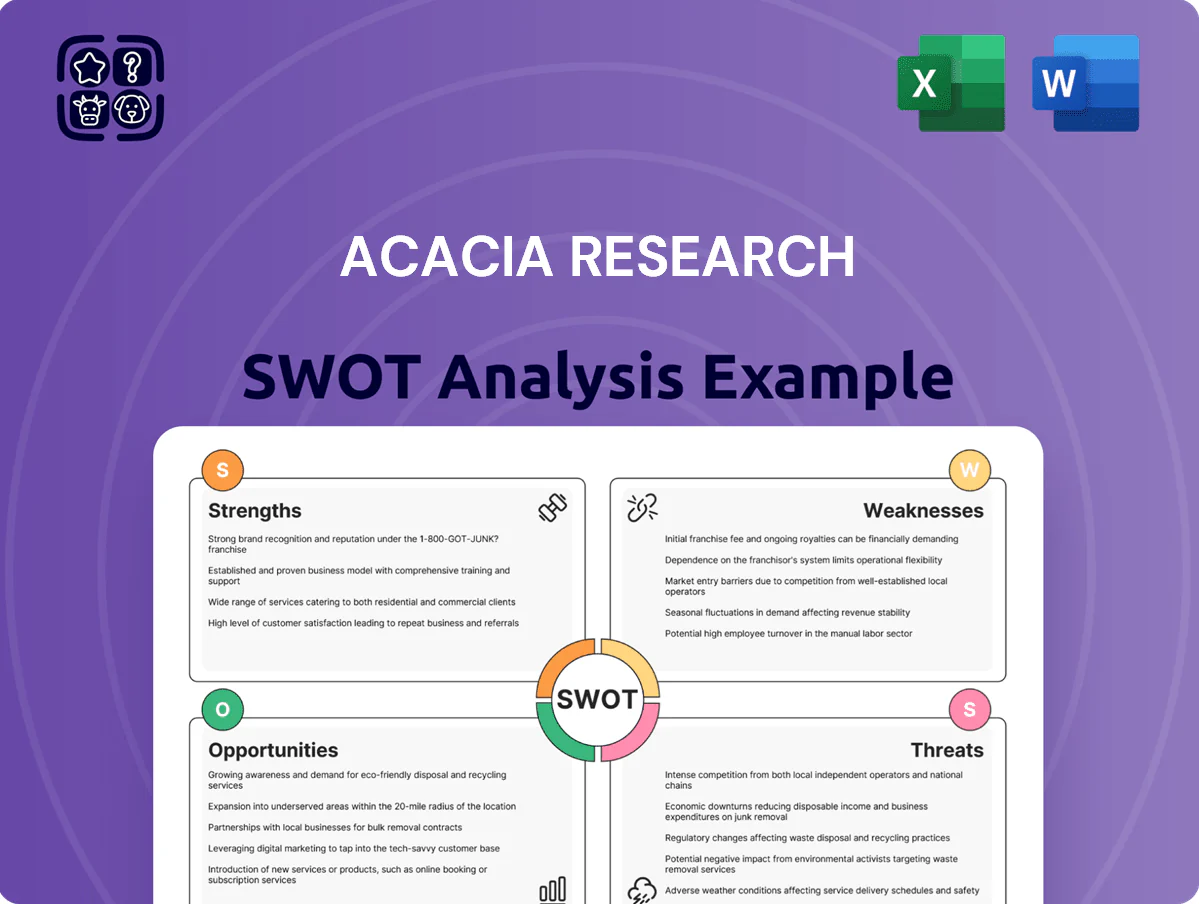

Acacia Research SWOT Analysis

Your Strategic Toolkit Starts Here

Acacia Research faces a mixed outlook—strong IP monetization expertise and strategic licensing relationships balanced against revenue cyclicality and litigation risks; our full SWOT unpacks these dynamics with financial context and actionable strategies. Purchase the complete SWOT analysis to get a professionally formatted Word report and editable Excel matrix for investment, strategy, or pitch-ready use.

Strengths

Strategic Partnership with Starboard Value

The long-term partnership with Starboard Value gives Acacia Research access to substantial capital—Starboard managed about $3.8 billion AUM in 2025—and deep corporate governance expertise, supporting disciplined value-creation plans.

Starboard’s activist track record (25+ proxy fights since 2014) helps Acacia identify undervalued IP assets and boosts credibility in negotiations and when raising debt or equity, lowering financing spreads.

Diversified Business Model

Acacia Research has shifted from pure patent licensing to a diversified holding model with operating subsidiaries like Printronix, reducing reliance on volatile legal settlements and stabilizing cash flow; for FY2024 Acacia reported consolidated revenue of $188.4m and operating income of $22.1m, with Printronix contributing ~$98m in revenue, which shows the company now captures direct operational value alongside IP monetization.

Strong Liquidity and Capital Position

As of late 2025 Acacia Research held about $220 million in cash and equivalents with under $10 million of debt, giving a net cash position near $210 million.

This strong liquidity lets Acacia move quickly on distressed or mispriced IP assets during market dislocations, often closing deals within 30–90 days.

Maintaining dry powder supports their strategy of buying assets that need immediate capital injections and remedial enforcement costs.

Deep Expertise in Intellectual Property Monetization

Acacia Research has a specialized team with decades of patent-law, licensing, and litigation experience, enabling precise valuation of complex IP and enforcement strategies that boost recoveries for inventors and partners.

The firm’s track record—over $1.2 billion in licensing recoveries since 2015 and multiple seven-figure settlements in 2024—deters infringers and attracts high-quality patent holders.

- Decades of IP law experience

- $1.2B+ recoveries since 2015

- Multiple 7-figure 2024 settlements

- Strong deterrent effect; attracts top patent owners

Disciplined Capital Allocation Framework

Management uses a strict, data-driven process to screen deals for risk-adjusted returns and clear value realization paths, deploying capital only where Acacia can influence outcomes and lift operating margins.

This focus limited speculative bets in 2025, as Acacia’s portfolio companies reported a combined 18% EBITDA margin vs. 12% peer average in the IP monetization sector.

That discipline helps protect shareholders from tech/IP froth by emphasizing fundamental value and measurable operational improvements.

- Rigorous deal screening

- Deploy only where influence exists

- 18% portfolio EBITDA (2025)

- Focus on fundamental value

Strong governance, $210M net cash & $1.2B+ recoveries fuel disciplined, profitable growth

Strong governance and $220M cash (net ~$210M) from Starboard ($3.8B AUM in 2025) enable quick IP acquisitions; diversified model (Printronix ~$98M revenue) stabilized FY2024 revenue $188.4M and operating income $22.1M; $1.2B+ recoveries since 2015 and multiple 7-figure 2024 settlements demonstrate enforcement expertise; disciplined deal screening drove 18% portfolio EBITDA (2025).

| Metric | Value |

|---|---|

| Cash | $220M |

| Net cash | $210M |

| FY2024 Rev | $188.4M |

| Printronix Rev | $98M |

| Op income | $22.1M |

| Recoveries since 2015 | $1.2B+ |

| Portfolio EBITDA (2025) | 18% |

What is included in the product

Provides a concise SWOT overview of Acacia Research, highlighting its patent licensing strengths, operational and litigation-related weaknesses, market and technology-driven opportunities, and regulatory, competitive, and IP-enforcement threats shaping its strategic outlook.

Provides a concise Acacia Research SWOT matrix for fast, visual strategy alignment and quick stakeholder briefings.

Weaknesses

Revenue Volatility and Unpredictability

Despite diversification, about 60% of Acacia Research’s 2024 adjusted revenue still tied to patent-litigation outcomes, which are hard to forecast and depend on case timing and settlements.

That lumpy revenue drove quarterly EPS swings of +120% to -90% in 2024 and a 52-week share-price range of $3.10–$7.95, raising volatility concerns.

Investors seeking steady dividend growth may find Acacia’s model too erratic given uneven cash flows and no consistent payout history.

Complexity of the Conglomerate Structure

Operating as a diversified holding with IP assets and industrial subsidiaries makes Acacia Research hard to value; as of FY2024 revenue mix—$123m licensing vs $42m industrial—investors struggle to price future cash flows consistently.

This complexity contributes to a conglomerate discount: Acacia’s EV/EBITDA of ~6.2x (Dec 2024) sits ~25% below peer-weighted sum-of-parts multiples, implying market undervaluation.

Management still finds it hard to show synergy between litigation-driven licensing and capital-intensive subsidiaries, hurting narrative clarity and investor confidence.

High Legal and Administrative Overheads

Maintaining top legal and technical teams to manage Acacia Research Corporation’s patent portfolio drives large fixed costs—legal and admin expenses were $38.5 million in 2024, about 26% of operating expenses, so teams cost money even when settlements pause.

Patent litigation is costly and slow; median US patent case spends 18–24 months and legal bills often exceed $1–3 million per case, with no guarantee of recovery, raising execution risk.

High operating expenses erode margins: Acacia reported a 2024 operating margin of roughly 12%, so slower settlement activity or unfavorable rulings can materially cut profits.

Dependence on Key Personnel

Acacia’s strategy depends on a small team of senior execs and partners with niche deal-making and legal skills; losing them would impair revenue generation tied to patents and licensing, which contributed $92.3M of royalty/licensing income in 2024.

Any shift with activist investor Starboard Value, which held ~9.8% at year-end 2024, could change board dynamics and strategy execution.

Retention is hard: private equity and IP-law talent command premium pay—turnover would raise costs and slow deal flow.

- Key-person risk: small leadership pool

- $92.3M licensing revenue in 2024

- Starboard ~9.8% stake (2024)

- High-cost competition for IP/legal talent

Limited Market Recognition and Liquidity

As a small-cap (market cap ~US$150m as of Dec 31, 2025) with a niche licensing model, Acacia Research gets limited sell-side coverage and lower average daily volume (~60k shares), which reduces visibility and can keep the stock below intrinsic value even when fundamentals improve.

Smaller float raises sensitivity to market swings and institutional selling; during 2022–2024 macro shocks the stock fell ~45% versus the S&P 500 down ~10%, showing higher volatility and downside risk.

- Market cap ~US$150m (Dec 31, 2025)

- Avg daily volume ~60k shares

- Stock volatility > S&P 500 (2022–24: −45% vs −10%)

- Limited analyst coverage, higher institutional selling risk

Litigation-Driven, Highly Volatile Microcap: Big Legal Costs, Tight Float, Execution Risk

Heavy reliance on patent-litigation drives lumpy, unpredictable revenue (≈60% of 2024 adjusted revenue), large EPS swings (+120% to −90% in 2024) and high volatility (2022–24: −45% vs S&P −10%); high fixed legal costs ($38.5M in 2024) and key-person risk (small senior team) raise execution risk; limited float (avg vol ~60k) and market cap ≈$150M (Dec 31, 2025) reduce visibility.

| Metric | Value |

|---|---|

| Patent-litigation share | ~60% (2024) |

| Legal/admin costs | $38.5M (2024) |

| EPS swing | +120% to −90% (2024) |

| Market cap | $150M (Dec 31, 2025) |

| Avg daily vol | ~60k shares |

Full Version Awaits

Acacia Research SWOT Analysis

This preview is the actual Acacia Research SWOT analysis document you’ll receive upon purchase—no samples, just the full professional report ready for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Acacia Research faces a mixed outlook—strong IP monetization expertise and strategic licensing relationships balanced against revenue cyclicality and litigation risks; our full SWOT unpacks these dynamics with financial context and actionable strategies. Purchase the complete SWOT analysis to get a professionally formatted Word report and editable Excel matrix for investment, strategy, or pitch-ready use.

Strengths

Strategic Partnership with Starboard Value

The long-term partnership with Starboard Value gives Acacia Research access to substantial capital—Starboard managed about $3.8 billion AUM in 2025—and deep corporate governance expertise, supporting disciplined value-creation plans.

Starboard’s activist track record (25+ proxy fights since 2014) helps Acacia identify undervalued IP assets and boosts credibility in negotiations and when raising debt or equity, lowering financing spreads.

Diversified Business Model

Acacia Research has shifted from pure patent licensing to a diversified holding model with operating subsidiaries like Printronix, reducing reliance on volatile legal settlements and stabilizing cash flow; for FY2024 Acacia reported consolidated revenue of $188.4m and operating income of $22.1m, with Printronix contributing ~$98m in revenue, which shows the company now captures direct operational value alongside IP monetization.

Strong Liquidity and Capital Position

As of late 2025 Acacia Research held about $220 million in cash and equivalents with under $10 million of debt, giving a net cash position near $210 million.

This strong liquidity lets Acacia move quickly on distressed or mispriced IP assets during market dislocations, often closing deals within 30–90 days.

Maintaining dry powder supports their strategy of buying assets that need immediate capital injections and remedial enforcement costs.

Deep Expertise in Intellectual Property Monetization

Acacia Research has a specialized team with decades of patent-law, licensing, and litigation experience, enabling precise valuation of complex IP and enforcement strategies that boost recoveries for inventors and partners.

The firm’s track record—over $1.2 billion in licensing recoveries since 2015 and multiple seven-figure settlements in 2024—deters infringers and attracts high-quality patent holders.

- Decades of IP law experience

- $1.2B+ recoveries since 2015

- Multiple 7-figure 2024 settlements

- Strong deterrent effect; attracts top patent owners

Disciplined Capital Allocation Framework

Management uses a strict, data-driven process to screen deals for risk-adjusted returns and clear value realization paths, deploying capital only where Acacia can influence outcomes and lift operating margins.

This focus limited speculative bets in 2025, as Acacia’s portfolio companies reported a combined 18% EBITDA margin vs. 12% peer average in the IP monetization sector.

That discipline helps protect shareholders from tech/IP froth by emphasizing fundamental value and measurable operational improvements.

- Rigorous deal screening

- Deploy only where influence exists

- 18% portfolio EBITDA (2025)

- Focus on fundamental value

Strong governance, $210M net cash & $1.2B+ recoveries fuel disciplined, profitable growth

Strong governance and $220M cash (net ~$210M) from Starboard ($3.8B AUM in 2025) enable quick IP acquisitions; diversified model (Printronix ~$98M revenue) stabilized FY2024 revenue $188.4M and operating income $22.1M; $1.2B+ recoveries since 2015 and multiple 7-figure 2024 settlements demonstrate enforcement expertise; disciplined deal screening drove 18% portfolio EBITDA (2025).

| Metric | Value |

|---|---|

| Cash | $220M |

| Net cash | $210M |

| FY2024 Rev | $188.4M |

| Printronix Rev | $98M |

| Op income | $22.1M |

| Recoveries since 2015 | $1.2B+ |

| Portfolio EBITDA (2025) | 18% |

What is included in the product

Provides a concise SWOT overview of Acacia Research, highlighting its patent licensing strengths, operational and litigation-related weaknesses, market and technology-driven opportunities, and regulatory, competitive, and IP-enforcement threats shaping its strategic outlook.

Provides a concise Acacia Research SWOT matrix for fast, visual strategy alignment and quick stakeholder briefings.

Weaknesses

Revenue Volatility and Unpredictability

Despite diversification, about 60% of Acacia Research’s 2024 adjusted revenue still tied to patent-litigation outcomes, which are hard to forecast and depend on case timing and settlements.

That lumpy revenue drove quarterly EPS swings of +120% to -90% in 2024 and a 52-week share-price range of $3.10–$7.95, raising volatility concerns.

Investors seeking steady dividend growth may find Acacia’s model too erratic given uneven cash flows and no consistent payout history.

Complexity of the Conglomerate Structure

Operating as a diversified holding with IP assets and industrial subsidiaries makes Acacia Research hard to value; as of FY2024 revenue mix—$123m licensing vs $42m industrial—investors struggle to price future cash flows consistently.

This complexity contributes to a conglomerate discount: Acacia’s EV/EBITDA of ~6.2x (Dec 2024) sits ~25% below peer-weighted sum-of-parts multiples, implying market undervaluation.

Management still finds it hard to show synergy between litigation-driven licensing and capital-intensive subsidiaries, hurting narrative clarity and investor confidence.

High Legal and Administrative Overheads

Maintaining top legal and technical teams to manage Acacia Research Corporation’s patent portfolio drives large fixed costs—legal and admin expenses were $38.5 million in 2024, about 26% of operating expenses, so teams cost money even when settlements pause.

Patent litigation is costly and slow; median US patent case spends 18–24 months and legal bills often exceed $1–3 million per case, with no guarantee of recovery, raising execution risk.

High operating expenses erode margins: Acacia reported a 2024 operating margin of roughly 12%, so slower settlement activity or unfavorable rulings can materially cut profits.

Dependence on Key Personnel

Acacia’s strategy depends on a small team of senior execs and partners with niche deal-making and legal skills; losing them would impair revenue generation tied to patents and licensing, which contributed $92.3M of royalty/licensing income in 2024.

Any shift with activist investor Starboard Value, which held ~9.8% at year-end 2024, could change board dynamics and strategy execution.

Retention is hard: private equity and IP-law talent command premium pay—turnover would raise costs and slow deal flow.

- Key-person risk: small leadership pool

- $92.3M licensing revenue in 2024

- Starboard ~9.8% stake (2024)

- High-cost competition for IP/legal talent

Limited Market Recognition and Liquidity

As a small-cap (market cap ~US$150m as of Dec 31, 2025) with a niche licensing model, Acacia Research gets limited sell-side coverage and lower average daily volume (~60k shares), which reduces visibility and can keep the stock below intrinsic value even when fundamentals improve.

Smaller float raises sensitivity to market swings and institutional selling; during 2022–2024 macro shocks the stock fell ~45% versus the S&P 500 down ~10%, showing higher volatility and downside risk.

- Market cap ~US$150m (Dec 31, 2025)

- Avg daily volume ~60k shares

- Stock volatility > S&P 500 (2022–24: −45% vs −10%)

- Limited analyst coverage, higher institutional selling risk

Litigation-Driven, Highly Volatile Microcap: Big Legal Costs, Tight Float, Execution Risk

Heavy reliance on patent-litigation drives lumpy, unpredictable revenue (≈60% of 2024 adjusted revenue), large EPS swings (+120% to −90% in 2024) and high volatility (2022–24: −45% vs S&P −10%); high fixed legal costs ($38.5M in 2024) and key-person risk (small senior team) raise execution risk; limited float (avg vol ~60k) and market cap ≈$150M (Dec 31, 2025) reduce visibility.

| Metric | Value |

|---|---|

| Patent-litigation share | ~60% (2024) |

| Legal/admin costs | $38.5M (2024) |

| EPS swing | +120% to −90% (2024) |

| Market cap | $150M (Dec 31, 2025) |

| Avg daily vol | ~60k shares |

Full Version Awaits

Acacia Research SWOT Analysis

This preview is the actual Acacia Research SWOT analysis document you’ll receive upon purchase—no samples, just the full professional report ready for download.