ACV Auctions Porter's Five Forces Analysis

Don't Miss the Bigger Picture

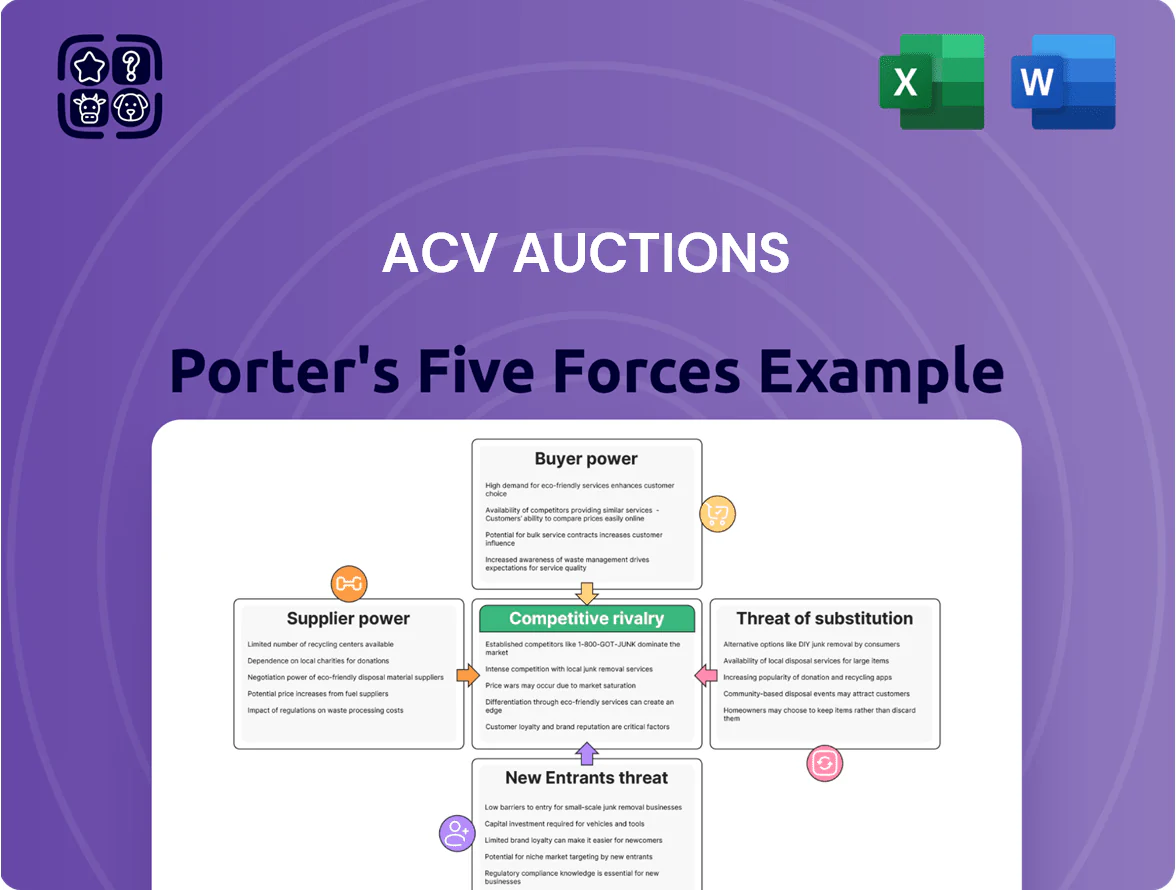

ACV Auctions faces intense buyer and competitor pressures amid rapid digitalization and moderate supplier leverage, with new entrants and substitutes posing evolving threats that shape pricing and margins; strategic differentiation and scale are key to sustaining growth. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore ACV Auctions’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of the Dealer Base

The primary suppliers for ACV Auctions are thousands of franchise and independent dealers selling trade-in inventory; no single dealer group controls enough volume to set fees. This fragmentation cuts suppliers’ bargaining power since dealers depend on ACV’s national buyer network—ACV reported ~7,000 active dealer sellers in 2025. By end-2025 ACV integrated with 12 major dealer management systems to streamline listings and reduce frictions.

Dependence on Digital Liquidity

Dealers need fast inventory turnover to protect cash flow and cut depreciation; ACV Auctions reports median sell times under 20 minutes on platform lots vs days at physical auctions, boosting digital liquidity. That speed gives ACV stronger supplier power because dealers rely on it to clear inventory quickly—J.D. Power noted 2024 wholesale digital penetration at ~28%, and churn falls when time-to-sale is shortest.

Value of Proprietary Inspection Data

ACV uses trained inspectors and proprietary tech like Virtual Lift to produce detailed condition reports, increasing buyer trust and typically raising sale prices—ACV reported a 7–10% higher realized price for inspected vehicles in 2024 versus non-inspected peers.

Because ACV owns the inspection process and data, suppliers must accept ACV’s standards and report accuracy, limiting their ability to shape vehicle narratives and increasing supplier dependence on ACV’s platform and outcomes.

Switching Costs and Platform Integration

ACV’s deep software integration creates practical switching costs: dealers can list elsewhere but retraining staff and rebuilding workflows is costly, and by late 2025 ACV bundled transport and financing tools cover ~35% of dealer wholesale needs, reducing incentive to leave.

Leaving risks loss of historical pricing and performance analytics—ACV reported cumulative auction data on ~1.2M vehicles by 2025—so small fee cuts by rivals rarely flip loyalty.

- Integration raises retraining costs

- Platform covers transport+finance (one-stop)

- ~1.2M vehicles in ACV data by 2025

- ~35% dealer wholesale coverage reduces churn

Alternative Wholesale Channels

Suppliers still can use physical auctions or dealer-to-dealer trades—legacy players Manheim (IAA merged volumes: ~2.3M units in 2024 industry-wide) and ADESA run large lanes favored for bulk liquidations.

But digitization cuts appeal: ACV Auctions reported 2024 seller take rates improving and online lane fill rates rising, while transport costs rose ~8% YOY and offline turn times average 3–5 days longer, reducing legacy leverage.

Overall, rising online adoption and faster sell-through are eroding traditional auction houses’ bargaining power versus digital marketplaces.

- Manheim/ADESA still handle bulk lanes (~millions units/year)

- Transport costs +8% YOY (2024)

- Offline turn times 3–5 days longer

- ACV online fill/turn improvements in 2024

ACV's scale & fast sales shrink dealer leverage despite fragmented 7K seller market

Suppliers (franchise/independent dealers) have low bargaining power due to fragmentation (~7,000 active dealer sellers in 2025), ACV’s fast median sell times (<20 minutes) and proprietary inspections raising prices 7–10% (2024), plus integrated DMS, transport and finance (~35% dealer coverage) and ~1.2M-vehicle historical dataset by 2025, making switching costly despite legacy bulk lanes (Manheim/ADESA ~2.3M units 2024).

| Metric | Value |

|---|---|

| Active dealer sellers (2025) | ~7,000 |

| Median sell time | <20 minutes |

| Inspected price lift (2024) | 7–10% |

| Dealer wholesale coverage | ~35% |

| ACV dataset (cumulative, 2025) | ~1.2M vehicles |

| Legacy bulk lanes (IAA/Manheim, 2024) | ~2.3M units |

What is included in the product

Tailored Porter's Five Forces analysis for ACV Auctions highlighting competitive intensity, buyer/supplier power, substitute threats, and entry barriers, with strategic insights on disruptive risks and pricing pressures.

A concise Porter's Five Forces one-sheet for ACV Auctions that highlights competitive pressures and relieves strategic uncertainty—ready to drop into investor decks or boardroom briefs.

Customers Bargaining Power

Access to Multiple Sourcing Platforms

Buying dealers can use multiple digital platforms—Openlane, BacklotCars, Manheim Express and ACV—so they can compare millions of VINs and prices; industry reports show 60–70% of dealers use two or more channels, giving customers moderate bargaining power.

That choice lets buyers shift volume to the best-priced platform, so ACV must keep innovating its UI and bidding tools; platform engagement KPIs (session length, bid rate) fell 8% industrywide in 2024 when features lagged.

By 2025 buyer loyalty hinges more on data accuracy than exclusive inventory: ADAS/condition report accuracy and mileage verification reduces dispute rates; platforms reporting >95% data accuracy retain ~20% higher repeat purchase rates.

Sensitivity to Transaction and Transport Fees

Wholesale buyers operate on thin margins and are very sensitive to total acquisition cost, including ACV Auctions’ buyer fees and transport; a 2024 JD Power report showed wholesale dealers cite fees as a top-3 switching reason for 46% of transactions. If ACV raises fees materially, high-volume buyers can move volume to rivals or local auctions to save 2–4% in overhead. ACV balances take-rate with vehicle value and runs tiered fees and loyalty discounts to limit churn—tiering cut churn by an estimated 15% in 2023.

Reliance on Condition Report Accuracy

The cornerstone of buyer trust in ACV Auctions is the accuracy of its condition reports; in 2024 ACV reported over 4.6 million vehicle inspections, and any drop in report quality raises real risk of undisclosed mechanical defects.

That risk gives buyers leverage: they demand strong accountability and arbitration—ACV logged a 0.8% dispute rate in 2024—so buyers pressure for protections and refunds.

Because ACV demonstrably reduces inspection risk, buyers accept its pricing premium vs. cheaper, opaque alternatives, supporting ACV’s pricing power and lower churn.

Inventory Scarcity and Market Competition

When high-quality used inventory is scarce, power shifts to ACV Auctions as the aggregator of desirable cars; buyers then bid aggressively, pushing wholesale prices up and enlarging marketplace take-rates.

By 2025 demand for data-backed wholesale units stayed strong—wholesale used-vehicle prices rose ~12% YoY in 2024—so individual buyers had limited room to negotiate fees.

The competitive bidding format reduces collective buyer leverage: multiple bidders per lot (often 5–10) and transparent bidding history favor platform pricing power.

- Inventory scarcity → platform leverage

- Competitive bids raise prices (~12% YoY 2024)

- Data-backed units keep fee pressure low

- 5–10 bidders typical per lot, lowering buyer bargaining power

Technological Empowerment and Data Usage

Advanced buyers use ACV Auctions’ data-driven insights and market-pricing tools to avoid overpaying, increasing customer bargaining power through transparency; in 2024 ACV reported 25% year-over-year growth in analytics-enabled listings, showing rising uptake.

By 2025 sophisticated buyers deploy AI-integrated bidding (automated bids tied to margin targets), forcing ACV to deliver more complex tooling and API access to retain high-value customers.

- 25% YoY growth in analytics-enabled listings (2024)

- AI-bidding automates margin targets by 2025

- Transparency reduces price dispersion, raising buyer leverage

- ACV must expand APIs and advanced analytics

Strong data + competitive bids bolster ACV take-rates despite buyer fee sensitivity

Buyers have moderate bargaining power: multi-platform use (60–70% use ≥2 channels) and fee sensitivity (46% cite fees as top-3 switch reason) limit ACV’s pricing power, but >95% data accuracy and competitive bidding (5–10 bidders; wholesale prices +12% YoY 2024) sustain premium take-rates and lower churn.

| Metric | 2024/2025 |

|---|---|

| Multi-channel dealers | 60–70% |

| Dispute rate | 0.8% |

| Bidder count | 5–10 |

| Wholesale price change | +12% YoY |

Preview Before You Purchase

ACV Auctions Porter's Five Forces Analysis

This preview shows the exact ACV Auctions Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted deliverable, ready for download and use the moment you buy.

No samples or edits needed: what you see here is the same final file you'll get instantly upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

ACV Auctions faces intense buyer and competitor pressures amid rapid digitalization and moderate supplier leverage, with new entrants and substitutes posing evolving threats that shape pricing and margins; strategic differentiation and scale are key to sustaining growth. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore ACV Auctions’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmentation of the Dealer Base

The primary suppliers for ACV Auctions are thousands of franchise and independent dealers selling trade-in inventory; no single dealer group controls enough volume to set fees. This fragmentation cuts suppliers’ bargaining power since dealers depend on ACV’s national buyer network—ACV reported ~7,000 active dealer sellers in 2025. By end-2025 ACV integrated with 12 major dealer management systems to streamline listings and reduce frictions.

Dependence on Digital Liquidity

Dealers need fast inventory turnover to protect cash flow and cut depreciation; ACV Auctions reports median sell times under 20 minutes on platform lots vs days at physical auctions, boosting digital liquidity. That speed gives ACV stronger supplier power because dealers rely on it to clear inventory quickly—J.D. Power noted 2024 wholesale digital penetration at ~28%, and churn falls when time-to-sale is shortest.

Value of Proprietary Inspection Data

ACV uses trained inspectors and proprietary tech like Virtual Lift to produce detailed condition reports, increasing buyer trust and typically raising sale prices—ACV reported a 7–10% higher realized price for inspected vehicles in 2024 versus non-inspected peers.

Because ACV owns the inspection process and data, suppliers must accept ACV’s standards and report accuracy, limiting their ability to shape vehicle narratives and increasing supplier dependence on ACV’s platform and outcomes.

Switching Costs and Platform Integration

ACV’s deep software integration creates practical switching costs: dealers can list elsewhere but retraining staff and rebuilding workflows is costly, and by late 2025 ACV bundled transport and financing tools cover ~35% of dealer wholesale needs, reducing incentive to leave.

Leaving risks loss of historical pricing and performance analytics—ACV reported cumulative auction data on ~1.2M vehicles by 2025—so small fee cuts by rivals rarely flip loyalty.

- Integration raises retraining costs

- Platform covers transport+finance (one-stop)

- ~1.2M vehicles in ACV data by 2025

- ~35% dealer wholesale coverage reduces churn

Alternative Wholesale Channels

Suppliers still can use physical auctions or dealer-to-dealer trades—legacy players Manheim (IAA merged volumes: ~2.3M units in 2024 industry-wide) and ADESA run large lanes favored for bulk liquidations.

But digitization cuts appeal: ACV Auctions reported 2024 seller take rates improving and online lane fill rates rising, while transport costs rose ~8% YOY and offline turn times average 3–5 days longer, reducing legacy leverage.

Overall, rising online adoption and faster sell-through are eroding traditional auction houses’ bargaining power versus digital marketplaces.

- Manheim/ADESA still handle bulk lanes (~millions units/year)

- Transport costs +8% YOY (2024)

- Offline turn times 3–5 days longer

- ACV online fill/turn improvements in 2024

ACV's scale & fast sales shrink dealer leverage despite fragmented 7K seller market

Suppliers (franchise/independent dealers) have low bargaining power due to fragmentation (~7,000 active dealer sellers in 2025), ACV’s fast median sell times (<20 minutes) and proprietary inspections raising prices 7–10% (2024), plus integrated DMS, transport and finance (~35% dealer coverage) and ~1.2M-vehicle historical dataset by 2025, making switching costly despite legacy bulk lanes (Manheim/ADESA ~2.3M units 2024).

| Metric | Value |

|---|---|

| Active dealer sellers (2025) | ~7,000 |

| Median sell time | <20 minutes |

| Inspected price lift (2024) | 7–10% |

| Dealer wholesale coverage | ~35% |

| ACV dataset (cumulative, 2025) | ~1.2M vehicles |

| Legacy bulk lanes (IAA/Manheim, 2024) | ~2.3M units |

What is included in the product

Tailored Porter's Five Forces analysis for ACV Auctions highlighting competitive intensity, buyer/supplier power, substitute threats, and entry barriers, with strategic insights on disruptive risks and pricing pressures.

A concise Porter's Five Forces one-sheet for ACV Auctions that highlights competitive pressures and relieves strategic uncertainty—ready to drop into investor decks or boardroom briefs.

Customers Bargaining Power

Access to Multiple Sourcing Platforms

Buying dealers can use multiple digital platforms—Openlane, BacklotCars, Manheim Express and ACV—so they can compare millions of VINs and prices; industry reports show 60–70% of dealers use two or more channels, giving customers moderate bargaining power.

That choice lets buyers shift volume to the best-priced platform, so ACV must keep innovating its UI and bidding tools; platform engagement KPIs (session length, bid rate) fell 8% industrywide in 2024 when features lagged.

By 2025 buyer loyalty hinges more on data accuracy than exclusive inventory: ADAS/condition report accuracy and mileage verification reduces dispute rates; platforms reporting >95% data accuracy retain ~20% higher repeat purchase rates.

Sensitivity to Transaction and Transport Fees

Wholesale buyers operate on thin margins and are very sensitive to total acquisition cost, including ACV Auctions’ buyer fees and transport; a 2024 JD Power report showed wholesale dealers cite fees as a top-3 switching reason for 46% of transactions. If ACV raises fees materially, high-volume buyers can move volume to rivals or local auctions to save 2–4% in overhead. ACV balances take-rate with vehicle value and runs tiered fees and loyalty discounts to limit churn—tiering cut churn by an estimated 15% in 2023.

Reliance on Condition Report Accuracy

The cornerstone of buyer trust in ACV Auctions is the accuracy of its condition reports; in 2024 ACV reported over 4.6 million vehicle inspections, and any drop in report quality raises real risk of undisclosed mechanical defects.

That risk gives buyers leverage: they demand strong accountability and arbitration—ACV logged a 0.8% dispute rate in 2024—so buyers pressure for protections and refunds.

Because ACV demonstrably reduces inspection risk, buyers accept its pricing premium vs. cheaper, opaque alternatives, supporting ACV’s pricing power and lower churn.

Inventory Scarcity and Market Competition

When high-quality used inventory is scarce, power shifts to ACV Auctions as the aggregator of desirable cars; buyers then bid aggressively, pushing wholesale prices up and enlarging marketplace take-rates.

By 2025 demand for data-backed wholesale units stayed strong—wholesale used-vehicle prices rose ~12% YoY in 2024—so individual buyers had limited room to negotiate fees.

The competitive bidding format reduces collective buyer leverage: multiple bidders per lot (often 5–10) and transparent bidding history favor platform pricing power.

- Inventory scarcity → platform leverage

- Competitive bids raise prices (~12% YoY 2024)

- Data-backed units keep fee pressure low

- 5–10 bidders typical per lot, lowering buyer bargaining power

Technological Empowerment and Data Usage

Advanced buyers use ACV Auctions’ data-driven insights and market-pricing tools to avoid overpaying, increasing customer bargaining power through transparency; in 2024 ACV reported 25% year-over-year growth in analytics-enabled listings, showing rising uptake.

By 2025 sophisticated buyers deploy AI-integrated bidding (automated bids tied to margin targets), forcing ACV to deliver more complex tooling and API access to retain high-value customers.

- 25% YoY growth in analytics-enabled listings (2024)

- AI-bidding automates margin targets by 2025

- Transparency reduces price dispersion, raising buyer leverage

- ACV must expand APIs and advanced analytics

Strong data + competitive bids bolster ACV take-rates despite buyer fee sensitivity

Buyers have moderate bargaining power: multi-platform use (60–70% use ≥2 channels) and fee sensitivity (46% cite fees as top-3 switch reason) limit ACV’s pricing power, but >95% data accuracy and competitive bidding (5–10 bidders; wholesale prices +12% YoY 2024) sustain premium take-rates and lower churn.

| Metric | 2024/2025 |

|---|---|

| Multi-channel dealers | 60–70% |

| Dispute rate | 0.8% |

| Bidder count | 5–10 |

| Wholesale price change | +12% YoY |

Preview Before You Purchase

ACV Auctions Porter's Five Forces Analysis

This preview shows the exact ACV Auctions Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted deliverable, ready for download and use the moment you buy.

No samples or edits needed: what you see here is the same final file you'll get instantly upon payment.