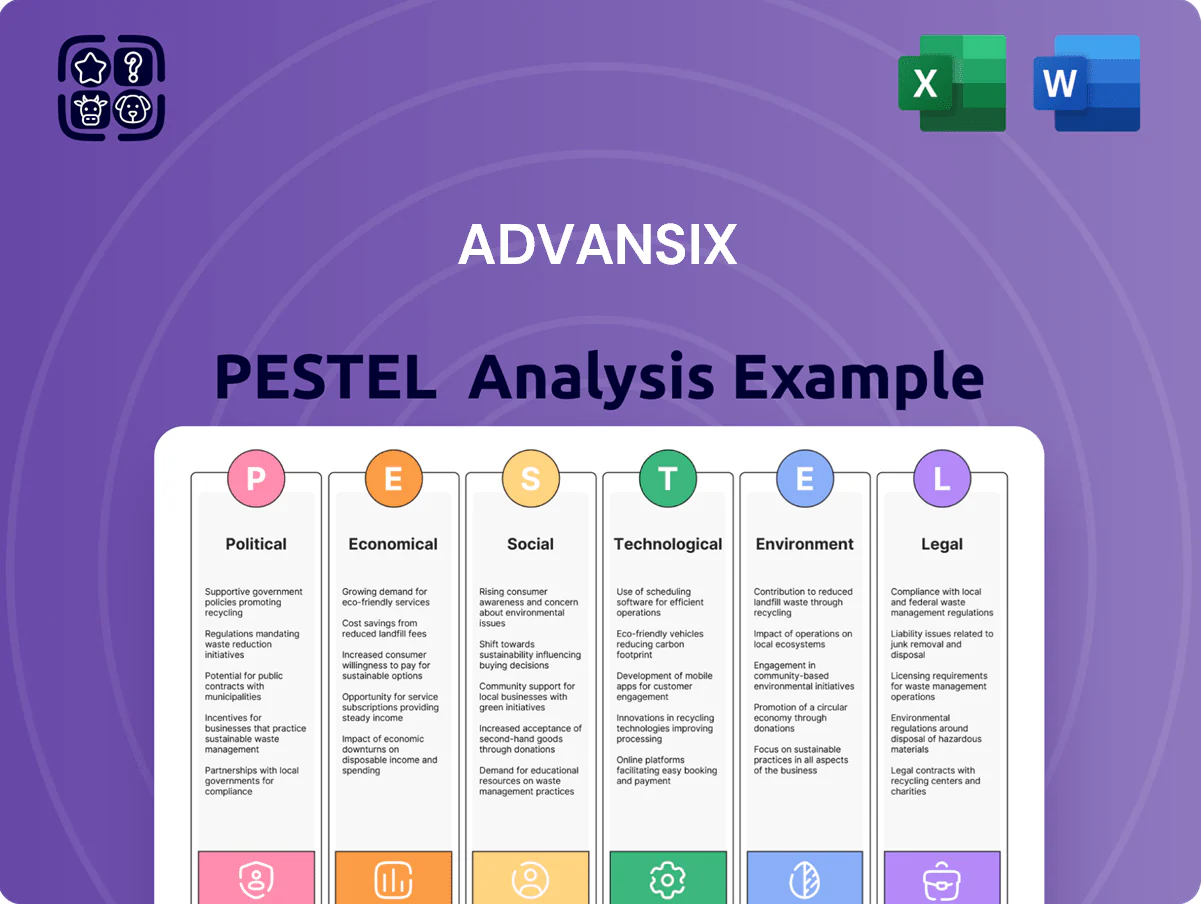

AdvanSix PESTLE Analysis

Skip the Research. Get the Strategy.

Explore how political, economic, social, technological, legal, and environmental forces are shaping AdvanSix’s prospects in our concise PESTLE snapshot — ideal for investors and strategists who need quick, actionable context. Purchase the full PESTLE for a detailed breakdown, risk scores, and strategic recommendations you can use immediately to inform investment decisions or corporate planning.

Political factors

Trade policy and tariffs

Trade tensions and protectionist measures disrupt flow of chemical intermediates and nylon resins; global resin trade fell 6% in 2024 amid higher tariffs and supply-chain rerouting. Changes to trade agreements or anti-dumping duties—US recent duties on certain polyester imports rose to 15–25% in 2024—reshape competitive dynamics, pressuring US producers. AdvanSix must manage input costs and pricing to defend market share versus lower-cost foreign imports.

U.S. manufacturing incentives

Federal initiatives like the CHIPS and Science Act and the Inflation Reduction Act, alongside $50B+ planned federal infrastructure investments, boost demand for domestically produced chemicals, creating a tailwind for integrated providers such as AdvanSix; domestic sourcing requirements and tax incentives improve project economics. Legislative support for reshoring and incentives for manufacturing capacity have contributed to a 12–15% rise in U.S. chemical capital expenditures in 2024–2025, encouraging long-term investment. These policies help stabilize supply chains for essential polymers and fertilizers, supporting AdvanSix’s position in urethane, nylon intermediates and ammonia-based fertilizers.

Agricultural subsidy programs

Government support for agriculture, including the 2023 US Farm Bill allocations and $15.2 billion in federal crop insurance outlays in 2024, directly affects demand for ammonium sulfate fertilizer used by AdvanSix customers.

Changes to subsidy rates or insurance indemnity rules alter farm cash flow and purchasing power, with USDA data showing net farm income down 6% in 2024 versus 2023, influencing fertilizer spend.

AdvanSix monitors these political shifts and models seasonal demand, noting that a 1% change in planted acreage historically correlates to ~0.8% change in ammonium sulfate volumes.

Geopolitical stability and energy security

Global political instability raises raw material and energy price volatility; crude oil jumped to about $85–95/bbl in 2024–2025 on supply shocks, pressuring feedstock costs for chemical producers like AdvanSix.

As a domestic ammonium sulfate and nylon precursor maker, AdvanSix benefits from U.S. energy exports and reduced supply-chain risk, but its margins remain sensitive to global oil and natural gas price swings—U.S. Henry Hub averaged near $3–5/MMBtu in 2024, yet spikes occur with geopolitics.

Political unrest in major energy regions can rapidly increase operating costs and input shortages, driving input-driven EBITDA variability for AdvanSix, which reported energy and feedstock as material cost drivers in recent filings.

- Crude oil ~ $85–95/bbl (2024–2025)

- Henry Hub ~ $3–5/MMBtu (2024 average)

- Energy/feedstock = material driver of AdvanSix margins per recent filings

Regulatory oversight on chemical safety

Political pressure for tighter oversight raises compliance costs for chemical makers like AdvanSix, which spent about $45m on environmental and safety capital projects in 2024; stricter rules can alter operational protocols and increase opex.

Shifts in leadership at EPA and OSHA since 2023 have changed enforcement focus toward risk-based inspections and community right-to-know, raising regulatory uncertainty for specialty-chemicals producers.

Ongoing engagement with policymakers helps keep regulations balanced and science-based; AdvanSix’s government affairs outreach increased in 2024 as it sought to influence rulemaking affecting an estimated $800m in annual revenue.

- Compliance capex: $45m (2024)

- Revenue potentially affected: $800m annually

- Regulatory focus: risk-based inspections, community disclosure

Tariffs, energy swings and policy lift reshape chemicals—reshoring offsets weaker farm demand

Trade barriers and tariffs (resin trade -6% in 2024; polyester duties 15–25%) raise input costs; federal incentives (CHIPS/IRA, $50B+ infrastructure) lifted US chemical capex ~12–15% (2024–25), aiding reshoring; farm support ($15.2B crop insurance 2024) and -6% net farm income in 2024 compress fertilizer demand; energy volatility (crude $85–95/bbl; Henry Hub $3–5/MMBtu) drives margin risk.

| Metric | 2024–25 |

|---|---|

| Global resin trade | -6% |

| Polyester duties | 15–25% |

| US chemical capex | +12–15% |

| Crop insurance outlays | $15.2B |

| Net farm income | -6% |

| Crude oil | $85–95/bbl |

| Henry Hub | $3–5/MMBtu |

| AdvanSix compliance capex | $45M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact AdvanSix, with data-backed trends and industry-specific examples to identify risks and opportunities.

A concise, visually segmented AdvanSix PESTLE summary that can be dropped into presentations or shared across teams, helping stakeholders quickly assess external risks, regulatory impacts, and market positioning for faster, aligned decision-making.

Economic factors

Global commodity price volatility

AdvanSix profitability hinges on spreads between raw material and finished goods prices; benzene averaged about $1,050/ton in 2024 versus nylon 6 contract prices near $2,500/ton, compressing margins when benzene or natural gas rise.

Natural gas Henry Hub averaged $3.80/MMBtu in 2024, and a 20% rise can erode caprolactam margins materially given energy intensity of production.

In 2024 AdvanSix reported adjusted EBITDA of $178 million; strategic hedging of feedstocks and lean supply-chain logistics are therefore critical to stabilize cash flows and protect margins against commodity volatility.

Interest rate environment

Prevailing interest rates raise AdvanSixs cost of capital for large-scale upgrades; the US Federal Reserve's fed funds rate at 5.25–5.50% (Feb 2025) increases borrowing costs vs. the 2021–22 lows, affecting project IRRs.

Higher rates can reduce demand in construction and automotive—US housing starts fell 11% YoY in 2024 and US vehicle sales dipped ~4%—pressuring volumes for nylon and chemical inputs.

AdvanSix must actively manage its debt profile and capital allocation: as of FY2024 it carried roughly $200m–$300m of net debt (company filings), requiring hedging and staged capex to mitigate rate risk.

Cyclicality of end markets

Demand for engineered plastics and fibers at AdvanSix is tied to automotive, electronics and housing cycles; U.S. auto production fell 8% in 2023 and global smartphone shipments declined ~4% in 2023–24, pressuring nylon 6 volumes. Economic downturns pull consumer spending on durables, and AdvanSix reported a 6% volume drop in specialty intermediates in 2023 versus 2022. Diversification across industrial, packaging and textile end markets helps buffer sector-specific contractions.

Labor market dynamics

- Wage inflation: chemical sector ~5% (2024)

- Manufacturing wage growth: 4.0% YoY (2024)

- Capex/R&D rise: ~8% (2024)

- Labor hours/unit down: ~6% (post-automation)

Currency exchange rate fluctuations

As a global supplier, AdvanSix’s competitiveness in 2024–2025 is sensitive to U.S. dollar moves; the dollar strengthened ~5% vs. a trade-weighted basket in 2024, which can make AdvanSix exports pricier for overseas buyers and pressure volumes.

A strong dollar also makes imports cheaper for U.S. customers, potentially increasing domestic competition and squeezing margins; annual FX swings have driven quarterly revenue variability for chemical exporters by up to 3–6% in recent reports.

Currency volatility requires robust hedging and financial planning; AdvanSix would need instruments like forward contracts and natural hedges to protect international revenue and stabilize EBITDA exposed to FX.

- 2024 trade-weighted USD +5% — export price pressure

- FX swings linked to 3–6% revenue variability

- Hedging, forwards, natural hedges recommended

AdvanSix margins squeezed as benzene/nylon spreads, energy and FX costs bite

AdvanSix margins hinge on benzene vs nylon spreads (benzene ~$1,050/t, nylon 6 ~$2,500/t in 2024); Henry Hub ~$3.80/MMBtu (2024) and fed funds 5.25–5.50% (Feb 2025) raise energy and funding costs; FY2024 adj. EBITDA $178M with net debt ~$200–300M, wage inflation ~4–5% (2024) and USD +5% (trade-weighted) add volume and FX pressure.

| Metric | 2024/2025 |

|---|---|

| Benzene | $1,050/t |

| Nylon 6 | $2,500/t |

| Henry Hub | $3.80/MMBtu |

| Adj. EBITDA | $178M |

| Net debt | $200–300M |

| Fed funds | 5.25–5.50% |

| USD TWI | +5% |

Preview the Actual Deliverable

AdvanSix PESTLE Analysis

The preview shown here is the exact AdvanSix PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making and investor review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Explore how political, economic, social, technological, legal, and environmental forces are shaping AdvanSix’s prospects in our concise PESTLE snapshot — ideal for investors and strategists who need quick, actionable context. Purchase the full PESTLE for a detailed breakdown, risk scores, and strategic recommendations you can use immediately to inform investment decisions or corporate planning.

Political factors

Trade policy and tariffs

Trade tensions and protectionist measures disrupt flow of chemical intermediates and nylon resins; global resin trade fell 6% in 2024 amid higher tariffs and supply-chain rerouting. Changes to trade agreements or anti-dumping duties—US recent duties on certain polyester imports rose to 15–25% in 2024—reshape competitive dynamics, pressuring US producers. AdvanSix must manage input costs and pricing to defend market share versus lower-cost foreign imports.

U.S. manufacturing incentives

Federal initiatives like the CHIPS and Science Act and the Inflation Reduction Act, alongside $50B+ planned federal infrastructure investments, boost demand for domestically produced chemicals, creating a tailwind for integrated providers such as AdvanSix; domestic sourcing requirements and tax incentives improve project economics. Legislative support for reshoring and incentives for manufacturing capacity have contributed to a 12–15% rise in U.S. chemical capital expenditures in 2024–2025, encouraging long-term investment. These policies help stabilize supply chains for essential polymers and fertilizers, supporting AdvanSix’s position in urethane, nylon intermediates and ammonia-based fertilizers.

Agricultural subsidy programs

Government support for agriculture, including the 2023 US Farm Bill allocations and $15.2 billion in federal crop insurance outlays in 2024, directly affects demand for ammonium sulfate fertilizer used by AdvanSix customers.

Changes to subsidy rates or insurance indemnity rules alter farm cash flow and purchasing power, with USDA data showing net farm income down 6% in 2024 versus 2023, influencing fertilizer spend.

AdvanSix monitors these political shifts and models seasonal demand, noting that a 1% change in planted acreage historically correlates to ~0.8% change in ammonium sulfate volumes.

Geopolitical stability and energy security

Global political instability raises raw material and energy price volatility; crude oil jumped to about $85–95/bbl in 2024–2025 on supply shocks, pressuring feedstock costs for chemical producers like AdvanSix.

As a domestic ammonium sulfate and nylon precursor maker, AdvanSix benefits from U.S. energy exports and reduced supply-chain risk, but its margins remain sensitive to global oil and natural gas price swings—U.S. Henry Hub averaged near $3–5/MMBtu in 2024, yet spikes occur with geopolitics.

Political unrest in major energy regions can rapidly increase operating costs and input shortages, driving input-driven EBITDA variability for AdvanSix, which reported energy and feedstock as material cost drivers in recent filings.

- Crude oil ~ $85–95/bbl (2024–2025)

- Henry Hub ~ $3–5/MMBtu (2024 average)

- Energy/feedstock = material driver of AdvanSix margins per recent filings

Regulatory oversight on chemical safety

Political pressure for tighter oversight raises compliance costs for chemical makers like AdvanSix, which spent about $45m on environmental and safety capital projects in 2024; stricter rules can alter operational protocols and increase opex.

Shifts in leadership at EPA and OSHA since 2023 have changed enforcement focus toward risk-based inspections and community right-to-know, raising regulatory uncertainty for specialty-chemicals producers.

Ongoing engagement with policymakers helps keep regulations balanced and science-based; AdvanSix’s government affairs outreach increased in 2024 as it sought to influence rulemaking affecting an estimated $800m in annual revenue.

- Compliance capex: $45m (2024)

- Revenue potentially affected: $800m annually

- Regulatory focus: risk-based inspections, community disclosure

Tariffs, energy swings and policy lift reshape chemicals—reshoring offsets weaker farm demand

Trade barriers and tariffs (resin trade -6% in 2024; polyester duties 15–25%) raise input costs; federal incentives (CHIPS/IRA, $50B+ infrastructure) lifted US chemical capex ~12–15% (2024–25), aiding reshoring; farm support ($15.2B crop insurance 2024) and -6% net farm income in 2024 compress fertilizer demand; energy volatility (crude $85–95/bbl; Henry Hub $3–5/MMBtu) drives margin risk.

| Metric | 2024–25 |

|---|---|

| Global resin trade | -6% |

| Polyester duties | 15–25% |

| US chemical capex | +12–15% |

| Crop insurance outlays | $15.2B |

| Net farm income | -6% |

| Crude oil | $85–95/bbl |

| Henry Hub | $3–5/MMBtu |

| AdvanSix compliance capex | $45M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact AdvanSix, with data-backed trends and industry-specific examples to identify risks and opportunities.

A concise, visually segmented AdvanSix PESTLE summary that can be dropped into presentations or shared across teams, helping stakeholders quickly assess external risks, regulatory impacts, and market positioning for faster, aligned decision-making.

Economic factors

Global commodity price volatility

AdvanSix profitability hinges on spreads between raw material and finished goods prices; benzene averaged about $1,050/ton in 2024 versus nylon 6 contract prices near $2,500/ton, compressing margins when benzene or natural gas rise.

Natural gas Henry Hub averaged $3.80/MMBtu in 2024, and a 20% rise can erode caprolactam margins materially given energy intensity of production.

In 2024 AdvanSix reported adjusted EBITDA of $178 million; strategic hedging of feedstocks and lean supply-chain logistics are therefore critical to stabilize cash flows and protect margins against commodity volatility.

Interest rate environment

Prevailing interest rates raise AdvanSixs cost of capital for large-scale upgrades; the US Federal Reserve's fed funds rate at 5.25–5.50% (Feb 2025) increases borrowing costs vs. the 2021–22 lows, affecting project IRRs.

Higher rates can reduce demand in construction and automotive—US housing starts fell 11% YoY in 2024 and US vehicle sales dipped ~4%—pressuring volumes for nylon and chemical inputs.

AdvanSix must actively manage its debt profile and capital allocation: as of FY2024 it carried roughly $200m–$300m of net debt (company filings), requiring hedging and staged capex to mitigate rate risk.

Cyclicality of end markets

Demand for engineered plastics and fibers at AdvanSix is tied to automotive, electronics and housing cycles; U.S. auto production fell 8% in 2023 and global smartphone shipments declined ~4% in 2023–24, pressuring nylon 6 volumes. Economic downturns pull consumer spending on durables, and AdvanSix reported a 6% volume drop in specialty intermediates in 2023 versus 2022. Diversification across industrial, packaging and textile end markets helps buffer sector-specific contractions.

Labor market dynamics

- Wage inflation: chemical sector ~5% (2024)

- Manufacturing wage growth: 4.0% YoY (2024)

- Capex/R&D rise: ~8% (2024)

- Labor hours/unit down: ~6% (post-automation)

Currency exchange rate fluctuations

As a global supplier, AdvanSix’s competitiveness in 2024–2025 is sensitive to U.S. dollar moves; the dollar strengthened ~5% vs. a trade-weighted basket in 2024, which can make AdvanSix exports pricier for overseas buyers and pressure volumes.

A strong dollar also makes imports cheaper for U.S. customers, potentially increasing domestic competition and squeezing margins; annual FX swings have driven quarterly revenue variability for chemical exporters by up to 3–6% in recent reports.

Currency volatility requires robust hedging and financial planning; AdvanSix would need instruments like forward contracts and natural hedges to protect international revenue and stabilize EBITDA exposed to FX.

- 2024 trade-weighted USD +5% — export price pressure

- FX swings linked to 3–6% revenue variability

- Hedging, forwards, natural hedges recommended

AdvanSix margins squeezed as benzene/nylon spreads, energy and FX costs bite

AdvanSix margins hinge on benzene vs nylon spreads (benzene ~$1,050/t, nylon 6 ~$2,500/t in 2024); Henry Hub ~$3.80/MMBtu (2024) and fed funds 5.25–5.50% (Feb 2025) raise energy and funding costs; FY2024 adj. EBITDA $178M with net debt ~$200–300M, wage inflation ~4–5% (2024) and USD +5% (trade-weighted) add volume and FX pressure.

| Metric | 2024/2025 |

|---|---|

| Benzene | $1,050/t |

| Nylon 6 | $2,500/t |

| Henry Hub | $3.80/MMBtu |

| Adj. EBITDA | $178M |

| Net debt | $200–300M |

| Fed funds | 5.25–5.50% |

| USD TWI | +5% |

Preview the Actual Deliverable

AdvanSix PESTLE Analysis

The preview shown here is the exact AdvanSix PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decision-making and investor review.