AccorHotels PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and rising sustainability expectations are reshaping AccorHotels’ strategy and growth outlook—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions. Purchase the full PESTLE analysis for a complete, editable report with deep-dive insights, data-backed forecasts, and practical recommendations you can use right away.

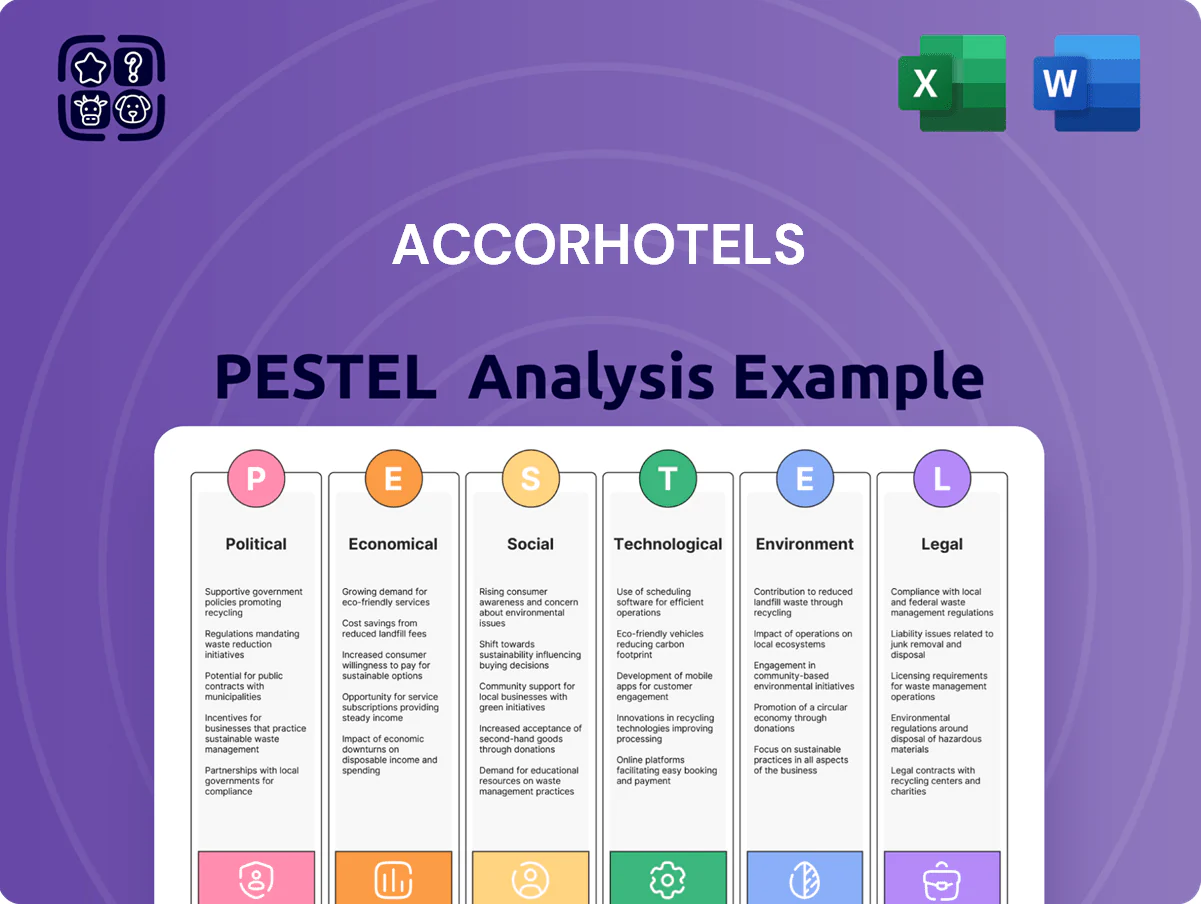

Political factors

Geopolitical instability in key regions

Geopolitical tensions in Eastern Europe and the Middle East in 2025 continue to reshape travel: UNWTO reported 2024 arrivals down 3% in affected corridors, and volatile Brent oil prices (range USD 70–95/bbl in 2024–25) drove regional transport costs higher, squeezing margins for Accor’s 5,500+ properties; sudden travel bans and advisories caused localized occupancy drops of 8–12%, forcing Accor to intensify contingency planning and diplomatic engagement to protect assets.

Government tourism incentives and support

Many governments in 2025 rolled out post-recovery tourism strategies providing tax breaks and infrastructure funds; OECD reports travel subsidies rose by 18% YoY, aiding hotel chains. Accor benefits notably in Southeast Asia and the Middle East, where governments subsidized luxury tourism—GCC tourism investment reached $45bn in 2024–25—boosting demand for upscale properties. Aligning with national agendas enabled Accor to secure favorable land leases and reduced-tax development terms for new builds and renovations, supporting its 2025 pipeline expansion of ~200 projects.

Visa and border policy changes

Streamlined visa processes in the Schengen Area and parts of Asia by late 2025 raised cross-border arrivals, with EU tourism receipts up 8.2% YoY in 2024 and intra-Asia travel growing 12% in H1 2025, benefiting Accor’s international occupancy. Conversely, tighter migration rules in some Western countries contributed to hospitality labor shortages, with EU hospitality vacancy rates reaching 7.1% in 2024. Accor closely monitors these shifts, adjusting recruitment—including a 15% rise in local hiring initiatives in 2024—and tailoring guest services to changing entry requirements.

International trade relations and sanctions

Trade disputes between major economies can trigger tariffs and export controls that raise costs for luxury goods and construction materials; e.g., 2023 steel and aluminum tariffs raised import costs by up to 15% for EU hotels, squeezing margins on Accor’s €1.8bn 2023 renovation capex pipeline.

Sanctions have forced hotel groups to exit markets; Accor suspended Russian operations in 2022 and recognized related impairment charges, illustrating risk of divestment and revenue loss in sanctioned jurisdictions.

Managing these pressures requires a strong legal and governmental affairs team; in 2024 Accor expanded compliance staffing after regulatory fines across the sector totaled over €200m globally in 2022–23.

- Tariff-driven cost increases up to 15% on materials

- 2022 Russia exit caused impairments for hotel groups

- Sector regulatory fines >€200m (2022–23)

- €1.8bn 2023 renovation capex exposed to trade risk

Political stability in emerging markets

Accor’s expansion into Africa and South America depends on political stability and rule of law; 2024 UNCTAD shows FDI flows to Africa rose 12% to about $60 billion while several countries still face governance risks that threaten hotel investments.

Political upheavals or ideological shifts can alter property rights or force profit repatriation, affecting returns on Accor’s long-term assets and concessions.

The group prioritizes markets with stable governance to protect franchise and management agreements; as of 2025 Accor reports over 5,300 hotels under management in high-governance markets.

- FDI to Africa +12% in 2024 (~$60bn)

- Political risk can reverse property rights or repatriation rules

- Accor favors stable-governance markets to secure agreements

- 2025: >5,300 hotels managed in high-governance regions

Geopolitics squeeze margins but subsidies fuel Accor’s 200-project, 5,300-hotel pipeline

Political risks (geo-tensions, sanctions, trade barriers) compressed margins via travel bans and tariff-driven material cost rises (~15%), forced market exits (Russia 2022 impairments) and increased compliance spend (>€200m sector fines 2022–23), while tourism subsidies and eased visas (OECD subsidies +18% YoY; EU receipts +8.2% 2024) supported Accor’s ~200-project 2025 pipeline and >5,300 managed hotels in stable markets.

| Metric | Value |

|---|---|

| Tariff impact on materials | ~15% |

| Sector regulatory fines (2022–23) | >€200m |

| OECD tourism subsidies YoY | +18% |

| EU tourism receipts 2024 | +8.2% |

| Accor 2025 projects | ~200 |

| Managed hotels in stable markets (2025) | >5,300 |

What is included in the product

Explores how macro-environmental factors uniquely affect AccorHotels across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region-specific insights and forward-looking implications to inform strategy, risk mitigation, and investor-ready documents.

A concise, neatly segmented PESTLE summary for AccorHotels that simplifies external risk and opportunity assessment, making it easy to drop into presentations, share across teams, or annotate with region-specific notes for faster strategic decisions.

Economic factors

Interest rate impacts on hospitality assets

By end-2025 global rate stabilization around 4–5% has tightened Accor’s capital expenditure, with net debt at EUR 2.9bn in FY2024 limiting cash deployment for new assets.

Higher borrowing costs versus 2010s have raised acquisition financing costs by ~200–300bps, making transactions pricier and nudging Accor toward asset-light strategies.

Focus shifts to higher-margin management and franchise fees, which accounted for ~60% of FY2024 recurring revenues, reducing reliance on property ownership.

Global inflation and consumer spending

Persistent inflation in services—global CPI for services rose 5.1% in 2024—has forced Accor to absorb higher labor and utility costs while keeping room rates competitive, squeezing margins particularly in economy and midscale brands. Luxury RevPAR grew 7% in 2024, showing resilience, but midscale RevPAR fell 2–3% in several markets as middle-class disposable income declined. Accor deploys dynamic pricing and revenue-management algorithms that lifted group-wide RevPAR by 4.5% in 2024, balancing yield and perceived value across its brand tiers.

Currency exchange rate volatility

As a French-headquartered group operating in 110+ countries, Accor faces material forex risk: a 10% EUR depreciation vs USD or major EM currencies could cut repatriated EBITDA by roughly 5–8% given 2024 geographic revenue mix (approx. 40% Europe, 30% APAC, 20% Americas, 10% MEA/AFR).

Labor market shortages and wage inflation

The hospitality sector faces structural labor shortages in 2025, pushing wage growth—average hotel hourly wages rose ~6.5% YoY in 2024—and higher benefits expectations, pressuring Accor’s payroll costs.

Accor needs greater investment in retention and training; 2024 reported staff costs increased ~8% and remain a key driver of margin pressure against 2025 RevPAR recovery targets.

- Wage inflation ~6–8% (2024–25)

- Staff costs +8% in 2024

- Retention/training capex rising to protect service quality

Growth of the middle class in Asia-Pacific

The expanding middle class in China and India—projected to add over 500 million people to global middle-income status by 2025—drives rising domestic and regional travel, boosting demand for Accor’s midscale and economy brands such as ibis and Novotel; this offsets slower growth in Western markets and supports RevPAR recovery (Asia Pacific RevPAR up ~45% YoY in 2023–24 for economy/midscale segments in several markets).

- ~500 million new middle-class consumers by 2025 (Asia-Pacific)

- Accor accelerating openings: thousands of rooms planned in India/China through 2025

- Domestic/regional travel growth fueling steadier occupancy vs West

Accor pivots asset‑light as fees fuel growth amid rising costs and APAC midscale demand

Higher rates and EUR 2.9bn net debt (FY2024) push Accor toward asset-light growth; management/franchise fees ~60% of FY2024 recurring revenue, RevPAR +4.5% group-wide in 2024 with luxury +7% and midscale -2–3%; wage inflation 6–8% and staff costs +8% in 2024 squeeze margins; APAC middle-class expansion (~500m by 2025) supports midscale openings.

| Metric | Value (2024/2025) |

|---|---|

| Net debt | EUR 2.9bn |

| Recurring revenue from fees | ~60% |

| Group RevPAR growth | +4.5% |

| Luxury RevPAR | +7% |

| Midscale RevPAR | -2–3% |

| Wage inflation | 6–8% |

| Staff costs YoY | +8% |

| APAC middle class add | ~500m by 2025 |

Full Version Awaits

AccorHotels PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the AccorHotels PESTLE analysis displayed is the real, final file with full content and structure.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and rising sustainability expectations are reshaping AccorHotels’ strategy and growth outlook—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter decisions. Purchase the full PESTLE analysis for a complete, editable report with deep-dive insights, data-backed forecasts, and practical recommendations you can use right away.

Political factors

Geopolitical instability in key regions

Geopolitical tensions in Eastern Europe and the Middle East in 2025 continue to reshape travel: UNWTO reported 2024 arrivals down 3% in affected corridors, and volatile Brent oil prices (range USD 70–95/bbl in 2024–25) drove regional transport costs higher, squeezing margins for Accor’s 5,500+ properties; sudden travel bans and advisories caused localized occupancy drops of 8–12%, forcing Accor to intensify contingency planning and diplomatic engagement to protect assets.

Government tourism incentives and support

Many governments in 2025 rolled out post-recovery tourism strategies providing tax breaks and infrastructure funds; OECD reports travel subsidies rose by 18% YoY, aiding hotel chains. Accor benefits notably in Southeast Asia and the Middle East, where governments subsidized luxury tourism—GCC tourism investment reached $45bn in 2024–25—boosting demand for upscale properties. Aligning with national agendas enabled Accor to secure favorable land leases and reduced-tax development terms for new builds and renovations, supporting its 2025 pipeline expansion of ~200 projects.

Visa and border policy changes

Streamlined visa processes in the Schengen Area and parts of Asia by late 2025 raised cross-border arrivals, with EU tourism receipts up 8.2% YoY in 2024 and intra-Asia travel growing 12% in H1 2025, benefiting Accor’s international occupancy. Conversely, tighter migration rules in some Western countries contributed to hospitality labor shortages, with EU hospitality vacancy rates reaching 7.1% in 2024. Accor closely monitors these shifts, adjusting recruitment—including a 15% rise in local hiring initiatives in 2024—and tailoring guest services to changing entry requirements.

International trade relations and sanctions

Trade disputes between major economies can trigger tariffs and export controls that raise costs for luxury goods and construction materials; e.g., 2023 steel and aluminum tariffs raised import costs by up to 15% for EU hotels, squeezing margins on Accor’s €1.8bn 2023 renovation capex pipeline.

Sanctions have forced hotel groups to exit markets; Accor suspended Russian operations in 2022 and recognized related impairment charges, illustrating risk of divestment and revenue loss in sanctioned jurisdictions.

Managing these pressures requires a strong legal and governmental affairs team; in 2024 Accor expanded compliance staffing after regulatory fines across the sector totaled over €200m globally in 2022–23.

- Tariff-driven cost increases up to 15% on materials

- 2022 Russia exit caused impairments for hotel groups

- Sector regulatory fines >€200m (2022–23)

- €1.8bn 2023 renovation capex exposed to trade risk

Political stability in emerging markets

Accor’s expansion into Africa and South America depends on political stability and rule of law; 2024 UNCTAD shows FDI flows to Africa rose 12% to about $60 billion while several countries still face governance risks that threaten hotel investments.

Political upheavals or ideological shifts can alter property rights or force profit repatriation, affecting returns on Accor’s long-term assets and concessions.

The group prioritizes markets with stable governance to protect franchise and management agreements; as of 2025 Accor reports over 5,300 hotels under management in high-governance markets.

- FDI to Africa +12% in 2024 (~$60bn)

- Political risk can reverse property rights or repatriation rules

- Accor favors stable-governance markets to secure agreements

- 2025: >5,300 hotels managed in high-governance regions

Geopolitics squeeze margins but subsidies fuel Accor’s 200-project, 5,300-hotel pipeline

Political risks (geo-tensions, sanctions, trade barriers) compressed margins via travel bans and tariff-driven material cost rises (~15%), forced market exits (Russia 2022 impairments) and increased compliance spend (>€200m sector fines 2022–23), while tourism subsidies and eased visas (OECD subsidies +18% YoY; EU receipts +8.2% 2024) supported Accor’s ~200-project 2025 pipeline and >5,300 managed hotels in stable markets.

| Metric | Value |

|---|---|

| Tariff impact on materials | ~15% |

| Sector regulatory fines (2022–23) | >€200m |

| OECD tourism subsidies YoY | +18% |

| EU tourism receipts 2024 | +8.2% |

| Accor 2025 projects | ~200 |

| Managed hotels in stable markets (2025) | >5,300 |

What is included in the product

Explores how macro-environmental factors uniquely affect AccorHotels across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region-specific insights and forward-looking implications to inform strategy, risk mitigation, and investor-ready documents.

A concise, neatly segmented PESTLE summary for AccorHotels that simplifies external risk and opportunity assessment, making it easy to drop into presentations, share across teams, or annotate with region-specific notes for faster strategic decisions.

Economic factors

Interest rate impacts on hospitality assets

By end-2025 global rate stabilization around 4–5% has tightened Accor’s capital expenditure, with net debt at EUR 2.9bn in FY2024 limiting cash deployment for new assets.

Higher borrowing costs versus 2010s have raised acquisition financing costs by ~200–300bps, making transactions pricier and nudging Accor toward asset-light strategies.

Focus shifts to higher-margin management and franchise fees, which accounted for ~60% of FY2024 recurring revenues, reducing reliance on property ownership.

Global inflation and consumer spending

Persistent inflation in services—global CPI for services rose 5.1% in 2024—has forced Accor to absorb higher labor and utility costs while keeping room rates competitive, squeezing margins particularly in economy and midscale brands. Luxury RevPAR grew 7% in 2024, showing resilience, but midscale RevPAR fell 2–3% in several markets as middle-class disposable income declined. Accor deploys dynamic pricing and revenue-management algorithms that lifted group-wide RevPAR by 4.5% in 2024, balancing yield and perceived value across its brand tiers.

Currency exchange rate volatility

As a French-headquartered group operating in 110+ countries, Accor faces material forex risk: a 10% EUR depreciation vs USD or major EM currencies could cut repatriated EBITDA by roughly 5–8% given 2024 geographic revenue mix (approx. 40% Europe, 30% APAC, 20% Americas, 10% MEA/AFR).

Labor market shortages and wage inflation

The hospitality sector faces structural labor shortages in 2025, pushing wage growth—average hotel hourly wages rose ~6.5% YoY in 2024—and higher benefits expectations, pressuring Accor’s payroll costs.

Accor needs greater investment in retention and training; 2024 reported staff costs increased ~8% and remain a key driver of margin pressure against 2025 RevPAR recovery targets.

- Wage inflation ~6–8% (2024–25)

- Staff costs +8% in 2024

- Retention/training capex rising to protect service quality

Growth of the middle class in Asia-Pacific

The expanding middle class in China and India—projected to add over 500 million people to global middle-income status by 2025—drives rising domestic and regional travel, boosting demand for Accor’s midscale and economy brands such as ibis and Novotel; this offsets slower growth in Western markets and supports RevPAR recovery (Asia Pacific RevPAR up ~45% YoY in 2023–24 for economy/midscale segments in several markets).

- ~500 million new middle-class consumers by 2025 (Asia-Pacific)

- Accor accelerating openings: thousands of rooms planned in India/China through 2025

- Domestic/regional travel growth fueling steadier occupancy vs West

Accor pivots asset‑light as fees fuel growth amid rising costs and APAC midscale demand

Higher rates and EUR 2.9bn net debt (FY2024) push Accor toward asset-light growth; management/franchise fees ~60% of FY2024 recurring revenue, RevPAR +4.5% group-wide in 2024 with luxury +7% and midscale -2–3%; wage inflation 6–8% and staff costs +8% in 2024 squeeze margins; APAC middle-class expansion (~500m by 2025) supports midscale openings.

| Metric | Value (2024/2025) |

|---|---|

| Net debt | EUR 2.9bn |

| Recurring revenue from fees | ~60% |

| Group RevPAR growth | +4.5% |

| Luxury RevPAR | +7% |

| Midscale RevPAR | -2–3% |

| Wage inflation | 6–8% |

| Staff costs YoY | +8% |

| APAC middle class add | ~500m by 2025 |

Full Version Awaits

AccorHotels PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the AccorHotels PESTLE analysis displayed is the real, final file with full content and structure.