Acciona PESTLE Analysis

Your Competitive Advantage Starts with This Report

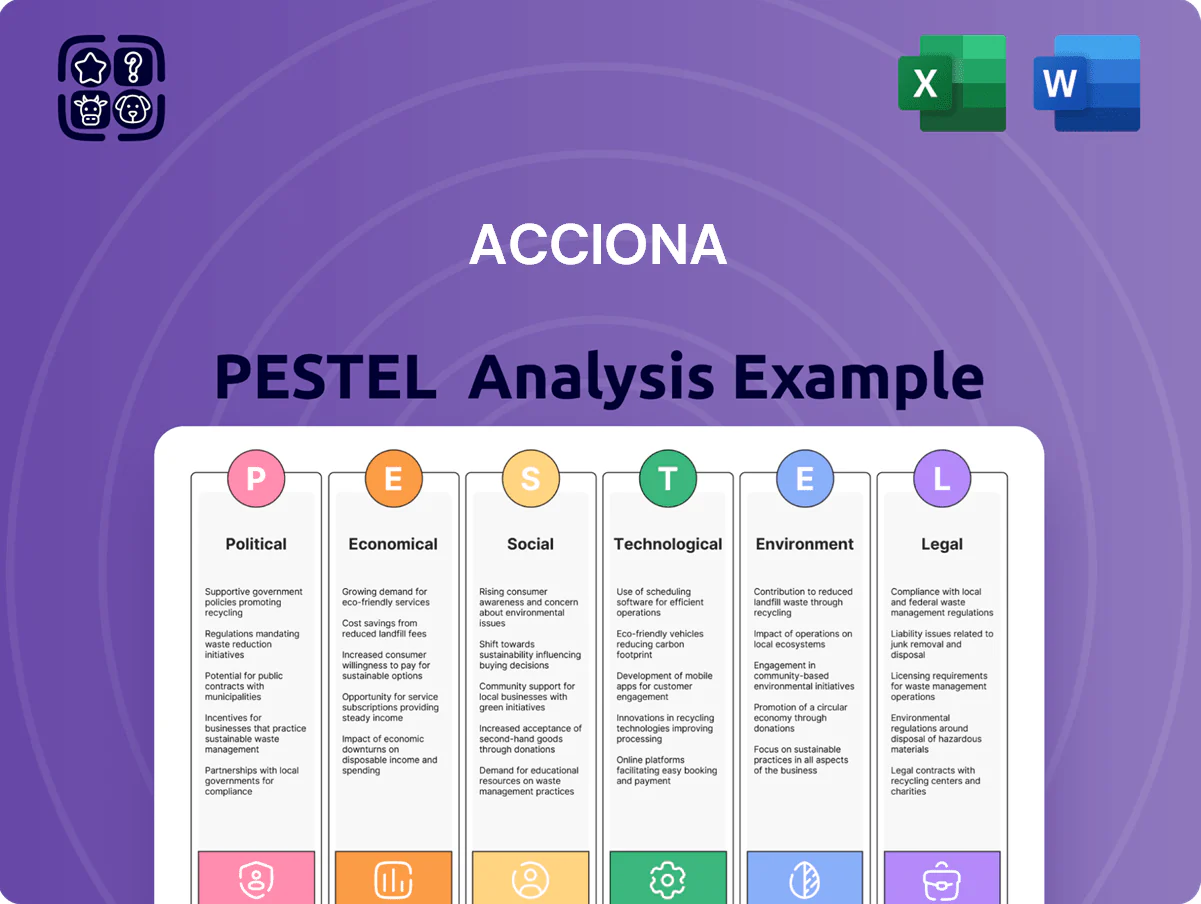

Gain strategic clarity with our Acciona PESTLE Analysis—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping the firm's future; buy the full report to access actionable insights, forecasts, and ready-to-use slides for investment or strategic planning.

Political factors

European Green Deal and Policy Alignment

Acciona benefits from the EU Green Deal and Fit for 55, which target a 55% GHG reduction by 2030 and mobilized over €300bn annually in green investment by 2025, creating stable demand for renewables and grids.

The company’s €10.5bn order backlog (2025) and €4.2bn renewables pipeline position it to win high-value contracts as member states enforce mandatory carbon reduction targets.

Geopolitical Stability and Energy Sovereignty

The post-2022 push for energy security has accelerated government commitments to domestic renewables, increasing public tender volumes—EU green auctions grew 28% in 2023—and positioning Acciona as a strategic partner for scaling local wind and solar capacity, contributing to its 2024 renewables backlog of ~€9.8bn. Political instability in parts of Latin America and Africa, where Acciona has ~15% of projects, necessitates enhanced risk management, insurance and diplomatic engagement to protect operations and cash flows.

US Inflation Reduction Act Influence

The US Inflation Reduction Act reshaped renewable energy economics through 2023–25 by expanding tax credits—Investment Tax Credit and Production Tax Credit—supporting ~$370bn clean energy investment estimates to 2030; Acciona must leverage these incentives to compete with US incumbents capturing rapidly growing utility-scale solar and wind markets. Political shifts in Washington over credit sunset provisions (e.g., 10–15 year phase-ins) are key risks for Acciona’s North American capex and M&A planning.

Public-Private Partnership Frameworks

Governments increasingly use PPPs to close a $15+ trillion global infrastructure gap to 2040, making Acciona's bid pipeline sensitive to sovereign appetite for private capital and off-balance financing.

Acciona's access to large projects hinges on transparent procurement—World Bank 2024 data shows PPP-backed transport projects’ success rates drop 30% where procurement lapses occur.

Electoral turnover can reprioritize spending; managing political relationships is essential as 40% of announced PPPs in 2023 faced renegotiation after administration changes.

- Global infrastructure gap ~$15 trillion to 2040

- 30% lower PPP success where procurement is opaque (World Bank 2024)

- 40% of 2023 PPPs renegotiated post-election

Global Trade Policy and Protectionism

Rising protectionism raised tariffs on solar panels to 15-25% in key markets in 2024, and EU provisional duties on Chinese solar cells reached 18% in 2025, increasing Acciona’s component costs and straining its global supply chain.

Tariff volatility—shocks in 2024 that delayed turbine part shipments by 8-12 weeks for some projects—can inflate project CAPEX and push back EBITDA recognition for construction and energy divisions.

Acciona must track WTO disputes, US-China trade talks and EU trade remedies to hedge exposure and renegotiate supplier contracts to preserve margins.

- 2024–25 tariff hikes: 15–25% on solar; 18% EU duties on Chinese cells

- Shipment delays observed: 8–12 weeks in 2024

- Actions: monitor negotiations, hedge import risk, renegotiate supplier terms

Acciona poised as EU Green Deal and US IRA fuel €14.7bn renewables pipeline amid policy risks

EU Green Deal/ Fit for 55 spurs stable renewables demand; Acciona benefits from €10.5bn order backlog (2025) and €4.2bn renewables pipeline. US IRA tax credits support ~$370bn clean investment to 2030 but political risks in Washington affect North America plans. PPPs matter amid a ~$15tn infrastructure gap to 2040; 40% of 2023 PPPs saw renegotiation. Tariff hikes (15–25% solar; 18% EU duty 2025) caused 8–12 week delays in 2024.

| Metric | Value |

|---|---|

| Order backlog (2025) | €10.5bn |

| Renewables pipeline | €4.2bn |

| Renewables backlog (2024) | ~€9.8bn |

| Global infra gap to 2040 | ~$15tn |

| IRA-driven investment to 2030 | ~$370bn |

What is included in the product

Explores how macro-environmental forces uniquely affect Acciona across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and region-specific trends to identify risks and opportunities for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Acciona that streamlines external risk review and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Interest Rate Environment and Capital Cost

As a capital-intensive group, Acciona remains sensitive to global rates which stabilized around 3.5–4.0% by end-2025, easing financing stress for new projects.

Higher borrowing costs directly compress IRRs on renewables and infrastructure; a 100 bp change can swing project IRRs by several hundred basis points on long tenors.

Acciona reported net debt of €5.6bn (FY2024) and is optimizing tenor and fixed-rate share to hedge residual cost-of-capital volatility and protect margins.

Inflationary Pressures on Raw Materials

Persistent inflation in steel, cement and specialized renewable components—steel up ~15% YoY and cement input costs up ~8% in 2024—squeezes Acciona construction margins on long-cycle projects.

Acciona employs hedging and indexed contracts; as of FY2024 ~40% of project volume had price escalation clauses, reducing exposure to short-term spikes.

Active cost management is crucial to protect profitability of fixed-price tenders where materials represent ~30–35% of project costs.

Expansion of the Green Finance Market

The maturing green bond market gives Acciona cheaper access to dedicated sustainable capital, with global green bond issuance reaching about USD 560 billion in 2024 and expected steady flows into 2025, improving refinancing terms for large projects.

Investor demand for high-quality ESG assets rose in 2025, with sustainable fund flows up ~12% YoY, positioning Acciona favorably for new capital raises targeted at grade-A ESG credentials.

This economic tailwind supports Acciona’s aggressive growth in water treatment and renewables as it taps lower-cost green debt to fund capacity expansions and project pipelines.

Currency Exchange Rate Volatility

Operating in over 40 countries exposes Acciona to material FX risk: in 2024 roughly 18% of revenue originated outside the eurozone, amplifying translation exposure when converting earnings from emerging markets back to EUR.

Economic swings in Australia, Chile and Mexico—where 2023-24 local GDP growth ranged 1.5–3.5%—can materially affect consolidated results if not effectively hedged; Acciona reported FX losses of €45m in 2023.

The firm’s geographic diversity provides a partial natural hedge, yet sharp currency devaluations (eg. MXN or CLP moves >10%) remain a key economic risk requiring active risk management.

- ~40 countries footprint; 18% revenue outside eurozone (2024)

- FX losses €45m in 2023

- Local GDP variability (Australia/Chile/Mexico ~1.5–3.5% 2023-24)

- Devaluations >10% (MXN/CLP) pose significant translation risk

Global Infrastructure Spending Trends

Global stimulus through 2025 channels over USD 2.5 trillion toward green infrastructure, supporting demand for Acciona in high-speed rail, desalination and renewables—company backlog grew 8% to EUR 10.4bn in 2024, reflecting this trend.

However, IMF 2025 forecasts cut global GDP growth to 2.8%, raising risk of fiscal tightening that could delay non-essential projects and compress public capex.

- Green stimulus >USD 2.5tn (through 2025)

- Acciona backlog EUR 10.4bn (+8% in 2024)

- IMF 2025 global GDP forecast 2.8%—risk of budget cuts

Stabilizing costs, €5.6bn debt, €10.4bn backlog boosted by green stimulus

Capital costs stabilized (~3.5–4.0% end-2025) easing financing; net debt €5.6bn (FY2024) with ~40% price-escalation clauses; materials inflation (steel +15%, cement +8% in 2024) pressures margins; green bond market (~USD560bn issuance 2024) and >USD2.5tn green stimulus through 2025 support backlog (€10.4bn, +8% 2024); 18% revenue outside eurozone, FX losses €45m (2023).

| Metric | Value |

|---|---|

| Net debt | €5.6bn (FY2024) |

| Backlog | €10.4bn (+8% 2024) |

| Green bond issuance | USD560bn (2024) |

| Revenue outside EUR | 18% (2024) |

Full Version Awaits

Acciona PESTLE Analysis

The preview shown here is the exact Acciona PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use, with comprehensive political, economic, social, technological, legal, and environmental insights.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain strategic clarity with our Acciona PESTLE Analysis—concise, current, and focused on the political, economic, social, technological, legal, and environmental forces shaping the firm's future; buy the full report to access actionable insights, forecasts, and ready-to-use slides for investment or strategic planning.

Political factors

European Green Deal and Policy Alignment

Acciona benefits from the EU Green Deal and Fit for 55, which target a 55% GHG reduction by 2030 and mobilized over €300bn annually in green investment by 2025, creating stable demand for renewables and grids.

The company’s €10.5bn order backlog (2025) and €4.2bn renewables pipeline position it to win high-value contracts as member states enforce mandatory carbon reduction targets.

Geopolitical Stability and Energy Sovereignty

The post-2022 push for energy security has accelerated government commitments to domestic renewables, increasing public tender volumes—EU green auctions grew 28% in 2023—and positioning Acciona as a strategic partner for scaling local wind and solar capacity, contributing to its 2024 renewables backlog of ~€9.8bn. Political instability in parts of Latin America and Africa, where Acciona has ~15% of projects, necessitates enhanced risk management, insurance and diplomatic engagement to protect operations and cash flows.

US Inflation Reduction Act Influence

The US Inflation Reduction Act reshaped renewable energy economics through 2023–25 by expanding tax credits—Investment Tax Credit and Production Tax Credit—supporting ~$370bn clean energy investment estimates to 2030; Acciona must leverage these incentives to compete with US incumbents capturing rapidly growing utility-scale solar and wind markets. Political shifts in Washington over credit sunset provisions (e.g., 10–15 year phase-ins) are key risks for Acciona’s North American capex and M&A planning.

Public-Private Partnership Frameworks

Governments increasingly use PPPs to close a $15+ trillion global infrastructure gap to 2040, making Acciona's bid pipeline sensitive to sovereign appetite for private capital and off-balance financing.

Acciona's access to large projects hinges on transparent procurement—World Bank 2024 data shows PPP-backed transport projects’ success rates drop 30% where procurement lapses occur.

Electoral turnover can reprioritize spending; managing political relationships is essential as 40% of announced PPPs in 2023 faced renegotiation after administration changes.

- Global infrastructure gap ~$15 trillion to 2040

- 30% lower PPP success where procurement is opaque (World Bank 2024)

- 40% of 2023 PPPs renegotiated post-election

Global Trade Policy and Protectionism

Rising protectionism raised tariffs on solar panels to 15-25% in key markets in 2024, and EU provisional duties on Chinese solar cells reached 18% in 2025, increasing Acciona’s component costs and straining its global supply chain.

Tariff volatility—shocks in 2024 that delayed turbine part shipments by 8-12 weeks for some projects—can inflate project CAPEX and push back EBITDA recognition for construction and energy divisions.

Acciona must track WTO disputes, US-China trade talks and EU trade remedies to hedge exposure and renegotiate supplier contracts to preserve margins.

- 2024–25 tariff hikes: 15–25% on solar; 18% EU duties on Chinese cells

- Shipment delays observed: 8–12 weeks in 2024

- Actions: monitor negotiations, hedge import risk, renegotiate supplier terms

Acciona poised as EU Green Deal and US IRA fuel €14.7bn renewables pipeline amid policy risks

EU Green Deal/ Fit for 55 spurs stable renewables demand; Acciona benefits from €10.5bn order backlog (2025) and €4.2bn renewables pipeline. US IRA tax credits support ~$370bn clean investment to 2030 but political risks in Washington affect North America plans. PPPs matter amid a ~$15tn infrastructure gap to 2040; 40% of 2023 PPPs saw renegotiation. Tariff hikes (15–25% solar; 18% EU duty 2025) caused 8–12 week delays in 2024.

| Metric | Value |

|---|---|

| Order backlog (2025) | €10.5bn |

| Renewables pipeline | €4.2bn |

| Renewables backlog (2024) | ~€9.8bn |

| Global infra gap to 2040 | ~$15tn |

| IRA-driven investment to 2030 | ~$370bn |

What is included in the product

Explores how macro-environmental forces uniquely affect Acciona across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and region-specific trends to identify risks and opportunities for executives, investors and strategists.

A concise, visually segmented PESTLE summary for Acciona that streamlines external risk review and can be dropped into presentations or shared across teams for quick alignment.

Economic factors

Interest Rate Environment and Capital Cost

As a capital-intensive group, Acciona remains sensitive to global rates which stabilized around 3.5–4.0% by end-2025, easing financing stress for new projects.

Higher borrowing costs directly compress IRRs on renewables and infrastructure; a 100 bp change can swing project IRRs by several hundred basis points on long tenors.

Acciona reported net debt of €5.6bn (FY2024) and is optimizing tenor and fixed-rate share to hedge residual cost-of-capital volatility and protect margins.

Inflationary Pressures on Raw Materials

Persistent inflation in steel, cement and specialized renewable components—steel up ~15% YoY and cement input costs up ~8% in 2024—squeezes Acciona construction margins on long-cycle projects.

Acciona employs hedging and indexed contracts; as of FY2024 ~40% of project volume had price escalation clauses, reducing exposure to short-term spikes.

Active cost management is crucial to protect profitability of fixed-price tenders where materials represent ~30–35% of project costs.

Expansion of the Green Finance Market

The maturing green bond market gives Acciona cheaper access to dedicated sustainable capital, with global green bond issuance reaching about USD 560 billion in 2024 and expected steady flows into 2025, improving refinancing terms for large projects.

Investor demand for high-quality ESG assets rose in 2025, with sustainable fund flows up ~12% YoY, positioning Acciona favorably for new capital raises targeted at grade-A ESG credentials.

This economic tailwind supports Acciona’s aggressive growth in water treatment and renewables as it taps lower-cost green debt to fund capacity expansions and project pipelines.

Currency Exchange Rate Volatility

Operating in over 40 countries exposes Acciona to material FX risk: in 2024 roughly 18% of revenue originated outside the eurozone, amplifying translation exposure when converting earnings from emerging markets back to EUR.

Economic swings in Australia, Chile and Mexico—where 2023-24 local GDP growth ranged 1.5–3.5%—can materially affect consolidated results if not effectively hedged; Acciona reported FX losses of €45m in 2023.

The firm’s geographic diversity provides a partial natural hedge, yet sharp currency devaluations (eg. MXN or CLP moves >10%) remain a key economic risk requiring active risk management.

- ~40 countries footprint; 18% revenue outside eurozone (2024)

- FX losses €45m in 2023

- Local GDP variability (Australia/Chile/Mexico ~1.5–3.5% 2023-24)

- Devaluations >10% (MXN/CLP) pose significant translation risk

Global Infrastructure Spending Trends

Global stimulus through 2025 channels over USD 2.5 trillion toward green infrastructure, supporting demand for Acciona in high-speed rail, desalination and renewables—company backlog grew 8% to EUR 10.4bn in 2024, reflecting this trend.

However, IMF 2025 forecasts cut global GDP growth to 2.8%, raising risk of fiscal tightening that could delay non-essential projects and compress public capex.

- Green stimulus >USD 2.5tn (through 2025)

- Acciona backlog EUR 10.4bn (+8% in 2024)

- IMF 2025 global GDP forecast 2.8%—risk of budget cuts

Stabilizing costs, €5.6bn debt, €10.4bn backlog boosted by green stimulus

Capital costs stabilized (~3.5–4.0% end-2025) easing financing; net debt €5.6bn (FY2024) with ~40% price-escalation clauses; materials inflation (steel +15%, cement +8% in 2024) pressures margins; green bond market (~USD560bn issuance 2024) and >USD2.5tn green stimulus through 2025 support backlog (€10.4bn, +8% 2024); 18% revenue outside eurozone, FX losses €45m (2023).

| Metric | Value |

|---|---|

| Net debt | €5.6bn (FY2024) |

| Backlog | €10.4bn (+8% 2024) |

| Green bond issuance | USD560bn (2024) |

| Revenue outside EUR | 18% (2024) |

Full Version Awaits

Acciona PESTLE Analysis

The preview shown here is the exact Acciona PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use, with comprehensive political, economic, social, technological, legal, and environmental insights.