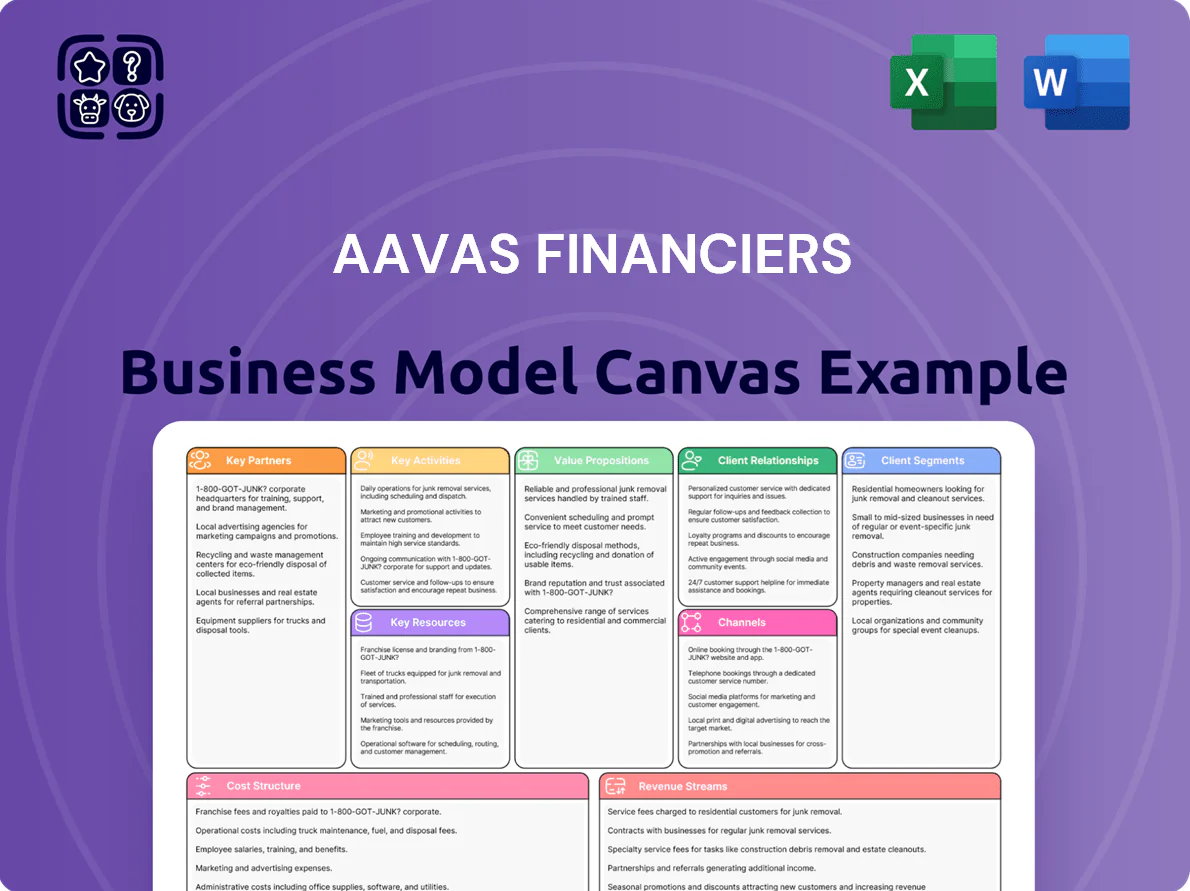

Aavas Financiers Business Model Canvas

Aavas Financiers: Scalable Profits from Affordable Housing Demand

Discover how Aavas Financiers converts niche affordable-housing demand into profitable growth—this concise Business Model Canvas outlines customer segments, unique value propositions, revenue streams, and scalable operations to inspire investors and strategists.

Partnerships

Banking and Financial Institution Alliances

Aavas Financiers partners with 20+ commercial banks and NBFCs to secure term loans and syndicated facilities, underpinning a liquidity buffer of ₹6,200 crore as of FY2024 and keeping blended cost of funds near 9.5% in FY2024. These alliances supply steady capital to support a ~22% CAGR in loan book growth (FY2021–FY2024) for rural and semi‑urban housing credit.

National Housing Bank Refinancing

The National Housing Bank (NHB) partnership gives Aavas Financiers access to low-cost refinance and liquidity; as of FY2024 NHB lines covered about 18% of Aavas’s borrowings, lowering blended funding cost by ~60 bps and enabling retail loans at sub-9% rates to low-income borrowers.

Local Contractors and Small Developers

Aavas Financiers ties with local masons, contractors, and small developers across Tier II–V towns drive lead flow, with channel-originated loans accounting for about 35% of disbursements in FY2024 (₹6.3bn of ₹18bn total home loans). These partners refer buyers for new builds and renovations, keeping Aavas the preferred grassroots financier and cutting customer acquisition cost by an estimated 22% versus branch-only sourcing.

Insurance and Ancillary Service Providers

Strategic tie-ups with life and general insurers let Aavas offer credit-linked insurance, protecting borrowers' families and cutting expected credit losses; in FY2024 Aavas reported ~12-15bps reduction in GNPA risk from insurance-covered loans.

These alliances also drive non-interest income—commissions and fees made up ~9% of Aavas' total income in FY2024, boosting ROA and diversifying revenue.

- Credit-linked insurance reduces borrower default loss

- Insurance partnerships lower portfolio risk by ~12-15bps (FY2024)

- Commissions/fees ≈9% of total income (FY2024)

Technology and Fintech Collaborators

By end-2025 Aavas Financiers expanded fintech ties, deploying alternative-data credit models that raised approval rates for thin-file borrowers by ~18% and cut NPLs by 0.6pp in pilot cohorts, boosting digital underwriting and analytics capacity.

These tech partnerships automate sourcing-to-collections workflows, reducing time-to-disbursement from 9 to 4 days and lowering servicing cost per loan ~22%.

- 18% higher approvals for thin-file

- 0.6pp NPL reduction in pilots

- Disbursement time down 5 days

- Servicing cost −22%

Aavas’ ₹6,200cr liquidity, 9.5% funding cost fuels 22% CAGR; channel & fintech cut NPLs

Aavas’s 20+ bank/NBFC partners and NHB refinance provided a ₹6,200cr liquidity buffer (FY2024), keeping blended funding cost ~9.5% and supporting ~22% loan-book CAGR (FY2021–FY2024); channel partners generated ~35% of disbursements (FY2024) while insurance and fintech ties cut expected credit loss ~12–15bps and NPLs 0.6pp, sped disbursements 9→4 days, and lifted thin-file approvals +18%.

| Metric | Value |

|---|---|

| Liquidity buffer (FY2024) | ₹6,200 crore |

| Blended cost of funds (FY2024) | ~9.5% |

| Loan-book CAGR (FY2021–FY2024) | ~22% |

| Channel-originated disbursals (FY2024) | 35% (₹6.3bn of ₹18bn) |

| NHB share of borrowings (FY2024) | ~18% |

| Insurance impact on GNPA | −12–15 bps |

| Thin-file approval lift (pilot) | +18% |

| NPL reduction (pilot) | −0.6 pp |

| Disbursement time | 9 → 4 days |

What is included in the product

A concise, pre-written Business Model Canvas for Aavas Financiers covering customer segments, channels, value propositions, revenue streams, cost structure, key resources, partners, activities, and customer relationships, reflecting real-world operations and strategic plans with SWOT-linked insights and competitive advantages; ideal for presentations, funding discussions, and decision-making by entrepreneurs and analysts.

High-level one-page Business Model Canvas for Aavas Financiers that condenses lending strategy, customer segments, and revenue streams into an editable layout—ideal for quick reviews and team collaboration.

Activities

Loan Sourcing and Lead Generation

Aavas Financiers sources loans via a 3,500+ strong field force targeting semi-urban clusters; in FY2024 it generated ~62% of new customer leads through door-to-door visits and community meetings, focusing on borrowers without formal income proof who are largely ignored by banks.

Rigorous Credit Underwriting and Appraisal

Rigorous credit underwriting at Aavas Financiers uses physical verification and cash-flow analysis to assess informal incomes; credit officers visit work and home to validate earnings for self-employed borrowers, supporting a 0.9% gross NPA reported in FY2025 and sustaining a PAR>30 of 0.6% as of Sep 2025.—this diligence lets Aavas serve 1.2 million customers across rural India while keeping asset quality high.

Loan Servicing and Collection Management

Aavas manages the loan lifecycle with rapid disbursements (median 5–7 days in FY2024) and proactive collections; a localized model uses ~2,200 relationship managers who average weekly borrower contact to sustain payment discipline.

Geographic Expansion and Branch Operations

- ~515 branches (FY2024–25)

- 9 states covered

- Loan book Rs 22,800 crore (Mar 31, 2025)

- Hub-and-spoke lowers branch Opex per loan

- Branches handle onboarding, docs, local marketing

Risk Management and Regulatory Compliance

Ensuring strict adherence to Reserve Bank of India and National Housing Bank rules is continuous; Aavas reported compliance-related operating expenses of INR 92 crore in FY2024 to bolster that effort.

Aavas invests in internal audits, fraud-detection systems, and risk monitoring—its credit loss provisions were INR 210 crore in FY2024—supporting balance-sheet protection and investor confidence.

- RBI/NHB compliance: ongoing oversight

- Compliance spend FY2024: INR 92 crore

- Credit loss provisions FY2024: INR 210 crore

- Strengthens governance and investor trust

Aavas: 1.2M customers, Rs22,800cr loan book, 515 branches, GNPA 0.9%

Aavas runs a 3,500+ field force and ~515 branches (9 states) to source and service 1.2M customers; FY2025 loan book Rs 22,800 crore, median disbursement 5–7 days, 2,200 RMs, weekly borrower contact. FY2024 compliance spend Rs 92 crore; credit provisions Rs 210 crore; gross NPA 0.9% (FY2025), PAR>30 0.6% (Sep 2025).

| Metric | Value |

|---|---|

| Branches | ~515 |

| Loan book | Rs 22,800 cr |

| Customers | 1.2M |

| Gross NPA | 0.9% |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas previewed here is the actual Aavas Financiers document you’ll receive—no mockups or samples. Upon purchase you’ll get this same fully structured, editable file (Word/Excel), complete with all sections, ready for presentation or analysis. What you see is what you’ll download: the full, professional deliverable with no hidden pages or placeholders.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Aavas Financiers: Scalable Profits from Affordable Housing Demand

Discover how Aavas Financiers converts niche affordable-housing demand into profitable growth—this concise Business Model Canvas outlines customer segments, unique value propositions, revenue streams, and scalable operations to inspire investors and strategists.

Partnerships

Banking and Financial Institution Alliances

Aavas Financiers partners with 20+ commercial banks and NBFCs to secure term loans and syndicated facilities, underpinning a liquidity buffer of ₹6,200 crore as of FY2024 and keeping blended cost of funds near 9.5% in FY2024. These alliances supply steady capital to support a ~22% CAGR in loan book growth (FY2021–FY2024) for rural and semi‑urban housing credit.

National Housing Bank Refinancing

The National Housing Bank (NHB) partnership gives Aavas Financiers access to low-cost refinance and liquidity; as of FY2024 NHB lines covered about 18% of Aavas’s borrowings, lowering blended funding cost by ~60 bps and enabling retail loans at sub-9% rates to low-income borrowers.

Local Contractors and Small Developers

Aavas Financiers ties with local masons, contractors, and small developers across Tier II–V towns drive lead flow, with channel-originated loans accounting for about 35% of disbursements in FY2024 (₹6.3bn of ₹18bn total home loans). These partners refer buyers for new builds and renovations, keeping Aavas the preferred grassroots financier and cutting customer acquisition cost by an estimated 22% versus branch-only sourcing.

Insurance and Ancillary Service Providers

Strategic tie-ups with life and general insurers let Aavas offer credit-linked insurance, protecting borrowers' families and cutting expected credit losses; in FY2024 Aavas reported ~12-15bps reduction in GNPA risk from insurance-covered loans.

These alliances also drive non-interest income—commissions and fees made up ~9% of Aavas' total income in FY2024, boosting ROA and diversifying revenue.

- Credit-linked insurance reduces borrower default loss

- Insurance partnerships lower portfolio risk by ~12-15bps (FY2024)

- Commissions/fees ≈9% of total income (FY2024)

Technology and Fintech Collaborators

By end-2025 Aavas Financiers expanded fintech ties, deploying alternative-data credit models that raised approval rates for thin-file borrowers by ~18% and cut NPLs by 0.6pp in pilot cohorts, boosting digital underwriting and analytics capacity.

These tech partnerships automate sourcing-to-collections workflows, reducing time-to-disbursement from 9 to 4 days and lowering servicing cost per loan ~22%.

- 18% higher approvals for thin-file

- 0.6pp NPL reduction in pilots

- Disbursement time down 5 days

- Servicing cost −22%

Aavas’ ₹6,200cr liquidity, 9.5% funding cost fuels 22% CAGR; channel & fintech cut NPLs

Aavas’s 20+ bank/NBFC partners and NHB refinance provided a ₹6,200cr liquidity buffer (FY2024), keeping blended funding cost ~9.5% and supporting ~22% loan-book CAGR (FY2021–FY2024); channel partners generated ~35% of disbursements (FY2024) while insurance and fintech ties cut expected credit loss ~12–15bps and NPLs 0.6pp, sped disbursements 9→4 days, and lifted thin-file approvals +18%.

| Metric | Value |

|---|---|

| Liquidity buffer (FY2024) | ₹6,200 crore |

| Blended cost of funds (FY2024) | ~9.5% |

| Loan-book CAGR (FY2021–FY2024) | ~22% |

| Channel-originated disbursals (FY2024) | 35% (₹6.3bn of ₹18bn) |

| NHB share of borrowings (FY2024) | ~18% |

| Insurance impact on GNPA | −12–15 bps |

| Thin-file approval lift (pilot) | +18% |

| NPL reduction (pilot) | −0.6 pp |

| Disbursement time | 9 → 4 days |

What is included in the product

A concise, pre-written Business Model Canvas for Aavas Financiers covering customer segments, channels, value propositions, revenue streams, cost structure, key resources, partners, activities, and customer relationships, reflecting real-world operations and strategic plans with SWOT-linked insights and competitive advantages; ideal for presentations, funding discussions, and decision-making by entrepreneurs and analysts.

High-level one-page Business Model Canvas for Aavas Financiers that condenses lending strategy, customer segments, and revenue streams into an editable layout—ideal for quick reviews and team collaboration.

Activities

Loan Sourcing and Lead Generation

Aavas Financiers sources loans via a 3,500+ strong field force targeting semi-urban clusters; in FY2024 it generated ~62% of new customer leads through door-to-door visits and community meetings, focusing on borrowers without formal income proof who are largely ignored by banks.

Rigorous Credit Underwriting and Appraisal

Rigorous credit underwriting at Aavas Financiers uses physical verification and cash-flow analysis to assess informal incomes; credit officers visit work and home to validate earnings for self-employed borrowers, supporting a 0.9% gross NPA reported in FY2025 and sustaining a PAR>30 of 0.6% as of Sep 2025.—this diligence lets Aavas serve 1.2 million customers across rural India while keeping asset quality high.

Loan Servicing and Collection Management

Aavas manages the loan lifecycle with rapid disbursements (median 5–7 days in FY2024) and proactive collections; a localized model uses ~2,200 relationship managers who average weekly borrower contact to sustain payment discipline.

Geographic Expansion and Branch Operations

- ~515 branches (FY2024–25)

- 9 states covered

- Loan book Rs 22,800 crore (Mar 31, 2025)

- Hub-and-spoke lowers branch Opex per loan

- Branches handle onboarding, docs, local marketing

Risk Management and Regulatory Compliance

Ensuring strict adherence to Reserve Bank of India and National Housing Bank rules is continuous; Aavas reported compliance-related operating expenses of INR 92 crore in FY2024 to bolster that effort.

Aavas invests in internal audits, fraud-detection systems, and risk monitoring—its credit loss provisions were INR 210 crore in FY2024—supporting balance-sheet protection and investor confidence.

- RBI/NHB compliance: ongoing oversight

- Compliance spend FY2024: INR 92 crore

- Credit loss provisions FY2024: INR 210 crore

- Strengthens governance and investor trust

Aavas: 1.2M customers, Rs22,800cr loan book, 515 branches, GNPA 0.9%

Aavas runs a 3,500+ field force and ~515 branches (9 states) to source and service 1.2M customers; FY2025 loan book Rs 22,800 crore, median disbursement 5–7 days, 2,200 RMs, weekly borrower contact. FY2024 compliance spend Rs 92 crore; credit provisions Rs 210 crore; gross NPA 0.9% (FY2025), PAR>30 0.6% (Sep 2025).

| Metric | Value |

|---|---|

| Branches | ~515 |

| Loan book | Rs 22,800 cr |

| Customers | 1.2M |

| Gross NPA | 0.9% |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas previewed here is the actual Aavas Financiers document you’ll receive—no mockups or samples. Upon purchase you’ll get this same fully structured, editable file (Word/Excel), complete with all sections, ready for presentation or analysis. What you see is what you’ll download: the full, professional deliverable with no hidden pages or placeholders.