Acceptance Insurance SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Acceptance Insurance shows resilient niche positioning in specialty personal lines and a customer-centric claims model, but faces regulatory and catastrophe exposure risks that could pressure margins; its growth hinges on digital transformation and geographic expansion. Discover the full SWOT analysis for actionable insights, financial context, and editable deliverables to support investment, strategy, or advisory decisions.

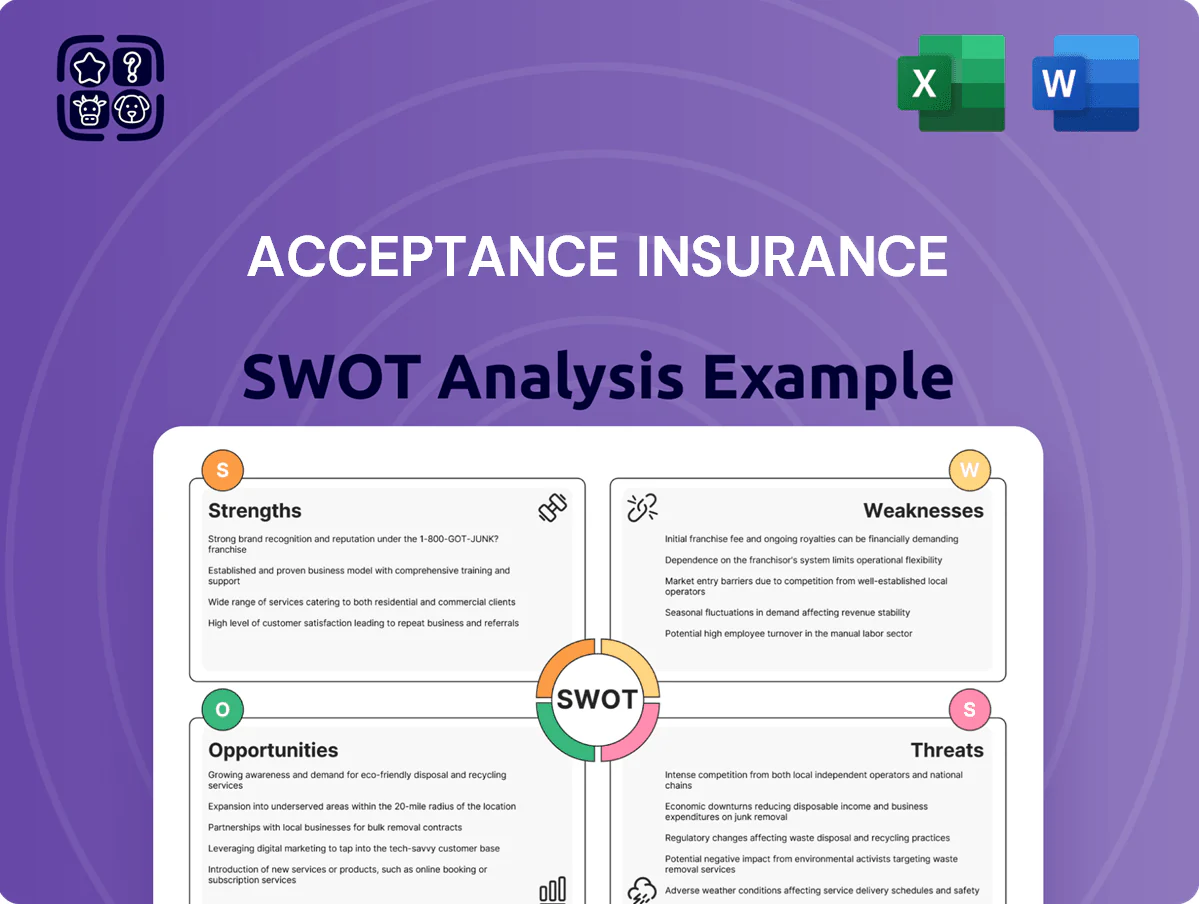

Strengths

Deep Expertise in Non-Standard Auto Segments

Acceptance Insurance holds a clear edge in non-standard auto insurance, underwriting high-risk drivers that larger carriers avoid; by year-end 2025 it served roughly 520,000 policies, up 4% YoY, concentrating on drivers with prior violations or credit issues.

Robust Multi-Channel Distribution Network

Acceptance Insurance uses over 300 retail locations, a network of independent agents, and a growing digital platform, giving it broad multi-channel reach; in 2024 direct written premium was $1.1 billion, reflecting channel synergies. The strong local footprint enables face-to-face service that builds trust with customers who prefer in-person interactions, particularly in underserved regions. By 2025 this channel integration expanded geographic reach across 12 states while keeping persistency rates above 80%, supporting customer engagement and retention.

Flexible Payment and Product Options

Acceptance Insurance boosts acquisition by offering low down payments (often under $100) and flexible installment plans, appealing to budget-conscious drivers where 2024 CFPB data shows subprime auto borrowers made 28% of new loans. Ancillary products—roadside assistance and hospital indemnity—lift revenue per policy by an estimated 12–18% per policy in 2023, improving lifetime value in a price-sensitive market.

Proven Operational Resilience and Security

By early 2026 Acceptance Corporation improved detection and recovery from cyber threats, cutting mean-time-to-recover for ransomware incidents from 48 to 8 hours and avoiding any customer-impacting outages in 2025.

That tech maturity preserved regulatory compliance and policyholder data, supporting a 6% retention uplift in 2025 and preventing estimated remediation costs of $4.2M.

Migration off legacy systems freed ~18% of IT budget, boosting automation and accelerating new-product time-to-market.

- MTTR down 48→8 hrs

- Zero customer outages in 2025

- 2025 retention +6%

- Estimated avoided remediation $4.2M

- IT budget freed ~18%

Strong Brand Recognition and Customer Loyalty

With over 50 years in the market, Acceptance Insurance has a brand that resonates with its core demographic as a reliable, accessible provider; renewal rates were ~64% in 2024, supporting retention despite competition.

Customer testimonials cite competitive pricing and helpful support teams for policy updates; Net Promoter Score (NPS) was reported near 28 in 2024, reflecting positive sentiment.

This positive sentiment and consistent service delivery provide a stable foundation for retaining customers as market competition intensifies.

- 50+ years' tenure

- 2024 renewal rate ~64%

- 2024 NPS ~28

- Competitive pricing cited by customers

Acceptance Insurance: $1.1B DWP, 520K policies, 80% retention, cyber MTTR 48→8 hrs

Acceptance Insurance dominates non-standard auto insurance with ~520,000 policies (2025), $1.1B direct written premium (2024), >300 retail locations across 12 states, retention ~80% (2025) and renewal ~64% (2024); cyber MTTR fell 48→8 hrs, saving ~$4.2M and freeing ~18% of IT budget, while ancillary sales raise revenue per policy ~15%.

| Metric | Value |

|---|---|

| Policies (2025) | ~520,000 |

| DWP (2024) | $1.1B |

| Retail locations | >300 |

| States | 12 |

| Retention (2025) | ~80% |

| Renewal (2024) | ~64% |

| NPS (2024) | ~28 |

| Ancillary lift | ~15% rev/policy |

| Cyber MTTR | 48→8 hrs |

| IT budget freed | ~18% |

| Avoided remediation | $4.2M |

What is included in the product

Delivers a strategic overview of Acceptance Insurance’s internal and external business factors, outlining its strengths, weaknesses, opportunities, and threats to clarify competitive position and future risks.

Provides a concise Acceptance Insurance SWOT matrix for fast, visual strategy alignment and quick stakeholder presentations, ideal for executives needing a snapshot of competitive positioning.

Weaknesses

Impact of Loss Severity on Profitability

In 2025 Acceptance Insurance reported a decline in net income as physical damage loss severity rose, with combined ratio pressure pushing it above 100% in several quarters and net income down about 18% year‑over‑year through Q3 2025.

Auto parts costs rose roughly 12–15% vs. 2023 due to inflation and tariff uncertainty, making average claim severity materially higher and raising per‑claim payouts.

Higher loss severity squeezed underwriting margins, forcing frequent pricing updates and tighter rate filings to restore profitability.

Geographic Concentration in Select States

Acceptance Insurance’s footprint spans 14 states, but top three states accounted for about 62% of 2024 premiums written, so regional recessions or state rule changes could cut volumes sharply.

State-level regulatory shifts—like Florida’s 2023 rate reforms—show how legal changes can force price compression and uplift claims, increasing volatility in premium income.

Expanding beyond core regions is costly: 2024 customer acquisition cost in new markets rose ~35%, and building local distribution and underwriting expertise limits rapid diversification.

Higher Underwriting Expense Ratios

The non-standard auto segment typically posts underwriting expense ratios 5–10 pts higher than standard lines; in 2024 Acceptance Insurance Group (Aingo Insurance Group Inc. proxy) reported a combined ratio near 104–108% in some quarters, reflecting elevated expense pressure. Frequent cancellations, non-payments, and intensive vetting for high-risk drivers drive higher policy acquisition and servicing costs, raising loss-adjusted overhead. For Acceptance, keeping premiums affordable for price-sensitive customers while covering these transaction-heavy costs compresses underwriting margin and caps expansion. What this estimate hides: reinsurance and digital-servicing gains can slightly offset but not eliminate the drag.

Sensitivity to Macroeconomic Policy Shifts

The company’s earnings swing sharply with macro moves: a 2024 IHS Markit estimate showed US auto parts import tariffs could raise average repair costs by 8–12%, squeezing margins when regulatory approval delays prevent timely premium hikes.

Regulatory lag in many states averages 6–9 months for rate filings (NAIC 2023), so sudden tariff-driven cost spikes can outpace revenue adjustments, raising combined ratios above 100% quickly.

Dependence on trade policy and politics—2021–24 tariff headlines and semiconductor shortages—adds volatility the firm cannot control, increasing underwriting risk and capital strain.

- Repair-cost sensitivity: +8–12% (IHS Markit 2024)

- Rate-filing lag: 6–9 months (NAIC 2023)

- Combined-ratio risk: can exceed 100% after shocks

Dependence on Reinsurance for Risk Mitigation

Acceptance relies on large reinsurance treaties to cap losses and protect solvency, with 2025 reports showing ceded premiums around 28% of gross written premium, reducing net revenue.

This protection raises vulnerability: if reinsurance markets harden and rates rise (industry loss-cost increases of 15–25% in 2024–25), Acceptance’s ceded costs would climb and compress margins.

What this hides: heavy ceded ratios limit upside from premium growth and tie profitability to third-party capacity.

- 2025 ceded ≈28% of GWP

- 2024–25 market rate increases 15–25%

- Higher reinsurance costs shrink net premiums

Rising claims, concentrated premiums and heavy reinsurance squeeze insurer margins in 2025

Underwriting losses rose as combined ratios exceeded 100% in multiple 2025 quarters, driving an ~18% YTD net income decline through Q3 2025; claim severity jumped 12–15% vs 2023 from parts inflation and tariffs. Top three states made up ~62% of 2024 premiums, concentrating geographic risk, while rate‑filing lags (6–9 months) and heavy reinsurance (ceded ≈28% of GWP in 2025) compress margins and limit upside.

| Metric | Value |

|---|---|

| YTD net income change (through Q3 2025) | −18% |

| Claim severity increase vs 2023 | 12–15% |

| Top 3 states premium share (2024) | ≈62% |

| Rate‑filing lag (NAIC) | 6–9 months |

| Ceded premiums (2025) | ≈28% of GWP |

What You See Is What You Get

Acceptance Insurance SWOT Analysis

This is the actual Acceptance Insurance SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version with in-depth insights and strategic implications.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Acceptance Insurance shows resilient niche positioning in specialty personal lines and a customer-centric claims model, but faces regulatory and catastrophe exposure risks that could pressure margins; its growth hinges on digital transformation and geographic expansion. Discover the full SWOT analysis for actionable insights, financial context, and editable deliverables to support investment, strategy, or advisory decisions.

Strengths

Deep Expertise in Non-Standard Auto Segments

Acceptance Insurance holds a clear edge in non-standard auto insurance, underwriting high-risk drivers that larger carriers avoid; by year-end 2025 it served roughly 520,000 policies, up 4% YoY, concentrating on drivers with prior violations or credit issues.

Robust Multi-Channel Distribution Network

Acceptance Insurance uses over 300 retail locations, a network of independent agents, and a growing digital platform, giving it broad multi-channel reach; in 2024 direct written premium was $1.1 billion, reflecting channel synergies. The strong local footprint enables face-to-face service that builds trust with customers who prefer in-person interactions, particularly in underserved regions. By 2025 this channel integration expanded geographic reach across 12 states while keeping persistency rates above 80%, supporting customer engagement and retention.

Flexible Payment and Product Options

Acceptance Insurance boosts acquisition by offering low down payments (often under $100) and flexible installment plans, appealing to budget-conscious drivers where 2024 CFPB data shows subprime auto borrowers made 28% of new loans. Ancillary products—roadside assistance and hospital indemnity—lift revenue per policy by an estimated 12–18% per policy in 2023, improving lifetime value in a price-sensitive market.

Proven Operational Resilience and Security

By early 2026 Acceptance Corporation improved detection and recovery from cyber threats, cutting mean-time-to-recover for ransomware incidents from 48 to 8 hours and avoiding any customer-impacting outages in 2025.

That tech maturity preserved regulatory compliance and policyholder data, supporting a 6% retention uplift in 2025 and preventing estimated remediation costs of $4.2M.

Migration off legacy systems freed ~18% of IT budget, boosting automation and accelerating new-product time-to-market.

- MTTR down 48→8 hrs

- Zero customer outages in 2025

- 2025 retention +6%

- Estimated avoided remediation $4.2M

- IT budget freed ~18%

Strong Brand Recognition and Customer Loyalty

With over 50 years in the market, Acceptance Insurance has a brand that resonates with its core demographic as a reliable, accessible provider; renewal rates were ~64% in 2024, supporting retention despite competition.

Customer testimonials cite competitive pricing and helpful support teams for policy updates; Net Promoter Score (NPS) was reported near 28 in 2024, reflecting positive sentiment.

This positive sentiment and consistent service delivery provide a stable foundation for retaining customers as market competition intensifies.

- 50+ years' tenure

- 2024 renewal rate ~64%

- 2024 NPS ~28

- Competitive pricing cited by customers

Acceptance Insurance: $1.1B DWP, 520K policies, 80% retention, cyber MTTR 48→8 hrs

Acceptance Insurance dominates non-standard auto insurance with ~520,000 policies (2025), $1.1B direct written premium (2024), >300 retail locations across 12 states, retention ~80% (2025) and renewal ~64% (2024); cyber MTTR fell 48→8 hrs, saving ~$4.2M and freeing ~18% of IT budget, while ancillary sales raise revenue per policy ~15%.

| Metric | Value |

|---|---|

| Policies (2025) | ~520,000 |

| DWP (2024) | $1.1B |

| Retail locations | >300 |

| States | 12 |

| Retention (2025) | ~80% |

| Renewal (2024) | ~64% |

| NPS (2024) | ~28 |

| Ancillary lift | ~15% rev/policy |

| Cyber MTTR | 48→8 hrs |

| IT budget freed | ~18% |

| Avoided remediation | $4.2M |

What is included in the product

Delivers a strategic overview of Acceptance Insurance’s internal and external business factors, outlining its strengths, weaknesses, opportunities, and threats to clarify competitive position and future risks.

Provides a concise Acceptance Insurance SWOT matrix for fast, visual strategy alignment and quick stakeholder presentations, ideal for executives needing a snapshot of competitive positioning.

Weaknesses

Impact of Loss Severity on Profitability

In 2025 Acceptance Insurance reported a decline in net income as physical damage loss severity rose, with combined ratio pressure pushing it above 100% in several quarters and net income down about 18% year‑over‑year through Q3 2025.

Auto parts costs rose roughly 12–15% vs. 2023 due to inflation and tariff uncertainty, making average claim severity materially higher and raising per‑claim payouts.

Higher loss severity squeezed underwriting margins, forcing frequent pricing updates and tighter rate filings to restore profitability.

Geographic Concentration in Select States

Acceptance Insurance’s footprint spans 14 states, but top three states accounted for about 62% of 2024 premiums written, so regional recessions or state rule changes could cut volumes sharply.

State-level regulatory shifts—like Florida’s 2023 rate reforms—show how legal changes can force price compression and uplift claims, increasing volatility in premium income.

Expanding beyond core regions is costly: 2024 customer acquisition cost in new markets rose ~35%, and building local distribution and underwriting expertise limits rapid diversification.

Higher Underwriting Expense Ratios

The non-standard auto segment typically posts underwriting expense ratios 5–10 pts higher than standard lines; in 2024 Acceptance Insurance Group (Aingo Insurance Group Inc. proxy) reported a combined ratio near 104–108% in some quarters, reflecting elevated expense pressure. Frequent cancellations, non-payments, and intensive vetting for high-risk drivers drive higher policy acquisition and servicing costs, raising loss-adjusted overhead. For Acceptance, keeping premiums affordable for price-sensitive customers while covering these transaction-heavy costs compresses underwriting margin and caps expansion. What this estimate hides: reinsurance and digital-servicing gains can slightly offset but not eliminate the drag.

Sensitivity to Macroeconomic Policy Shifts

The company’s earnings swing sharply with macro moves: a 2024 IHS Markit estimate showed US auto parts import tariffs could raise average repair costs by 8–12%, squeezing margins when regulatory approval delays prevent timely premium hikes.

Regulatory lag in many states averages 6–9 months for rate filings (NAIC 2023), so sudden tariff-driven cost spikes can outpace revenue adjustments, raising combined ratios above 100% quickly.

Dependence on trade policy and politics—2021–24 tariff headlines and semiconductor shortages—adds volatility the firm cannot control, increasing underwriting risk and capital strain.

- Repair-cost sensitivity: +8–12% (IHS Markit 2024)

- Rate-filing lag: 6–9 months (NAIC 2023)

- Combined-ratio risk: can exceed 100% after shocks

Dependence on Reinsurance for Risk Mitigation

Acceptance relies on large reinsurance treaties to cap losses and protect solvency, with 2025 reports showing ceded premiums around 28% of gross written premium, reducing net revenue.

This protection raises vulnerability: if reinsurance markets harden and rates rise (industry loss-cost increases of 15–25% in 2024–25), Acceptance’s ceded costs would climb and compress margins.

What this hides: heavy ceded ratios limit upside from premium growth and tie profitability to third-party capacity.

- 2025 ceded ≈28% of GWP

- 2024–25 market rate increases 15–25%

- Higher reinsurance costs shrink net premiums

Rising claims, concentrated premiums and heavy reinsurance squeeze insurer margins in 2025

Underwriting losses rose as combined ratios exceeded 100% in multiple 2025 quarters, driving an ~18% YTD net income decline through Q3 2025; claim severity jumped 12–15% vs 2023 from parts inflation and tariffs. Top three states made up ~62% of 2024 premiums, concentrating geographic risk, while rate‑filing lags (6–9 months) and heavy reinsurance (ceded ≈28% of GWP in 2025) compress margins and limit upside.

| Metric | Value |

|---|---|

| YTD net income change (through Q3 2025) | −18% |

| Claim severity increase vs 2023 | 12–15% |

| Top 3 states premium share (2024) | ≈62% |

| Rate‑filing lag (NAIC) | 6–9 months |

| Ceded premiums (2025) | ≈28% of GWP |

What You See Is What You Get

Acceptance Insurance SWOT Analysis

This is the actual Acceptance Insurance SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; buy now to unlock the complete, editable version with in-depth insights and strategic implications.