA, 2024) |

| Univ. partnerships | 200+ (2025) |

| Medidata deal | $5.8B (2020) |

| R&D licensing saving | mid single‑digit % |

What is included in the product

Tailored exclusively for Dassault Systèmes, this Porter's Five Forces analysis uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats to evaluate pricing power and strategic resilience.

Compact, one-sheet Porter's Five Forces for Dassault Systèmes—clarify competitive pressures quickly and tailor threat levels as M&A, PLM shifts, or cloud adoption evolve.

Customers Bargaining Power

High Switching Costs for Enterprise Clients

Large aerospace and automotive clients face huge costs and risks switching PLM providers—implementing Dassault Systèmes’ 3DEXPERIENCE across design-to-manufacturing creates deep lock-in; vendors estimate migration can cost tens to hundreds of millions and take 12–36 months. This structural dependency cuts buyers’ leverage on prices, letting Dassault raise subscription and maintenance fees with limited churn; by end-2025, customer stickiness remains its strongest defense in core markets.

Consolidation of Global Industrial Giants

Consolidation in aerospace and defense concentrates revenue: in 2024 Boeing and Airbus accounted for an estimated 18–25% of Dassault Systèmes’ industry bookings, giving megacustomers scale to demand tailored features and discounts.

Those buyers exert strong bargaining power via volume and long procurement cycles, often pushing for integration with supplier PLM ecosystems.

Dassault reduces dependence by expanding into Life Sciences and Infrastructure; by FY2024, non-aerospace sectors made up roughly 46% of revenue, limiting single-group financial leverage.

Price Sensitivity in the SMB and Mid-Market

SMB and mid-market buyers show high price sensitivity and lower switching costs than enterprises; 2024 surveys suggest ~62% of SMBs prioritize subscription price when choosing CAD/PLM tools.

Many evaluate SolidWorks against lower-cost or cloud-native rivals (Onshape, Fusion 360) offering simpler subscriptions; cloud CAD growth hit ~28% YoY in 2023–24.

Dassault introduced flexible licensing and modular cloud packages in 2022–24, enabling tiered capture of SMB spend while preserving premium enterprise pricing.

Demand for Open Standards and Interoperability

Modern customers push for open standards and interoperability to avoid vendor lock-in, raising buyer power as platforms must offer APIs and join standards bodies; 2024 surveys show 68% of industrial software buyers rank interoperability as a top-three purchase driver.

Dassault Systemes responds by joining standards initiatives and exposing APIs but positions 3DEXPERIENCE as the orchestration hub, turning interoperability demand into a lock-in advantage—3DEXPERIENCE-related revenue grew ~12% in FY2024, supporting this strategy.

- 68% of buyers prioritize interoperability (2024 survey)

- 3DEXPERIENCE revenue +12% FY2024

- APIs and standards reduce switching for core workflows

Influence of Sustainability and Regulatory Compliance

Corporate buyers now favor software that supports strict ESG targets and carbon reporting; 72% of Fortune 500 firms had formal Scope 3 reduction targets by 2024, increasing demand for life-cycle assessment (LCA) and material-selection features.

That shift boosts customer bargaining power to demand sustainability features, so Dassault Systèmes embedded environmental-impact simulation into CAD and PLM workflows (2023–2025 releases), preserving premium pricing and lowering churn to green-tech rivals.

- 72% Fortune 500 with Scope 3 targets (2024)

- Dassault added LCA/sustainability modules in 2023–2025

- Feature integration reduces switch to niche green vendors

Dassault: Pricing power with big clients; 3DEXPERIENCE +12%, ESG & APIs curb churn

Customers have moderate-to-high bargaining power: large aerospace/auto clients face high switching costs (migration 12–36 months, $10M–$200M), giving Dassault pricing power; SMBs remain price-sensitive (≈62% prioritize price). 2024: 3DEXPERIENCE revenue +12%, non-aero revenue ~46%. Interoperability (68% buyers) and ESG (72% Fortune 500 Scope 3) drive feature demands, but integrated LCA and APIs limit churn.

| Metric | Value (2024) |

|---|---|

| 3DEXPERIENCE rev growth | +12% |

| Non-aero revenue | ≈46% |

| SMBs price priority | ≈62% |

| Interoperability priority | 68% |

| Fortune 500 Scope 3 | 72% |

Same Document Delivered

Dassault Systemes Porter's Five Forces Analysis

This preview shows the exact Dassault Systèmes Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no samples.

The document displayed is the final, professionally formatted analysis covering competitive rivalry, threat of new entrants, supplier and buyer power, and threat of substitutes.

Once you buy, you’ll get instant access to this identical file, ready to download and use for due diligence, strategy, or investment decisions.