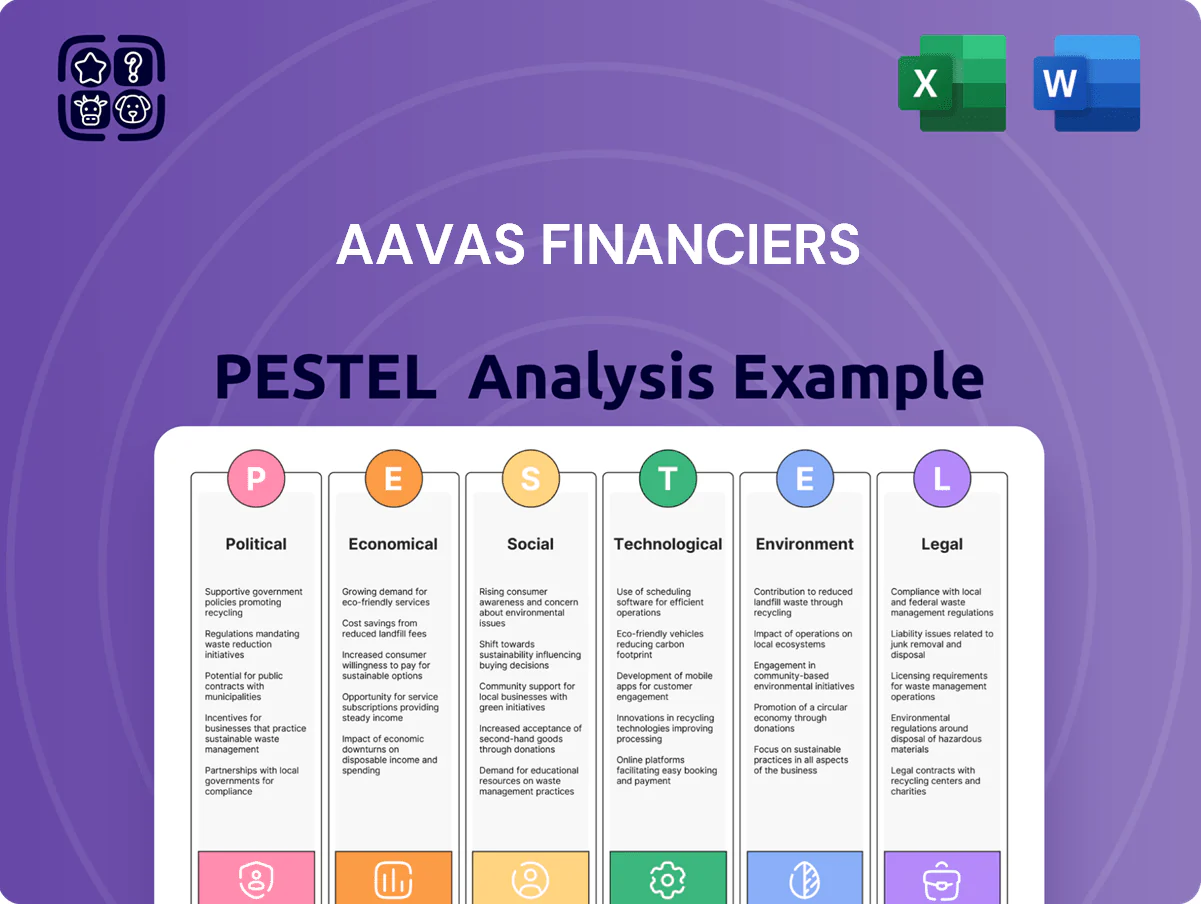

Aavas Financiers PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our targeted PESTLE Analysis for Aavas Financiers—unpack the political, economic, social, technological, legal, and environmental forces shaping its growth and risks; perfect for investors and strategists seeking actionable insights. Purchase the full report to download a ready-to-use, fully referenced analysis that accelerates decision-making and strategic planning.

Political factors

PMAY 2.0 implementation and subsidies

The continuation and expansion of PMAY-Urban and Gramin through 2025 offers Aavas a policy tailwind: PMAY targets 2.95 crore housing units (2020–25) with central subsidies that cut effective borrowing costs for low/middle-income borrowers—interest subvention schemes reduced EMIs by ~1–3 percentage points historically—supporting Aavas’ focus on semi-urban first-time buyers and sustaining loan origination growth projected at mid-teens CAGR.

State level political stability and infrastructure focus

Aavas Financiers benefits from stable state governments in Rajasthan, Gujarat and Maharashtra that have prioritized rural infrastructure; e.g., Rajasthan’s 2024–25 budget allocates ~INR 12,000 crore to rural roads and utilities, while Gujarat’s rural connectivity projects grew 18% YoY in 2024, enabling faster land-title clearances and approvals for housing projects. These investments raise collateral values in Aavas’s core micro‑home portfolio, supporting loan quality and recovery ratios.

Regulatory focus on rural development

The central government’s rural development push—including PM-KISAN payouts of 200 billion+ INR in 2024 and increased MNREGA allocations of ~1.2 trillion INR—boosts rural incomes and indirectly enhances Aavas Financiers’ borrowers’ creditworthiness; stronger rural demand cut reported rural NPA pressure, helping Aavas maintain GNPA near 0.6% in FY2024. Alignment with national schemes also eases access to institutional support and favorable policy measures.

Taxation policies for affordable housing

Fiscal tax incentives for developers and buyers remain a key lever; in FY2024 Aavas reported 38% of disbursements to affordable segment influenced by state-level stamp duty concessions and central tax benefits.

Deductions under Section 24 and 80C encourage middle-income buyers—home loan interest relief up to 200,000/yr and principal deductions up to 150,000—supporting a 22% YoY increase in retail loan applications in 2024.

Any alteration in tax slabs or new rural housing incentives (PMAY-style subsidies) would materially affect Aavas’s disbursement volumes, where rural loans comprised ~55% of total disbursements in FY2024.

- 38% disbursements tied to affordable incentives (FY2024)

- Interest deduction up to 200,000 and principal up to 150,000 drive demand

- Rural loans ~55% of disbursements (FY2024); policy shifts pose upside/downside risk

Geopolitical influence on borrowing costs

Global geopolitical tensions, such as US-China trade frictions and the 2022–2024 Russia-Ukraine shock, can tighten global liquidity and push up sovereign yields, indirectly raising Indian NBFC borrowing costs; India 10Y yield rose from 6.60% in Jan 2022 to ~7.30% in 2023 amid volatility, affecting debt pricing for players like Aavas.

Federal political stability supports predictable FII flows; net FPI inflows to India were ~INR 1.5 trillion in 2023, aiding NBFC access to capital—any erosion in stability risks sudden reversals that would raise Aavas’s cost of funds.

Aavas must actively hedge and diversify funding sources—domestic banks, bonds, and external commercial borrowings—to preserve its ~8–9% blended borrowing cost and ensure steady market access during macro-political shocks.

- Geopolitics → higher sovereign yields → pricier NBFC debt

- Federal stability sustains FII flows (~INR 1.5T in 2023)

- Diversified funding and hedges protect Aavas’s ~8–9% blended cost

Aavas: PMAY & rural spending fuel growth while rising yields and FPI flows risk funding

Policy support from PMAY (2.95Cr units to 2025) and state rural spending (Rajasthan ~INR12,000Cr FY25) underpins Aavas’s rural affordable lending—rural loans ~55% of FY2024 disbursals; tax benefits (interest deduction ₹200k, principal ₹150k) and FY2024: 38% disbursals tied to incentives sustain demand, while global yield spikes (India 10Y ~7.3% in 2023) and FPI sensitivity (~INR1.5T inflows 2023) pose funding-cost risks.

| Metric | Value |

|---|---|

| Rural share | ~55% |

| Incentive-linked disbursals | 38% |

| India 10Y (2023) | ~7.3% |

| FPI inflows (2023) | ~INR1.5T |

What is included in the product

Explores how macro-environmental forces uniquely affect Aavas Financiers across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE summary tailored for Aavas Financiers that highlights regulatory, economic, and demographic drivers—ready to drop into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest rate cycle and margins

The RBI's repo rate of 6.5% in Dec 2025 directly influences Aavas Financiers' borrowing costs and spreads, pressuring net interest margins as rural borrowers remain price-sensitive.

Quarterly NIMs of ~7.2% in FY2025 faced compression after the 2025 hikes; Aavas offsets volatility via a mix of ~55% fixed and 45% floating borrowings and active liability repricing.

Income growth in the informal sector

The economic health of self-employed and informal-income segments drives Aavas Financiers' credit demand, with India’s informal sector contributing about 45% of GDP and microenterprises expanding in Tier II/III cities; growth in small-scale industries and local services raised household incomes by ~6–8% y/y in many rural districts in 2024, improving repayment capacity for Aavas’ core borrowers. Monitoring regional indicators like GST collections, agrarian wages and rural consumption empowers calibration of underwriting for customers lacking formal income documentation.

Inflation in construction materials

Rising cement and steel prices—cement up about 18% and rebar up 22% year-on-year in 2025—plus 10–12% wage inflation for construction labor have discouraged new builds, reducing demand for housing loans in Aavas Financiers’ rural and semi-urban markets. Persistent inflation erodes disposable income for low-income borrowers, contributing to a 6–8% decline in fresh loan applications in comparable microhousing segments in FY2024–25. Aavas must factor these cost escalations into tighter loan-to-value ratios and more conservative construction-linked disbursement schedules to limit cost-overrun risks.

Liquidity conditions in the debt market

Liquidity in India’s banking system and debt markets underpins Aavas Financiers’ resource mobilization; systemic liquidity tightened in 2024 with SLR and LCR pressures but RBI liquidity injections kept 1-year G-sec yields around 7.2% in Dec 2024, enabling NCD and term-loan issuance.

Stable macro conditions in 2024–25 allowed diversification via NCDs, term loans and assignment of receivables; Aavas’ access depends on maintaining high ratings—its CARE/ICRA ratings in 2024 supported lower borrowing costs that feed into competitive customer lending rates.

- RBI liquidity operations and 1Y G-sec ~7.2% (Dec 2024)

- Diversification: NCDs, term loans, receivables assignment

- High credit ratings reduce funding cost, enabling competitive lending

Urbanization and migration patterns

Economic migration from rural to semi-urban areas fuels demand for affordable housing; India’s semi-urban population grew to ~46% in 2024, supporting a steady pipeline for small-ticket home loans.

Aavas targets peripheral corridors near industrial hubs—regions showing 7–9% annual housing demand growth—boosting loan book growth in FY2024 with retail mortgage disbursals up ~22% YoY.

- Semi-urban population ~46% (2024)

- Housing demand growth in corridors 7–9% pa

- Aavas disbursals up ~22% YoY FY2024

Aavas weathers margin squeeze via fixed/floating mix and rural demand despite input inflation

Rising repo (6.5% Dec 2025) and 1y G-sec ~7.2% (Dec 2024) squeezed NIMs (~7.2% FY2025); Aavas offsets via 55/45 fixed/floating mix and diversified funding (NCDs, term loans, receivables) supported by strong ratings. Rural income gains (household income +6–8% y/y in 2024) and semi-urban population ~46% (2024) sustain demand, but input inflation (cement +18%, rebar +22% 2025) cut new-build loan applications 6–8%.

| Metric | Value |

|---|---|

| Repo (Dec 2025) | 6.5% |

| 1y G-sec (Dec 2024) | ~7.2% |

| NIM FY2025 | ~7.2% |

| Cement / Rebar YoY (2025) | +18% / +22% |

| Semi-urban pop (2024) | ~46% |

Preview the Actual Deliverable

Aavas Financiers PESTLE Analysis

The preview shown here is the exact Aavas Financiers PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our targeted PESTLE Analysis for Aavas Financiers—unpack the political, economic, social, technological, legal, and environmental forces shaping its growth and risks; perfect for investors and strategists seeking actionable insights. Purchase the full report to download a ready-to-use, fully referenced analysis that accelerates decision-making and strategic planning.

Political factors

PMAY 2.0 implementation and subsidies

The continuation and expansion of PMAY-Urban and Gramin through 2025 offers Aavas a policy tailwind: PMAY targets 2.95 crore housing units (2020–25) with central subsidies that cut effective borrowing costs for low/middle-income borrowers—interest subvention schemes reduced EMIs by ~1–3 percentage points historically—supporting Aavas’ focus on semi-urban first-time buyers and sustaining loan origination growth projected at mid-teens CAGR.

State level political stability and infrastructure focus

Aavas Financiers benefits from stable state governments in Rajasthan, Gujarat and Maharashtra that have prioritized rural infrastructure; e.g., Rajasthan’s 2024–25 budget allocates ~INR 12,000 crore to rural roads and utilities, while Gujarat’s rural connectivity projects grew 18% YoY in 2024, enabling faster land-title clearances and approvals for housing projects. These investments raise collateral values in Aavas’s core micro‑home portfolio, supporting loan quality and recovery ratios.

Regulatory focus on rural development

The central government’s rural development push—including PM-KISAN payouts of 200 billion+ INR in 2024 and increased MNREGA allocations of ~1.2 trillion INR—boosts rural incomes and indirectly enhances Aavas Financiers’ borrowers’ creditworthiness; stronger rural demand cut reported rural NPA pressure, helping Aavas maintain GNPA near 0.6% in FY2024. Alignment with national schemes also eases access to institutional support and favorable policy measures.

Taxation policies for affordable housing

Fiscal tax incentives for developers and buyers remain a key lever; in FY2024 Aavas reported 38% of disbursements to affordable segment influenced by state-level stamp duty concessions and central tax benefits.

Deductions under Section 24 and 80C encourage middle-income buyers—home loan interest relief up to 200,000/yr and principal deductions up to 150,000—supporting a 22% YoY increase in retail loan applications in 2024.

Any alteration in tax slabs or new rural housing incentives (PMAY-style subsidies) would materially affect Aavas’s disbursement volumes, where rural loans comprised ~55% of total disbursements in FY2024.

- 38% disbursements tied to affordable incentives (FY2024)

- Interest deduction up to 200,000 and principal up to 150,000 drive demand

- Rural loans ~55% of disbursements (FY2024); policy shifts pose upside/downside risk

Geopolitical influence on borrowing costs

Global geopolitical tensions, such as US-China trade frictions and the 2022–2024 Russia-Ukraine shock, can tighten global liquidity and push up sovereign yields, indirectly raising Indian NBFC borrowing costs; India 10Y yield rose from 6.60% in Jan 2022 to ~7.30% in 2023 amid volatility, affecting debt pricing for players like Aavas.

Federal political stability supports predictable FII flows; net FPI inflows to India were ~INR 1.5 trillion in 2023, aiding NBFC access to capital—any erosion in stability risks sudden reversals that would raise Aavas’s cost of funds.

Aavas must actively hedge and diversify funding sources—domestic banks, bonds, and external commercial borrowings—to preserve its ~8–9% blended borrowing cost and ensure steady market access during macro-political shocks.

- Geopolitics → higher sovereign yields → pricier NBFC debt

- Federal stability sustains FII flows (~INR 1.5T in 2023)

- Diversified funding and hedges protect Aavas’s ~8–9% blended cost

Aavas: PMAY & rural spending fuel growth while rising yields and FPI flows risk funding

Policy support from PMAY (2.95Cr units to 2025) and state rural spending (Rajasthan ~INR12,000Cr FY25) underpins Aavas’s rural affordable lending—rural loans ~55% of FY2024 disbursals; tax benefits (interest deduction ₹200k, principal ₹150k) and FY2024: 38% disbursals tied to incentives sustain demand, while global yield spikes (India 10Y ~7.3% in 2023) and FPI sensitivity (~INR1.5T inflows 2023) pose funding-cost risks.

| Metric | Value |

|---|---|

| Rural share | ~55% |

| Incentive-linked disbursals | 38% |

| India 10Y (2023) | ~7.3% |

| FPI inflows (2023) | ~INR1.5T |

What is included in the product

Explores how macro-environmental forces uniquely affect Aavas Financiers across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis to identify threats and opportunities for executives, investors, and strategists.

A concise PESTLE summary tailored for Aavas Financiers that highlights regulatory, economic, and demographic drivers—ready to drop into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest rate cycle and margins

The RBI's repo rate of 6.5% in Dec 2025 directly influences Aavas Financiers' borrowing costs and spreads, pressuring net interest margins as rural borrowers remain price-sensitive.

Quarterly NIMs of ~7.2% in FY2025 faced compression after the 2025 hikes; Aavas offsets volatility via a mix of ~55% fixed and 45% floating borrowings and active liability repricing.

Income growth in the informal sector

The economic health of self-employed and informal-income segments drives Aavas Financiers' credit demand, with India’s informal sector contributing about 45% of GDP and microenterprises expanding in Tier II/III cities; growth in small-scale industries and local services raised household incomes by ~6–8% y/y in many rural districts in 2024, improving repayment capacity for Aavas’ core borrowers. Monitoring regional indicators like GST collections, agrarian wages and rural consumption empowers calibration of underwriting for customers lacking formal income documentation.

Inflation in construction materials

Rising cement and steel prices—cement up about 18% and rebar up 22% year-on-year in 2025—plus 10–12% wage inflation for construction labor have discouraged new builds, reducing demand for housing loans in Aavas Financiers’ rural and semi-urban markets. Persistent inflation erodes disposable income for low-income borrowers, contributing to a 6–8% decline in fresh loan applications in comparable microhousing segments in FY2024–25. Aavas must factor these cost escalations into tighter loan-to-value ratios and more conservative construction-linked disbursement schedules to limit cost-overrun risks.

Liquidity conditions in the debt market

Liquidity in India’s banking system and debt markets underpins Aavas Financiers’ resource mobilization; systemic liquidity tightened in 2024 with SLR and LCR pressures but RBI liquidity injections kept 1-year G-sec yields around 7.2% in Dec 2024, enabling NCD and term-loan issuance.

Stable macro conditions in 2024–25 allowed diversification via NCDs, term loans and assignment of receivables; Aavas’ access depends on maintaining high ratings—its CARE/ICRA ratings in 2024 supported lower borrowing costs that feed into competitive customer lending rates.

- RBI liquidity operations and 1Y G-sec ~7.2% (Dec 2024)

- Diversification: NCDs, term loans, receivables assignment

- High credit ratings reduce funding cost, enabling competitive lending

Urbanization and migration patterns

Economic migration from rural to semi-urban areas fuels demand for affordable housing; India’s semi-urban population grew to ~46% in 2024, supporting a steady pipeline for small-ticket home loans.

Aavas targets peripheral corridors near industrial hubs—regions showing 7–9% annual housing demand growth—boosting loan book growth in FY2024 with retail mortgage disbursals up ~22% YoY.

- Semi-urban population ~46% (2024)

- Housing demand growth in corridors 7–9% pa

- Aavas disbursals up ~22% YoY FY2024

Aavas weathers margin squeeze via fixed/floating mix and rural demand despite input inflation

Rising repo (6.5% Dec 2025) and 1y G-sec ~7.2% (Dec 2024) squeezed NIMs (~7.2% FY2025); Aavas offsets via 55/45 fixed/floating mix and diversified funding (NCDs, term loans, receivables) supported by strong ratings. Rural income gains (household income +6–8% y/y in 2024) and semi-urban population ~46% (2024) sustain demand, but input inflation (cement +18%, rebar +22% 2025) cut new-build loan applications 6–8%.

| Metric | Value |

|---|---|

| Repo (Dec 2025) | 6.5% |

| 1y G-sec (Dec 2024) | ~7.2% |

| NIM FY2025 | ~7.2% |

| Cement / Rebar YoY (2025) | +18% / +22% |

| Semi-urban pop (2024) | ~46% |

Preview the Actual Deliverable

Aavas Financiers PESTLE Analysis

The preview shown here is the exact Aavas Financiers PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.