Acciona Porter's Five Forces Analysis

Don't Miss the Bigger Picture

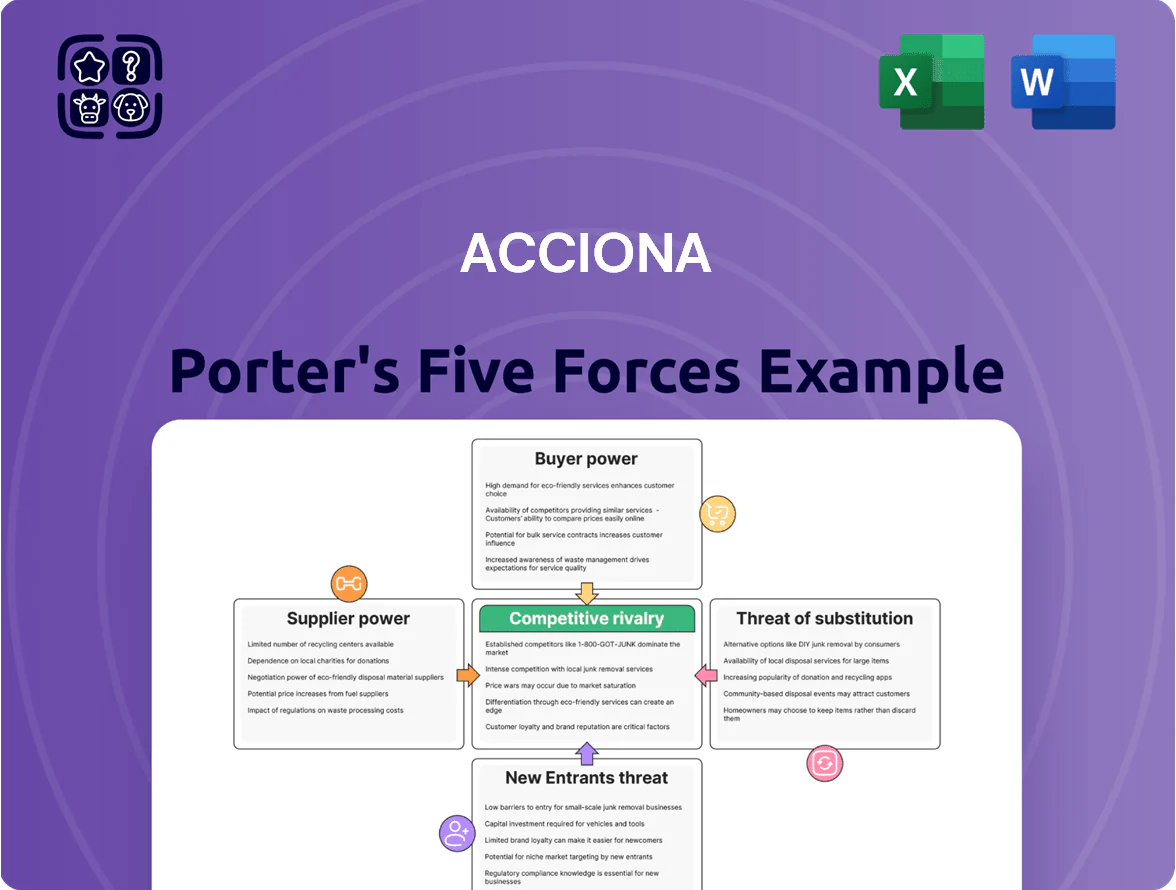

Acciona faces moderate competitive rivalry driven by large infrastructure peers and growing renewable entrants, while supplier and buyer power vary across its construction and energy segments, shaping margins and strategic choices.

Regulatory shifts and technology adoption heighten threats from substitutes and new entrants, but Acciona’s scale and integrated project capabilities provide defensive advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acciona’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Renewable Technology OEMs

The market for high-capacity wind turbines and solar modules is concentrated among a few OEMs—Vestas, Siemens Gamesa, Goldwind and leading Chinese PV makers—giving suppliers strong leverage during demand spikes; global turbine shipments fell 12% in 2023 while order backlogs rose 18% through Q3 2024. Acciona relies on these suppliers for critical CAPEX items, so suppliers can pressure prices and lead times. Acciona counters with large-scale procurement: in 2024 it signed multi-year framework agreements covering ~2.5 GW/year of wind and 3 GW/year of PV, smoothing prices and reducing spot exposure. This scale buys negotiating power but not full insulation from global supply shocks.

Volatility in Raw Material Costs

Suppliers of steel, copper and battery minerals exert strong bargaining power for Acciona because few substitutes exist for large-scale turbines and infrastructure; global steel prices rose ~18% in 2024 and copper averaged $9,100/ton in 2024, tightening margins. Acciona shields itself via diversified sourcing across 12+ suppliers and regions and uses price-adjustment clauses in long-term contracts to pass roughly 60–80% of input inflation to clients.

Scarcity of Specialized Technical Labor

As demand for green-hydrogen and offshore-wind engineers outstrips supply—IEA estimated 1.2 million clean-energy jobs gap by 2030 in 2025 scenarios—specialist consultants can charge 20–50% premiums; Acciona reduces supplier power by spending ~€120m on training and hiring 3,500 technical staff globally in 2024, cutting external contractor spend and securing project delivery.

Geopolitical Influence on Solar Supply Chains

Acciona faces supplier power risks as over 80% of solar PV module manufacturing and 70% of polysilicon capacity were China-based in 2024, raising exposure to export controls and tariff shifts.

Chinese suppliers can alter prices or quotas amid tensions; Acciona should diversify into regional manufacturing in EU and Latin America and lock multi-year contracts to hedge cost swings.

Supply-chain transparency and ESG reporting to meet Acciona’s end-2025 targets require traceability systems and supplier audits, reducing disruption risk and meeting investor standards.

- 2024: >80% modules, 70% polysilicon China

- Mitigation: regional plants, multi-year contracts

- ESG: traceability + audits by end-2025

Logistics and Specialized Transport Providers

Specialized heavy‑lift logistics firms wield notable supplier power when moving wind blades or desalination membranes because global heavy‑lift capacity is limited and delivery windows are tight; in 2024, global project delays from transport bottlenecks rose 18% year‑on‑year.

Acciona reduces this risk by folding logistics planning into early design stages, contracting capacity ahead—cutting schedule overrun risk by an estimated 12–20% on large renewable and water projects.

- Limited heavy‑lift fleet: high bargaining power

- Tight delivery windows: increased delay risk (2024 +18%)

- Early logistics integration: reduces overruns ~12–20%

Acciona tames supplier power with multi‑year frameworks, diversification & €120m upskilling

Suppliers hold moderate-to-high power over Acciona due to concentrated OEMs for turbines/PV, commodity price swings (steel +18% in 2024, copper $9,100/ton in 2024) and China-centric PV supply (>80% modules, 70% polysilicon in 2024); Acciona offsets this with multi-year frameworks (~2.5 GW/yr wind, 3 GW/yr PV), 12+ diversified suppliers, €120m 2024 hiring/training and early logistics integration that trims overruns ~12–20%.

| Metric | 2024 |

|---|---|

| Modules China share | >80% |

| Polysilicon China share | 70% |

| Steel price change | +18% |

| Copper avg | $9,100/ton |

| Framework capacity | 2.5GW wind / 3GW PV per year |

| Training/hiring spend | €120m (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Acciona, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its sector positioning and profitability.

A concise Porter's Five Forces snapshot for Acciona—clearly showing competitive pressures and regulatory risks to speed strategic decisions and investor assessments.

Customers Bargaining Power

Government Influence through Public Tenders

Corporate Power Purchase Agreements PPA

Large multinationals aiming for net-zero by 2025 increasingly buy renewables directly, giving them strong bargaining power as they can pick from a global developer pool; corporate PPA volume hit a record 32 GW in 2024, up 18% YoY. These sophisticated buyers demand custom pricing and risk terms, pressuring margins, so Acciona defends market share with 24/7 green energy offers and digital tracking that meet transparency needs.

Wholesale Electricity Market Dynamics

In wholesale markets, prices set by supply-demand dynamics, not negotiations, give market participants collective bargaining power that caps merchant plant revenues; in 2024 European power day-ahead prices averaged €120/MWh vs Acciona's long-term contract reference ~€55–€65/MWh, showing spot-driven volatility.

Acciona shifts sales toward long-term fixed-price PPAs—about 45% of its 2024 production contracted—reducing spot exposure and stabilizing cash flow; higher hedging cut merchant revenue volatility by an estimated 30% in 2024.

Municipal Water Authority Demands

Municipal buyers demand low tariffs and 99.99% uptime; long-term contracts (10–30 years) give them strong leverage and include KPIs and penalties—e.g., EU municipal contracts average 15‑year terms with 5–10% performance holdbacks in 2024.

Acciona counters with reverse osmosis and recycling tech that cuts energy use ~20% and OPEX ~12%, making it preferred despite buyer power; its desalination backlog was €1.1bn in 2025.

- Municipal contracts: 10–30 yrs, 5–10% penalties

- Uptime required: 99.99%

- Acciona tech: −20% energy, −12% OPEX

- Backlog: €1.1bn (2025)

Low Switching Costs in Liberalized Markets

In deregulated markets where switching costs are low, commercial and industrial buyers can move providers quickly, pressuring Acciona to prove value via uptime and energy-management services; in 2024 renewables PPAs accounted for ~28% of corporate deals in Europe, raising churn risk.

Acciona counters with strategic partnerships and integrated infra—solar, storage, O&M—to boost stickiness; long-term service contracts and 10–15% higher-margin integrated projects reduce customer turnover.

- Low switching in deregulated markets increases price sensitivity

- 2024: ~28% of EU corporate PPAs were renewables

- Acciona uses integrated infra and long-term contracts

- Integrated projects show ~10–15% margin premium

Acciona squeezed by buyer power but shields margins with PPAs, tech cuts and €1.1bn desal

Buyers wield strong power: 55% of Acciona’s 2024 revenue from public tenders with fixed specs and price caps; corporate PPAs hit 32 GW in 2024, boosting buyer leverage. Acciona counters with 45% of 2024 production under long-term PPAs, lifecycle contracting, tech that cuts energy ~20% and OPEX ~12%, and a €1.1bn desal backlog (2025), which stabilizes margins and reduces churn.

| Metric | Value |

|---|---|

| Public-tender revenue | 55% (2024) |

| Corporate PPA market | 32 GW (2024) |

| Production contracted | 45% (2024) |

| Energy/OPEX savings | −20% / −12% |

| Desalination backlog | €1.1bn (2025) |

What You See Is What You Get

Acciona Porter's Five Forces Analysis

This preview shows the exact Acciona Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no samples.

The file displayed is the final, professionally formatted document ready for immediate download and use once you complete your purchase.

No mockups or excerpts: what you see here is the full deliverable you’ll get instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Acciona faces moderate competitive rivalry driven by large infrastructure peers and growing renewable entrants, while supplier and buyer power vary across its construction and energy segments, shaping margins and strategic choices.

Regulatory shifts and technology adoption heighten threats from substitutes and new entrants, but Acciona’s scale and integrated project capabilities provide defensive advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acciona’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Renewable Technology OEMs

The market for high-capacity wind turbines and solar modules is concentrated among a few OEMs—Vestas, Siemens Gamesa, Goldwind and leading Chinese PV makers—giving suppliers strong leverage during demand spikes; global turbine shipments fell 12% in 2023 while order backlogs rose 18% through Q3 2024. Acciona relies on these suppliers for critical CAPEX items, so suppliers can pressure prices and lead times. Acciona counters with large-scale procurement: in 2024 it signed multi-year framework agreements covering ~2.5 GW/year of wind and 3 GW/year of PV, smoothing prices and reducing spot exposure. This scale buys negotiating power but not full insulation from global supply shocks.

Volatility in Raw Material Costs

Suppliers of steel, copper and battery minerals exert strong bargaining power for Acciona because few substitutes exist for large-scale turbines and infrastructure; global steel prices rose ~18% in 2024 and copper averaged $9,100/ton in 2024, tightening margins. Acciona shields itself via diversified sourcing across 12+ suppliers and regions and uses price-adjustment clauses in long-term contracts to pass roughly 60–80% of input inflation to clients.

Scarcity of Specialized Technical Labor

As demand for green-hydrogen and offshore-wind engineers outstrips supply—IEA estimated 1.2 million clean-energy jobs gap by 2030 in 2025 scenarios—specialist consultants can charge 20–50% premiums; Acciona reduces supplier power by spending ~€120m on training and hiring 3,500 technical staff globally in 2024, cutting external contractor spend and securing project delivery.

Geopolitical Influence on Solar Supply Chains

Acciona faces supplier power risks as over 80% of solar PV module manufacturing and 70% of polysilicon capacity were China-based in 2024, raising exposure to export controls and tariff shifts.

Chinese suppliers can alter prices or quotas amid tensions; Acciona should diversify into regional manufacturing in EU and Latin America and lock multi-year contracts to hedge cost swings.

Supply-chain transparency and ESG reporting to meet Acciona’s end-2025 targets require traceability systems and supplier audits, reducing disruption risk and meeting investor standards.

- 2024: >80% modules, 70% polysilicon China

- Mitigation: regional plants, multi-year contracts

- ESG: traceability + audits by end-2025

Logistics and Specialized Transport Providers

Specialized heavy‑lift logistics firms wield notable supplier power when moving wind blades or desalination membranes because global heavy‑lift capacity is limited and delivery windows are tight; in 2024, global project delays from transport bottlenecks rose 18% year‑on‑year.

Acciona reduces this risk by folding logistics planning into early design stages, contracting capacity ahead—cutting schedule overrun risk by an estimated 12–20% on large renewable and water projects.

- Limited heavy‑lift fleet: high bargaining power

- Tight delivery windows: increased delay risk (2024 +18%)

- Early logistics integration: reduces overruns ~12–20%

Acciona tames supplier power with multi‑year frameworks, diversification & €120m upskilling

Suppliers hold moderate-to-high power over Acciona due to concentrated OEMs for turbines/PV, commodity price swings (steel +18% in 2024, copper $9,100/ton in 2024) and China-centric PV supply (>80% modules, 70% polysilicon in 2024); Acciona offsets this with multi-year frameworks (~2.5 GW/yr wind, 3 GW/yr PV), 12+ diversified suppliers, €120m 2024 hiring/training and early logistics integration that trims overruns ~12–20%.

| Metric | 2024 |

|---|---|

| Modules China share | >80% |

| Polysilicon China share | 70% |

| Steel price change | +18% |

| Copper avg | $9,100/ton |

| Framework capacity | 2.5GW wind / 3GW PV per year |

| Training/hiring spend | €120m (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Acciona, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its sector positioning and profitability.

A concise Porter's Five Forces snapshot for Acciona—clearly showing competitive pressures and regulatory risks to speed strategic decisions and investor assessments.

Customers Bargaining Power

Government Influence through Public Tenders

Corporate Power Purchase Agreements PPA

Large multinationals aiming for net-zero by 2025 increasingly buy renewables directly, giving them strong bargaining power as they can pick from a global developer pool; corporate PPA volume hit a record 32 GW in 2024, up 18% YoY. These sophisticated buyers demand custom pricing and risk terms, pressuring margins, so Acciona defends market share with 24/7 green energy offers and digital tracking that meet transparency needs.

Wholesale Electricity Market Dynamics

In wholesale markets, prices set by supply-demand dynamics, not negotiations, give market participants collective bargaining power that caps merchant plant revenues; in 2024 European power day-ahead prices averaged €120/MWh vs Acciona's long-term contract reference ~€55–€65/MWh, showing spot-driven volatility.

Acciona shifts sales toward long-term fixed-price PPAs—about 45% of its 2024 production contracted—reducing spot exposure and stabilizing cash flow; higher hedging cut merchant revenue volatility by an estimated 30% in 2024.

Municipal Water Authority Demands

Municipal buyers demand low tariffs and 99.99% uptime; long-term contracts (10–30 years) give them strong leverage and include KPIs and penalties—e.g., EU municipal contracts average 15‑year terms with 5–10% performance holdbacks in 2024.

Acciona counters with reverse osmosis and recycling tech that cuts energy use ~20% and OPEX ~12%, making it preferred despite buyer power; its desalination backlog was €1.1bn in 2025.

- Municipal contracts: 10–30 yrs, 5–10% penalties

- Uptime required: 99.99%

- Acciona tech: −20% energy, −12% OPEX

- Backlog: €1.1bn (2025)

Low Switching Costs in Liberalized Markets

In deregulated markets where switching costs are low, commercial and industrial buyers can move providers quickly, pressuring Acciona to prove value via uptime and energy-management services; in 2024 renewables PPAs accounted for ~28% of corporate deals in Europe, raising churn risk.

Acciona counters with strategic partnerships and integrated infra—solar, storage, O&M—to boost stickiness; long-term service contracts and 10–15% higher-margin integrated projects reduce customer turnover.

- Low switching in deregulated markets increases price sensitivity

- 2024: ~28% of EU corporate PPAs were renewables

- Acciona uses integrated infra and long-term contracts

- Integrated projects show ~10–15% margin premium

Acciona squeezed by buyer power but shields margins with PPAs, tech cuts and €1.1bn desal

Buyers wield strong power: 55% of Acciona’s 2024 revenue from public tenders with fixed specs and price caps; corporate PPAs hit 32 GW in 2024, boosting buyer leverage. Acciona counters with 45% of 2024 production under long-term PPAs, lifecycle contracting, tech that cuts energy ~20% and OPEX ~12%, and a €1.1bn desal backlog (2025), which stabilizes margins and reduces churn.

| Metric | Value |

|---|---|

| Public-tender revenue | 55% (2024) |

| Corporate PPA market | 32 GW (2024) |

| Production contracted | 45% (2024) |

| Energy/OPEX savings | −20% / −12% |

| Desalination backlog | €1.1bn (2025) |

What You See Is What You Get

Acciona Porter's Five Forces Analysis

This preview shows the exact Acciona Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no samples.

The file displayed is the final, professionally formatted document ready for immediate download and use once you complete your purchase.

No mockups or excerpts: what you see here is the full deliverable you’ll get instantly after payment.