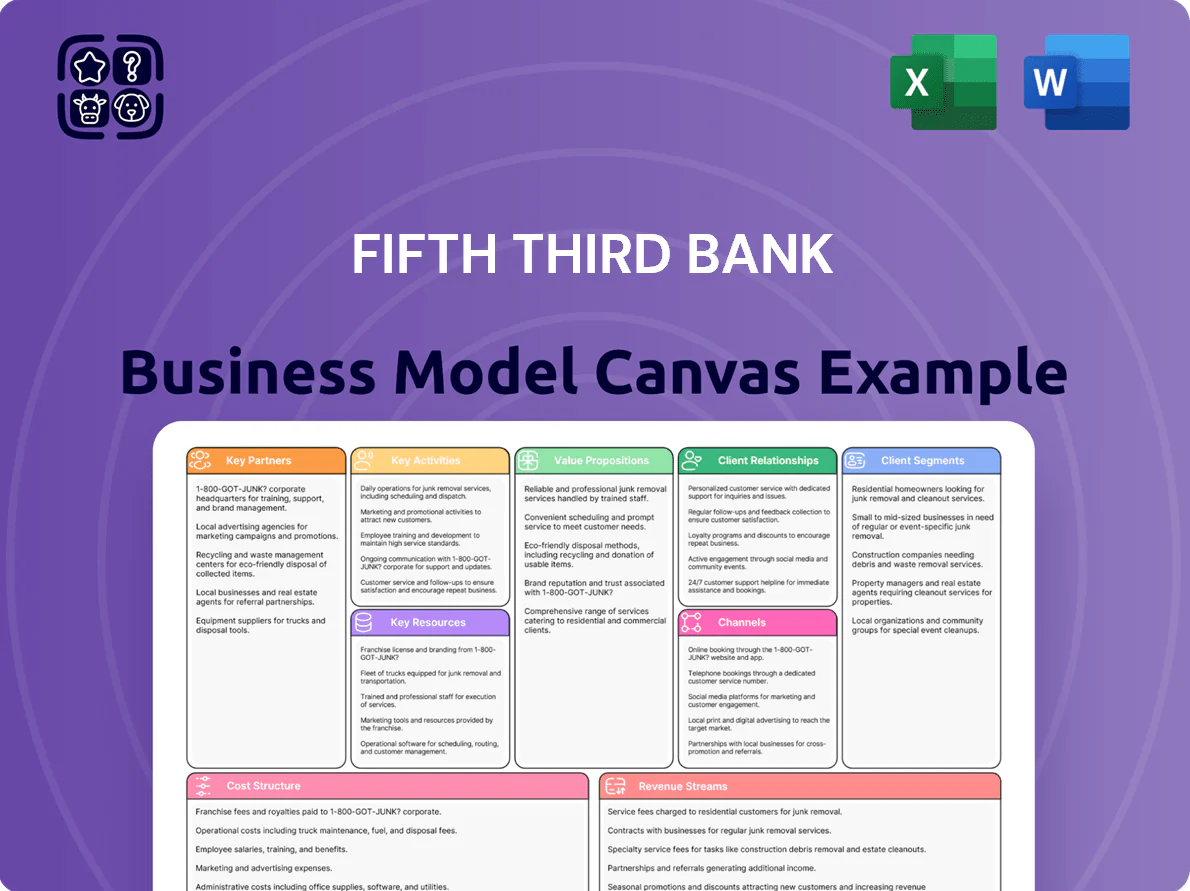

Fifth Third Bank Business Model Canvas

Fifth Third Bank Business Model Canvas: Full 9‑Block Blueprint & Downloadable Tools

Unlock the full strategic blueprint behind Fifth Third Bank’s business model—our in-depth Business Model Canvas reveals how the bank creates customer value, captures revenue, and sustains competitive advantage across retail and commercial segments.

Perfect for investors, advisors, and strategists, the complete canvas includes company-specific insights for all nine blocks plus Word and Excel files ready for benchmarking, presentations, or strategic planning—download to gain actionable clarity.

Partnerships

Fintech and Embedded Payment Partners

The bank partners with fintechs to embed payments into commercial workflows, offering services such as Dividend Finance for point-of-sale lending and NewDominion for healthcare payments; these integrations helped Fifth Third originate over $2.3bn in digital loan volume in 2024, boosting fee income and merchant reach. By outsourcing tech expertise, Fifth Third cuts development time and kept digital transaction growth at ~18% YoY in 2024, preserving its competitive edge.

Technology and Cloud Infrastructure Providers

Fifth Third Bank partners with major cloud providers such as Microsoft Azure and Amazon Web Services to support digital transformation, using their scalable infrastructure for data processing, cybersecurity, and mobile app hosting; as of 2024 the bank reported a 20% YoY increase in digital transactions, underscoring the need for scale. These alliances are critical for 24/7 availability and data protection—outsourced cloud resilience reduces outage risk and helps meet regulatory security standards.

Regulatory and Government Agencies

The bank keeps mandatory ties with the Federal Reserve, the Office of the Comptroller of the Currency (OCC), and the FDIC for compliance with evolving laws; in 2024 Fifth Third reported regulatory capital ratios of CET1 9.7% and Tier 1 leverage 8.2%, reflecting oversight-driven capital targets. These partnerships include quarterly audits, monthly regulatory reporting, and participation in Fed liquidity programs that shaped its $157 billion liquidity buffer in 2024, preserving its charter and public trust.

Community and Non-Profit Organizations

Collaborations with local community and non-profit organizations help Fifth Third Bank meet Community Reinvestment Act (CRA) goals and spur regional growth; in 2024 the bank reported $2.3 billion in community development lending and investments, targeting small business and affordable housing.

These partners surface underserved markets for lending and housing projects, boosting brand presence in core Midwest and Southeast territories and supporting long-term economic health.

- 2024: $2.3B community development lending/investments

- Focus: small business lending, affordable housing, CRA compliance

- Geography: Midwest and Southeast core markets

Third-Party Mortgage and Insurance Servicers

Fifth Third Bank partners with third-party mortgage and insurance servicers to handle loan processing, appraisals, and insurance underwriting, letting the bank support a $148.5 billion loan portfolio (2024 end) while avoiding large fixed staffing increases.

These partners scale operations quickly, cutting per-loan overhead and improving turnaround; in 2024 external servicing reduced cycle times by ~18% for retail mortgages.

- Third-party servicing covers processing, appraisals, underwriting

- Supports $148.5B loan book (2024)

- Reduces per-loan overhead and staffing needs

- Shortened mortgage cycle times ~18% in 2024

Fifth Third Scales Digital Lending: $2.3B Originations, $148.5B Loan Book, ~18% Growth

Fifth Third leverages fintechs, cloud providers (Azure/AWS), regulators (Fed/OCC/FDIC), community orgs, and third-party servicers to scale digital lending, ensure regulatory compliance, meet CRA targets, and trim operational costs; key 2024 metrics: $2.3B digital loan originations, $2.3B community lending, $148.5B loan book, ~18% digital/transaction growth.

| Metric | 2024 |

|---|---|

| Digital loan originations | $2.3B |

| Community lending | $2.3B |

| Loan portfolio | $148.5B |

| Digital growth | ~18% YoY |

What is included in the product

A concise Business Model Canvas for Fifth Third Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and customer relationships aligned with its regional retail, commercial banking, and wealth management strategy.

Condenses Fifth Third Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and boardroom-ready insights.

Activities

Lending and Credit Portfolio Management

Fifth Third Bank originates and manages loans from residential mortgages to $1bn+ commercial credit lines, with total loans held for investment of $114.8 billion as of Q4 2025; rigorous credit analysis and stress testing cut weighted-average default exposure and support net interest income. Ongoing monitoring of borrower performance, collateral valuation, and workout teams keeps nonperforming assets at 0.92% in 2025, helping minimize charge-offs while sustaining yield.

Digital Banking and Platform Development

Fifth Third invests heavily in digital banking, spending about $1.1 billion on technology in 2024 to keep its mobile app and online portal competitive; continuous updates power features like real-time fraud alerts, automated budgeting tools, and instant transfers that drove a 12% YoY rise in mobile users in 2024. Keeping platforms secure and user-friendly—supporting 68% of deposits via digital channels in 2024—is essential to retain customers in a digital-first market.

Wealth Management and Investment Advisory

Fifth Third Bank delivers wealth management, estate planning, and investment advisory to HNW individuals and institutions, with advisors actively managing portfolios to match goals and risk; as of FY2024 the bank reported $272 billion in wealth and investment assets under administration, driving fee revenue that was 14% of noninterest income in 2024.

Risk Management and Regulatory Compliance

Fifth Third dedicates major operations to monitoring market trends, credit risk, and internal controls to meet legal rules — AML (anti-money laundering) systems scanned $1.2 trillion in transactions in 2024 and stress tests upheld CET1-like capital buffers near 11% at YE 2024.

Robust controls and strict data-privacy protocols reduce shock exposure and fines, protecting reputation and ensuring regulatory capital adequacy.

- AML surveillance: $1.2T transactions screened in 2024

- Capital buffer: ~11% common equity tier 1 (YE 2024)

- Stress testing: quarterly scenario runs; regulatory reporting

- Data privacy: GDPR/CCPA-aligned controls and encryption

Treasury and Payment Processing Services

Fifth Third Bank manages corporate cash flow via treasury management and merchant services, processing millions of transactions monthly and supporting liquidity needs for clients—treasury fees contributed materially to 2024 noninterest income of $4.6 billion (FY 2024), helping firms automate payroll and vendor payments and reduce float.

- Processes millions of transactions monthly

- Treasury-related fees part of $4.6B noninterest income (2024)

- Supports liquidity, payroll, vendor payment automation

Leading bank: $114.8B loans, 68% digital deposits, $272B wealth AUA, $1.1B tech spend

Originates and services $114.8B loans (Q4 2025) while keeping NPAs 0.92% (2025); invests $1.1B in tech (2024) driving +12% mobile users and 68% digital deposits (2024); manages $272B wealth AUA (FY2024) and processed $1.2T AML-screened txns (2024), treasury fees part of $4.6B noninterest income (2024).

| Metric | Value |

|---|---|

| Loans held | $114.8B (Q4 2025) |

| NPAs | 0.92% (2025) |

| Tech spend | $1.1B (2024) |

| Digital deposits | 68% (2024) |

| Wealth AUA | $272B (FY2024) |

| AML screened | $1.2T (2024) |

| Treasury fees | Part of $4.6B noninterest income (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the authentic Fifth Third Bank Business Model Canvas—not a mockup or sample—and it's the exact file you'll receive after purchase, fully populated and professionally formatted. Upon completing your order you'll get this same deliverable ready to edit, present, or share in Word and Excel formats, with all sections and content included—no surprises, no fillers.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Fifth Third Bank Business Model Canvas: Full 9‑Block Blueprint & Downloadable Tools

Unlock the full strategic blueprint behind Fifth Third Bank’s business model—our in-depth Business Model Canvas reveals how the bank creates customer value, captures revenue, and sustains competitive advantage across retail and commercial segments.

Perfect for investors, advisors, and strategists, the complete canvas includes company-specific insights for all nine blocks plus Word and Excel files ready for benchmarking, presentations, or strategic planning—download to gain actionable clarity.

Partnerships

Fintech and Embedded Payment Partners

The bank partners with fintechs to embed payments into commercial workflows, offering services such as Dividend Finance for point-of-sale lending and NewDominion for healthcare payments; these integrations helped Fifth Third originate over $2.3bn in digital loan volume in 2024, boosting fee income and merchant reach. By outsourcing tech expertise, Fifth Third cuts development time and kept digital transaction growth at ~18% YoY in 2024, preserving its competitive edge.

Technology and Cloud Infrastructure Providers

Fifth Third Bank partners with major cloud providers such as Microsoft Azure and Amazon Web Services to support digital transformation, using their scalable infrastructure for data processing, cybersecurity, and mobile app hosting; as of 2024 the bank reported a 20% YoY increase in digital transactions, underscoring the need for scale. These alliances are critical for 24/7 availability and data protection—outsourced cloud resilience reduces outage risk and helps meet regulatory security standards.

Regulatory and Government Agencies

The bank keeps mandatory ties with the Federal Reserve, the Office of the Comptroller of the Currency (OCC), and the FDIC for compliance with evolving laws; in 2024 Fifth Third reported regulatory capital ratios of CET1 9.7% and Tier 1 leverage 8.2%, reflecting oversight-driven capital targets. These partnerships include quarterly audits, monthly regulatory reporting, and participation in Fed liquidity programs that shaped its $157 billion liquidity buffer in 2024, preserving its charter and public trust.

Community and Non-Profit Organizations

Collaborations with local community and non-profit organizations help Fifth Third Bank meet Community Reinvestment Act (CRA) goals and spur regional growth; in 2024 the bank reported $2.3 billion in community development lending and investments, targeting small business and affordable housing.

These partners surface underserved markets for lending and housing projects, boosting brand presence in core Midwest and Southeast territories and supporting long-term economic health.

- 2024: $2.3B community development lending/investments

- Focus: small business lending, affordable housing, CRA compliance

- Geography: Midwest and Southeast core markets

Third-Party Mortgage and Insurance Servicers

Fifth Third Bank partners with third-party mortgage and insurance servicers to handle loan processing, appraisals, and insurance underwriting, letting the bank support a $148.5 billion loan portfolio (2024 end) while avoiding large fixed staffing increases.

These partners scale operations quickly, cutting per-loan overhead and improving turnaround; in 2024 external servicing reduced cycle times by ~18% for retail mortgages.

- Third-party servicing covers processing, appraisals, underwriting

- Supports $148.5B loan book (2024)

- Reduces per-loan overhead and staffing needs

- Shortened mortgage cycle times ~18% in 2024

Fifth Third Scales Digital Lending: $2.3B Originations, $148.5B Loan Book, ~18% Growth

Fifth Third leverages fintechs, cloud providers (Azure/AWS), regulators (Fed/OCC/FDIC), community orgs, and third-party servicers to scale digital lending, ensure regulatory compliance, meet CRA targets, and trim operational costs; key 2024 metrics: $2.3B digital loan originations, $2.3B community lending, $148.5B loan book, ~18% digital/transaction growth.

| Metric | 2024 |

|---|---|

| Digital loan originations | $2.3B |

| Community lending | $2.3B |

| Loan portfolio | $148.5B |

| Digital growth | ~18% YoY |

What is included in the product

A concise Business Model Canvas for Fifth Third Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and customer relationships aligned with its regional retail, commercial banking, and wealth management strategy.

Condenses Fifth Third Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and boardroom-ready insights.

Activities

Lending and Credit Portfolio Management

Fifth Third Bank originates and manages loans from residential mortgages to $1bn+ commercial credit lines, with total loans held for investment of $114.8 billion as of Q4 2025; rigorous credit analysis and stress testing cut weighted-average default exposure and support net interest income. Ongoing monitoring of borrower performance, collateral valuation, and workout teams keeps nonperforming assets at 0.92% in 2025, helping minimize charge-offs while sustaining yield.

Digital Banking and Platform Development

Fifth Third invests heavily in digital banking, spending about $1.1 billion on technology in 2024 to keep its mobile app and online portal competitive; continuous updates power features like real-time fraud alerts, automated budgeting tools, and instant transfers that drove a 12% YoY rise in mobile users in 2024. Keeping platforms secure and user-friendly—supporting 68% of deposits via digital channels in 2024—is essential to retain customers in a digital-first market.

Wealth Management and Investment Advisory

Fifth Third Bank delivers wealth management, estate planning, and investment advisory to HNW individuals and institutions, with advisors actively managing portfolios to match goals and risk; as of FY2024 the bank reported $272 billion in wealth and investment assets under administration, driving fee revenue that was 14% of noninterest income in 2024.

Risk Management and Regulatory Compliance

Fifth Third dedicates major operations to monitoring market trends, credit risk, and internal controls to meet legal rules — AML (anti-money laundering) systems scanned $1.2 trillion in transactions in 2024 and stress tests upheld CET1-like capital buffers near 11% at YE 2024.

Robust controls and strict data-privacy protocols reduce shock exposure and fines, protecting reputation and ensuring regulatory capital adequacy.

- AML surveillance: $1.2T transactions screened in 2024

- Capital buffer: ~11% common equity tier 1 (YE 2024)

- Stress testing: quarterly scenario runs; regulatory reporting

- Data privacy: GDPR/CCPA-aligned controls and encryption

Treasury and Payment Processing Services

Fifth Third Bank manages corporate cash flow via treasury management and merchant services, processing millions of transactions monthly and supporting liquidity needs for clients—treasury fees contributed materially to 2024 noninterest income of $4.6 billion (FY 2024), helping firms automate payroll and vendor payments and reduce float.

- Processes millions of transactions monthly

- Treasury-related fees part of $4.6B noninterest income (2024)

- Supports liquidity, payroll, vendor payment automation

Leading bank: $114.8B loans, 68% digital deposits, $272B wealth AUA, $1.1B tech spend

Originates and services $114.8B loans (Q4 2025) while keeping NPAs 0.92% (2025); invests $1.1B in tech (2024) driving +12% mobile users and 68% digital deposits (2024); manages $272B wealth AUA (FY2024) and processed $1.2T AML-screened txns (2024), treasury fees part of $4.6B noninterest income (2024).

| Metric | Value |

|---|---|

| Loans held | $114.8B (Q4 2025) |

| NPAs | 0.92% (2025) |

| Tech spend | $1.1B (2024) |

| Digital deposits | 68% (2024) |

| Wealth AUA | $272B (FY2024) |

| AML screened | $1.2T (2024) |

| Treasury fees | Part of $4.6B noninterest income (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the authentic Fifth Third Bank Business Model Canvas—not a mockup or sample—and it's the exact file you'll receive after purchase, fully populated and professionally formatted. Upon completing your order you'll get this same deliverable ready to edit, present, or share in Word and Excel formats, with all sections and content included—no surprises, no fillers.