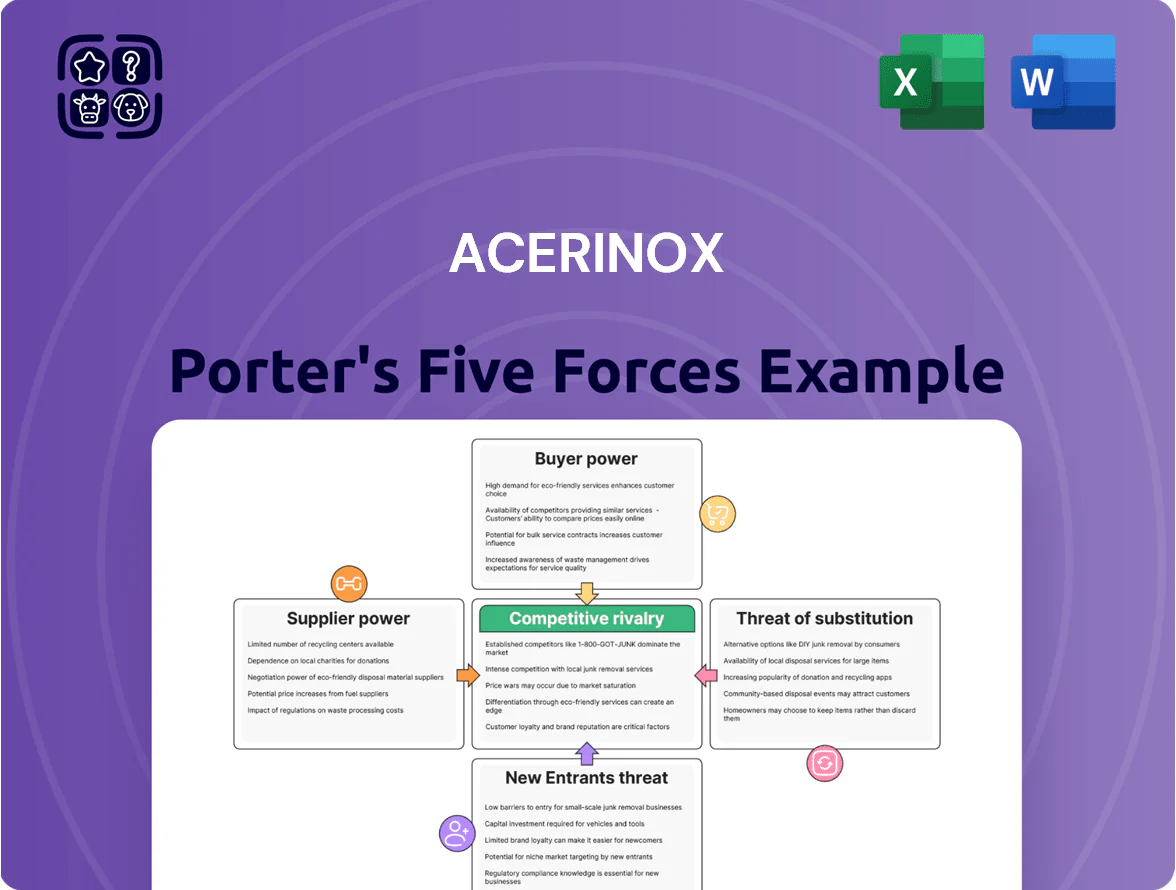

Acerinox Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Acerinox faces moderate rivalry with cyclicality-driven pricing pressure, concentrated raw material suppliers, and steady buyer bargaining from large distributors, while barriers to entry remain high due to capital intensity and scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acerinox’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

The production of stainless steel depends on nickel, chromium and molybdenum, whose 2024 price swings were large—nickel up ~35% y/y in LME average, molybdenum +18%—making these inputs a major share (25–35%) of Acerinox’s COGS and giving suppliers leverage.

Acerinox uses forward contracts and metal hedges; sudden LME moves in 2024 wiped ~€40–70/ton off margins, so hedging complexity is high and essential.

Mining for nickel and molybdenum is concentrated (top 5 producers >60% supply), limiting alternative sourcing despite long-term supplier ties and raising supplier bargaining power.

Energy market dependence

Stainless steel making is energy-heavy; electricity and gas account for about 20–30% of production costs, so stable low-cost supply is critical.

In Europe, where Acerinox had €2.8bn sales in 2024, suppliers hold strong bargaining power amid regulatory shifts and 2022–2024 gas volatility raising industrial prices by ~40% in some months.

Renewable transition creates new vendor lock‑ins for grid and storage, increasing dependence on specific utilities and infrastructure investments.

Price swings cut Acerinox’s cost competitiveness versus producers in lower‑cost regions; a €10/MWh electricity rise can shave several euros per tonne of margin.

Scrap metal availability

Acerinox uses about 70% recycled stainless scrap as feedstock, cutting ore dependence and CO2; high-quality scrap comes from a fragmented network of collectors/processors who can push prices in tight markets. Global scrap demand rose ~8% in 2024, tightening supply and raising supplier leverage, while local scrap access remains critical to cut logistics (savings up to 15% per tonne) and keep mills running.

Concentration of specialized technology providers

The maintenance and upgrading of Acerinox’s smelting and rolling lines depends on a few global engineering firms that control proprietary tech and long-term service contracts; in 2024 capital equipment suppliers accounted for roughly 60% of major plant outages globally, raising supplier leverage.

Disruption in spare parts or specialist engineers can cause multi-week downtime costing millions—Acerinox must secure multi-year agreements and local stocking to keep efficiency and quality high.

- Few suppliers = high bargaining power

- Proprietary tech → long service contracts

- Spare-part delays → multi-week, multi-million losses

- Mitigation: multi-year deals, local inventories

Logistics and transportation constraints

Shipping and logistics firms are key for moving Acerinox’s bulky steel inputs and products; in 2023 container freight rates spiked 120% year-over-year during congestion, raising supplier leverage.

Acerinox’s integrated global footprint—plants in Europe, Americas, and Africa—means a 1–3% fuel price rise can add several million euros to annual transport costs, increasing suppliers’ bargaining power.

To reduce exposure, Acerinox invests in logistics hubs and long-term contracts; owning or controlling terminals lowers spot-rate sensitivity and caps freight-cost volatility.

- 2023 container rate surge: +120%

- Fuel cost sensitivity: 1–3% rise → millions € impact

- Mitigation: logistics hubs, long-term freight contracts

Supplier squeeze: nickel surge, energy costs cut margins €40–70/ton; scrap use rises

Suppliers exert medium‑high power: key alloys (nickel +35% y/y 2024 LME), energy (20–30% costs) and spare‑parts/services are concentrated, while 70% scrap use and forward hedges mitigate but don’t eliminate risk—2024 metal swings cut margins €40–70/ton and global scrap demand rose ~8%.

| Metric | 2024 value |

|---|---|

| Nickel LME change | +35% y/y |

| Scrap share | 70% |

| Margin hit | €40–70/ton |

| Scrap demand | +8% |

What is included in the product

Tailored Porter’s Five Forces analysis for Acerinox, uncovering key competitive drivers, supplier and buyer power, substitution risks, and barriers to entry that shape its pricing, margins, and strategic positioning.

A concise Porter's Five Forces snapshot for Acerinox—ideal for swift strategic decisions and boardroom use.

Customers Bargaining Power

Industrial buyer concentration

Availability of commodity alternatives

For standard stainless-steel grades, buyers treat sheets and coils as commodities, so price dominates purchasing choices; global supply from >50 major producers lets customers compare quotes quickly and push for lower prices.

Market transparency—benchmarks like CRU and Platts showing spot spread swings of ±8–12% in 2024—limits Acerinox’s ability to earn premiums on basic flat products.

Acerinox counters by selling differentiated, high-performance alloys and value-added services—these niche lines, ~22% of 2024 sales, face less buyer mobility and command higher margins.

Low switching costs for standard grades

Low switching costs in general-purpose stainless steel let buyers shift suppliers easily; standardized grades (AISI/EN specs) mean the mill of origin often doesn't matter, so purchasers push prices down—spot prices for cold-rolled 304 dropped ~12% in 2024 in Europe, showing price pressure.

Acerinox fights this by deepening supply-chain ties: in 2024 it expanded just-in-time delivery contracts and technical service teams, raising contract share to ~62% of sales to lock demand and reduce buyer bargaining leverage.

Sensitivity to economic cycles

The demand for stainless steel is highly cyclical and tracked to global GDP; World Steel Association data showed a 2.3% global stainless-steel demand change in 2024, heightening buyer leverage in downturns.

When construction and consumer-goods buyers cut orders, Acerinox faces stronger customer bargaining power and must flex production to protect margins and utilization.

Geographic diversification—mills in Spain, USA, South Africa, Mexico—helps balance regional demand swings and customer power.

- Stainless demand tied to GDP; 2024 change +2.3%

- Downturns raise buyer leverage via order cuts

- Flexible production reduces price pressure

- Global footprint evens regional demand shifts

Influence of large distributors

Acerinox sells large volumes via independent service centers and distributors that aggregate demand from thousands of small users; in 2024 roughly 40% of global stainless shipments flowed through such channels, concentrating bargaining power.

Distributors can switch suppliers quickly based on price and lead times, pressuring Acerinox on margins; their local inventory visibility and market intelligence strengthen negotiation leverage.

Keeping balanced terms and reliable supply is vital to secure steady volumes and a predictable order book.

- ~40% stainless via distributors (2024)

- Distributors shift based on price/lead time

- Local inventory intel boosts their leverage

- Stable terms needed for volume predictability

Buyers squeeze prices; Acerinox leans on contracts and niche alloys to protect margins

Buyers hold strong leverage: large industrial customers (≈62% of demand in 2024) and distributors (~40% of shipments) push prices and terms; commodity grades drove spot 304 CR down ~12% in Europe (2024), while niche alloy sales (~22% of Acerinox 2024 revenue) earn premiums. Acerinox raised contract share to ~62% in 2024 to limit switching and stabilize margins.

| Metric | 2024 |

|---|---|

| Industrial demand share | 62% |

| Distributor flow | 40% |

| Niche sales | 22% |

| Contract share | 62% |

Full Version Awaits

Acerinox Porter's Five Forces Analysis

This preview shows the exact Acerinox Porter’s Five Forces analysis you will receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use; it assesses competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. The document displayed here is the actual file you’ll be able to download instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Acerinox faces moderate rivalry with cyclicality-driven pricing pressure, concentrated raw material suppliers, and steady buyer bargaining from large distributors, while barriers to entry remain high due to capital intensity and scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acerinox’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

The production of stainless steel depends on nickel, chromium and molybdenum, whose 2024 price swings were large—nickel up ~35% y/y in LME average, molybdenum +18%—making these inputs a major share (25–35%) of Acerinox’s COGS and giving suppliers leverage.

Acerinox uses forward contracts and metal hedges; sudden LME moves in 2024 wiped ~€40–70/ton off margins, so hedging complexity is high and essential.

Mining for nickel and molybdenum is concentrated (top 5 producers >60% supply), limiting alternative sourcing despite long-term supplier ties and raising supplier bargaining power.

Energy market dependence

Stainless steel making is energy-heavy; electricity and gas account for about 20–30% of production costs, so stable low-cost supply is critical.

In Europe, where Acerinox had €2.8bn sales in 2024, suppliers hold strong bargaining power amid regulatory shifts and 2022–2024 gas volatility raising industrial prices by ~40% in some months.

Renewable transition creates new vendor lock‑ins for grid and storage, increasing dependence on specific utilities and infrastructure investments.

Price swings cut Acerinox’s cost competitiveness versus producers in lower‑cost regions; a €10/MWh electricity rise can shave several euros per tonne of margin.

Scrap metal availability

Acerinox uses about 70% recycled stainless scrap as feedstock, cutting ore dependence and CO2; high-quality scrap comes from a fragmented network of collectors/processors who can push prices in tight markets. Global scrap demand rose ~8% in 2024, tightening supply and raising supplier leverage, while local scrap access remains critical to cut logistics (savings up to 15% per tonne) and keep mills running.

Concentration of specialized technology providers

The maintenance and upgrading of Acerinox’s smelting and rolling lines depends on a few global engineering firms that control proprietary tech and long-term service contracts; in 2024 capital equipment suppliers accounted for roughly 60% of major plant outages globally, raising supplier leverage.

Disruption in spare parts or specialist engineers can cause multi-week downtime costing millions—Acerinox must secure multi-year agreements and local stocking to keep efficiency and quality high.

- Few suppliers = high bargaining power

- Proprietary tech → long service contracts

- Spare-part delays → multi-week, multi-million losses

- Mitigation: multi-year deals, local inventories

Logistics and transportation constraints

Shipping and logistics firms are key for moving Acerinox’s bulky steel inputs and products; in 2023 container freight rates spiked 120% year-over-year during congestion, raising supplier leverage.

Acerinox’s integrated global footprint—plants in Europe, Americas, and Africa—means a 1–3% fuel price rise can add several million euros to annual transport costs, increasing suppliers’ bargaining power.

To reduce exposure, Acerinox invests in logistics hubs and long-term contracts; owning or controlling terminals lowers spot-rate sensitivity and caps freight-cost volatility.

- 2023 container rate surge: +120%

- Fuel cost sensitivity: 1–3% rise → millions € impact

- Mitigation: logistics hubs, long-term freight contracts

Supplier squeeze: nickel surge, energy costs cut margins €40–70/ton; scrap use rises

Suppliers exert medium‑high power: key alloys (nickel +35% y/y 2024 LME), energy (20–30% costs) and spare‑parts/services are concentrated, while 70% scrap use and forward hedges mitigate but don’t eliminate risk—2024 metal swings cut margins €40–70/ton and global scrap demand rose ~8%.

| Metric | 2024 value |

|---|---|

| Nickel LME change | +35% y/y |

| Scrap share | 70% |

| Margin hit | €40–70/ton |

| Scrap demand | +8% |

What is included in the product

Tailored Porter’s Five Forces analysis for Acerinox, uncovering key competitive drivers, supplier and buyer power, substitution risks, and barriers to entry that shape its pricing, margins, and strategic positioning.

A concise Porter's Five Forces snapshot for Acerinox—ideal for swift strategic decisions and boardroom use.

Customers Bargaining Power

Industrial buyer concentration

Availability of commodity alternatives

For standard stainless-steel grades, buyers treat sheets and coils as commodities, so price dominates purchasing choices; global supply from >50 major producers lets customers compare quotes quickly and push for lower prices.

Market transparency—benchmarks like CRU and Platts showing spot spread swings of ±8–12% in 2024—limits Acerinox’s ability to earn premiums on basic flat products.

Acerinox counters by selling differentiated, high-performance alloys and value-added services—these niche lines, ~22% of 2024 sales, face less buyer mobility and command higher margins.

Low switching costs for standard grades

Low switching costs in general-purpose stainless steel let buyers shift suppliers easily; standardized grades (AISI/EN specs) mean the mill of origin often doesn't matter, so purchasers push prices down—spot prices for cold-rolled 304 dropped ~12% in 2024 in Europe, showing price pressure.

Acerinox fights this by deepening supply-chain ties: in 2024 it expanded just-in-time delivery contracts and technical service teams, raising contract share to ~62% of sales to lock demand and reduce buyer bargaining leverage.

Sensitivity to economic cycles

The demand for stainless steel is highly cyclical and tracked to global GDP; World Steel Association data showed a 2.3% global stainless-steel demand change in 2024, heightening buyer leverage in downturns.

When construction and consumer-goods buyers cut orders, Acerinox faces stronger customer bargaining power and must flex production to protect margins and utilization.

Geographic diversification—mills in Spain, USA, South Africa, Mexico—helps balance regional demand swings and customer power.

- Stainless demand tied to GDP; 2024 change +2.3%

- Downturns raise buyer leverage via order cuts

- Flexible production reduces price pressure

- Global footprint evens regional demand shifts

Influence of large distributors

Acerinox sells large volumes via independent service centers and distributors that aggregate demand from thousands of small users; in 2024 roughly 40% of global stainless shipments flowed through such channels, concentrating bargaining power.

Distributors can switch suppliers quickly based on price and lead times, pressuring Acerinox on margins; their local inventory visibility and market intelligence strengthen negotiation leverage.

Keeping balanced terms and reliable supply is vital to secure steady volumes and a predictable order book.

- ~40% stainless via distributors (2024)

- Distributors shift based on price/lead time

- Local inventory intel boosts their leverage

- Stable terms needed for volume predictability

Buyers squeeze prices; Acerinox leans on contracts and niche alloys to protect margins

Buyers hold strong leverage: large industrial customers (≈62% of demand in 2024) and distributors (~40% of shipments) push prices and terms; commodity grades drove spot 304 CR down ~12% in Europe (2024), while niche alloy sales (~22% of Acerinox 2024 revenue) earn premiums. Acerinox raised contract share to ~62% in 2024 to limit switching and stabilize margins.

| Metric | 2024 |

|---|---|

| Industrial demand share | 62% |

| Distributor flow | 40% |

| Niche sales | 22% |

| Contract share | 62% |

Full Version Awaits

Acerinox Porter's Five Forces Analysis

This preview shows the exact Acerinox Porter’s Five Forces analysis you will receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use; it assesses competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. The document displayed here is the actual file you’ll be able to download instantly upon payment.