A2A PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, energy markets, and environmental policy are reshaping A2A’s strategic outlook with our concise PESTLE snapshot—designed to spotlight risks and growth levers for investors and planners; purchase the full analysis to access the complete, actionable breakdown instantly.

Political factors

European Green Deal Alignment

A2A must align with the European Green Deal’s targets — 55% EU emissions cut by 2030 and climate neutrality by 2050 — forcing capex shifts: A2A disclosed €2.7bn CAPEX 2024–27 prioritizing renewables and grids to meet these mandates.

Its industrial plan must comply with EU directives on renewables (REPowerEU targets raising renewables share to ~45% by 2030); non-alignment risks fines and reduced market access.

Brussels’ evolving stance on taxonomy eligibility for gas or waste-to-energy affects A2A’s access to green financing and ESG-linked loans; changes could reclassify projects, altering funding costs and valuation.

Italian National Energy and Climate Plan

The 2019 PNIEC, updated in 2023, targets 55% renewable electricity by 2030 and 25% reduction in final energy consumption, directly shaping A2A’s investments in biomethane, hydrogen and solar; Italy allocated €30bn in green subsidies 2021–2023, but ministerial changes have redirected funds, affecting project timelines. A2A must manage regional permitting delays—average 18–36 months—and local political opposition when siting waste‑to‑energy and new plants.

Geopolitical Energy Security

The EU has boosted gas diversification after 2022, cutting Russian pipeline gas imports from 40% to under 10% by 2024, accelerating LNG and renewables—Italy raised renewables share to ~36% of power in 2023, benefiting A2A’s domestic generation expansion.

Instability in the Mediterranean affects commodity costs: European natural gas TTF averaged €80/MWh in 2023 vs €35/MWh pre‑2021, raising fuel procurement and capex for A2A’s thermal backup and storage.

Governments deployed interventions: EU/Italy considered windfall taxes yielding €10–15bn sectorwide in 2022–24; recurring risk of price caps or special levies could compress A2A EBITDA margins in high volatility periods.

Public-Private Municipal Relations

A2A, majority-owned by the Municipalities of Milan (24.4%) and Brescia (19.6%), faces influence from local political cycles that can reprioritise investments in smart grids, district heating or waste services tied to urban agendas.

Strategic choices must balance ROI—A2A reported EBITDA of EUR 1.6bn in 2024—with municipal social objectives, affecting dividend policies and capex timing for multi-year projects.

Local elections in 2024–25 shifted priorities in both cities, altering procurement timelines for waste contracts and slowing rollout of some smart city pilots by up to 12 months.

- Municipal ownership: Milan 24.4%, Brescia 19.6%

- 2024 EBITDA: EUR 1.6bn

- Electoral shifts delayed projects up to 12 months

- Decisions balance shareholder returns and local social needs

Waste Management Policy Reforms

National and regional circular economy laws, like Italy’s 2023 National Recovery and Resilience Plan targets, drive feasibility of new waste-to-energy plants by setting recycling quotas — Italy aims for 55% recycling by 2025, affecting feedstock availability and capital returns for A2A’s projects.

Local political opposition (NIMBY) frequently delays permits; recent Lombardy cases required regional mediation, extending approval timelines by 12–24 months and raising project costs ~8–15%.

Shifts in waste export rules and plastic levies—EU’s 2025 plastic packaging tax and Italy’s asymmetric export restrictions—can cut A2A Ambiente margins by an estimated 3–6% or alter cash flows materially.

- Recycling targets: Italy 55% by 2025 — impacts feedstock

- Permitting delays: +12–24 months, +8–15% costs

- Policy taxes/export rules: -3–6% margins for A2A Ambiente

A2A ramps €2.7bn green CAPEX as municipal owners balance dividends amid margin risks

A2A must meet EU targets (55% emissions cut by 2030; climate neutrality 2050) driving €2.7bn CAPEX 2024–27 to renewables/grids; municipal ownership (Milan 24.4%, Brescia 19.6%) steers investment timing and dividend trade‑offs as 2024 EBITDA was €1.6bn. Permitting delays (18–36 months; +8–15% costs) and recycling targets (Italy 55% by 2025) constrain waste‑to‑energy feedstock and margins (‑3–6%).

| Metric | Value |

|---|---|

| CAPEX 2024–27 | €2.7bn |

| 2024 EBITDA | €1.6bn |

| Milan ownership | 24.4% |

| Brescia ownership | 19.6% |

| Permitting delays | 18–36 months |

| Italy recycling target | 55% by 2025 |

| Margin impact (waste rules) | ‑3–6% |

What is included in the product

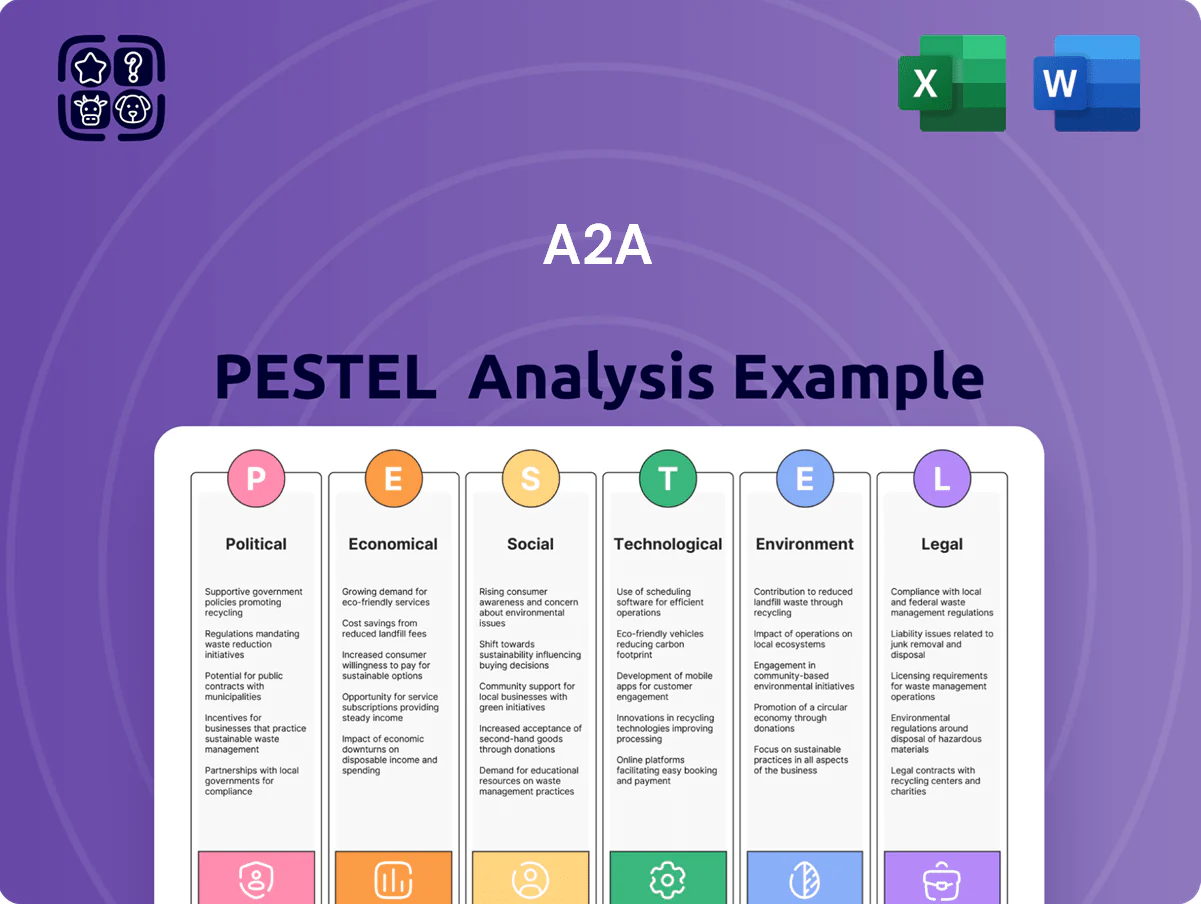

Explores how external macro-environmental factors uniquely affect the A2A across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight region- and industry-specific threats and opportunities.

A concise, PESTLE-segmented summary that teams can drop into presentations or share quickly, using plain language for cross-functional alignment and editable notes for local or business-line context.

Economic factors

Interest Rate Environment

As a capital-intensive utility, A2A is highly sensitive to European Central Bank policy; ECB rates rose to 4.00% in 2023–24, lifting average corporate borrowing costs and increasing project finance spreads by ~100–200bps for utilities. High rates pushed A2A’s 2024 net financial expense higher, constraining free cash flow for renewables and grid upgrades. Conversly, ECB guidance toward stabilization by end-2025 improves visibility for A2A’s EUR 3–4bn annual capex planning.

Energy Market Volatility

Fluctuations in wholesale electricity and gas prices directly affect A2A’s revenues and margins; 2024 Italian power forward prices rose ~28% YoY to ~120 €/MWh in Jan 2024, heightening volatility exposure. A2A uses hedging and long-term contracts to limit swings, but extreme moves can depress demand and raise receivable credit risk. Eurozone GDP growth of 0.4% Q4 2024 supports industrial energy use, a key B2B driver for A2A.

Inflationary Pressure on Operating Costs

Persistent inflation raised input costs for utilities in 2024–25, with EU industrial producer prices up 8.6% YoY in 2024 and Italian electricity generation fuel costs rising ~12% in 2024, pressuring A2A’s spending on raw materials, labor, and maintenance.

Under regulated tariffs for distribution and some supply segments, A2A must optimize its cost structure to protect 2025 EBITDA margins (2024 group EBITDA €1.25bn) without full repricing power.

Regulatory caps and retail competition limit pass-through: Italy’s ARERA allowed partial tariff adjustments in 2024, leaving residual cost exposure that A2A needs to hedge or offset via efficiency gains.

Funding via PNRR and Green Bonds

Access to Italy’s PNRR directs up to 191.5 billion euros nationally, with energy and digital transitions among top priorities—A2A can leverage these funds to digitalize grids and build circular economy hubs supporting its 2035 plan.

A2A’s Green Bond issuance taps growing sustainable finance: European green bond market reached ~175 billion euros in 2024, enabling potentially lower-cost capital for A2A’s multi-billion-euro investments.

PNRR and green bonds together are pivotal to fund A2A’s stated 2035 capex, roughly several billion euros annually under its strategic roadmap.

- PNRR: Italy total 191.5 bn euros; energy/digital priorities

- EU green bond market ~175 bn euros in 2024

- A2A 2035 plan requires multi‑bn euros capex annually

Economic Growth and Industrial Demand

The GDP of Northern Italy (Lombardy, Veneto, Piedmont) grew ~1.2% in 2024; manufacturing contraction of -0.5% Y/Y in H2 2024 lowered industrial power demand, pressuring A2A’s electricity and gas volumes.

Home-renovation tax incentives (65% ecological bonus; 2024 green superbonus extensions) and 2024 heat-pump installations up ~18% support rising demand for A2A’s heat-pump and district-heating services, partially offsetting industrial weakness.

- Northern Italy GDP growth ~1.2% (2024)

- Manufacturing -0.5% Y/Y in H2 2024

- Heat-pump installations +18% (2024)

- Ecobonus 65% & green superbonus extensions driving retrofit demand

A2A squeezed by ECB rates and rising power costs, but green funding and PNRR offer relief

A2A faces higher borrowing costs after ECB hikes (4.00% in 2023–24) that raised 2024 net financial expense and constrained FCF for capex; wholesale power rose ~28% YoY to ~120 €/MWh in Jan‑2024, increasing revenue volatility; 2024 EU industrial PPI +8.6% raised input costs; PNRR (Italy €191.5bn) and €175bn EU green bond market in 2024 offer funding for A2A’s multi‑bn€/yr 2035 capex.

| Metric | 2024/2025 |

|---|---|

| ECB rate | 4.00% |

| Power price Jan‑2024 | ~120 €/MWh (+28% YoY) |

| EU industrial PPI 2024 | +8.6% |

| Italy PNRR | €191.5bn |

| EU green bonds 2024 | €175bn |

Preview the Actual Deliverable

A2A PESTLE Analysis

The preview shown here is the exact A2A PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, energy markets, and environmental policy are reshaping A2A’s strategic outlook with our concise PESTLE snapshot—designed to spotlight risks and growth levers for investors and planners; purchase the full analysis to access the complete, actionable breakdown instantly.

Political factors

European Green Deal Alignment

A2A must align with the European Green Deal’s targets — 55% EU emissions cut by 2030 and climate neutrality by 2050 — forcing capex shifts: A2A disclosed €2.7bn CAPEX 2024–27 prioritizing renewables and grids to meet these mandates.

Its industrial plan must comply with EU directives on renewables (REPowerEU targets raising renewables share to ~45% by 2030); non-alignment risks fines and reduced market access.

Brussels’ evolving stance on taxonomy eligibility for gas or waste-to-energy affects A2A’s access to green financing and ESG-linked loans; changes could reclassify projects, altering funding costs and valuation.

Italian National Energy and Climate Plan

The 2019 PNIEC, updated in 2023, targets 55% renewable electricity by 2030 and 25% reduction in final energy consumption, directly shaping A2A’s investments in biomethane, hydrogen and solar; Italy allocated €30bn in green subsidies 2021–2023, but ministerial changes have redirected funds, affecting project timelines. A2A must manage regional permitting delays—average 18–36 months—and local political opposition when siting waste‑to‑energy and new plants.

Geopolitical Energy Security

The EU has boosted gas diversification after 2022, cutting Russian pipeline gas imports from 40% to under 10% by 2024, accelerating LNG and renewables—Italy raised renewables share to ~36% of power in 2023, benefiting A2A’s domestic generation expansion.

Instability in the Mediterranean affects commodity costs: European natural gas TTF averaged €80/MWh in 2023 vs €35/MWh pre‑2021, raising fuel procurement and capex for A2A’s thermal backup and storage.

Governments deployed interventions: EU/Italy considered windfall taxes yielding €10–15bn sectorwide in 2022–24; recurring risk of price caps or special levies could compress A2A EBITDA margins in high volatility periods.

Public-Private Municipal Relations

A2A, majority-owned by the Municipalities of Milan (24.4%) and Brescia (19.6%), faces influence from local political cycles that can reprioritise investments in smart grids, district heating or waste services tied to urban agendas.

Strategic choices must balance ROI—A2A reported EBITDA of EUR 1.6bn in 2024—with municipal social objectives, affecting dividend policies and capex timing for multi-year projects.

Local elections in 2024–25 shifted priorities in both cities, altering procurement timelines for waste contracts and slowing rollout of some smart city pilots by up to 12 months.

- Municipal ownership: Milan 24.4%, Brescia 19.6%

- 2024 EBITDA: EUR 1.6bn

- Electoral shifts delayed projects up to 12 months

- Decisions balance shareholder returns and local social needs

Waste Management Policy Reforms

National and regional circular economy laws, like Italy’s 2023 National Recovery and Resilience Plan targets, drive feasibility of new waste-to-energy plants by setting recycling quotas — Italy aims for 55% recycling by 2025, affecting feedstock availability and capital returns for A2A’s projects.

Local political opposition (NIMBY) frequently delays permits; recent Lombardy cases required regional mediation, extending approval timelines by 12–24 months and raising project costs ~8–15%.

Shifts in waste export rules and plastic levies—EU’s 2025 plastic packaging tax and Italy’s asymmetric export restrictions—can cut A2A Ambiente margins by an estimated 3–6% or alter cash flows materially.

- Recycling targets: Italy 55% by 2025 — impacts feedstock

- Permitting delays: +12–24 months, +8–15% costs

- Policy taxes/export rules: -3–6% margins for A2A Ambiente

A2A ramps €2.7bn green CAPEX as municipal owners balance dividends amid margin risks

A2A must meet EU targets (55% emissions cut by 2030; climate neutrality 2050) driving €2.7bn CAPEX 2024–27 to renewables/grids; municipal ownership (Milan 24.4%, Brescia 19.6%) steers investment timing and dividend trade‑offs as 2024 EBITDA was €1.6bn. Permitting delays (18–36 months; +8–15% costs) and recycling targets (Italy 55% by 2025) constrain waste‑to‑energy feedstock and margins (‑3–6%).

| Metric | Value |

|---|---|

| CAPEX 2024–27 | €2.7bn |

| 2024 EBITDA | €1.6bn |

| Milan ownership | 24.4% |

| Brescia ownership | 19.6% |

| Permitting delays | 18–36 months |

| Italy recycling target | 55% by 2025 |

| Margin impact (waste rules) | ‑3–6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the A2A across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight region- and industry-specific threats and opportunities.

A concise, PESTLE-segmented summary that teams can drop into presentations or share quickly, using plain language for cross-functional alignment and editable notes for local or business-line context.

Economic factors

Interest Rate Environment

As a capital-intensive utility, A2A is highly sensitive to European Central Bank policy; ECB rates rose to 4.00% in 2023–24, lifting average corporate borrowing costs and increasing project finance spreads by ~100–200bps for utilities. High rates pushed A2A’s 2024 net financial expense higher, constraining free cash flow for renewables and grid upgrades. Conversly, ECB guidance toward stabilization by end-2025 improves visibility for A2A’s EUR 3–4bn annual capex planning.

Energy Market Volatility

Fluctuations in wholesale electricity and gas prices directly affect A2A’s revenues and margins; 2024 Italian power forward prices rose ~28% YoY to ~120 €/MWh in Jan 2024, heightening volatility exposure. A2A uses hedging and long-term contracts to limit swings, but extreme moves can depress demand and raise receivable credit risk. Eurozone GDP growth of 0.4% Q4 2024 supports industrial energy use, a key B2B driver for A2A.

Inflationary Pressure on Operating Costs

Persistent inflation raised input costs for utilities in 2024–25, with EU industrial producer prices up 8.6% YoY in 2024 and Italian electricity generation fuel costs rising ~12% in 2024, pressuring A2A’s spending on raw materials, labor, and maintenance.

Under regulated tariffs for distribution and some supply segments, A2A must optimize its cost structure to protect 2025 EBITDA margins (2024 group EBITDA €1.25bn) without full repricing power.

Regulatory caps and retail competition limit pass-through: Italy’s ARERA allowed partial tariff adjustments in 2024, leaving residual cost exposure that A2A needs to hedge or offset via efficiency gains.

Funding via PNRR and Green Bonds

Access to Italy’s PNRR directs up to 191.5 billion euros nationally, with energy and digital transitions among top priorities—A2A can leverage these funds to digitalize grids and build circular economy hubs supporting its 2035 plan.

A2A’s Green Bond issuance taps growing sustainable finance: European green bond market reached ~175 billion euros in 2024, enabling potentially lower-cost capital for A2A’s multi-billion-euro investments.

PNRR and green bonds together are pivotal to fund A2A’s stated 2035 capex, roughly several billion euros annually under its strategic roadmap.

- PNRR: Italy total 191.5 bn euros; energy/digital priorities

- EU green bond market ~175 bn euros in 2024

- A2A 2035 plan requires multi‑bn euros capex annually

Economic Growth and Industrial Demand

The GDP of Northern Italy (Lombardy, Veneto, Piedmont) grew ~1.2% in 2024; manufacturing contraction of -0.5% Y/Y in H2 2024 lowered industrial power demand, pressuring A2A’s electricity and gas volumes.

Home-renovation tax incentives (65% ecological bonus; 2024 green superbonus extensions) and 2024 heat-pump installations up ~18% support rising demand for A2A’s heat-pump and district-heating services, partially offsetting industrial weakness.

- Northern Italy GDP growth ~1.2% (2024)

- Manufacturing -0.5% Y/Y in H2 2024

- Heat-pump installations +18% (2024)

- Ecobonus 65% & green superbonus extensions driving retrofit demand

A2A squeezed by ECB rates and rising power costs, but green funding and PNRR offer relief

A2A faces higher borrowing costs after ECB hikes (4.00% in 2023–24) that raised 2024 net financial expense and constrained FCF for capex; wholesale power rose ~28% YoY to ~120 €/MWh in Jan‑2024, increasing revenue volatility; 2024 EU industrial PPI +8.6% raised input costs; PNRR (Italy €191.5bn) and €175bn EU green bond market in 2024 offer funding for A2A’s multi‑bn€/yr 2035 capex.

| Metric | 2024/2025 |

|---|---|

| ECB rate | 4.00% |

| Power price Jan‑2024 | ~120 €/MWh (+28% YoY) |

| EU industrial PPI 2024 | +8.6% |

| Italy PNRR | €191.5bn |

| EU green bonds 2024 | €175bn |

Preview the Actual Deliverable

A2A PESTLE Analysis

The preview shown here is the exact A2A PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.