American Axle & Manufacturing Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

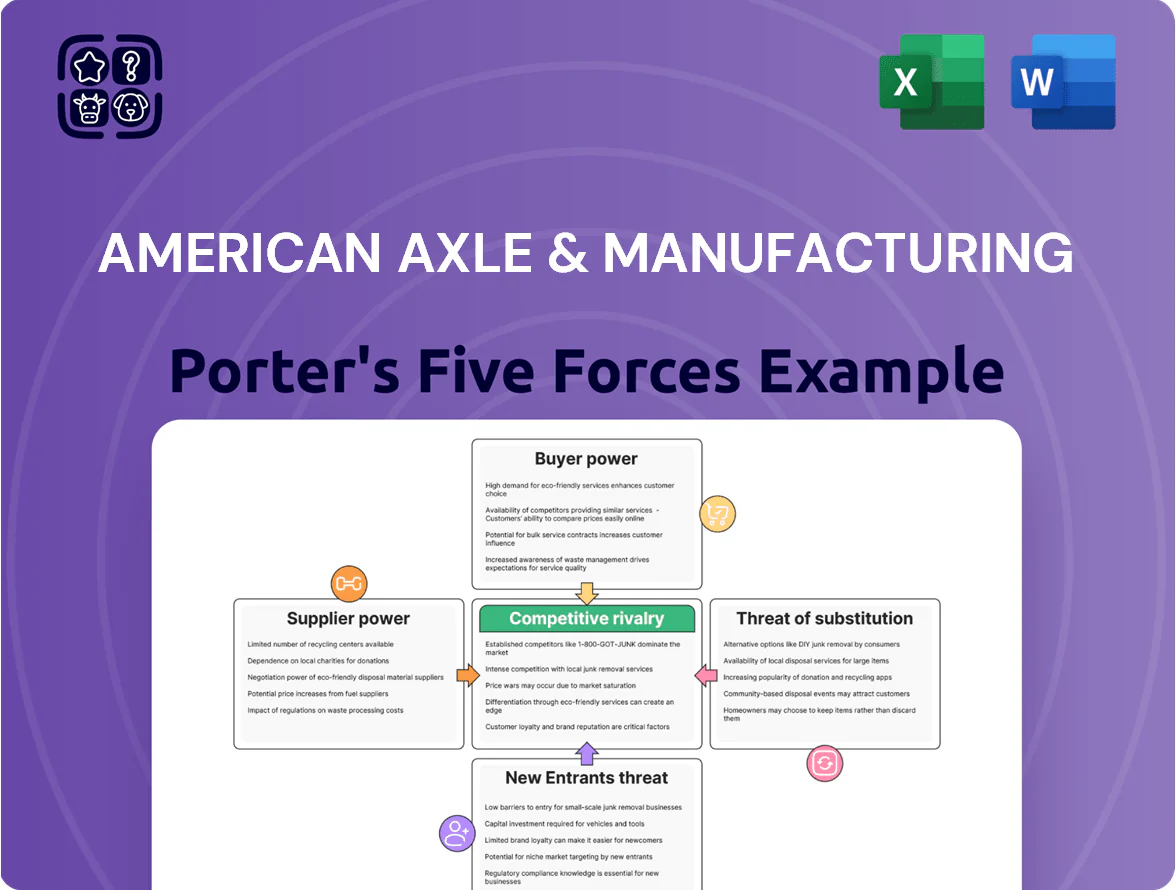

American Axle & Manufacturing faces moderate supplier power due to specialized component inputs, intense rivalry from global OEM suppliers, and steady buyer bargaining from large automakers squeezing margins.

Barriers to entry remain high given capital intensity and economies of scale, while threat of substitutes is low but rising with EV drivetrain changes that could reshape demand for traditional axles.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore American Axle & Manufacturing’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Volatility

AAM depends on steel, aluminum and scrap metal, whose prices rose ~18% YoY in 2024–2025 for flat-rolled steel and 12% for aluminum, driven by inflation and trade measures; these inputs now account for an estimated 20–25% of COGS.

Index-based pricing in many AAM contracts helps but lags market moves by 30–90 days, so cost spikes erode margins before pass-through; large commodity producers use volume discounts and tight availability to exert leverage over Tier 1 suppliers.

Specialized Electronic Component Providers

The shift to electric drivelines raised AAM’s reliance on semiconductors, sensors, and power electronics, components dominated by roughly 5–10 high‑end suppliers, giving them strong bargaining power; semiconductor shortages in 2021–22 cut global auto production by ~10% and still push premiums of 5–20% on lead components in 2024.

Energy and Utility Dependencies

Manufacturing metal-formed components and driveline systems is energy-intensive, needing steady electricity and natural gas; in 2024 U.S. industrial electricity prices averaged 10.9 cents/kWh and Henry Hub gas averaged ~$2.50/MMBtu, so energy swings hit AAM’s margins directly.

Regional utility monopolies and national grids limit AAM’s bargaining power; industrial customers often accept long-term tariffs—U.S. large industrial contracts rose 6% YoY in 2023—so AAM faces constrained rate negotiation.

Carbon pricing and renewables transition add volatility: EU carbon EUA averaged €80/ton in 2024 and U.S. state programs vary, raising operating costs and capex for electrification and efficiency upgrades.

Labor Market Dynamics

The limited pool of advanced manufacturing and software engineers raises supplier power for American Axle & Manufacturing (AAM); industry data show US manufacturing job vacancies rose to 470,000 in 2024 and engineering roles commanding 15–30% premium in EV-related firms.

Unionized labor in auto hubs and competition from tech firms push wages up—AAM reported 2024 labor costs increasing ~6% year-over-year—so failing to retain talent risks delays and higher OPEX.

- 470,000 US manufacturing vacancies (2024)

- 15–30% wage premiums for EV engineers

- AAM labor costs +6% YoY in 2024

- Risk: production delays, higher OPEX

Tier 2 and Tier 3 Sub-Component Suppliers

AAM relies on many small Tier 2/3 suppliers for specialized fasteners, seals and sub-assemblies; a single supplier failure can stop a line—AAM reported parts shortages cost North American production 3.8% of volume in 2023. Consolidation among these vendors has cut choices, nudging their collective bargaining power up slightly. AAM keeps multi-sourcing, long-term contracts and dual-supply qualification to reduce disruption risk and inventory days.

- 2023: 3.8% production lost to parts shortages

- Consolidation: fewer qualified Tier 2/3 vendors

- Mitigation: multi-sourcing, long-term contracts, dual qualifications

Supplier power squeezes AAM: metals, semiconductors and labor risk margins

AAM faces moderate-to-high supplier power: metals (20–25% COGS) and semiconductors (5–10 critical suppliers) drive cost exposure; commodity price lags (30–90 days) and energy/gas swings cut margins; skilled labor shortages (470,000 US vacancies in 2024) and supplier consolidation raised disruption risk (3.8% lost volume in 2023); mitigations: multi-sourcing, long-term contracts, index pass-throughs.

| Metric | Value (2023–2025) |

|---|---|

| Metals share of COGS | 20–25% |

| Flat-rolled steel/aluminum price change | +18% / +12% YoY (2024–25) |

| Critical high‑end suppliers | 5–10 |

| US mfg vacancies | 470,000 (2024) |

| Lost production from parts shortages | 3.8% (2023) |

What is included in the product

Tailored exclusively for American Axle & Manufacturing, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, barriers to entry, substitute threats, and strategic pressures shaping its profitability and market position.

A concise Porter's Five Forces one-sheet for American Axle & Manufacturing—quickly spot supplier and buyer power, rivalry intensity, and threat vectors to streamline strategic decisions.

Customers Bargaining Power

Concentration of Major OEM Revenue

AAM earns roughly 40% of revenue from its top three OEMs, with General Motors alone accounting for about 25% of 2024 sales, giving these customers strong leverage over pricing, delivery and specs.

That concentration means a single OEM cutting orders or switching suppliers would hit margins and cash flow quickly; AAM accepted lower gross margins in 2024 to secure multi-year, high-volume contracts.

High dependence forces AAM to prioritize contract retention over price, keeping operating margins constrained.

Aggressive Annual Cost Reduction Mandates

Automotive OEMs force annual productivity givebacks—often 2–4% yearly—into long-term contracts, shifting cost-reduction responsibility to Tier 1s like American Axle & Manufacturing (AAM).

AAM must invest continually in automation and process redesign to protect margins; failing to meet targets cut its adjusted operating margin, which was 3.8% in 2024, and risks losing platforms to lower-cost rivals.

Vertical Integration and Insourcing

AAM faces rising customer power as major OEMs insource EV drive units and axles; Ford, GM, and Stellantis announced roughly $40–60 billion combined EV manufacturing investments in 2023–2025 to secure margins and jobs, shrinking the addressable market for suppliers. As automakers internalize core components, AAM’s revenue exposure—60% automotive in 2024—faces contract pressure and potential share loss. When OEMs can build a part, their negotiating leverage grows sharply, forcing price, lead-time, and capex concessions from AAM.

Strict Quality and Sustainability Compliance

OEMs demand strict ESG and zero-defect quality; failure risks audits and contract termination, giving buyers strong leverage over AAM.

Meeting these rules forced AAM to spend capital—AAM reported $122 million in sustainability and quality investments in 2024—without raising per-unit prices, squeezing margins.

The OEMs’ ability to set non-negotiable standards underscores their dominant position in the value chain.

- OEM audit power: can terminate contracts

- $122M AAM 2024 sustainability/quality spend

- Investments often don’t allow higher per-unit pricing

- Raises compliance-driven margin pressure

Low Switching Costs for New Platforms

OEMs find it hard to swap suppliers mid-cycle, but they can redesign new platforms and re-source for the next decade; each new vehicle program is a fresh bidding opportunity—AAM faces potential loss at every launch.

This bidding pressure forces AAM to compete on technology and price; with 2024 US light-vehicle production ~11.5M units, platform churn keeps buyers firmly in charge.

- New launches = re-evaluation chance

- Past wins ≠ future contracts

- Must match tech and price every bid

- 11.5M US vehicles (2024) = repeated opportunities

AAM under pressure: concentrated OEM power, razor-thin margins, EV insourcing risks

AAM faces very high customer bargaining power: top 3 OEMs = ~40% revenue, GM ~25% of 2024 sales, forcing price, specs and productivity givebacks; AAM’s 2024 adjusted operating margin was 3.8% after accepting lower gross margins to retain multi-year contracts; OEM insourcing of EV drive units and $40–60B combined OEM EV investments (2023–25) shrink supplier addressable market; AAM spent $122M on sustainability/quality in 2024, absorbing costs without price pass-through.

| Metric | Value |

|---|---|

| Top-3 OEM revenue share (2024) | ~40% |

| GM share (2024) | ~25% |

| Adjusted operating margin (2024) | 3.8% |

| Sustainability/quality spend (2024) | $122M |

| OEM EV investments (2023–25) | $40–60B |

Same Document Delivered

American Axle & Manufacturing Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of American Axle & Manufacturing you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file available for instant download the moment you buy. You're looking at the actual deliverable: ready-to-use, concise, and tailored for decision-making. No mockups or samples—what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

American Axle & Manufacturing faces moderate supplier power due to specialized component inputs, intense rivalry from global OEM suppliers, and steady buyer bargaining from large automakers squeezing margins.

Barriers to entry remain high given capital intensity and economies of scale, while threat of substitutes is low but rising with EV drivetrain changes that could reshape demand for traditional axles.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore American Axle & Manufacturing’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Volatility

AAM depends on steel, aluminum and scrap metal, whose prices rose ~18% YoY in 2024–2025 for flat-rolled steel and 12% for aluminum, driven by inflation and trade measures; these inputs now account for an estimated 20–25% of COGS.

Index-based pricing in many AAM contracts helps but lags market moves by 30–90 days, so cost spikes erode margins before pass-through; large commodity producers use volume discounts and tight availability to exert leverage over Tier 1 suppliers.

Specialized Electronic Component Providers

The shift to electric drivelines raised AAM’s reliance on semiconductors, sensors, and power electronics, components dominated by roughly 5–10 high‑end suppliers, giving them strong bargaining power; semiconductor shortages in 2021–22 cut global auto production by ~10% and still push premiums of 5–20% on lead components in 2024.

Energy and Utility Dependencies

Manufacturing metal-formed components and driveline systems is energy-intensive, needing steady electricity and natural gas; in 2024 U.S. industrial electricity prices averaged 10.9 cents/kWh and Henry Hub gas averaged ~$2.50/MMBtu, so energy swings hit AAM’s margins directly.

Regional utility monopolies and national grids limit AAM’s bargaining power; industrial customers often accept long-term tariffs—U.S. large industrial contracts rose 6% YoY in 2023—so AAM faces constrained rate negotiation.

Carbon pricing and renewables transition add volatility: EU carbon EUA averaged €80/ton in 2024 and U.S. state programs vary, raising operating costs and capex for electrification and efficiency upgrades.

Labor Market Dynamics

The limited pool of advanced manufacturing and software engineers raises supplier power for American Axle & Manufacturing (AAM); industry data show US manufacturing job vacancies rose to 470,000 in 2024 and engineering roles commanding 15–30% premium in EV-related firms.

Unionized labor in auto hubs and competition from tech firms push wages up—AAM reported 2024 labor costs increasing ~6% year-over-year—so failing to retain talent risks delays and higher OPEX.

- 470,000 US manufacturing vacancies (2024)

- 15–30% wage premiums for EV engineers

- AAM labor costs +6% YoY in 2024

- Risk: production delays, higher OPEX

Tier 2 and Tier 3 Sub-Component Suppliers

AAM relies on many small Tier 2/3 suppliers for specialized fasteners, seals and sub-assemblies; a single supplier failure can stop a line—AAM reported parts shortages cost North American production 3.8% of volume in 2023. Consolidation among these vendors has cut choices, nudging their collective bargaining power up slightly. AAM keeps multi-sourcing, long-term contracts and dual-supply qualification to reduce disruption risk and inventory days.

- 2023: 3.8% production lost to parts shortages

- Consolidation: fewer qualified Tier 2/3 vendors

- Mitigation: multi-sourcing, long-term contracts, dual qualifications

Supplier power squeezes AAM: metals, semiconductors and labor risk margins

AAM faces moderate-to-high supplier power: metals (20–25% COGS) and semiconductors (5–10 critical suppliers) drive cost exposure; commodity price lags (30–90 days) and energy/gas swings cut margins; skilled labor shortages (470,000 US vacancies in 2024) and supplier consolidation raised disruption risk (3.8% lost volume in 2023); mitigations: multi-sourcing, long-term contracts, index pass-throughs.

| Metric | Value (2023–2025) |

|---|---|

| Metals share of COGS | 20–25% |

| Flat-rolled steel/aluminum price change | +18% / +12% YoY (2024–25) |

| Critical high‑end suppliers | 5–10 |

| US mfg vacancies | 470,000 (2024) |

| Lost production from parts shortages | 3.8% (2023) |

What is included in the product

Tailored exclusively for American Axle & Manufacturing, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, barriers to entry, substitute threats, and strategic pressures shaping its profitability and market position.

A concise Porter's Five Forces one-sheet for American Axle & Manufacturing—quickly spot supplier and buyer power, rivalry intensity, and threat vectors to streamline strategic decisions.

Customers Bargaining Power

Concentration of Major OEM Revenue

AAM earns roughly 40% of revenue from its top three OEMs, with General Motors alone accounting for about 25% of 2024 sales, giving these customers strong leverage over pricing, delivery and specs.

That concentration means a single OEM cutting orders or switching suppliers would hit margins and cash flow quickly; AAM accepted lower gross margins in 2024 to secure multi-year, high-volume contracts.

High dependence forces AAM to prioritize contract retention over price, keeping operating margins constrained.

Aggressive Annual Cost Reduction Mandates

Automotive OEMs force annual productivity givebacks—often 2–4% yearly—into long-term contracts, shifting cost-reduction responsibility to Tier 1s like American Axle & Manufacturing (AAM).

AAM must invest continually in automation and process redesign to protect margins; failing to meet targets cut its adjusted operating margin, which was 3.8% in 2024, and risks losing platforms to lower-cost rivals.

Vertical Integration and Insourcing

AAM faces rising customer power as major OEMs insource EV drive units and axles; Ford, GM, and Stellantis announced roughly $40–60 billion combined EV manufacturing investments in 2023–2025 to secure margins and jobs, shrinking the addressable market for suppliers. As automakers internalize core components, AAM’s revenue exposure—60% automotive in 2024—faces contract pressure and potential share loss. When OEMs can build a part, their negotiating leverage grows sharply, forcing price, lead-time, and capex concessions from AAM.

Strict Quality and Sustainability Compliance

OEMs demand strict ESG and zero-defect quality; failure risks audits and contract termination, giving buyers strong leverage over AAM.

Meeting these rules forced AAM to spend capital—AAM reported $122 million in sustainability and quality investments in 2024—without raising per-unit prices, squeezing margins.

The OEMs’ ability to set non-negotiable standards underscores their dominant position in the value chain.

- OEM audit power: can terminate contracts

- $122M AAM 2024 sustainability/quality spend

- Investments often don’t allow higher per-unit pricing

- Raises compliance-driven margin pressure

Low Switching Costs for New Platforms

OEMs find it hard to swap suppliers mid-cycle, but they can redesign new platforms and re-source for the next decade; each new vehicle program is a fresh bidding opportunity—AAM faces potential loss at every launch.

This bidding pressure forces AAM to compete on technology and price; with 2024 US light-vehicle production ~11.5M units, platform churn keeps buyers firmly in charge.

- New launches = re-evaluation chance

- Past wins ≠ future contracts

- Must match tech and price every bid

- 11.5M US vehicles (2024) = repeated opportunities

AAM under pressure: concentrated OEM power, razor-thin margins, EV insourcing risks

AAM faces very high customer bargaining power: top 3 OEMs = ~40% revenue, GM ~25% of 2024 sales, forcing price, specs and productivity givebacks; AAM’s 2024 adjusted operating margin was 3.8% after accepting lower gross margins to retain multi-year contracts; OEM insourcing of EV drive units and $40–60B combined OEM EV investments (2023–25) shrink supplier addressable market; AAM spent $122M on sustainability/quality in 2024, absorbing costs without price pass-through.

| Metric | Value |

|---|---|

| Top-3 OEM revenue share (2024) | ~40% |

| GM share (2024) | ~25% |

| Adjusted operating margin (2024) | 3.8% |

| Sustainability/quality spend (2024) | $122M |

| OEM EV investments (2023–25) | $40–60B |

Same Document Delivered

American Axle & Manufacturing Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of American Axle & Manufacturing you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file available for instant download the moment you buy. You're looking at the actual deliverable: ready-to-use, concise, and tailored for decision-making. No mockups or samples—what you see is what you get.