Acuity Brands Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

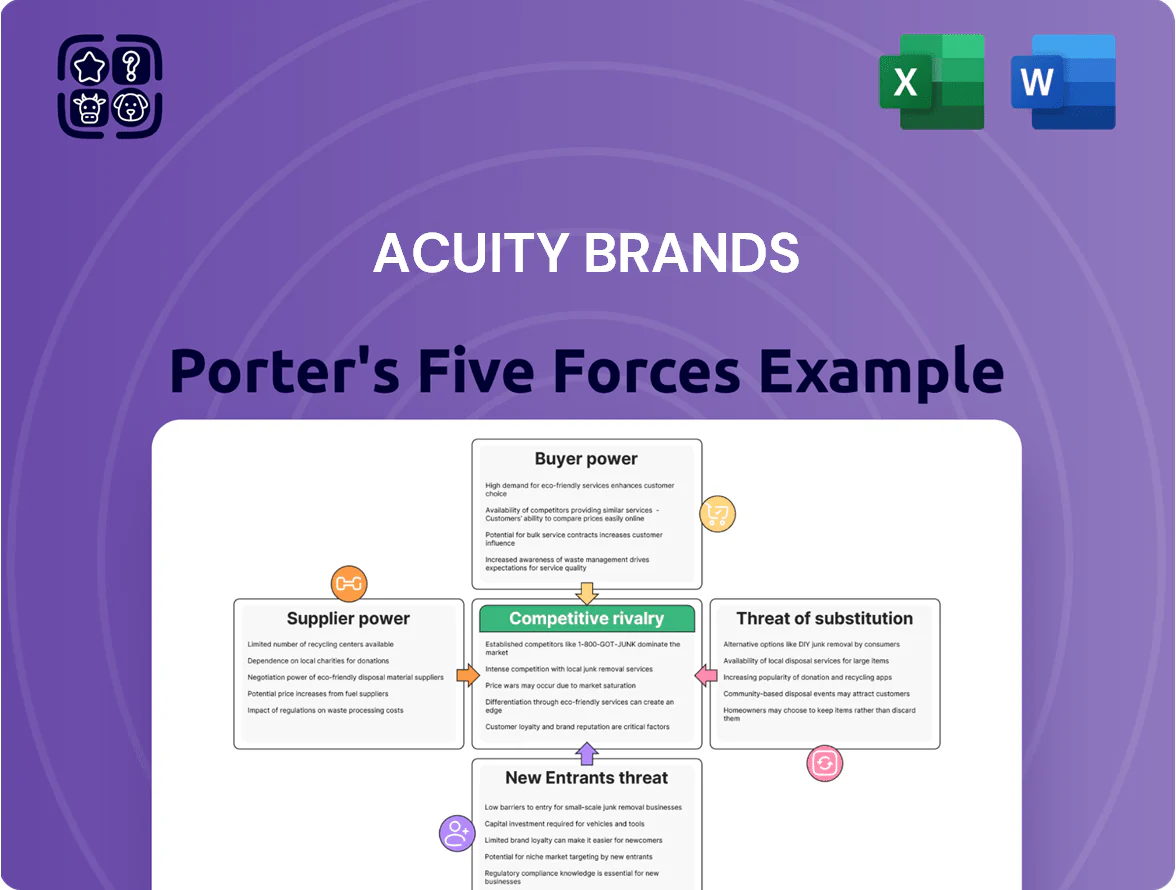

Acuity Brands faces moderate supplier power and rising buyer expectations amid steady demand for energy-efficient lighting; rivalry is intense due to large incumbents and rapid technological change, while barriers to entry are moderate given capital needs but significant regulatory and distribution challenges.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acuity Brands’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on semiconductor and LED chip manufacturers

Acuity Brands depends on a small set of global suppliers for LED chips and drivers; by Q4 2025, the top 5 suppliers controlled an estimated 68% of high-efficiency LED chip capacity, giving suppliers strong pricing and lead-time leverage.

Supplier consolidation raised average chip price volatility to ±12% year-over-year in 2025, so Acuity must keep strategic contracts and joint R&D deals to secure timely delivery and access to next-gen components for intelligent building systems.

Volatility in raw material and commodity pricing

The production of lighting fixtures and building controls requires large amounts of aluminum, steel, and copper; in 2025 aluminum rose ~18% YTD and copper ~12% YTD, forcing Acuity Brands to navigate volatile input costs that squeezed gross margins (Q3 2025 GAAP gross margin fell to ~29.5% vs 31.8% year‑ago).

Switching costs for proprietary technology components

Integrating third-party sensors and comms modules into Acuity Brands Atrius creates technical dependencies that raise switching costs; redesigning hardware and firmware often exceeds $1–3M and takes 6–12 months, per industry reports.

Switching suppliers risks product-certification delays (UL/ETL, FCC) and software incompatibility, which can cut time-to-market and revenue by 20–35% in smart-building rollouts.

This technical lock-in boosts bargaining power of specialized tech partners—vendors supplying 5G, Zigbee, or Matter-capable modules can command price premiums and priority support, impacting Acuity’s margins and procurement leverage.

Impact of global logistics and supply chain stability

Reliance on international shipping and specialized logistics keeps supplier leverage high for Acuity Brands; 2023-24 container rates and port congestion raised component costs by ~8-12% for electronics OEMs, pushing Acuity to favor suppliers with diversified plants to cut 21% longer average lead-times risk.

Suppliers with multi-country footprints now charge premiums—often 3-7%—for guaranteed lead times and resilient routes; this squeezes margins unless Acuity secures long-term contracts or shifts sourcing to nearer-shore partners.

- International shipping drives supplier power

- Diversified manufacturers demand 3-7% premium

- Lead-time risk reduced by multi-site suppliers

- Long-term contracts mitigate margin pressure

Supplier concentration in the driver and optics segment

- Few suppliers: high concentration

- FY2024 supply-cost rise ~6%

- Multi-year contracts common

- Disruption → immediate production risk

Supplier power squeezes Acuity: concentrated LED capacity, rising chip & metal costs

Acuity faces high supplier power: top-5 LED-chip suppliers held ~68% capacity by Q4 2025, chip price volatility ±12% YoY, FY2024 supply costs +6%, aluminum +18% and copper +12% YTD 2025, and driver/optics vendors command premiums; long-term contracts and multi-site suppliers reduce but don’t eliminate lead-time and margin risk.

| Metric | Value |

|---|---|

| Top-5 LED capacity (Q4 2025) | 68% |

| Chip price volatility (2025) | ±12% YoY |

| FY2024 supply-cost rise | ~6% |

| Aluminum YTD 2025 | +18% |

| Copper YTD 2025 | +12% |

What is included in the product

Tailored Porter's Five Forces analysis for Acuity Brands that uncovers competitive pressures, supplier and buyer leverage, substitution risks, and entry barriers, with strategic insights on emerging threats and opportunities.

A concise Acuity Brands Porter’s Five Forces snapshot—instantly highlights supplier, buyer, substitute, entrant, and rivalry pressures to speed strategic decisions and investor briefs.

Customers Bargaining Power

Concentration of sales through large electrical distributors

Influence of specifiers and lighting designers

Architects, lighting designers, and engineers specify fixtures for large commercial projects and indirectly control brand choice; their specs influenced roughly 60% of US commercial lighting purchases in 2024, shaping Acuity Brands’ share of that ~$12.5B market.

Because specifiers aren’t payers, Acuity must spend on education, BIM/Revit libraries, and digital lighting design tools—Acuity disclosed R&D and sales support at ~6.1% of 2024 revenue ($119M) to keep preference among these influencers.

Low switching costs for standardized LED products

In commodity-grade LED fixtures, switching costs are low, so buyers often choose by price; US residential and contractor segments saw LED unit price declines ~18% from 2020–2024, increasing price sensitivity.

Because many basic fixtures meet similar efficacy standards (e.g., ENERGY STAR), Acuity Brands (NYSE: AYI) faces limited pricing power; a 5% price rise risks volume loss to lower-cost US imports or Southeast Asian suppliers.

Rising demand for integrated smart building platforms

Sophisticated enterprise customers now seek integrated smart building platforms over standalone fixtures, pushing Acuity Brands to bundle lighting, controls, and analytics into software-centric offers.

These high-value clients can demand customized software integrations and multi-year service level agreements (SLAs), often tying up 60–80% of project value in recurring services; in 2024 Acuity reported software and service revenue growth of ~18% year-over-year.

As Acuity shifts toward subscription and platform models, large corporate and institutional customers gain leverage through multi-year contracts that increase switching costs and demand supplier co-investment in integrations.

Price transparency in the digital marketplace

Online procurement platforms and digital catalogs have pushed price transparency; 2024 B2B e-procurement adoption hit ~62% globally, letting specifiers compare Acuity Brands' fixtures and prices in real time.

Buyers cross-check lumen output, color rendering (CRI), and lifecycle costs across makers, pressuring Acuity to validate ~10–15% premium via tech, brand, or energy savings; reported LED system energy reductions of 30–50% are key.

- 62% B2B e-procurement adoption (2024)

- Buyers compare specs/prices live

- Acuity must justify 10–15% premium

- Energy savings cited 30–50% in LED systems

Distributors & Specifiers Drive Pricing Power as Platforms Capture High-Value Growth

Large distributors (Graybar, Wesco) and specifiers (architects/engineers) exert strong bargaining power—distributors drove ~25–30% of AYI 2024 revenue and Graybar reported $7.8B electrical sales; specifiers influenced ~60% of US commercial lighting (~$12.5B market). Price transparency (62% B2B e‑procurement, 2024) and 18% software/service growth (AYI 2024) split power between low‑price buyers and high‑value platform customers.

| Metric | 2024 |

|---|---|

| Distributor revenue share | 25–30% |

| Graybar electrical sales | $7.8B |

| Specifier influence | ~60% |

| B2B e‑procurement | 62% |

| AYI software/service growth | ~18% |

Preview Before You Purchase

Acuity Brands Porter's Five Forces Analysis

This preview shows the exact Acuity Brands Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the full, professionally formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Acuity Brands faces moderate supplier power and rising buyer expectations amid steady demand for energy-efficient lighting; rivalry is intense due to large incumbents and rapid technological change, while barriers to entry are moderate given capital needs but significant regulatory and distribution challenges.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acuity Brands’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on semiconductor and LED chip manufacturers

Acuity Brands depends on a small set of global suppliers for LED chips and drivers; by Q4 2025, the top 5 suppliers controlled an estimated 68% of high-efficiency LED chip capacity, giving suppliers strong pricing and lead-time leverage.

Supplier consolidation raised average chip price volatility to ±12% year-over-year in 2025, so Acuity must keep strategic contracts and joint R&D deals to secure timely delivery and access to next-gen components for intelligent building systems.

Volatility in raw material and commodity pricing

The production of lighting fixtures and building controls requires large amounts of aluminum, steel, and copper; in 2025 aluminum rose ~18% YTD and copper ~12% YTD, forcing Acuity Brands to navigate volatile input costs that squeezed gross margins (Q3 2025 GAAP gross margin fell to ~29.5% vs 31.8% year‑ago).

Switching costs for proprietary technology components

Integrating third-party sensors and comms modules into Acuity Brands Atrius creates technical dependencies that raise switching costs; redesigning hardware and firmware often exceeds $1–3M and takes 6–12 months, per industry reports.

Switching suppliers risks product-certification delays (UL/ETL, FCC) and software incompatibility, which can cut time-to-market and revenue by 20–35% in smart-building rollouts.

This technical lock-in boosts bargaining power of specialized tech partners—vendors supplying 5G, Zigbee, or Matter-capable modules can command price premiums and priority support, impacting Acuity’s margins and procurement leverage.

Impact of global logistics and supply chain stability

Reliance on international shipping and specialized logistics keeps supplier leverage high for Acuity Brands; 2023-24 container rates and port congestion raised component costs by ~8-12% for electronics OEMs, pushing Acuity to favor suppliers with diversified plants to cut 21% longer average lead-times risk.

Suppliers with multi-country footprints now charge premiums—often 3-7%—for guaranteed lead times and resilient routes; this squeezes margins unless Acuity secures long-term contracts or shifts sourcing to nearer-shore partners.

- International shipping drives supplier power

- Diversified manufacturers demand 3-7% premium

- Lead-time risk reduced by multi-site suppliers

- Long-term contracts mitigate margin pressure

Supplier concentration in the driver and optics segment

- Few suppliers: high concentration

- FY2024 supply-cost rise ~6%

- Multi-year contracts common

- Disruption → immediate production risk

Supplier power squeezes Acuity: concentrated LED capacity, rising chip & metal costs

Acuity faces high supplier power: top-5 LED-chip suppliers held ~68% capacity by Q4 2025, chip price volatility ±12% YoY, FY2024 supply costs +6%, aluminum +18% and copper +12% YTD 2025, and driver/optics vendors command premiums; long-term contracts and multi-site suppliers reduce but don’t eliminate lead-time and margin risk.

| Metric | Value |

|---|---|

| Top-5 LED capacity (Q4 2025) | 68% |

| Chip price volatility (2025) | ±12% YoY |

| FY2024 supply-cost rise | ~6% |

| Aluminum YTD 2025 | +18% |

| Copper YTD 2025 | +12% |

What is included in the product

Tailored Porter's Five Forces analysis for Acuity Brands that uncovers competitive pressures, supplier and buyer leverage, substitution risks, and entry barriers, with strategic insights on emerging threats and opportunities.

A concise Acuity Brands Porter’s Five Forces snapshot—instantly highlights supplier, buyer, substitute, entrant, and rivalry pressures to speed strategic decisions and investor briefs.

Customers Bargaining Power

Concentration of sales through large electrical distributors

Influence of specifiers and lighting designers

Architects, lighting designers, and engineers specify fixtures for large commercial projects and indirectly control brand choice; their specs influenced roughly 60% of US commercial lighting purchases in 2024, shaping Acuity Brands’ share of that ~$12.5B market.

Because specifiers aren’t payers, Acuity must spend on education, BIM/Revit libraries, and digital lighting design tools—Acuity disclosed R&D and sales support at ~6.1% of 2024 revenue ($119M) to keep preference among these influencers.

Low switching costs for standardized LED products

In commodity-grade LED fixtures, switching costs are low, so buyers often choose by price; US residential and contractor segments saw LED unit price declines ~18% from 2020–2024, increasing price sensitivity.

Because many basic fixtures meet similar efficacy standards (e.g., ENERGY STAR), Acuity Brands (NYSE: AYI) faces limited pricing power; a 5% price rise risks volume loss to lower-cost US imports or Southeast Asian suppliers.

Rising demand for integrated smart building platforms

Sophisticated enterprise customers now seek integrated smart building platforms over standalone fixtures, pushing Acuity Brands to bundle lighting, controls, and analytics into software-centric offers.

These high-value clients can demand customized software integrations and multi-year service level agreements (SLAs), often tying up 60–80% of project value in recurring services; in 2024 Acuity reported software and service revenue growth of ~18% year-over-year.

As Acuity shifts toward subscription and platform models, large corporate and institutional customers gain leverage through multi-year contracts that increase switching costs and demand supplier co-investment in integrations.

Price transparency in the digital marketplace

Online procurement platforms and digital catalogs have pushed price transparency; 2024 B2B e-procurement adoption hit ~62% globally, letting specifiers compare Acuity Brands' fixtures and prices in real time.

Buyers cross-check lumen output, color rendering (CRI), and lifecycle costs across makers, pressuring Acuity to validate ~10–15% premium via tech, brand, or energy savings; reported LED system energy reductions of 30–50% are key.

- 62% B2B e-procurement adoption (2024)

- Buyers compare specs/prices live

- Acuity must justify 10–15% premium

- Energy savings cited 30–50% in LED systems

Distributors & Specifiers Drive Pricing Power as Platforms Capture High-Value Growth

Large distributors (Graybar, Wesco) and specifiers (architects/engineers) exert strong bargaining power—distributors drove ~25–30% of AYI 2024 revenue and Graybar reported $7.8B electrical sales; specifiers influenced ~60% of US commercial lighting (~$12.5B market). Price transparency (62% B2B e‑procurement, 2024) and 18% software/service growth (AYI 2024) split power between low‑price buyers and high‑value platform customers.

| Metric | 2024 |

|---|---|

| Distributor revenue share | 25–30% |

| Graybar electrical sales | $7.8B |

| Specifier influence | ~60% |

| B2B e‑procurement | 62% |

| AYI software/service growth | ~18% |

Preview Before You Purchase

Acuity Brands Porter's Five Forces Analysis

This preview shows the exact Acuity Brands Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the full, professionally formatted document is ready for download and use the moment you buy.