AdvanSix Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

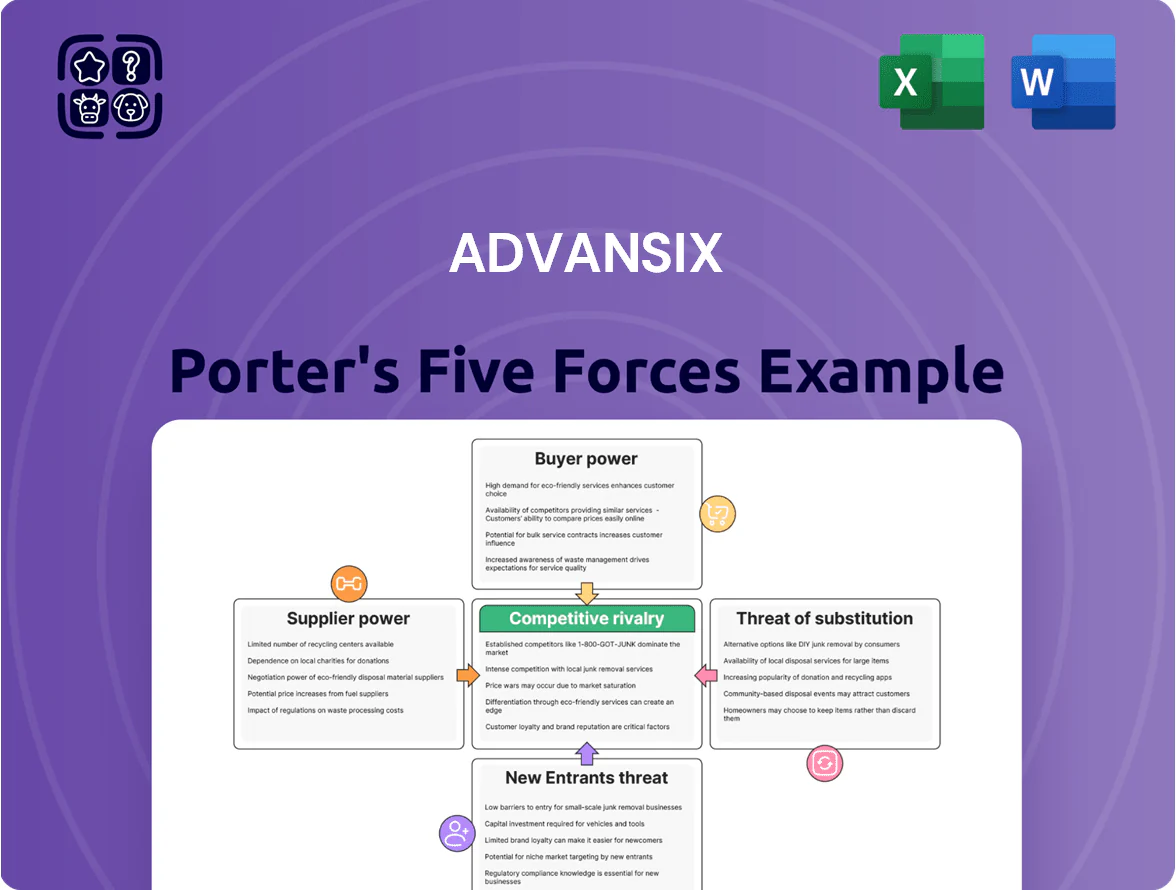

AdvanSix faces moderate supplier power, steady buyer demand, and material threat from substitutes and regulatory shifts that together shape a capital‑intensive competitive landscape; strategic scale, feedstock control, and product differentiation are key levers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore AdvanSix’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

AdvanSix depends on a small group of suppliers for cumene and natural gas, inputs that fuel its integrated phenol-acetone and nylon intermediates operations; in 2024 roughly 65% of feedstock volume came from three major providers. If one or more suppliers consolidate or hit outages, AdvanSix would struggle to replace high-volume supply quickly, given few qualified alternatives. This supplier concentration gives counterparties strong pricing leverage—spot gas spikes in 2022 raised feedstock costs ~28%, squeezing margins.

Volatile Energy and Feedstock Pricing

Benzene and propylene prices, which drive cumene economics, moved 38% and 22% year-over-year in 2024 at CME-tracked benchmarks, tying them closely to oil and gas volatility; as a large-scale buyer, AdvanSix is typically a price-taker and faces upside cost shocks when supply tightens. This exposure compressed AdvanSix’s 2024 gross margin by an estimated 180–250 basis points versus 2023 when costs rose faster than selling prices. If AdvanSix cannot pass spikes to customers within a quarter, profit margins erode quickly.

Critical Utility Dependencies

Manufacturing at Hopewell (VA) and Frankford (PA) needs large, continuous gas and electricity inputs; AdvanSix reported energy costs at about 18% of COGS in 2024, and site outages cost chemical plants an average $100k–$1M+ per day. Local utilities—Dominion Energy in VA and PPL/Norristown-area suppliers in PA—have near-monopoly footprints, so limited supplier choice raises their bargaining power and exposes AdvanSix to price and reliability risk.

Long-term Supply Agreement Constraints

Long-term supply contracts give AdvanSix price stability but often include minimum purchase volumes and pricing formulas tied to feedstock indices like benzene or natural gas, which rose 18–32% in 2021–2022 and remain volatile into 2025.

Those clauses prevent switching to cheaper spot-market offers when global supply gluts cut spot prices, locking AdvanSix into suppliers’ ecosystems for 1–5 years and raising input-cost risk.

Impact of Logistics and Transportation

Logistics for hazardous chemicals and bulk feedstocks depends on specialized rail, barge, and pipeline networks dominated by a few carriers; in 2024 US chemical transport rail rates rose ~9% year-over-year, and inland barge rates spiked 12% during Q2 supply tightness.

Any route disruption or price shock flows directly into AdvanSix’s landed costs and plant reliability, so carriers exert significant pricing leverage over raw-material margins.

- Specialized transport concentrated among few firms

- 2024 rail rates +9% y/y; barge +12% in Q2

- Disruptions raise landed cost and downtime risk

- Carriers control final raw-material margin

Supplier concentration, fuel & feedstock shocks squeeze AdvanSix margins

Supplier concentration (65% from three providers in 2024), index-linked contracts (1–5 years), energy ~18% of COGS, and 2024 feedstock volatility (benzene +38% y/y; propylene +22% y/y) give suppliers and carriers strong leverage, limiting AdvanSix’s pricing flexibility and exposing margins to supply outages and transport rate shocks.

| Metric | 2024 value |

|---|---|

| Share from top 3 suppliers | 65% |

| Energy as % of COGS | 18% |

| Benzene y/y move | +38% |

| Propylene y/y move | +22% |

| Rail rate change 2024 | +9% |

| Barge spike Q2 2024 | +12% |

What is included in the product

Tailored Porter's Five Forces analysis for AdvanSix, uncovering competitive intensity, customer and supplier power, entry barriers, and substitute threats that shape its pricing power and profitability.

A concise Porter's Five Forces snapshot for AdvanSix—quickly reveals supplier, buyer, and competitive pressures to guide strategic choices.

Customers Bargaining Power

Price Sensitivity in Commodity Markets

Price sensitivity is high for AdvanSix products like ammonium sulfate and acetone, which trade as commodities where buyers prioritize price; global spot acetone fell ~28% in 2024, pressuring sellers. Large agricultural distributors and chemical processors can compare offers across suppliers and push for double-digit discounts, reducing seller leverage. Transparent pricing and periodic global oversupply—US ammonium sulfate exports rose ~12% in 2024—cap margins and limit pricing power.

Low Switching Costs for Buyers

For commodity products like phenol and standard-grade nylon resins, buyers face low switching costs and can move orders if specs match; spot-market swings showed US phenol price volatility of ±18% in 2024, so buyers chase better terms.

This ease lets purchasers leverage alternative suppliers and forces AdvanSix to compete on price and service; AdvanSix reported 2024 gross margin of about 16%, so margin pressure from switching risk is tangible.

Customer Concentration in Specific Segments

About 40% of AdvanSix’s 2024 revenue came from large buyers in automotive, carpet, and packaging, so losing one could cut utilization sharply; a 10–15% demand drop historically reduces plant utilization by ~12 percentage points. These customers use concentrated volumes to push for lower prices and extended payment terms, squeezing margins and working capital—AdvanSix disclosed receivables days rose to 52 in 2024, partly reflecting this pressure.

Cyclical Demand in End Markets

The demand for AdvanSix’s engineered plastics and fertilizer is highly cyclical, linked to housing, automotive, and agriculture; US housing starts fell 8.5% in 2024 and global auto production dropped ~4% YoY, intensifying downside.

In downturns buyers cut inventories and press for lower prices; AdvanSix faced margin compression in 2024 Q3 as volumes fell and spot PVC prices dropped ~15% vs 2023.

This cyclicality boosts customer bargaining power during lean years, forcing producers to compete for fewer orders and offer concessions.

- Housing starts −8.5% (2024)

- Global auto output −4% YoY (2024)

- Spot PVC prices −15% vs 2023

- Higher buyer leverage in downturns

Availability of Global Imports

Customers can source nylon resins and intermediates from low-cost Asian and European producers; 2024 US import volume for nylon polymers rose 12% YoY to ~220 kt, keeping global spot prices ~15–25% below some domestic contract levels.

This import pressure caps AdvanSix’s pricing power, forcing it to align with international spot prices—buyers demand matching or better rates to retain supply, especially for spot-heavy purchasers.

- Global imports up 12% in 2024 (~220 kt)

- International spots 15–25% cheaper

- Price ceiling on AdvanSix domestic contracts

- Buyers demand parity to keep sourcing

AdvanSix margins under pressure as buyers force double‑digit discounts amid oversupply

Buyers wield strong price leverage across AdvanSix’s commodity lines—acetone spot down ~28% in 2024, US ammonium sulfate exports +12%—and low switching costs push double-digit discounts; AdvanSix 2024 gross margin ~16% and receivables days 52 reflect pressure. Large customers (~40% revenue) can cut volumes (10–15%) and demand longer terms; US nylon imports +12% (2024, ~220 kt) keep international spots 15–25% cheaper.

| Metric | 2024 |

|---|---|

| Gross margin | ~16% |

| Receivables days | 52 |

| Acetone spot | −28% |

| Ammonium sulfate exports | +12% |

| Nylon imports (US) | +12% (~220 kt) |

Preview Before You Purchase

AdvanSix Porter's Five Forces Analysis

This preview shows the exact AdvanSix Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

No mockups, no samples: you’re previewing the final, professionally written file that will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

AdvanSix faces moderate supplier power, steady buyer demand, and material threat from substitutes and regulatory shifts that together shape a capital‑intensive competitive landscape; strategic scale, feedstock control, and product differentiation are key levers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore AdvanSix’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

AdvanSix depends on a small group of suppliers for cumene and natural gas, inputs that fuel its integrated phenol-acetone and nylon intermediates operations; in 2024 roughly 65% of feedstock volume came from three major providers. If one or more suppliers consolidate or hit outages, AdvanSix would struggle to replace high-volume supply quickly, given few qualified alternatives. This supplier concentration gives counterparties strong pricing leverage—spot gas spikes in 2022 raised feedstock costs ~28%, squeezing margins.

Volatile Energy and Feedstock Pricing

Benzene and propylene prices, which drive cumene economics, moved 38% and 22% year-over-year in 2024 at CME-tracked benchmarks, tying them closely to oil and gas volatility; as a large-scale buyer, AdvanSix is typically a price-taker and faces upside cost shocks when supply tightens. This exposure compressed AdvanSix’s 2024 gross margin by an estimated 180–250 basis points versus 2023 when costs rose faster than selling prices. If AdvanSix cannot pass spikes to customers within a quarter, profit margins erode quickly.

Critical Utility Dependencies

Manufacturing at Hopewell (VA) and Frankford (PA) needs large, continuous gas and electricity inputs; AdvanSix reported energy costs at about 18% of COGS in 2024, and site outages cost chemical plants an average $100k–$1M+ per day. Local utilities—Dominion Energy in VA and PPL/Norristown-area suppliers in PA—have near-monopoly footprints, so limited supplier choice raises their bargaining power and exposes AdvanSix to price and reliability risk.

Long-term Supply Agreement Constraints

Long-term supply contracts give AdvanSix price stability but often include minimum purchase volumes and pricing formulas tied to feedstock indices like benzene or natural gas, which rose 18–32% in 2021–2022 and remain volatile into 2025.

Those clauses prevent switching to cheaper spot-market offers when global supply gluts cut spot prices, locking AdvanSix into suppliers’ ecosystems for 1–5 years and raising input-cost risk.

Impact of Logistics and Transportation

Logistics for hazardous chemicals and bulk feedstocks depends on specialized rail, barge, and pipeline networks dominated by a few carriers; in 2024 US chemical transport rail rates rose ~9% year-over-year, and inland barge rates spiked 12% during Q2 supply tightness.

Any route disruption or price shock flows directly into AdvanSix’s landed costs and plant reliability, so carriers exert significant pricing leverage over raw-material margins.

- Specialized transport concentrated among few firms

- 2024 rail rates +9% y/y; barge +12% in Q2

- Disruptions raise landed cost and downtime risk

- Carriers control final raw-material margin

Supplier concentration, fuel & feedstock shocks squeeze AdvanSix margins

Supplier concentration (65% from three providers in 2024), index-linked contracts (1–5 years), energy ~18% of COGS, and 2024 feedstock volatility (benzene +38% y/y; propylene +22% y/y) give suppliers and carriers strong leverage, limiting AdvanSix’s pricing flexibility and exposing margins to supply outages and transport rate shocks.

| Metric | 2024 value |

|---|---|

| Share from top 3 suppliers | 65% |

| Energy as % of COGS | 18% |

| Benzene y/y move | +38% |

| Propylene y/y move | +22% |

| Rail rate change 2024 | +9% |

| Barge spike Q2 2024 | +12% |

What is included in the product

Tailored Porter's Five Forces analysis for AdvanSix, uncovering competitive intensity, customer and supplier power, entry barriers, and substitute threats that shape its pricing power and profitability.

A concise Porter's Five Forces snapshot for AdvanSix—quickly reveals supplier, buyer, and competitive pressures to guide strategic choices.

Customers Bargaining Power

Price Sensitivity in Commodity Markets

Price sensitivity is high for AdvanSix products like ammonium sulfate and acetone, which trade as commodities where buyers prioritize price; global spot acetone fell ~28% in 2024, pressuring sellers. Large agricultural distributors and chemical processors can compare offers across suppliers and push for double-digit discounts, reducing seller leverage. Transparent pricing and periodic global oversupply—US ammonium sulfate exports rose ~12% in 2024—cap margins and limit pricing power.

Low Switching Costs for Buyers

For commodity products like phenol and standard-grade nylon resins, buyers face low switching costs and can move orders if specs match; spot-market swings showed US phenol price volatility of ±18% in 2024, so buyers chase better terms.

This ease lets purchasers leverage alternative suppliers and forces AdvanSix to compete on price and service; AdvanSix reported 2024 gross margin of about 16%, so margin pressure from switching risk is tangible.

Customer Concentration in Specific Segments

About 40% of AdvanSix’s 2024 revenue came from large buyers in automotive, carpet, and packaging, so losing one could cut utilization sharply; a 10–15% demand drop historically reduces plant utilization by ~12 percentage points. These customers use concentrated volumes to push for lower prices and extended payment terms, squeezing margins and working capital—AdvanSix disclosed receivables days rose to 52 in 2024, partly reflecting this pressure.

Cyclical Demand in End Markets

The demand for AdvanSix’s engineered plastics and fertilizer is highly cyclical, linked to housing, automotive, and agriculture; US housing starts fell 8.5% in 2024 and global auto production dropped ~4% YoY, intensifying downside.

In downturns buyers cut inventories and press for lower prices; AdvanSix faced margin compression in 2024 Q3 as volumes fell and spot PVC prices dropped ~15% vs 2023.

This cyclicality boosts customer bargaining power during lean years, forcing producers to compete for fewer orders and offer concessions.

- Housing starts −8.5% (2024)

- Global auto output −4% YoY (2024)

- Spot PVC prices −15% vs 2023

- Higher buyer leverage in downturns

Availability of Global Imports

Customers can source nylon resins and intermediates from low-cost Asian and European producers; 2024 US import volume for nylon polymers rose 12% YoY to ~220 kt, keeping global spot prices ~15–25% below some domestic contract levels.

This import pressure caps AdvanSix’s pricing power, forcing it to align with international spot prices—buyers demand matching or better rates to retain supply, especially for spot-heavy purchasers.

- Global imports up 12% in 2024 (~220 kt)

- International spots 15–25% cheaper

- Price ceiling on AdvanSix domestic contracts

- Buyers demand parity to keep sourcing

AdvanSix margins under pressure as buyers force double‑digit discounts amid oversupply

Buyers wield strong price leverage across AdvanSix’s commodity lines—acetone spot down ~28% in 2024, US ammonium sulfate exports +12%—and low switching costs push double-digit discounts; AdvanSix 2024 gross margin ~16% and receivables days 52 reflect pressure. Large customers (~40% revenue) can cut volumes (10–15%) and demand longer terms; US nylon imports +12% (2024, ~220 kt) keep international spots 15–25% cheaper.

| Metric | 2024 |

|---|---|

| Gross margin | ~16% |

| Receivables days | 52 |

| Acetone spot | −28% |

| Ammonium sulfate exports | +12% |

| Nylon imports (US) | +12% (~220 kt) |

Preview Before You Purchase

AdvanSix Porter's Five Forces Analysis

This preview shows the exact AdvanSix Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

No mockups, no samples: you’re previewing the final, professionally written file that will be available to you instantly after payment.