ACTIA Group PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how macro forces—from regulatory shifts in automotive electronics to rapid tech innovation and supply-chain vulnerabilities—are reshaping ACTIA Group’s strategic landscape; our concise PESTLE highlights risks and opportunities you can act on today. Buy the full PESTLE for the complete, editable analysis and actionable insights to inform investment decisions, strategic planning, or competitive benchmarking.

Political factors

European Industrial Sovereignty

European push for technological autonomy compels ACTIA to align with EU industrial sovereignty goals, tapping into €43bn NextGenerationEU and IPCEI semiconductor funding streams to bolster regional manufacturing and R&D capacity.

Geopolitical Trade Dynamics

Shifting trade relations—notably EU-US tariff frictions and China supply-chain realignments—affect ACTIA’s access to semiconductors and connectors, with global chip shortages reducing component availability by ~15% in 2023 and raising input costs ~8–12%. Complex tariffs and non-tariff barriers can widen margins; a 5% tariff on select electronic modules would cut EBIT by several points on low-margin diagnostic lines. Diversifying plants across France, Morocco and Romania reduces exposure to regional disruption and supports onshoring trends that grew 10% in 2024.

Defense and Security Spending

Rising European defense budgets—EU members increased collective defense spending to over €230 billion in 2024, up ~5% year-on-year—expand demand for ACTIA’s telecom and embedded systems, especially high-reliability electronics for aerospace and land platforms; national modernization programs (e.g., France €50+ billion military plan 2024–2030) promise steady procurement pipelines, providing ACTIA a defensive revenue stream that offsets cyclical weakness in its automotive business.

Green Mobility Mandates

- EU 2035 ICE ban accelerates EV component demand

- €5–8bn public transport electrification funding (2024–25)

- 14% global EV share of new car sales in 2024

- ACTIA EV R&D +12% in 2024

Standardization and Global Cooperation

International agreements on ISO/SAE standards for connected vehicles ease ACTIA Group's telematics rollout; ISO 21217 and SAE J2735 harmonization supports faster market entry across EU, US, China where ADAS telematics market exceeded USD 18.5B in 2024.

Cooperative aerospace safety frameworks and ITU satellite comms allocations create predictable certification pathways—crucial as global satcom revenue reached ~USD 85B in 2024, lowering compliance uncertainty for ACTIA's avionics products.

Maintaining alignment with these global standards is vital for ACTIA to protect export revenues (approx. 60% of group sales in 2024) and sustain competitive advantage internationally.

- Harmonized vehicle standards: ISO/SAE (enables faster deployment)

- Aerospace/satellite frameworks: predictable certification, lower time-to-market

- Financial relevance: ADAS telematics USD 18.5B and satcom USD 85B (2024)

- Export exposure: ~60% of ACTIA Group 2024 sales

EU funds, defense & EV demand props ACTIA growth amid chip-driven cost pressures

EU industrial sovereignty and €43bn NextGenerationEU/IPCEI funds boost ACTIA R&D/onshoring; trade shifts and 15% chip shortages in 2023 raised input costs 8–12%, mitigated by diversification (France, Morocco, Romania). Rising defense spend (€230bn EU 2024) and EV policies (EU 2035 ICE ban; global EVs 14% of sales 2024) expand stable revenue streams; exports ≈60% of 2024 sales.

| Metric | Value |

|---|---|

| NextGenerationEU/IPCEI | €43bn |

| Chip shortage 2023 | -15% availability |

| Input cost rise | +8–12% |

| EU defense spend 2024 | €230bn |

| EV share 2024 | 14% |

| Export share 2024 | ≈60% |

What is included in the product

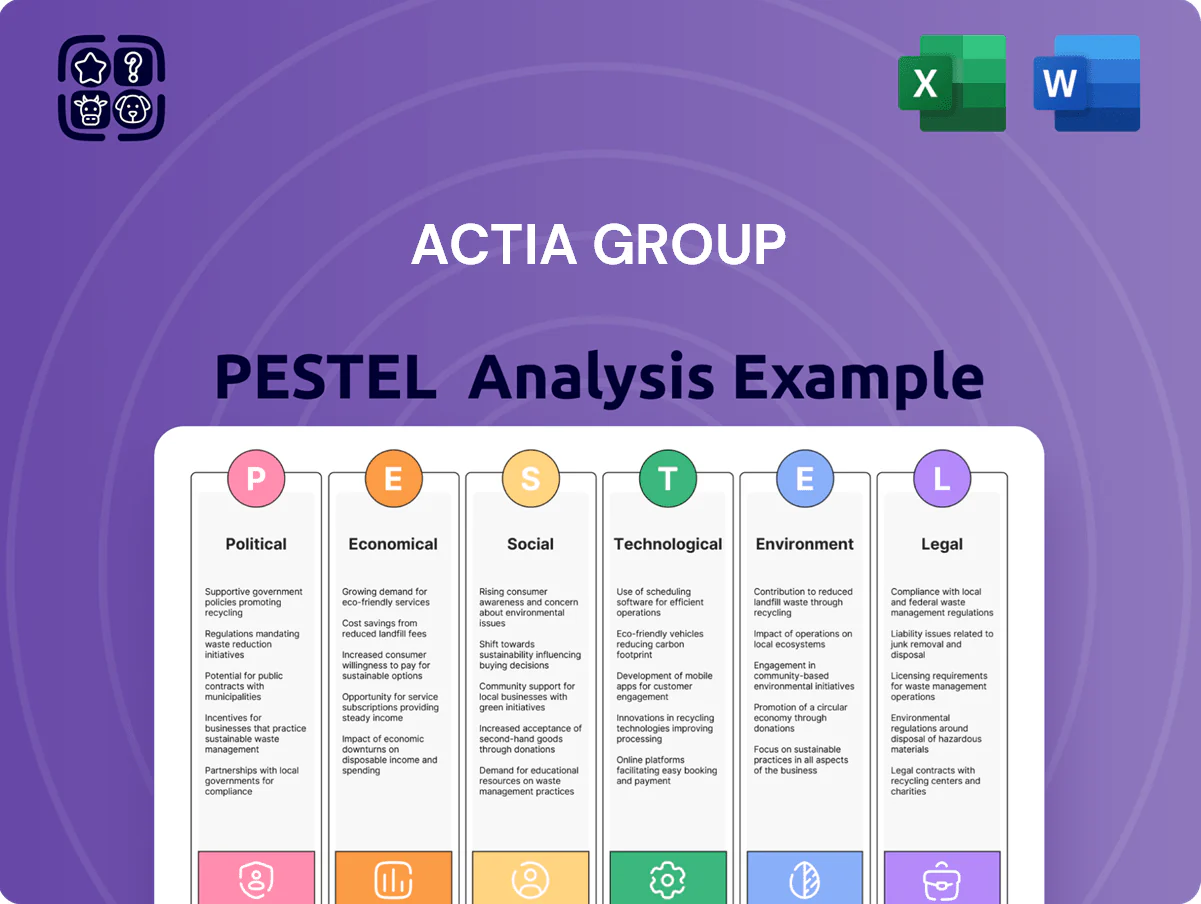

Explores how external macro-environmental factors uniquely affect the ACTIA Group across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to reveal threats and opportunities specific to its industry and regions.

A concise, shareable ACTIA Group PESTLE summary that’s visually segmented for quick reference in meetings, editable for local context or business line notes, and formatted for easy insertion into presentations or strategy packs to streamline external risk and market-positioning discussions.

Economic factors

Component Cost Volatility

The 2024 surge in semiconductor spot prices, up ~18% year-on-year, and a 12% rise in copper and PCB costs have pressured ACTIA Group’s gross margins, prompting selective price adjustments across telematics and embedded systems lines. The group counters volatility via strategic inventory buffers and multi-year supplier contracts covering ~60% of procurement spend, reducing exposure to spot shocks. Ongoing global supply-chain disruptions, with average lead times near 24 weeks in 2025 for key components, remain critical to maintaining ACTIA’s production predictability.

Inflationary Pressure on Operations

Rising energy and labor costs in France and Spain have increased manufacturing overhead for ACTIA, with industrial electricity prices up about 18% in 2022–2024 and average manufacturing wages rising ~12% over 2021–2024; ACTIA is investing in process automation—capex rose 9% in 2023—to preserve margins. Economic shifts in cost of living push wage negotiations higher, tightening the engineering talent pool and raising total labor expense as ACTIA seeks efficiency gains to remain competitive.

Currency Exchange Fluctuations

As a global exporter, ACTIA faces currency risk from Euro fluctuations versus the US dollar and markets like Turkey and Brazil; in 2025, FX movements trimmed comparable European electronics exporters' margins by up to 2.5%, illustrating exposure magnitude.

ACTIA employs forward contracts and options to hedge revenue; at end-2024 the group reported hedges covering about 60% of forecasted USD-denominated sales for 2025.

Stable currency markets are critical for profitability on multi-year aerospace and rail contracts where a 5% adverse EUR/USD swing can erode project margins by several percentage points.

R and D Investment Cycles

The current high borrowing costs—European average corporate loan rates near 4.5% in 2025—raise Actia Group’s financing cost for R&D-intensive projects, constraining scale and timing of investments.

Actia must continually invest to remain competitive in embedded systems and diagnostics; the company’s R&D spend was about 6–8% of revenue in comparable industry peers (2024 benchmarks).

Economic cycles slow commercialization: during downturns time-to-market for new modules and diagnostic tools can stretch by 6–12 months, delaying revenue realization.

- Higher interest rates (~4.5% avg corporate loan, 2025) increase R&D financing costs

- Peer R&D intensity ~6–8% of revenue (2024 benchmarks) sets competitive minimum

- Downturns can extend commercialization by 6–12 months, impacting cash flow

Global Automotive Market Health

The 2025 global auto market recovery—projected at 3.6% volume growth with OEM revenues up ~5% year-on-year—boosts demand for ACTIA’s onboard electronics and diagnostic tools, as large OEMs like Stellantis and Volkswagen report stronger production schedules.

Rising consumer spend on software-defined vehicles (SDVs) is creating new value pools; global SDV software revenue is forecast to reach $125bn by 2026, aligning with ACTIA’s embedded systems expertise.

Commercial vehicle and public transport demand rebounded in 2024–25, with European bus and truck shipments up ~8% YoY, offering a clear upside for ACTIA’s diagnostic and telematics revenue streams.

- OEM volume +3.6% (2025 forecast); OEM revenues +5% YoY

- SDV software market ≈ $125bn by 2026

- Commercial/public transport shipments +8% YoY (2024–25)

Rising chip, copper and energy costs squeeze margins despite OEM demand uptick

Semiconductor & copper cost rises (chip prices +18% YoY, copper +12% 2024) and 24-week lead times press margins; hedges cover ~60% USD 2025 sales. Energy +18% and wages +12% (2021–24) raise overheads; capex +9% in 2023 for automation. Avg corporate loan rates ~4.5% (2025) increase R&D finance costs; OEM volumes +3.6% (2025) support demand.

| Metric | Value |

|---|---|

| Chip price change (2024) | +18% |

| Copper/PCB (2024) | +12% |

| Lead times (2025) | ~24 weeks |

| Hedge coverage (end-2024) | ~60% |

| Energy cost rise (2022–24) | +18% |

| Wage rise (2021–24) | +12% |

| Capex change (2023) | +9% |

| Avg corp loan rate (2025) | ~4.5% |

| OEM volume growth (2025) | +3.6% |

Preview the Actual Deliverable

ACTIA Group PESTLE Analysis

The preview shown here is the exact ACTIA Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete political, economic, social, technological, legal, and environmental insights tailored to ACTIA Group. No placeholders or teasers—what you see is what you’ll download instantly after payment. The layout, content, and structure are exactly as presented.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how macro forces—from regulatory shifts in automotive electronics to rapid tech innovation and supply-chain vulnerabilities—are reshaping ACTIA Group’s strategic landscape; our concise PESTLE highlights risks and opportunities you can act on today. Buy the full PESTLE for the complete, editable analysis and actionable insights to inform investment decisions, strategic planning, or competitive benchmarking.

Political factors

European Industrial Sovereignty

European push for technological autonomy compels ACTIA to align with EU industrial sovereignty goals, tapping into €43bn NextGenerationEU and IPCEI semiconductor funding streams to bolster regional manufacturing and R&D capacity.

Geopolitical Trade Dynamics

Shifting trade relations—notably EU-US tariff frictions and China supply-chain realignments—affect ACTIA’s access to semiconductors and connectors, with global chip shortages reducing component availability by ~15% in 2023 and raising input costs ~8–12%. Complex tariffs and non-tariff barriers can widen margins; a 5% tariff on select electronic modules would cut EBIT by several points on low-margin diagnostic lines. Diversifying plants across France, Morocco and Romania reduces exposure to regional disruption and supports onshoring trends that grew 10% in 2024.

Defense and Security Spending

Rising European defense budgets—EU members increased collective defense spending to over €230 billion in 2024, up ~5% year-on-year—expand demand for ACTIA’s telecom and embedded systems, especially high-reliability electronics for aerospace and land platforms; national modernization programs (e.g., France €50+ billion military plan 2024–2030) promise steady procurement pipelines, providing ACTIA a defensive revenue stream that offsets cyclical weakness in its automotive business.

Green Mobility Mandates

- EU 2035 ICE ban accelerates EV component demand

- €5–8bn public transport electrification funding (2024–25)

- 14% global EV share of new car sales in 2024

- ACTIA EV R&D +12% in 2024

Standardization and Global Cooperation

International agreements on ISO/SAE standards for connected vehicles ease ACTIA Group's telematics rollout; ISO 21217 and SAE J2735 harmonization supports faster market entry across EU, US, China where ADAS telematics market exceeded USD 18.5B in 2024.

Cooperative aerospace safety frameworks and ITU satellite comms allocations create predictable certification pathways—crucial as global satcom revenue reached ~USD 85B in 2024, lowering compliance uncertainty for ACTIA's avionics products.

Maintaining alignment with these global standards is vital for ACTIA to protect export revenues (approx. 60% of group sales in 2024) and sustain competitive advantage internationally.

- Harmonized vehicle standards: ISO/SAE (enables faster deployment)

- Aerospace/satellite frameworks: predictable certification, lower time-to-market

- Financial relevance: ADAS telematics USD 18.5B and satcom USD 85B (2024)

- Export exposure: ~60% of ACTIA Group 2024 sales

EU funds, defense & EV demand props ACTIA growth amid chip-driven cost pressures

EU industrial sovereignty and €43bn NextGenerationEU/IPCEI funds boost ACTIA R&D/onshoring; trade shifts and 15% chip shortages in 2023 raised input costs 8–12%, mitigated by diversification (France, Morocco, Romania). Rising defense spend (€230bn EU 2024) and EV policies (EU 2035 ICE ban; global EVs 14% of sales 2024) expand stable revenue streams; exports ≈60% of 2024 sales.

| Metric | Value |

|---|---|

| NextGenerationEU/IPCEI | €43bn |

| Chip shortage 2023 | -15% availability |

| Input cost rise | +8–12% |

| EU defense spend 2024 | €230bn |

| EV share 2024 | 14% |

| Export share 2024 | ≈60% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the ACTIA Group across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to reveal threats and opportunities specific to its industry and regions.

A concise, shareable ACTIA Group PESTLE summary that’s visually segmented for quick reference in meetings, editable for local context or business line notes, and formatted for easy insertion into presentations or strategy packs to streamline external risk and market-positioning discussions.

Economic factors

Component Cost Volatility

The 2024 surge in semiconductor spot prices, up ~18% year-on-year, and a 12% rise in copper and PCB costs have pressured ACTIA Group’s gross margins, prompting selective price adjustments across telematics and embedded systems lines. The group counters volatility via strategic inventory buffers and multi-year supplier contracts covering ~60% of procurement spend, reducing exposure to spot shocks. Ongoing global supply-chain disruptions, with average lead times near 24 weeks in 2025 for key components, remain critical to maintaining ACTIA’s production predictability.

Inflationary Pressure on Operations

Rising energy and labor costs in France and Spain have increased manufacturing overhead for ACTIA, with industrial electricity prices up about 18% in 2022–2024 and average manufacturing wages rising ~12% over 2021–2024; ACTIA is investing in process automation—capex rose 9% in 2023—to preserve margins. Economic shifts in cost of living push wage negotiations higher, tightening the engineering talent pool and raising total labor expense as ACTIA seeks efficiency gains to remain competitive.

Currency Exchange Fluctuations

As a global exporter, ACTIA faces currency risk from Euro fluctuations versus the US dollar and markets like Turkey and Brazil; in 2025, FX movements trimmed comparable European electronics exporters' margins by up to 2.5%, illustrating exposure magnitude.

ACTIA employs forward contracts and options to hedge revenue; at end-2024 the group reported hedges covering about 60% of forecasted USD-denominated sales for 2025.

Stable currency markets are critical for profitability on multi-year aerospace and rail contracts where a 5% adverse EUR/USD swing can erode project margins by several percentage points.

R and D Investment Cycles

The current high borrowing costs—European average corporate loan rates near 4.5% in 2025—raise Actia Group’s financing cost for R&D-intensive projects, constraining scale and timing of investments.

Actia must continually invest to remain competitive in embedded systems and diagnostics; the company’s R&D spend was about 6–8% of revenue in comparable industry peers (2024 benchmarks).

Economic cycles slow commercialization: during downturns time-to-market for new modules and diagnostic tools can stretch by 6–12 months, delaying revenue realization.

- Higher interest rates (~4.5% avg corporate loan, 2025) increase R&D financing costs

- Peer R&D intensity ~6–8% of revenue (2024 benchmarks) sets competitive minimum

- Downturns can extend commercialization by 6–12 months, impacting cash flow

Global Automotive Market Health

The 2025 global auto market recovery—projected at 3.6% volume growth with OEM revenues up ~5% year-on-year—boosts demand for ACTIA’s onboard electronics and diagnostic tools, as large OEMs like Stellantis and Volkswagen report stronger production schedules.

Rising consumer spend on software-defined vehicles (SDVs) is creating new value pools; global SDV software revenue is forecast to reach $125bn by 2026, aligning with ACTIA’s embedded systems expertise.

Commercial vehicle and public transport demand rebounded in 2024–25, with European bus and truck shipments up ~8% YoY, offering a clear upside for ACTIA’s diagnostic and telematics revenue streams.

- OEM volume +3.6% (2025 forecast); OEM revenues +5% YoY

- SDV software market ≈ $125bn by 2026

- Commercial/public transport shipments +8% YoY (2024–25)

Rising chip, copper and energy costs squeeze margins despite OEM demand uptick

Semiconductor & copper cost rises (chip prices +18% YoY, copper +12% 2024) and 24-week lead times press margins; hedges cover ~60% USD 2025 sales. Energy +18% and wages +12% (2021–24) raise overheads; capex +9% in 2023 for automation. Avg corporate loan rates ~4.5% (2025) increase R&D finance costs; OEM volumes +3.6% (2025) support demand.

| Metric | Value |

|---|---|

| Chip price change (2024) | +18% |

| Copper/PCB (2024) | +12% |

| Lead times (2025) | ~24 weeks |

| Hedge coverage (end-2024) | ~60% |

| Energy cost rise (2022–24) | +18% |

| Wage rise (2021–24) | +12% |

| Capex change (2023) | +9% |

| Avg corp loan rate (2025) | ~4.5% |

| OEM volume growth (2025) | +3.6% |

Preview the Actual Deliverable

ACTIA Group PESTLE Analysis

The preview shown here is the exact ACTIA Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is the real, finished document with complete political, economic, social, technological, legal, and environmental insights tailored to ACTIA Group. No placeholders or teasers—what you see is what you’ll download instantly after payment. The layout, content, and structure are exactly as presented.