Acciona Boston Consulting Group Matrix

See the Bigger Picture

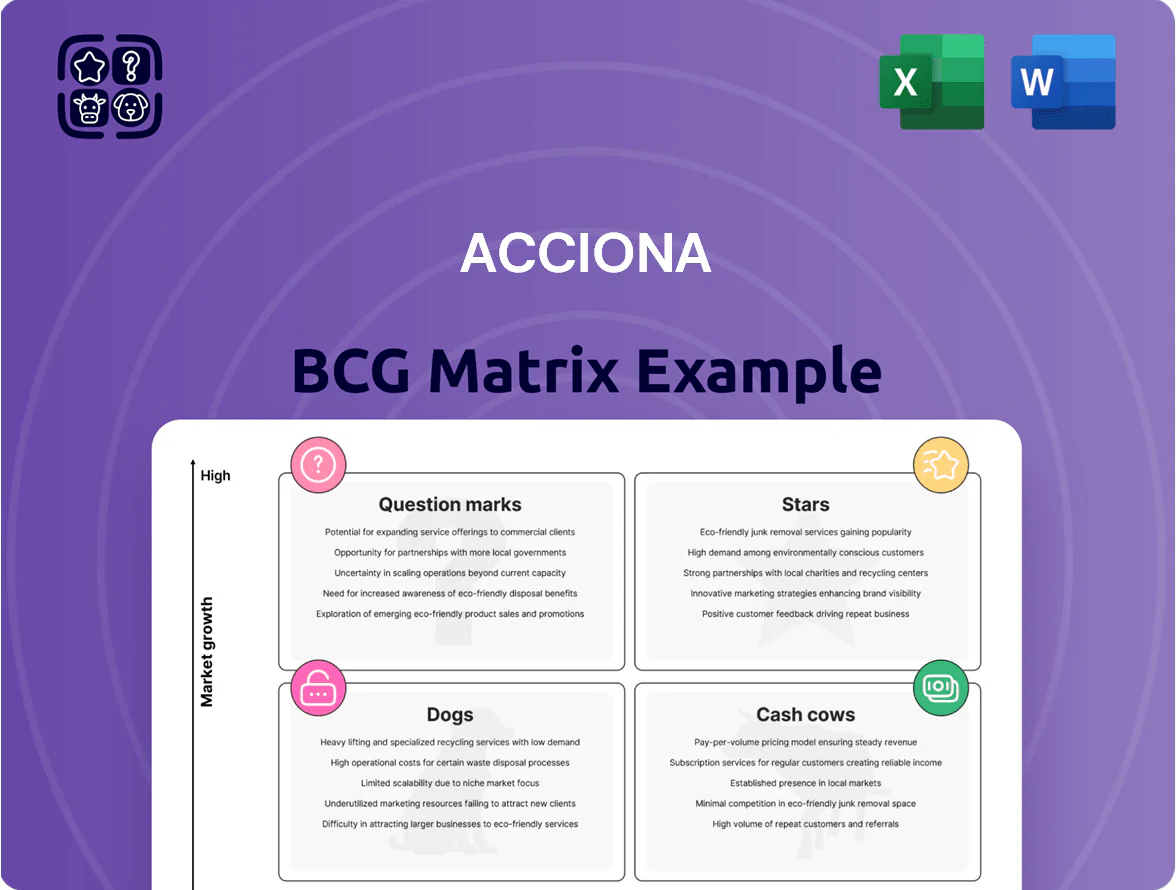

Acciona’s BCG Matrix preview highlights how its core segments—renewable energy, infrastructure, and water—stack up on market growth and relative share, revealing early Stars in renewables and potential Cash Cows in long-term concessions. This snapshot hints at where capital should flow and which businesses may need divestment or reinvestment. Purchase the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and a ready-to-use strategic report in Word and Excel to accelerate confident decisions.

Stars

Utility Scale Solar PV Expansion

By end-2025 Acciona held ~6 GW of utility-scale PV capacity globally, leading large-scale projects in North America and Australia and capturing ~12% market share in those regions.

Strong corporate demand and decarbonization policies drove contracted PPA revenues, with average project IRRs of 7–9% and expected EBITDA margins >25% once operational.

High upfront capex—land, panels, grid works—raised initial leverage (net debt/EBITDA ~4x at peak build), but scale boosts procurement savings and grid access.

As installations stabilize and debt amortizes over 15–20 years, these assets are set to become cash cows, generating steady free cash flow and supporting reinvestment.

Desalination and Water Treatment

Acciona’s Desalination and Water Treatment is a Star — global desalination demand is rising 7% annually and Acciona holds roughly 18% share in MENA desalination projects as of 2025, driven by GCC and North Africa contracts totaling €1.2bn backlog. Heavy R&D spend (≈€75m in 2024) on membrane tech sustains a tech lead but burns cash, keeping capex intensity high. This unit underpins Acciona’s long-term sustainability credentials and draws ESG-focused institutional capital seeking water-security exposure.

Australian Transport Infrastructure

Australian Transport Infrastructure is a Star for Acciona, driven by A$110bn federal and state transport commitments to 2028 and 8–10% annual sector growth, making Australia a primary growth engine for Acciona’s infrastructure arm.

Acciona holds ~25–30% share in complex tunneling and bridge projects, securing high-value contracts worth ~A$2.1bn through 2025 and reinforcing its market leadership.

High regional growth forces ongoing reinvestment—CapEx of ~A$120–160m annually in heavy machinery and local crews—to sustain margins and capacity.

Sustained Australian success is vital to offset flat-to-negative revenue growth in mature European markets, where Acciona’s infrastructure revenue growth slowed to ~1% in 2024.

Offshore Wind Development

Offshore wind is a high-growth star for Acciona, using its maritime engineering to bid on Northern Hemisphere tenders where 2030 capacity additions are forecast at ~90 GW annually (IEA 2024); Acciona’s project pipeline reached ~3.2 GW by end-2025, showing scale potential despite heavy capex.

High barriers—specialized vessels, grid hooks, consenting—raise upfront costs (LCOE range €60–€120/MWh); success needs long-term grid contracts and regulatory navigation to secure market dominance.

- 2030 market growth ~90 GW/year (IEA 2024)

- Acciona pipeline ~3.2 GW (end-2025)

- LCOE €60–€120/MWh

- Key risks: capex intensity, permitting, grid contracts

Specialized Social Infrastructure

Acciona’s high-tech hospitals and research centers are a Star: global demand for advanced healthcare facilities is growing ~6.5% CAGR to 2028, and Acciona holds a leading PPP market share in Spain and LATAM with ~25–30% of large healthcare PPPs.

Combining construction plus 20–30 year management contracts yields recurring revenue; a €200–€400m typical project boosts backlog and EBITDA margin via services.

High sector growth as governments retrofit aging hospitals; EU recovery funds and Latin American health spending lift annual capex by billions.

- 6.5% global market CAGR to 2028

- 25–30% market share in regional PPPs

- €200–€400m typical project size

- Ongoing investment: digital twins, energy-efficiency

Acciona: 6GW PV, €1.2bn desal backlog, A$2.1bn transport, 3.2GW offshore, strong PPP hospitals

Acciona Stars: utility-scale PV (~6 GW end-2025, ~12% NA/AU share; IRR 7–9%, EBITDA >25%), desalination (18% MENA share, €1.2bn backlog, €75m R&D 2024), Australian transport (A$2.1bn contracts, 25–30% tunneling share, A$120–160m annual CapEx), offshore wind (3.2 GW pipeline end-2025, LCOE €60–120/MWh), hospitals (25–30% PPP share, €200–400m projects).

| Unit | Key metric |

|---|---|

| PV | 6 GW; 12% NA/AU; IRR 7–9% |

| Desal | 18% MENA; €1.2bn backlog |

| Aus Transport | A$2.1bn; 25–30% share |

| Offshore | 3.2 GW pipeline; €60–120/MWh |

| Hospitals | 25–30% PPP; €200–400m |

What is included in the product

BCG Matrix of Acciona: quadrant-by-quadrant strategic review with investment, hold/divest recommendations and trend-based risks/opportunities.

One-page Acciona BCG Matrix placing each business unit in a quadrant for swift strategic clarity.

Cash Cows

Spanish Onshore Wind Portfolios

Acciona’s Spanish onshore wind portfolios sit in a mature market with >40% domestic onshore share in regions like Castilla y León and Navarra, delivering stable EBITDA margins ~65% and predictable cash flows from long-term PPAs that cover ~70% of output through 2028.

Hydroelectric Power Generation

Acciona’s fleet of hydroelectric plants functions as a classic cash cow: largely fully depreciated, they generate high EBITDA margins (around 45–55% in 2024) with low incremental CAPEX, producing roughly €350–400m annual free cash flow from hydro assets alone.

These plants provide flexible peak balancing—reducing system costs and earning ancillary revenues—while new large-scale hydro growth is limited by environmental permitting; Acciona’s existing footprint still supplies ~15–20% of its renewable generation.

Cash from hydro is critical for debt service (net debt €6.2bn as of 2024) and funds R&D in green hydrogen, where Acciona committed €120m+ to projects through 2025.

Regulated Toll Road Concessions

Long-term toll-road concessions in Spain and Latin America give Acciona steady, inflation-linked cashflows; as of FY 2024 these concessions contributed ~€420m in EBITDA, roughly 18% of group EBITDA.

Once built, competition is low so Acciona captures high regional traffic shares (some corridors >70%), requiring only maintenance and minor upgrades, converting a large share of revenue to profit (operating margins ~65% on concessions).

These mature assets require limited capex (2024 capex on concessions ~€60m), acting as a financial stabilizer that smooths group cashflow across construction cycles and reduces revenue volatility.

Integrated Water Cycle Management

Integrated Water Cycle Management in Acciona is a stable cash cow: operating and maintaining municipal water systems yields predictable revenue from long-term contracts (often 10–30 years), with high client exit costs and low cyclicality—2024 water services revenue for Acciona Agua was about EUR 1.1bn, supporting steady margins.

Growth in new municipal contracts is slow but steady; strong market share in Spain and Latin America delivers consistent free cash flow, helping Acciona pay dividends and keep investment-grade credit metrics (2024 net debt/EBITDA ~1.3x).

- Long contracts (10–30 yrs) = revenue visibility

- 2024 Acciona Agua revenue ~EUR 1.1bn

- High client exit barriers = low churn

- Net debt/EBITDA ~1.3x supports ratings

Legacy Wind O and M Services

Acciona’s Legacy Wind O and M Services runs high-margin, low-capex operations managing ~8.2 GW of turbines (2025), achieving gross margins ~28% via scale in spare parts and 1,200 field technicians; stable demand for older turbine servicing keeps utilization >90% and RoE above peers.

Reputation and long-term contracts give dominant share in Spain and growing share in LatAm; unit converts expertise into high returns on human capital with minimal incremental investment and predictable cash flow.

- Portfolio: ~8.2 GW under O&M (2025)

- Technicians: ~1,200 field staff

- Gross margin: ~28%

- Utilization: >90%

- Low capex, high ROE vs. group

Acciona’s cash cows: €770–820m FCF, high margins, low capex, solid balance sheet

Acciona’s cash cows—hydro, toll concessions, water services, and legacy wind O&M—produce steady free cash flow (~€770–820m combined in 2024–25), high margins (concessions ~65%, hydro 45–55%, O&M gross ~28%), low incremental capex (~€120m), and support net debt €6.2bn (net debt/EBITDA ~1.3x).

| Asset | 2024–25 |

|---|---|

| Hydro FCF | €350–400m |

| Concessions EBITDA | €420m |

| Water Rev | €1.1bn |

| O&M | 8.2GW, €~ |

What You’re Viewing Is Included

Acciona BCG Matrix

The file you're previewing on this page is the final Acciona BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report built for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Acciona’s BCG Matrix preview highlights how its core segments—renewable energy, infrastructure, and water—stack up on market growth and relative share, revealing early Stars in renewables and potential Cash Cows in long-term concessions. This snapshot hints at where capital should flow and which businesses may need divestment or reinvestment. Purchase the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and a ready-to-use strategic report in Word and Excel to accelerate confident decisions.

Stars

Utility Scale Solar PV Expansion

By end-2025 Acciona held ~6 GW of utility-scale PV capacity globally, leading large-scale projects in North America and Australia and capturing ~12% market share in those regions.

Strong corporate demand and decarbonization policies drove contracted PPA revenues, with average project IRRs of 7–9% and expected EBITDA margins >25% once operational.

High upfront capex—land, panels, grid works—raised initial leverage (net debt/EBITDA ~4x at peak build), but scale boosts procurement savings and grid access.

As installations stabilize and debt amortizes over 15–20 years, these assets are set to become cash cows, generating steady free cash flow and supporting reinvestment.

Desalination and Water Treatment

Acciona’s Desalination and Water Treatment is a Star — global desalination demand is rising 7% annually and Acciona holds roughly 18% share in MENA desalination projects as of 2025, driven by GCC and North Africa contracts totaling €1.2bn backlog. Heavy R&D spend (≈€75m in 2024) on membrane tech sustains a tech lead but burns cash, keeping capex intensity high. This unit underpins Acciona’s long-term sustainability credentials and draws ESG-focused institutional capital seeking water-security exposure.

Australian Transport Infrastructure

Australian Transport Infrastructure is a Star for Acciona, driven by A$110bn federal and state transport commitments to 2028 and 8–10% annual sector growth, making Australia a primary growth engine for Acciona’s infrastructure arm.

Acciona holds ~25–30% share in complex tunneling and bridge projects, securing high-value contracts worth ~A$2.1bn through 2025 and reinforcing its market leadership.

High regional growth forces ongoing reinvestment—CapEx of ~A$120–160m annually in heavy machinery and local crews—to sustain margins and capacity.

Sustained Australian success is vital to offset flat-to-negative revenue growth in mature European markets, where Acciona’s infrastructure revenue growth slowed to ~1% in 2024.

Offshore Wind Development

Offshore wind is a high-growth star for Acciona, using its maritime engineering to bid on Northern Hemisphere tenders where 2030 capacity additions are forecast at ~90 GW annually (IEA 2024); Acciona’s project pipeline reached ~3.2 GW by end-2025, showing scale potential despite heavy capex.

High barriers—specialized vessels, grid hooks, consenting—raise upfront costs (LCOE range €60–€120/MWh); success needs long-term grid contracts and regulatory navigation to secure market dominance.

- 2030 market growth ~90 GW/year (IEA 2024)

- Acciona pipeline ~3.2 GW (end-2025)

- LCOE €60–€120/MWh

- Key risks: capex intensity, permitting, grid contracts

Specialized Social Infrastructure

Acciona’s high-tech hospitals and research centers are a Star: global demand for advanced healthcare facilities is growing ~6.5% CAGR to 2028, and Acciona holds a leading PPP market share in Spain and LATAM with ~25–30% of large healthcare PPPs.

Combining construction plus 20–30 year management contracts yields recurring revenue; a €200–€400m typical project boosts backlog and EBITDA margin via services.

High sector growth as governments retrofit aging hospitals; EU recovery funds and Latin American health spending lift annual capex by billions.

- 6.5% global market CAGR to 2028

- 25–30% market share in regional PPPs

- €200–€400m typical project size

- Ongoing investment: digital twins, energy-efficiency

Acciona: 6GW PV, €1.2bn desal backlog, A$2.1bn transport, 3.2GW offshore, strong PPP hospitals

Acciona Stars: utility-scale PV (~6 GW end-2025, ~12% NA/AU share; IRR 7–9%, EBITDA >25%), desalination (18% MENA share, €1.2bn backlog, €75m R&D 2024), Australian transport (A$2.1bn contracts, 25–30% tunneling share, A$120–160m annual CapEx), offshore wind (3.2 GW pipeline end-2025, LCOE €60–120/MWh), hospitals (25–30% PPP share, €200–400m projects).

| Unit | Key metric |

|---|---|

| PV | 6 GW; 12% NA/AU; IRR 7–9% |

| Desal | 18% MENA; €1.2bn backlog |

| Aus Transport | A$2.1bn; 25–30% share |

| Offshore | 3.2 GW pipeline; €60–120/MWh |

| Hospitals | 25–30% PPP; €200–400m |

What is included in the product

BCG Matrix of Acciona: quadrant-by-quadrant strategic review with investment, hold/divest recommendations and trend-based risks/opportunities.

One-page Acciona BCG Matrix placing each business unit in a quadrant for swift strategic clarity.

Cash Cows

Spanish Onshore Wind Portfolios

Acciona’s Spanish onshore wind portfolios sit in a mature market with >40% domestic onshore share in regions like Castilla y León and Navarra, delivering stable EBITDA margins ~65% and predictable cash flows from long-term PPAs that cover ~70% of output through 2028.

Hydroelectric Power Generation

Acciona’s fleet of hydroelectric plants functions as a classic cash cow: largely fully depreciated, they generate high EBITDA margins (around 45–55% in 2024) with low incremental CAPEX, producing roughly €350–400m annual free cash flow from hydro assets alone.

These plants provide flexible peak balancing—reducing system costs and earning ancillary revenues—while new large-scale hydro growth is limited by environmental permitting; Acciona’s existing footprint still supplies ~15–20% of its renewable generation.

Cash from hydro is critical for debt service (net debt €6.2bn as of 2024) and funds R&D in green hydrogen, where Acciona committed €120m+ to projects through 2025.

Regulated Toll Road Concessions

Long-term toll-road concessions in Spain and Latin America give Acciona steady, inflation-linked cashflows; as of FY 2024 these concessions contributed ~€420m in EBITDA, roughly 18% of group EBITDA.

Once built, competition is low so Acciona captures high regional traffic shares (some corridors >70%), requiring only maintenance and minor upgrades, converting a large share of revenue to profit (operating margins ~65% on concessions).

These mature assets require limited capex (2024 capex on concessions ~€60m), acting as a financial stabilizer that smooths group cashflow across construction cycles and reduces revenue volatility.

Integrated Water Cycle Management

Integrated Water Cycle Management in Acciona is a stable cash cow: operating and maintaining municipal water systems yields predictable revenue from long-term contracts (often 10–30 years), with high client exit costs and low cyclicality—2024 water services revenue for Acciona Agua was about EUR 1.1bn, supporting steady margins.

Growth in new municipal contracts is slow but steady; strong market share in Spain and Latin America delivers consistent free cash flow, helping Acciona pay dividends and keep investment-grade credit metrics (2024 net debt/EBITDA ~1.3x).

- Long contracts (10–30 yrs) = revenue visibility

- 2024 Acciona Agua revenue ~EUR 1.1bn

- High client exit barriers = low churn

- Net debt/EBITDA ~1.3x supports ratings

Legacy Wind O and M Services

Acciona’s Legacy Wind O and M Services runs high-margin, low-capex operations managing ~8.2 GW of turbines (2025), achieving gross margins ~28% via scale in spare parts and 1,200 field technicians; stable demand for older turbine servicing keeps utilization >90% and RoE above peers.

Reputation and long-term contracts give dominant share in Spain and growing share in LatAm; unit converts expertise into high returns on human capital with minimal incremental investment and predictable cash flow.

- Portfolio: ~8.2 GW under O&M (2025)

- Technicians: ~1,200 field staff

- Gross margin: ~28%

- Utilization: >90%

- Low capex, high ROE vs. group

Acciona’s cash cows: €770–820m FCF, high margins, low capex, solid balance sheet

Acciona’s cash cows—hydro, toll concessions, water services, and legacy wind O&M—produce steady free cash flow (~€770–820m combined in 2024–25), high margins (concessions ~65%, hydro 45–55%, O&M gross ~28%), low incremental capex (~€120m), and support net debt €6.2bn (net debt/EBITDA ~1.3x).

| Asset | 2024–25 |

|---|---|

| Hydro FCF | €350–400m |

| Concessions EBITDA | €420m |

| Water Rev | €1.1bn |

| O&M | 8.2GW, €~ |

What You’re Viewing Is Included

Acciona BCG Matrix

The file you're previewing on this page is the final Acciona BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready report built for strategic clarity and professional use.