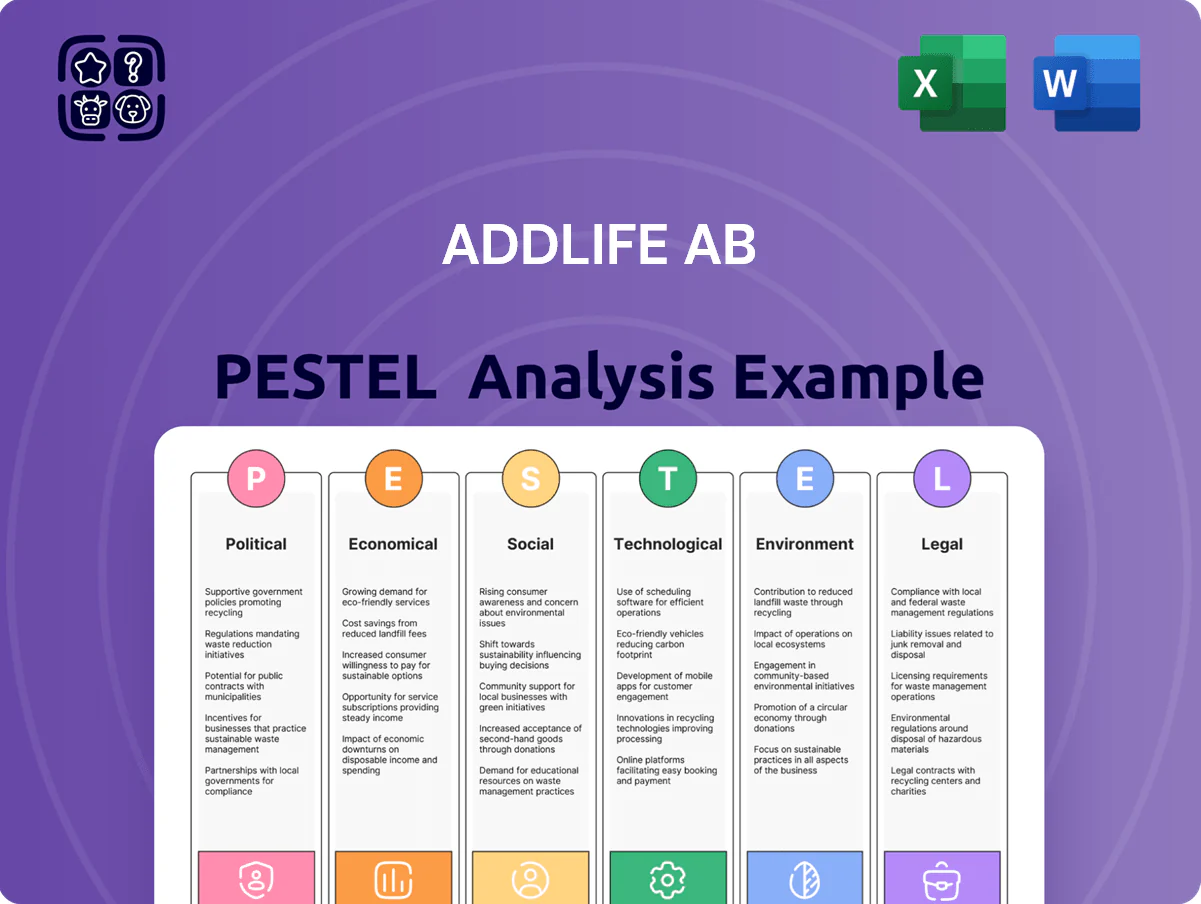

AddLife AB PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain actionable insights on how political shifts, economic cycles, regulation, social trends, technology advances, and environmental pressures shape AddLife AB’s prospects—our concise PESTLE highlights risks and opportunities you can act on. Ideal for investors and strategists who need fast, credible intelligence; purchase the full analysis to access the complete, downloadable report and data-driven recommendations.

Political factors

Nordic Public Healthcare Funding

AddLife's primary revenue depends on government healthcare budgets in Sweden, Norway, Denmark and Finland; public healthcare spending per capita in 2024: Sweden SEK ~62,000, Norway NOK ~87,000, Denmark DKK ~46,000, Finland EUR ~3,700, underpinning steady demand for Medtech and Labtech.

Political stability through late 2025 supports consistent investment, but coalition shifts have recently reprioritized procurement—e.g., Sweden's 2024 budget cut 1.2% for elective surgery grants in some regions, affecting device purchase timing.

Procurement is sensitive to national allocations for elective surgeries and screening: a 2024–25 uptick in mammography and colorectal screening funding (+8% combined in Nordics) correlates with higher diagnostic consumable sales for AddLife product lines.

EU Geopolitical Stability and Trade

AddLife depends on seamless movement of goods within the EEA to sustain its decentralized distribution; intra-EU trade accounted for about 70% of EU goods trade in 2024, underscoring exposure to border disruptions. Geopolitical tensions or EU trade disputes risk supply bottlenecks and higher tariffs on specialized components imported from non-EU suppliers, which comprised roughly 35% of AddLife’s sourced inputs in 2023. Strengthening ties with European manufacturers is a strategic priority to reduce volatility risk and safeguard margin stability.

National Health Security Policies

Following recent global health crises, Nordic governments increased domestic medical stockpiles by about 25%–40% between 2020–2024, favoring local suppliers; this policy shift strengthens AddLife AB’s position as a trusted regional partner for public hospitals.

AddLife’s 2024 Nordic revenue of ~SEK 6.1bn and diversified product portfolio make it well-placed to win multi-year government contracts tied to health sovereignty programs.

To capture these opportunities, AddLife must align inventory and logistics to national security mandates—holding higher buffer stocks and traceable supply chains—to meet procurement requirements and secure large-scale public tenders.

Healthcare Privatization Trends

Political debate over private versus public healthcare in Northern Europe affects AddLife AB; Sweden saw private providers capture about 30% of elective outpatient services in 2024, expanding addressable market segments for medical suppliers.

Greater privatization can boost demand from private clinics with shorter, varied purchasing cycles, while moves toward tighter public control risk centralized procurement—e.g., Sweden’s national framework contracts accounted for ~22% of hospital device spend in 2023—potentially compressing margins.

- 2024: private providers ~30% elective outpatient share (Sweden)

- 2023: national framework contracts ~22% of hospital device spend

- Privatization = diversified, faster purchasing; public control = centralized, rigid procurement

Global Regulatory Harmonization

Political moves toward EU-US-UK regulatory alignment, such as the 2023 EU-US Medical Device Memorandum of Understanding and post-Brexit UK conformity discussions, reduce approval timelines and lower duplication costs, helping AddLife introduce devices faster across markets where medtech trade between these blocs totaled over €120bn in 2024.

Trade agreements and regulatory convergence affect AddLife’s ability to license international innovations; strategic planners must monitor evolving frameworks to avoid average market-entry delays of 6–18 months and capture cross-border revenue upside.

- 2023 EU-US MOU and UK alignment talks speed approvals

- Medtech trade >€120bn (2024) signals large opportunity

- Typical market-entry delays 6–18 months if misaligned

AddLife SEK6.1bn: Public budgets, procurement & supply risks shape Nordic medtech growth

AddLife's 2024 Nordic revenue ~SEK 6.1bn ties closely to public health budgets (2024 per capita: SE SEK 62,000; NO NOK 87,000; DK DKK 46,000; FI EUR 3,700), with 70% intra-EEA trade exposure and ~35% non-EU input sourcing risk.

Public procurement (national frameworks ~22% hospital device spend 2023) vs private care (~30% elective outpatient share SE 2024) shapes demand and margin dynamics.

EU-US/UK regulatory alignment and +8% 2024–25 screening funding lift diagnostics sales; stockpile policies (+25–40% 2020–24) favor local suppliers.

| Metric | Value (2023–2024) |

|---|---|

| AddLife Nordic rev | ~SEK 6.1bn (2024) |

| Per-capita public health spend | SE 62,000; NO 87,000; DK 46,000; FI €3,700 (2024) |

| Intra-EEA trade exposure | ~70% (2024) |

| Non-EU inputs | ~35% (2023) |

| National frameworks share | ~22% hospital device spend (2023) |

| Private elective share (SE) | ~30% (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect AddLife AB across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and industry trends to identify risks and opportunities.

Compact PESTLE summary tailored for AddLife AB that distills external risks and opportunities by category for quick inclusion in presentations, team briefings, or client reports.

Economic factors

Interest Rate Volatility

AddLife's acquisition-led model is highly sensitive to central bank rate moves; with ECB policy rates near 3.75% in late 2025, higher borrowing costs raise the weighted average cost of capital for deals and increase annual interest expense on debt-funded acquisitions.

Elevated rates can slow portfolio expansion as service costs rise—AddLife reported net debt/EBITDA targets near 2.0x in 2024, making disciplined leverage vital to preserving credit metrics and M&A firepower.

By end-2025 management must prioritize capital allocation—balancing reinvestment, dividends and selective acquisitions—to maintain liquidity and meet covenant headroom amid rate volatility.

Inflationary Pressure on Operating Margins

Persistent inflation in raw materials, energy and logistics—Eurozone HICP at 5.3% in 2024—forces AddLife to be agile with pricing to protect margins amid rising medical‑grade plastics (+8–12% Y/Y) and electronics costs.

Long-term public sector contracts make inflation‑adjustment clauses vital; without them, 2024 cost pressures could erode gross margins already squeezed by higher input prices.

Management prioritizes operational efficiency and cost containment—lean manufacturing, supplier renegotiation and automation—to offset input inflation and sustain EBITDA margins near historical levels.

Currency Exchange Fluctuations

AddLife’s cross-border operations expose it to SEK volatility versus EUR, CHF and USD; a 5% SEK weakening vs EUR could swing reported EBIT by an estimated 2–4% given 2024 foreign-purchase intensity and ~35% revenue sourced outside Sweden.

Public Sector Budget Constraints

Economic downturns and low GDP growth prompt austerity in public healthcare; OECD health spending growth slowed to 0.9% in 2023, raising risk of delayed capital projects for laboratory infrastructure.

AddLife’s focus on value-based solutions that show lifecycle cost savings positions it competitively as hospitals cut capital expenditure—EU hospital capex fell ~6% in 2023 versus 2022.

- OECD health spending growth 0.9% (2023)

- EU hospital capex down ~6% (2023)

- AddLife emphasizes long-term cost-savings to secure budget-constrained buyers

Labor Market Competition

The tight labor market for life sciences specialists has driven wage inflation; OECD data show healthcare and technical roles rising 4–6% annually in 2024, increasing AddLife’s recruitment costs and margin pressure.

Securing skilled technicians, sales engineers and clinical experts is vital for service quality, forcing AddLife to offer premiums and signing bonuses to stay competitive.

Investing in retention and training—benchmarked against industry turnover of ~12% in 2024—reduces costly rehiring and preserves client-facing expertise.

- Wage inflation 4–6% (2024)

- Industry turnover ~12% (2024)

- Higher recruitment/bonus spend to secure specialized staff

- Retention/training investment required to protect margins

Rising ECB rates and inflation squeeze margins—M&A constrained as public health spend cools

Higher ECB rates (~3.75% late-2025) raise acquisition costs and interest expense; net debt/EBITDA ~2.0x (2024) constrains M&A. Eurozone HICP 5.3% (2024) pressures input costs; wage inflation 4–6% (2024) and turnover ~12% add HR costs. OECD health spending growth 0.9% (2023) and EU hospital capex -6% (2023) tighten public demand.

| Metric | Value |

|---|---|

| ECB rate (late-2025) | ~3.75% |

| Eurozone HICP (2024) | 5.3% |

| Net debt/EBITDA (AddLife 2024) | ~2.0x |

| Wage inflation (health, 2024) | 4–6% |

| OECD health spend (2023) | +0.9% |

| EU hospital capex (2023) | -6% |

Full Version Awaits

AddLife AB PESTLE Analysis

The preview shown here is the exact AddLife AB PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain actionable insights on how political shifts, economic cycles, regulation, social trends, technology advances, and environmental pressures shape AddLife AB’s prospects—our concise PESTLE highlights risks and opportunities you can act on. Ideal for investors and strategists who need fast, credible intelligence; purchase the full analysis to access the complete, downloadable report and data-driven recommendations.

Political factors

Nordic Public Healthcare Funding

AddLife's primary revenue depends on government healthcare budgets in Sweden, Norway, Denmark and Finland; public healthcare spending per capita in 2024: Sweden SEK ~62,000, Norway NOK ~87,000, Denmark DKK ~46,000, Finland EUR ~3,700, underpinning steady demand for Medtech and Labtech.

Political stability through late 2025 supports consistent investment, but coalition shifts have recently reprioritized procurement—e.g., Sweden's 2024 budget cut 1.2% for elective surgery grants in some regions, affecting device purchase timing.

Procurement is sensitive to national allocations for elective surgeries and screening: a 2024–25 uptick in mammography and colorectal screening funding (+8% combined in Nordics) correlates with higher diagnostic consumable sales for AddLife product lines.

EU Geopolitical Stability and Trade

AddLife depends on seamless movement of goods within the EEA to sustain its decentralized distribution; intra-EU trade accounted for about 70% of EU goods trade in 2024, underscoring exposure to border disruptions. Geopolitical tensions or EU trade disputes risk supply bottlenecks and higher tariffs on specialized components imported from non-EU suppliers, which comprised roughly 35% of AddLife’s sourced inputs in 2023. Strengthening ties with European manufacturers is a strategic priority to reduce volatility risk and safeguard margin stability.

National Health Security Policies

Following recent global health crises, Nordic governments increased domestic medical stockpiles by about 25%–40% between 2020–2024, favoring local suppliers; this policy shift strengthens AddLife AB’s position as a trusted regional partner for public hospitals.

AddLife’s 2024 Nordic revenue of ~SEK 6.1bn and diversified product portfolio make it well-placed to win multi-year government contracts tied to health sovereignty programs.

To capture these opportunities, AddLife must align inventory and logistics to national security mandates—holding higher buffer stocks and traceable supply chains—to meet procurement requirements and secure large-scale public tenders.

Healthcare Privatization Trends

Political debate over private versus public healthcare in Northern Europe affects AddLife AB; Sweden saw private providers capture about 30% of elective outpatient services in 2024, expanding addressable market segments for medical suppliers.

Greater privatization can boost demand from private clinics with shorter, varied purchasing cycles, while moves toward tighter public control risk centralized procurement—e.g., Sweden’s national framework contracts accounted for ~22% of hospital device spend in 2023—potentially compressing margins.

- 2024: private providers ~30% elective outpatient share (Sweden)

- 2023: national framework contracts ~22% of hospital device spend

- Privatization = diversified, faster purchasing; public control = centralized, rigid procurement

Global Regulatory Harmonization

Political moves toward EU-US-UK regulatory alignment, such as the 2023 EU-US Medical Device Memorandum of Understanding and post-Brexit UK conformity discussions, reduce approval timelines and lower duplication costs, helping AddLife introduce devices faster across markets where medtech trade between these blocs totaled over €120bn in 2024.

Trade agreements and regulatory convergence affect AddLife’s ability to license international innovations; strategic planners must monitor evolving frameworks to avoid average market-entry delays of 6–18 months and capture cross-border revenue upside.

- 2023 EU-US MOU and UK alignment talks speed approvals

- Medtech trade >€120bn (2024) signals large opportunity

- Typical market-entry delays 6–18 months if misaligned

AddLife SEK6.1bn: Public budgets, procurement & supply risks shape Nordic medtech growth

AddLife's 2024 Nordic revenue ~SEK 6.1bn ties closely to public health budgets (2024 per capita: SE SEK 62,000; NO NOK 87,000; DK DKK 46,000; FI EUR 3,700), with 70% intra-EEA trade exposure and ~35% non-EU input sourcing risk.

Public procurement (national frameworks ~22% hospital device spend 2023) vs private care (~30% elective outpatient share SE 2024) shapes demand and margin dynamics.

EU-US/UK regulatory alignment and +8% 2024–25 screening funding lift diagnostics sales; stockpile policies (+25–40% 2020–24) favor local suppliers.

| Metric | Value (2023–2024) |

|---|---|

| AddLife Nordic rev | ~SEK 6.1bn (2024) |

| Per-capita public health spend | SE 62,000; NO 87,000; DK 46,000; FI €3,700 (2024) |

| Intra-EEA trade exposure | ~70% (2024) |

| Non-EU inputs | ~35% (2023) |

| National frameworks share | ~22% hospital device spend (2023) |

| Private elective share (SE) | ~30% (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect AddLife AB across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by current data and industry trends to identify risks and opportunities.

Compact PESTLE summary tailored for AddLife AB that distills external risks and opportunities by category for quick inclusion in presentations, team briefings, or client reports.

Economic factors

Interest Rate Volatility

AddLife's acquisition-led model is highly sensitive to central bank rate moves; with ECB policy rates near 3.75% in late 2025, higher borrowing costs raise the weighted average cost of capital for deals and increase annual interest expense on debt-funded acquisitions.

Elevated rates can slow portfolio expansion as service costs rise—AddLife reported net debt/EBITDA targets near 2.0x in 2024, making disciplined leverage vital to preserving credit metrics and M&A firepower.

By end-2025 management must prioritize capital allocation—balancing reinvestment, dividends and selective acquisitions—to maintain liquidity and meet covenant headroom amid rate volatility.

Inflationary Pressure on Operating Margins

Persistent inflation in raw materials, energy and logistics—Eurozone HICP at 5.3% in 2024—forces AddLife to be agile with pricing to protect margins amid rising medical‑grade plastics (+8–12% Y/Y) and electronics costs.

Long-term public sector contracts make inflation‑adjustment clauses vital; without them, 2024 cost pressures could erode gross margins already squeezed by higher input prices.

Management prioritizes operational efficiency and cost containment—lean manufacturing, supplier renegotiation and automation—to offset input inflation and sustain EBITDA margins near historical levels.

Currency Exchange Fluctuations

AddLife’s cross-border operations expose it to SEK volatility versus EUR, CHF and USD; a 5% SEK weakening vs EUR could swing reported EBIT by an estimated 2–4% given 2024 foreign-purchase intensity and ~35% revenue sourced outside Sweden.

Public Sector Budget Constraints

Economic downturns and low GDP growth prompt austerity in public healthcare; OECD health spending growth slowed to 0.9% in 2023, raising risk of delayed capital projects for laboratory infrastructure.

AddLife’s focus on value-based solutions that show lifecycle cost savings positions it competitively as hospitals cut capital expenditure—EU hospital capex fell ~6% in 2023 versus 2022.

- OECD health spending growth 0.9% (2023)

- EU hospital capex down ~6% (2023)

- AddLife emphasizes long-term cost-savings to secure budget-constrained buyers

Labor Market Competition

The tight labor market for life sciences specialists has driven wage inflation; OECD data show healthcare and technical roles rising 4–6% annually in 2024, increasing AddLife’s recruitment costs and margin pressure.

Securing skilled technicians, sales engineers and clinical experts is vital for service quality, forcing AddLife to offer premiums and signing bonuses to stay competitive.

Investing in retention and training—benchmarked against industry turnover of ~12% in 2024—reduces costly rehiring and preserves client-facing expertise.

- Wage inflation 4–6% (2024)

- Industry turnover ~12% (2024)

- Higher recruitment/bonus spend to secure specialized staff

- Retention/training investment required to protect margins

Rising ECB rates and inflation squeeze margins—M&A constrained as public health spend cools

Higher ECB rates (~3.75% late-2025) raise acquisition costs and interest expense; net debt/EBITDA ~2.0x (2024) constrains M&A. Eurozone HICP 5.3% (2024) pressures input costs; wage inflation 4–6% (2024) and turnover ~12% add HR costs. OECD health spending growth 0.9% (2023) and EU hospital capex -6% (2023) tighten public demand.

| Metric | Value |

|---|---|

| ECB rate (late-2025) | ~3.75% |

| Eurozone HICP (2024) | 5.3% |

| Net debt/EBITDA (AddLife 2024) | ~2.0x |

| Wage inflation (health, 2024) | 4–6% |

| OECD health spend (2023) | +0.9% |

| EU hospital capex (2023) | -6% |

Full Version Awaits

AddLife AB PESTLE Analysis

The preview shown here is the exact AddLife AB PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making.