Abu Dhabi Commercial Bank Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

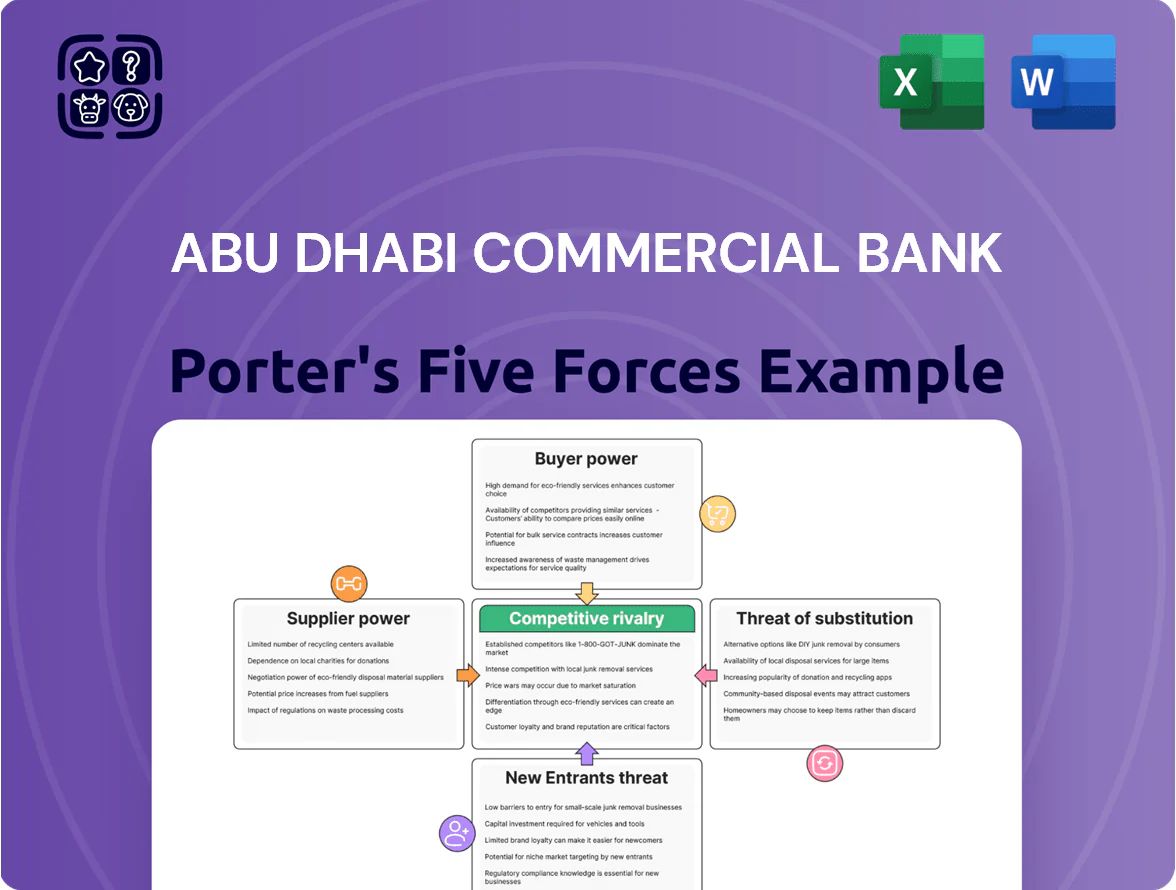

Abu Dhabi Commercial Bank (ADCB) faces moderate buyer power and intense rivalry from UAE legacy banks and rising fintech challengers, while regulatory oversight and capital requirements constrain new entrants; supplier power remains limited but technology partners are increasingly influential.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Abu Dhabi Commercial Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Low-Cost Deposits

Individual and corporate depositors supply most capital to Abu Dhabi Commercial Bank (ADCB); UAE interest rates and the central bank base rate drive their switching behavior, with the UAE base rate at 4.75% in Dec 2025.

By end-2025 ADCB kept a high CASA ratio of about 52%, lowering funding costs and weakening supplier power.

Still, large institutional depositors holding roughly 18% of deposits can push up yields or shift liquidity to rivals, raising short-term funding pressure.

Dependence on Global Technology Providers

ADCB depends on third-party vendors for cloud, cybersecurity and core banking systems, driving high supplier power as switching costs exceed $100m in legacy migration estimates and multi-month outages risk customer churn.

Cutting-edge AI needs push ADCB toward partners like Microsoft and Oracle; their platform lock-in and control of AI toolchains amplify leverage—global cloud market share: AWS 33%, Microsoft Azure 23% (2024).

Access to International Wholesale Funding

ADCB regularly taps international debt markets—issuing sukuk and bonds worth about $3–5bn annually (2023–2024)—to diversify funding and manage liquidity.

Global credit agencies and international investors supply this capital; their power tracks ADCB’s standalone ratings (A-/A3 range in 2024) and the UAE sovereign AA/AA2 ratings.

Shifts in global sentiment or a one-notch ESG downgrade could raise funding spreads by 25–75bp, lifting cost of funds and squeezing net interest margins.

Competition for Specialized Human Capital

The GCC has a constrained pool of fintech, risk and Sharia finance experts; industry surveys in 2024 showed UAE fintech talent shortage at ~35% and regional risk‑specialist vacancy growth of 22% year-over-year.

As ADCB targets full digital transformation by 2026, demand for these specialists raises their bargaining power, forcing higher pay and quicker hiring cycles.

ADCB must match market leads: premium pay, equity/bonus, training, and flexible work to secure talent and avoid project delays.

- 2024 UAE fintech talent gap ~35%

- Regional risk-specialist vacancies +22% YoY (2024)

- Target: digital transformation complete by 2026

- Retention tools: pay premium, equity, training, flexibility

Regulatory Influence of the UAE Central Bank

The Central Bank of the UAE is a de facto supplier of ADCB’s operating license and regulatory framework, controlling reserve requirements and the interest rate corridor that shape ADCB’s loanable funds and net interest margin; as of Dec 2025 reserve requirement stood at 14% for dirham liabilities, directly constraining liquidity.

Compliance is mandatory, so the regulator holds absolute sway over capital ratios, lending caps and product approvals—ADCB must adjust strategy when rules change, raising compliance costs and operational rigidity.

- Central Bank sets reserve req: 14% (Dec 2025)

- Interest rate corridor narrows NIM variability

- Regulatory changes raise compliance costs

- Licensing control limits market entry/expansion

Suppliers wield power: CASA cuts costs, big depositors, cloud dominance & fintech gaps

Suppliers have moderate-to-high power: retail deposits and 52% CASA cut funding costs, but 18% large depositors can pressure yields; cloud/AI vendors (AWS/Azure share 33%/23% in 2024) and scarce fintech talent (~35% gap 2024) raise switching costs; CBUAE control (reserve req 14% Dec 2025) is binding.

| Item | Value |

|---|---|

| CASA | 52% |

| Large depositors | ~18% |

| Reserve req | 14% (Dec 2025) |

| Cloud market | AWS 33% / Azure 23% (2024) |

| Fintech gap | ~35% (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Abu Dhabi Commercial Bank, identifying disruptive threats, supplier/buyer power, substitute products, and barriers that shape its profitability.

A concise, one-sheet Porter's Five Forces for Abu Dhabi Commercial Bank—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

High Sensitivity to Interest Rates and Fees

Retail and corporate customers in the UAE have grown highly price-sensitive as digital comparison platforms cut search costs; by Q4 2025 online rate aggregation showed 92% of mortgage offers and 87% of personal loan products publicly comparable. This transparency—mortgage spreads narrowing to a 0.35% median and average credit-card fee disclosure up 40% year-over-year—gives customers leverage to demand lower rates and fees. ADCB must tighten pricing: a 25–60 bps reduction on select loan products may be needed to retain share against aggressive lenders. If ADCB delays repricing, churn could rise beyond 6% annually.

Low Switching Costs in the Digital Era

Open banking rollouts in the UAE since 2023 cut switching friction: API-based account portability lets customers move deposits and payments in days, raising customer bargaining power against ADCB. A 2024 UAE survey found 42% of retail customers would consider switching within 12 months if onboarding is simple, so ADCB must invest in UX and targeted loyalty to retain deposits and fee income. Aim: reduce churn under 10% annually by 2026 via emotional and functional lock-in.

Sophisticated Demands of Corporate Clients

Growth of Digital-Only Banking Alternatives

The rise of neobanks and digital-first subsidiaries has expanded choices; globally neobanks grew customers ~20% in 2024 and UAE digital banking adoption hit 68% in 2024, shifting pricing and service leverage to consumers.

These platforms often offer fee-free accounts and higher savings yields—some UAE digital challengers advertised 3.0–4.5% on deposits in 2024—forcing incumbents to match offers.

ADCB launched its digital brand Hayyak in 2023 to compete, but the expanding pool of alternatives keeps customer bargaining power high and raises service expectations.

- Neobank customer growth ~20% (2024)

- UAE digital banking adoption 68% (2024)

- Digital deposit yields 3.0–4.5% (2024)

- ADCB digital brand Hayyak launched 2023

Influence of Online Reviews and Social Proof

In 2025 ADCB faces amplified social bargaining power as social media and review sites can trigger swift reputational damage; a viral complaint in 2024 led UAE banks to report up to 4% short-term retail deposit outflows in similar episodes.

ADCB now spends an estimated 30–40m AED annually on customer service and reputation management, and monitors NPS and sentiment daily to prevent mass exits.

- Viral risk: ~4% deposit shock (industry precedent)

- Reputation spend: 30–40m AED/yr

- Daily NPS/sentiment monitoring

Digital transparency empowers customers: thin spreads, neobank surge, switching risk

Customers hold high bargaining power: digital transparency cut mortgage spreads to 0.35% median (2025), UAE digital banking adoption 68% (2024), neobanks +20% growth (2024); corporate clients = 38% of Abu Dhabi corporate loans (2024) demand bespoke terms; open banking and social media raise switching risk (industry deposit shock ~4%); ADCB spends ~30–40m AED/yr on reputation/NPS monitoring.

| Metric | Value |

|---|---|

| Mortgage spread (median) | 0.35% (2025) |

| UAE digital adoption | 68% (2024) |

| Neobank growth | ~20% (2024) |

| Corp loans share | 38% (Abu Dhabi, 2024) |

| Viral deposit shock | ~4% (industry) |

| Reputation spend | 30–40m AED/yr |

Same Document Delivered

Abu Dhabi Commercial Bank Porter's Five Forces Analysis

This preview shows the exact Abu Dhabi Commercial Bank Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you complete payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Abu Dhabi Commercial Bank (ADCB) faces moderate buyer power and intense rivalry from UAE legacy banks and rising fintech challengers, while regulatory oversight and capital requirements constrain new entrants; supplier power remains limited but technology partners are increasingly influential.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Abu Dhabi Commercial Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Low-Cost Deposits

Individual and corporate depositors supply most capital to Abu Dhabi Commercial Bank (ADCB); UAE interest rates and the central bank base rate drive their switching behavior, with the UAE base rate at 4.75% in Dec 2025.

By end-2025 ADCB kept a high CASA ratio of about 52%, lowering funding costs and weakening supplier power.

Still, large institutional depositors holding roughly 18% of deposits can push up yields or shift liquidity to rivals, raising short-term funding pressure.

Dependence on Global Technology Providers

ADCB depends on third-party vendors for cloud, cybersecurity and core banking systems, driving high supplier power as switching costs exceed $100m in legacy migration estimates and multi-month outages risk customer churn.

Cutting-edge AI needs push ADCB toward partners like Microsoft and Oracle; their platform lock-in and control of AI toolchains amplify leverage—global cloud market share: AWS 33%, Microsoft Azure 23% (2024).

Access to International Wholesale Funding

ADCB regularly taps international debt markets—issuing sukuk and bonds worth about $3–5bn annually (2023–2024)—to diversify funding and manage liquidity.

Global credit agencies and international investors supply this capital; their power tracks ADCB’s standalone ratings (A-/A3 range in 2024) and the UAE sovereign AA/AA2 ratings.

Shifts in global sentiment or a one-notch ESG downgrade could raise funding spreads by 25–75bp, lifting cost of funds and squeezing net interest margins.

Competition for Specialized Human Capital

The GCC has a constrained pool of fintech, risk and Sharia finance experts; industry surveys in 2024 showed UAE fintech talent shortage at ~35% and regional risk‑specialist vacancy growth of 22% year-over-year.

As ADCB targets full digital transformation by 2026, demand for these specialists raises their bargaining power, forcing higher pay and quicker hiring cycles.

ADCB must match market leads: premium pay, equity/bonus, training, and flexible work to secure talent and avoid project delays.

- 2024 UAE fintech talent gap ~35%

- Regional risk-specialist vacancies +22% YoY (2024)

- Target: digital transformation complete by 2026

- Retention tools: pay premium, equity, training, flexibility

Regulatory Influence of the UAE Central Bank

The Central Bank of the UAE is a de facto supplier of ADCB’s operating license and regulatory framework, controlling reserve requirements and the interest rate corridor that shape ADCB’s loanable funds and net interest margin; as of Dec 2025 reserve requirement stood at 14% for dirham liabilities, directly constraining liquidity.

Compliance is mandatory, so the regulator holds absolute sway over capital ratios, lending caps and product approvals—ADCB must adjust strategy when rules change, raising compliance costs and operational rigidity.

- Central Bank sets reserve req: 14% (Dec 2025)

- Interest rate corridor narrows NIM variability

- Regulatory changes raise compliance costs

- Licensing control limits market entry/expansion

Suppliers wield power: CASA cuts costs, big depositors, cloud dominance & fintech gaps

Suppliers have moderate-to-high power: retail deposits and 52% CASA cut funding costs, but 18% large depositors can pressure yields; cloud/AI vendors (AWS/Azure share 33%/23% in 2024) and scarce fintech talent (~35% gap 2024) raise switching costs; CBUAE control (reserve req 14% Dec 2025) is binding.

| Item | Value |

|---|---|

| CASA | 52% |

| Large depositors | ~18% |

| Reserve req | 14% (Dec 2025) |

| Cloud market | AWS 33% / Azure 23% (2024) |

| Fintech gap | ~35% (2024) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Abu Dhabi Commercial Bank, identifying disruptive threats, supplier/buyer power, substitute products, and barriers that shape its profitability.

A concise, one-sheet Porter's Five Forces for Abu Dhabi Commercial Bank—ideal for quick strategic decisions and boardroom slides.

Customers Bargaining Power

High Sensitivity to Interest Rates and Fees

Retail and corporate customers in the UAE have grown highly price-sensitive as digital comparison platforms cut search costs; by Q4 2025 online rate aggregation showed 92% of mortgage offers and 87% of personal loan products publicly comparable. This transparency—mortgage spreads narrowing to a 0.35% median and average credit-card fee disclosure up 40% year-over-year—gives customers leverage to demand lower rates and fees. ADCB must tighten pricing: a 25–60 bps reduction on select loan products may be needed to retain share against aggressive lenders. If ADCB delays repricing, churn could rise beyond 6% annually.

Low Switching Costs in the Digital Era

Open banking rollouts in the UAE since 2023 cut switching friction: API-based account portability lets customers move deposits and payments in days, raising customer bargaining power against ADCB. A 2024 UAE survey found 42% of retail customers would consider switching within 12 months if onboarding is simple, so ADCB must invest in UX and targeted loyalty to retain deposits and fee income. Aim: reduce churn under 10% annually by 2026 via emotional and functional lock-in.

Sophisticated Demands of Corporate Clients

Growth of Digital-Only Banking Alternatives

The rise of neobanks and digital-first subsidiaries has expanded choices; globally neobanks grew customers ~20% in 2024 and UAE digital banking adoption hit 68% in 2024, shifting pricing and service leverage to consumers.

These platforms often offer fee-free accounts and higher savings yields—some UAE digital challengers advertised 3.0–4.5% on deposits in 2024—forcing incumbents to match offers.

ADCB launched its digital brand Hayyak in 2023 to compete, but the expanding pool of alternatives keeps customer bargaining power high and raises service expectations.

- Neobank customer growth ~20% (2024)

- UAE digital banking adoption 68% (2024)

- Digital deposit yields 3.0–4.5% (2024)

- ADCB digital brand Hayyak launched 2023

Influence of Online Reviews and Social Proof

In 2025 ADCB faces amplified social bargaining power as social media and review sites can trigger swift reputational damage; a viral complaint in 2024 led UAE banks to report up to 4% short-term retail deposit outflows in similar episodes.

ADCB now spends an estimated 30–40m AED annually on customer service and reputation management, and monitors NPS and sentiment daily to prevent mass exits.

- Viral risk: ~4% deposit shock (industry precedent)

- Reputation spend: 30–40m AED/yr

- Daily NPS/sentiment monitoring

Digital transparency empowers customers: thin spreads, neobank surge, switching risk

Customers hold high bargaining power: digital transparency cut mortgage spreads to 0.35% median (2025), UAE digital banking adoption 68% (2024), neobanks +20% growth (2024); corporate clients = 38% of Abu Dhabi corporate loans (2024) demand bespoke terms; open banking and social media raise switching risk (industry deposit shock ~4%); ADCB spends ~30–40m AED/yr on reputation/NPS monitoring.

| Metric | Value |

|---|---|

| Mortgage spread (median) | 0.35% (2025) |

| UAE digital adoption | 68% (2024) |

| Neobank growth | ~20% (2024) |

| Corp loans share | 38% (Abu Dhabi, 2024) |

| Viral deposit shock | ~4% (industry) |

| Reputation spend | 30–40m AED/yr |

Same Document Delivered

Abu Dhabi Commercial Bank Porter's Five Forces Analysis

This preview shows the exact Abu Dhabi Commercial Bank Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you complete payment.