ACS Solutions PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

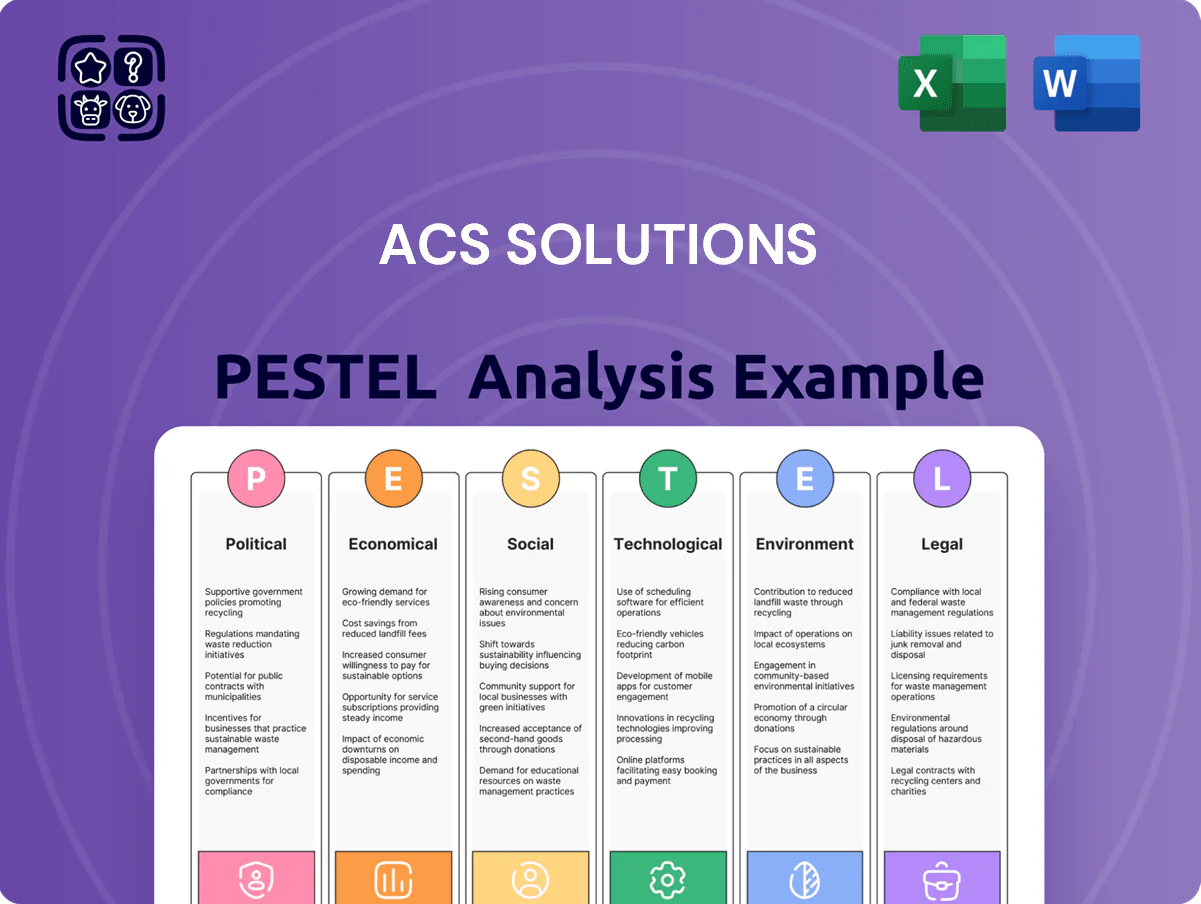

Discover how political, economic, social, technological, legal, and environmental forces are shaping ACS Solutions’ trajectory with our concise PESTLE Analysis—designed for investors, strategists, and consultants seeking actionable insight; purchase the full report to access detailed drivers, risks, and opportunities you can apply immediately.

Political factors

Government digital modernization initiatives

The continued push for digital sovereignty and modernized public infrastructure by late 2025 — with OECD governments planning EUR 150+ billion in digital transformation budgets in 2024–25 — creates major opportunities for ACS Solutions to win contracts migrating legacy systems.

Government agencies outsourced 37% more IT services in 2023–24 to close skill gaps, increasing demand for ACS’s end-to-end migration and cloud services.

To capture these lucrative public-sector deals ACS must navigate procurement cycles averaging 9–14 months and maintain high security clearances and compliance with standards like NIST and EU cybersecurity rules.

Geopolitical stability and offshore operations

Geopolitical tensions between US, China, and EU tech hubs in 2025—with global FDI into tech dipping 8% YoY to $320bn—raise risk of service disruptions for ACS, which relies on cross-border workflows. Trade restrictions and tighter visa rules cut skilled mobility, with H-1B approvals down ~12% in 2024–25, pressuring staffing models. ACS must diversify delivery centers; companies with multi‑region footprints saw 15% higher continuity scores during 2023–25 regional shocks.

National security and cybersecurity policy

Trade agreements and intellectual property

Evolving trade agreements like CPTPP and USMCA reshape ACS Solutions IP strategies, requiring compliance across 15+ jurisdictions; firms report 22% higher licensing disputes when multijurisdictional protections lapse.

Recent shifts in tax treaties and OECD BEPS 2.0 rules can alter effective tax rates on cross-border IT consulting margins—multinational firms saw ETR swings of 3–6 percentage points in 2024.

ACS must continuously monitor political changes to maintain tax-efficient structures and enforce IP protections, reducing legal risk and preserving global consulting profitability.

- Track CPTPP/USMCA/IPR clauses across 15+ markets

- Model ETR impact from BEPS 2.0 (3–6 ppt variance)

- Ensure multijurisdictional IP filings to lower 22% dispute risk

Incentives for domestic technology growth

Many governments in 2024–25 offered targeted incentives—grants, tax credits and training subsidies—totaling over $45B globally for domestic tech development, which ACS can access to reduce capex and training costs when opening labs in India, Vietnam or Mexico.

Aligning ACS strategy with local tech policies improves market access and can raise hiring retention by 10–15% versus non-aligned entrants, per regional labor studies.

- Access to grants and tax credits lowers expansion capex

- Training subsidies offset up to 30% of workforce development costs

- Policy alignment boosts local integration and retention

Public-sector tech boom fuels ACS pipeline—procurement, compliance & tax hurdles ahead

Political drivers—EUR 150B OECD digital budgets (2024–25), $215B cybersecurity spend (2024–25), and 37% rise in outsourced gov IT (2023–24)—boost ACS Solutions’ public-sector pipeline but require 9–14 month procurements, NIST/NIS2 compliance, multijurisdictional IP/tax management (BEPS 2.0 ETR swing 3–6 ppt) and diversified delivery centers amid an 8% YoY tech FDI decline (2025).

| Metric | Value |

|---|---|

| OECD digital budgets (2024–25) | €150B+ |

| Global cybersecurity spend (2024–25) | $215B |

| Govt IT outsourcing growth (2023–24) | +37% |

| Tech FDI (2025) | $320B (-8% YoY) |

| ETR variance (BEPS 2.0, 2024) | 3–6 ppt |

What is included in the product

Explores how external macro-environmental factors uniquely affect ACS Solutions across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

Condenses ACS Solutions' full PESTLE into a clean, shareable summary that’s visually segmented by factor, making it easy to drop into presentations, support planning discussions on external risks, and align teams quickly.

Economic factors

Global IT spending and budget cycles

By end-2025 global IT spending reached about 4.6 trillion USD, with corporate IT budgets stabilizing and prioritizing high-ROI digital transformation; ACS Solutions must align pricing to demonstrate efficiency and measurable outcomes tied to ROI metrics.

The shift to subscription and outcome-oriented models—SaaS revenue grew ~12% YoY in 2024—requires ACS adopt flexible financial project management, with usage-based billing and KPIs-driven SLAs to match client expectations.

Labor cost inflation and talent acquisition

The rising cost of highly skilled technical labor is squeezing margins for staffing and IT service firms; global tech wages rose ~6.8% in 2024 with software/AI roles up to 10–15% in key markets, forcing ACS to balance competitive pay and margin targets.

To secure talent in AI and cloud computing, ACS must offer premium packages amid a 2024–25 tight labor market where vacancy-to-unemployment ratios remain elevated in US/EU tech hubs.

Regional wage growth variance—e.g., 2024 average wage growth 5.5% in North America vs 3% in APAC—requires ACS a dynamic, globalized compensation strategy tied to local salary indices and inflation adjustments.

Currency exchange rate volatility

As ACS operates across multiple international markets, 2025 exchange-rate swings—USD strength up ~6% vs. EUR and 4% vs. INR in 2024—can materially affect reported earnings and operational costs, compressing margins if revenues are dollar-linked but costs local.

Managing currency risk via hedging (for example FX forwards covering 30–60% of projected exposures) or localized billing in euros/rupees becomes essential to preserve cash flow stability.

Unexpected dollar moves can change competitiveness of offshore delivery centers; a 5% USD appreciation versus INR can raise India-based cost of sales by similar magnitude, altering pricing power and contract renegotiations.

Interest rates and capital investment

By late 2025 US 10-year Treasury yields settled around 4.2% and average corporate borrowing costs remained near 5–6%, so ACS faces meaningful capital costs that slow internal tech investment and large infrastructure projects.

High financing rates constrain aggressive M&A; ACS should focus on organic growth, prioritize projects with >15% IRR, and manage cash conversion cycles to avoid over-leveraging.

- 10-year Treasury ~4.2% (late 2025)

- Corporate borrowing ~5–6%

- Target project hurdle >15% IRR

- Emphasize cash conversion and organic funding

Gig economy and flexible workforce trends

The gig economy grew to represent about 36% of US workers in 2024, shifting demand toward project-based staffing and pressuring ACS to redesign pricing and engagement models to serve more fluid talent pools.

Adapting reduces fixed overhead—contingent staffing can cut labor-related costs by 15–25%—but requires advanced talent management, real-time matching and compliance systems to ensure consistent service quality.

- 36% of US workers in gig roles (2024)

- 15–25% potential labor cost reduction via contingent staffing

- Need for real-time matching, compliance, and talent pipeline tools

ACS must reprice, adopt usage billing & hedging to hit >15% IRR amid tightening macro

Macro pressures—4.6T global IT spend (2025), 12% SaaS growth (2024), tech wages +6.8% (2024), USD +6% vs EUR (2024), US 10y ~4.2% (late‑2025), corporate borrowing 5–6%—force ACS to optimize pricing, adopt usage billing, hedge FX (30–60%), prioritize >15% IRR projects and leverage contingent staffing (36% gig share, 15–25% cost cut).

| Metric | Value |

|---|---|

| Global IT spend (2025) | 4.6T USD |

| SaaS growth (2024) | ~12% |

| Tech wage growth (2024) | ~6.8% |

| USD vs EUR (2024) | +6% |

| US 10y (late‑2025) | ~4.2% |

| Gig economy (2024) | 36% |

Preview Before You Purchase

ACS Solutions PESTLE Analysis

The preview shown here is the exact ACS Solutions PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping ACS Solutions’ trajectory with our concise PESTLE Analysis—designed for investors, strategists, and consultants seeking actionable insight; purchase the full report to access detailed drivers, risks, and opportunities you can apply immediately.

Political factors

Government digital modernization initiatives

The continued push for digital sovereignty and modernized public infrastructure by late 2025 — with OECD governments planning EUR 150+ billion in digital transformation budgets in 2024–25 — creates major opportunities for ACS Solutions to win contracts migrating legacy systems.

Government agencies outsourced 37% more IT services in 2023–24 to close skill gaps, increasing demand for ACS’s end-to-end migration and cloud services.

To capture these lucrative public-sector deals ACS must navigate procurement cycles averaging 9–14 months and maintain high security clearances and compliance with standards like NIST and EU cybersecurity rules.

Geopolitical stability and offshore operations

Geopolitical tensions between US, China, and EU tech hubs in 2025—with global FDI into tech dipping 8% YoY to $320bn—raise risk of service disruptions for ACS, which relies on cross-border workflows. Trade restrictions and tighter visa rules cut skilled mobility, with H-1B approvals down ~12% in 2024–25, pressuring staffing models. ACS must diversify delivery centers; companies with multi‑region footprints saw 15% higher continuity scores during 2023–25 regional shocks.

National security and cybersecurity policy

Trade agreements and intellectual property

Evolving trade agreements like CPTPP and USMCA reshape ACS Solutions IP strategies, requiring compliance across 15+ jurisdictions; firms report 22% higher licensing disputes when multijurisdictional protections lapse.

Recent shifts in tax treaties and OECD BEPS 2.0 rules can alter effective tax rates on cross-border IT consulting margins—multinational firms saw ETR swings of 3–6 percentage points in 2024.

ACS must continuously monitor political changes to maintain tax-efficient structures and enforce IP protections, reducing legal risk and preserving global consulting profitability.

- Track CPTPP/USMCA/IPR clauses across 15+ markets

- Model ETR impact from BEPS 2.0 (3–6 ppt variance)

- Ensure multijurisdictional IP filings to lower 22% dispute risk

Incentives for domestic technology growth

Many governments in 2024–25 offered targeted incentives—grants, tax credits and training subsidies—totaling over $45B globally for domestic tech development, which ACS can access to reduce capex and training costs when opening labs in India, Vietnam or Mexico.

Aligning ACS strategy with local tech policies improves market access and can raise hiring retention by 10–15% versus non-aligned entrants, per regional labor studies.

- Access to grants and tax credits lowers expansion capex

- Training subsidies offset up to 30% of workforce development costs

- Policy alignment boosts local integration and retention

Public-sector tech boom fuels ACS pipeline—procurement, compliance & tax hurdles ahead

Political drivers—EUR 150B OECD digital budgets (2024–25), $215B cybersecurity spend (2024–25), and 37% rise in outsourced gov IT (2023–24)—boost ACS Solutions’ public-sector pipeline but require 9–14 month procurements, NIST/NIS2 compliance, multijurisdictional IP/tax management (BEPS 2.0 ETR swing 3–6 ppt) and diversified delivery centers amid an 8% YoY tech FDI decline (2025).

| Metric | Value |

|---|---|

| OECD digital budgets (2024–25) | €150B+ |

| Global cybersecurity spend (2024–25) | $215B |

| Govt IT outsourcing growth (2023–24) | +37% |

| Tech FDI (2025) | $320B (-8% YoY) |

| ETR variance (BEPS 2.0, 2024) | 3–6 ppt |

What is included in the product

Explores how external macro-environmental factors uniquely affect ACS Solutions across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

Condenses ACS Solutions' full PESTLE into a clean, shareable summary that’s visually segmented by factor, making it easy to drop into presentations, support planning discussions on external risks, and align teams quickly.

Economic factors

Global IT spending and budget cycles

By end-2025 global IT spending reached about 4.6 trillion USD, with corporate IT budgets stabilizing and prioritizing high-ROI digital transformation; ACS Solutions must align pricing to demonstrate efficiency and measurable outcomes tied to ROI metrics.

The shift to subscription and outcome-oriented models—SaaS revenue grew ~12% YoY in 2024—requires ACS adopt flexible financial project management, with usage-based billing and KPIs-driven SLAs to match client expectations.

Labor cost inflation and talent acquisition

The rising cost of highly skilled technical labor is squeezing margins for staffing and IT service firms; global tech wages rose ~6.8% in 2024 with software/AI roles up to 10–15% in key markets, forcing ACS to balance competitive pay and margin targets.

To secure talent in AI and cloud computing, ACS must offer premium packages amid a 2024–25 tight labor market where vacancy-to-unemployment ratios remain elevated in US/EU tech hubs.

Regional wage growth variance—e.g., 2024 average wage growth 5.5% in North America vs 3% in APAC—requires ACS a dynamic, globalized compensation strategy tied to local salary indices and inflation adjustments.

Currency exchange rate volatility

As ACS operates across multiple international markets, 2025 exchange-rate swings—USD strength up ~6% vs. EUR and 4% vs. INR in 2024—can materially affect reported earnings and operational costs, compressing margins if revenues are dollar-linked but costs local.

Managing currency risk via hedging (for example FX forwards covering 30–60% of projected exposures) or localized billing in euros/rupees becomes essential to preserve cash flow stability.

Unexpected dollar moves can change competitiveness of offshore delivery centers; a 5% USD appreciation versus INR can raise India-based cost of sales by similar magnitude, altering pricing power and contract renegotiations.

Interest rates and capital investment

By late 2025 US 10-year Treasury yields settled around 4.2% and average corporate borrowing costs remained near 5–6%, so ACS faces meaningful capital costs that slow internal tech investment and large infrastructure projects.

High financing rates constrain aggressive M&A; ACS should focus on organic growth, prioritize projects with >15% IRR, and manage cash conversion cycles to avoid over-leveraging.

- 10-year Treasury ~4.2% (late 2025)

- Corporate borrowing ~5–6%

- Target project hurdle >15% IRR

- Emphasize cash conversion and organic funding

Gig economy and flexible workforce trends

The gig economy grew to represent about 36% of US workers in 2024, shifting demand toward project-based staffing and pressuring ACS to redesign pricing and engagement models to serve more fluid talent pools.

Adapting reduces fixed overhead—contingent staffing can cut labor-related costs by 15–25%—but requires advanced talent management, real-time matching and compliance systems to ensure consistent service quality.

- 36% of US workers in gig roles (2024)

- 15–25% potential labor cost reduction via contingent staffing

- Need for real-time matching, compliance, and talent pipeline tools

ACS must reprice, adopt usage billing & hedging to hit >15% IRR amid tightening macro

Macro pressures—4.6T global IT spend (2025), 12% SaaS growth (2024), tech wages +6.8% (2024), USD +6% vs EUR (2024), US 10y ~4.2% (late‑2025), corporate borrowing 5–6%—force ACS to optimize pricing, adopt usage billing, hedge FX (30–60%), prioritize >15% IRR projects and leverage contingent staffing (36% gig share, 15–25% cost cut).

| Metric | Value |

|---|---|

| Global IT spend (2025) | 4.6T USD |

| SaaS growth (2024) | ~12% |

| Tech wage growth (2024) | ~6.8% |

| USD vs EUR (2024) | +6% |

| US 10y (late‑2025) | ~4.2% |

| Gig economy (2024) | 36% |

Preview Before You Purchase

ACS Solutions PESTLE Analysis

The preview shown here is the exact ACS Solutions PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.