Albert Weber SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

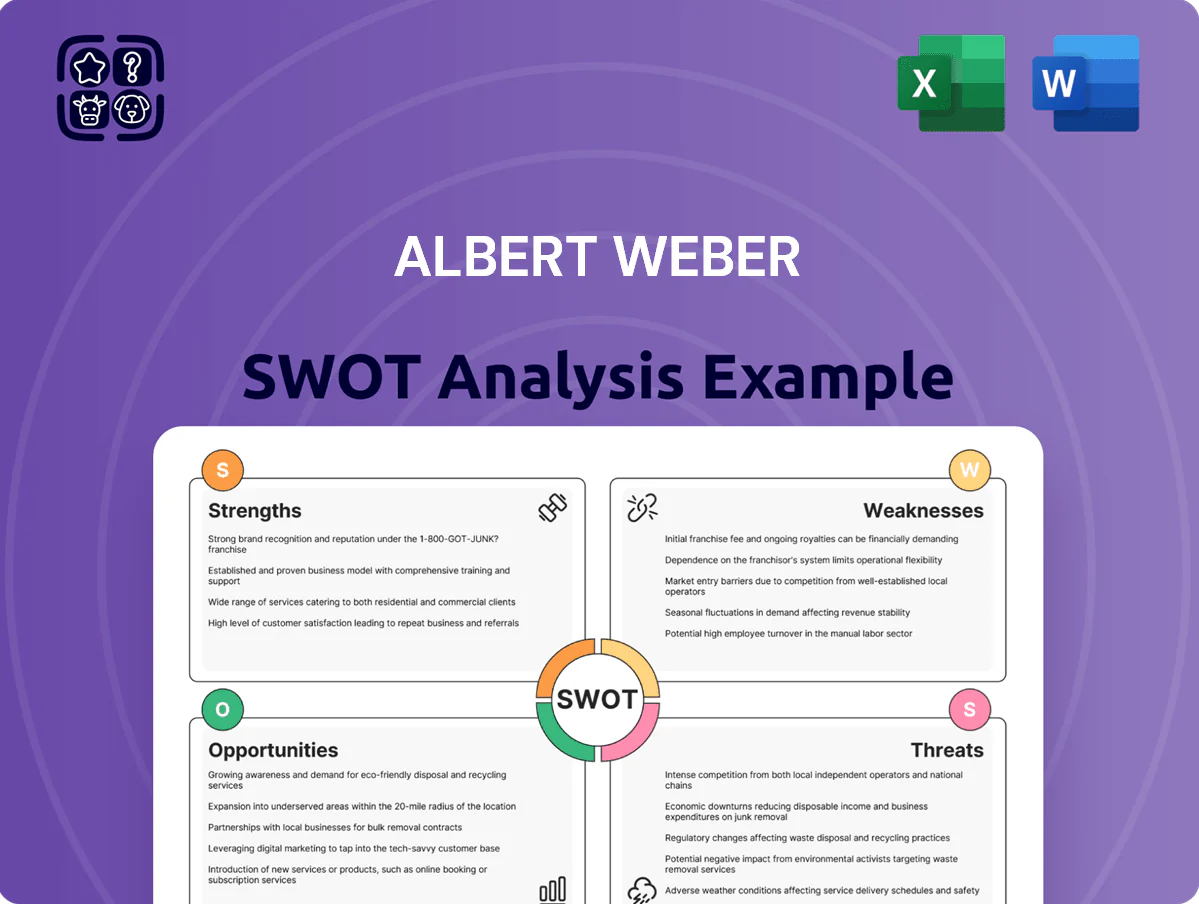

Albert Weber shows a focused market niche with strong brand recognition and operational efficiency, but faces supply-chain concentration and narrow product diversification that could limit scale; regulatory shifts and evolving customer preferences present both headwinds and opportunities. Purchase the full SWOT analysis to access a research-backed, editable report and Excel tools that translate these insights into strategic actions for investors and managers.

Strengths

Precision Engineering Expertise

Strategic OEM Partnerships

Global Manufacturing Footprint

With plants in Germany, Hungary, and the United States, Albert Weber cuts average transit time to key markets by ~28% and trims shipping costs for heavy metal components by roughly 12% versus single‑region peers (company 2024 reporting).

This footprint spreads sales risk: 2023–2024 regional revenue mix showed <45% Europe, 35% North America, 20% other, helping absorb local GDP swings and lower exposure to any one currency.

Having three jurisdictions reduced tariff and compliance shocks in 2022–2024, saving an estimated €8–12 million annually in duties and hedging costs, and improving supply resilience.

Advanced Assembly Integration

Albert Weber offers advanced assembly integration, turning components into ready-to-install systems and lowering clients' supplier count; in 2024 this raised average contract size by 18% and cut client onboarding time by 22%.

Vertical integration lets Albert Weber sell complete sub-assemblies, capturing ~30% more value per unit and raising switching costs as customers consolidate procurement.

- 18% higher contract size (2024)

- 22% faster onboarding (2024)

- ~30% more value captured per unit

Robust Quality Management

Albert Weber holds IATF 16949 and ISO 9001 certifications, and reported a 2024 defect rate of 12 ppm (parts per million), supporting its zero-defect claim for safety-critical chassis and engine parts.

That 12 ppm and on-time delivery of 98.6% in 2024 underpin a reliability reputation that secures tier-one/tier-two contracts in regulated automotive supply chains.

- IATF 16949 certified

- 12 ppm defect rate (2024)

- 98.6% on-time delivery (2024)

- Preferred tier-1/2 supplier status

Albert Weber: €142.3m parts, €420m OEM, 18% margin—lean global ops, €8–12m duty savings

| Metric | 2024 / FY |

|---|---|

| Parts revenue | €142.3m |

| Total OEM revenue | €420m (62%) |

| Gross margin | 18% |

| Defect rate | 12 ppm |

| On-time delivery | 98.6% |

| Capex | €24m |

| Regional mix | 45% EU / 35% NA / 20% other |

| Duty & hedging savings | €8–12m pa |

What is included in the product

Provides a concise SWOT overview of Albert Weber, outlining its core strengths and weaknesses while mapping market opportunities and external threats that shape the company’s strategic position.

Offers a compact SWOT layout tailored to Albert Weber for rapid strategic alignment and clearer decision-making.

Weaknesses

Internal Combustion Engine Dependency

High Capital Expenditure Requirements

Maintaining a leading edge in precision machining forces Albert Weber to reinvest heavily in CNC and robotic automation; capital expenditures totaled €72m in 2024 (18% of revenue), creating high fixed costs that squeeze liquidity during automotive downturns—vehicle production fell 7% EU-wide in 2024. Continuous capex needs cut free cash flow, limiting funds for diversification or faster debt reduction; net free cash flow was €8m in 2024.

Geographic Concentration in Europe

Limited Brand Recognition Outside B2B

As a specialized component manufacturer, Albert Weber operates almost exclusively in B2B channels and has low visibility among end consumers, meaning brand equity outside procurement is minimal.

Relying on technical reputation and procurement ties, the firm had 2024 sales of €142M with its top five customers accounting for ~58% of revenue, limiting leverage to drive demand.

That concentration makes pricing power weak and exposes Weber to buyer-driven margin pressure if large purchasers change sourcing.

- 2024 revenue €142M; top 5 buyers ~58%

- Low consumer awareness → no direct demand pull

- High dependence on procurement relationships

- Limited pricing leverage; high buyer-concentration risk

Slow Diversification Pace

- 75% revenue from automotive (2024)

- 18–36 months to repurpose talent/infrastructure

- 5–8% of sales in capex to enter new sectors

- 20–30% downside margin risk if automotive worsens

Albert Weber risks: heavy ICE, €72M capex, customer & regional concentration threaten margins

| Metric | 2024 |

|---|---|

| Total revenue | €142M |

| CapEx | €72M (18% rev) |

| Net FCF | €8M |

| Top-5 customers | ~58% |

| Automotive share | 75% |

| Europe revenue | >70% |

Preview the Actual Deliverable

Albert Weber SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Albert Weber shows a focused market niche with strong brand recognition and operational efficiency, but faces supply-chain concentration and narrow product diversification that could limit scale; regulatory shifts and evolving customer preferences present both headwinds and opportunities. Purchase the full SWOT analysis to access a research-backed, editable report and Excel tools that translate these insights into strategic actions for investors and managers.

Strengths

Precision Engineering Expertise

Strategic OEM Partnerships

Global Manufacturing Footprint

With plants in Germany, Hungary, and the United States, Albert Weber cuts average transit time to key markets by ~28% and trims shipping costs for heavy metal components by roughly 12% versus single‑region peers (company 2024 reporting).

This footprint spreads sales risk: 2023–2024 regional revenue mix showed <45% Europe, 35% North America, 20% other, helping absorb local GDP swings and lower exposure to any one currency.

Having three jurisdictions reduced tariff and compliance shocks in 2022–2024, saving an estimated €8–12 million annually in duties and hedging costs, and improving supply resilience.

Advanced Assembly Integration

Albert Weber offers advanced assembly integration, turning components into ready-to-install systems and lowering clients' supplier count; in 2024 this raised average contract size by 18% and cut client onboarding time by 22%.

Vertical integration lets Albert Weber sell complete sub-assemblies, capturing ~30% more value per unit and raising switching costs as customers consolidate procurement.

- 18% higher contract size (2024)

- 22% faster onboarding (2024)

- ~30% more value captured per unit

Robust Quality Management

Albert Weber holds IATF 16949 and ISO 9001 certifications, and reported a 2024 defect rate of 12 ppm (parts per million), supporting its zero-defect claim for safety-critical chassis and engine parts.

That 12 ppm and on-time delivery of 98.6% in 2024 underpin a reliability reputation that secures tier-one/tier-two contracts in regulated automotive supply chains.

- IATF 16949 certified

- 12 ppm defect rate (2024)

- 98.6% on-time delivery (2024)

- Preferred tier-1/2 supplier status

Albert Weber: €142.3m parts, €420m OEM, 18% margin—lean global ops, €8–12m duty savings

| Metric | 2024 / FY |

|---|---|

| Parts revenue | €142.3m |

| Total OEM revenue | €420m (62%) |

| Gross margin | 18% |

| Defect rate | 12 ppm |

| On-time delivery | 98.6% |

| Capex | €24m |

| Regional mix | 45% EU / 35% NA / 20% other |

| Duty & hedging savings | €8–12m pa |

What is included in the product

Provides a concise SWOT overview of Albert Weber, outlining its core strengths and weaknesses while mapping market opportunities and external threats that shape the company’s strategic position.

Offers a compact SWOT layout tailored to Albert Weber for rapid strategic alignment and clearer decision-making.

Weaknesses

Internal Combustion Engine Dependency

High Capital Expenditure Requirements

Maintaining a leading edge in precision machining forces Albert Weber to reinvest heavily in CNC and robotic automation; capital expenditures totaled €72m in 2024 (18% of revenue), creating high fixed costs that squeeze liquidity during automotive downturns—vehicle production fell 7% EU-wide in 2024. Continuous capex needs cut free cash flow, limiting funds for diversification or faster debt reduction; net free cash flow was €8m in 2024.

Geographic Concentration in Europe

Limited Brand Recognition Outside B2B

As a specialized component manufacturer, Albert Weber operates almost exclusively in B2B channels and has low visibility among end consumers, meaning brand equity outside procurement is minimal.

Relying on technical reputation and procurement ties, the firm had 2024 sales of €142M with its top five customers accounting for ~58% of revenue, limiting leverage to drive demand.

That concentration makes pricing power weak and exposes Weber to buyer-driven margin pressure if large purchasers change sourcing.

- 2024 revenue €142M; top 5 buyers ~58%

- Low consumer awareness → no direct demand pull

- High dependence on procurement relationships

- Limited pricing leverage; high buyer-concentration risk

Slow Diversification Pace

- 75% revenue from automotive (2024)

- 18–36 months to repurpose talent/infrastructure

- 5–8% of sales in capex to enter new sectors

- 20–30% downside margin risk if automotive worsens

Albert Weber risks: heavy ICE, €72M capex, customer & regional concentration threaten margins

| Metric | 2024 |

|---|---|

| Total revenue | €142M |

| CapEx | €72M (18% rev) |

| Net FCF | €8M |

| Top-5 customers | ~58% |

| Automotive share | 75% |

| Europe revenue | >70% |

Preview the Actual Deliverable

Albert Weber SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.