Aecon Boston Consulting Group Matrix

Actionable Strategy Starts Here

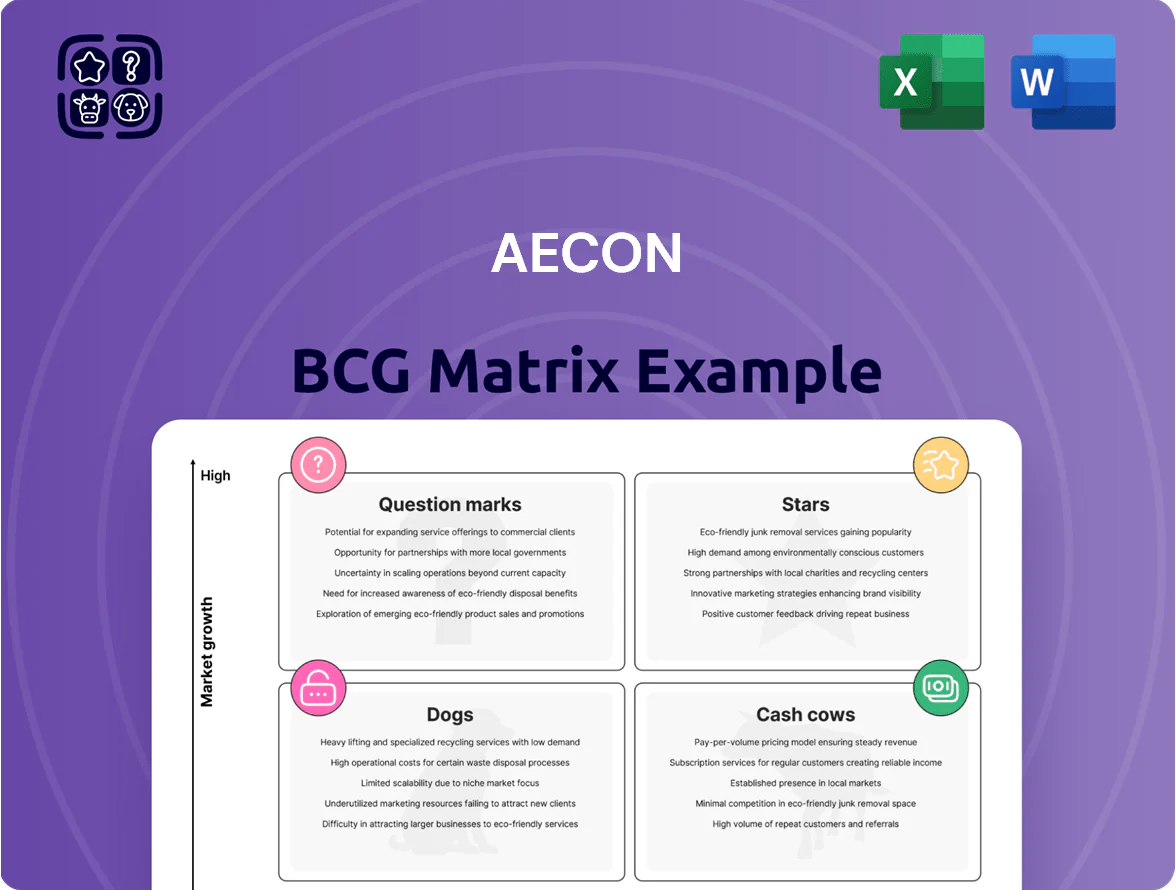

Aecon’s BCG Matrix preview highlights how its business units balance market share and growth — from infrastructure Stars to potential Dogs — offering a snapshot of where capital and strategic focus may be needed. This condensed view signals key strengths and risks but stops short of the granular, quadrant-level data that drives confident decisions. Purchase the full BCG Matrix for a complete breakdown, actionable recommendations, and downloadable Word and Excel formats to present and execute your strategy immediately.

Stars

Energy Transition and Nuclear SMRs

Aecon, via partnerships with Ontario Power Generation, holds a leading SMR pipeline worth ~C$3.2bn in contracted work to 2030, capturing early-mover margins in a sector Canada targets for net-zero by 2050 and net-zero electricity by 2035; SMR market demand is projected at C$20–30bn nationally through 2040.

Major Urban Transit Expansion

Aecon leads multi-billion-dollar transit projects including Toronto’s Ontario Line (budget C$11.6B total; Aecon scope ~C$2–3B) and Montreal REM expansions, key to urban decarbonization and public transit ridership growth of 12% in Toronto 2019–24. These contracts drain cash for equipment and labor but sit in Canada’s fastest-growing infra segment, with light rail market forecast CAGR 6.2% to 2030.

Grid Modernization and Electrification

Aecon’s utilities segment is capturing high-voltage transmission demand driven by EV adoption; Canada’s EV stock rose 55% in 2024, pushing grid upgrade spend—transmission capex in North America hit US$56bn in 2024 (IEA/NEB mix)—and Aecon’s revenues from utilities rose ~18% in FY2024.

Industrial Decarbonization Projects

Aecon is winning ~25% of Canadian heavy-industrial retrofit contracts in 2023–2025, capturing key petrochemical and steel site work as carbon taxes and ESG rules push companies to decarbonize.

Demand grew ~18% CAGR 2020–2025 for industrial decarbonization spending; Aecon’s heavy CAPEX now positions it as preferred contractor for complex green conversions.

- Market share ~25% (2023–2025)

- Sector spend CAGR ~18% (2020–2025)

- Target clients: petrochemical, steel, cement

- Rising compliance costs (carbon tax increases to 2030)

Digital Infrastructure and Connectivity

Aecon’s Digital Infrastructure and Connectivity is a star: the firm is a key contractor in Canada’s 5G and fiber-to-the-home (FTTH) rollout, a market forecasted to grow ~8% CAGR through 2028 with Canadian telecom capex topping CAD 10–12B annually in 2024–25.

High capex needs—tower builds, fiber trenching, equipment—force heavy upfront investment and working-capital cycles; Aecon’s recent telecom backlog of CAD ~1.2B (2024) supports rapid deployment schedules.

Connectivity is essential to GDP growth, so this segment earns premium returns despite execution risk from tech shifts and permitting delays.

- Market growth ~8% CAGR to 2028

- Canadian telco capex CAD 10–12B (2024–25)

- Aecon telecom backlog ~CAD 1.2B (2024)

- High upfront capex, rapid deployment required

Aecon’s C$11.6bn Opportunity: SMR, Transit, Utilities, Telecom & Heavy-Industrial Growth

Aecon’s Stars: SMR pipeline C$3.2bn contracted to 2030; transit scope ~C$2–3bn on Ontario Line (total C$11.6bn); utilities revenue +18% FY2024 amid 55% EV stock rise (2024); telecom backlog C$1.2bn with telco capex C$10–12bn (2024–25); heavy-industrial market share ~25% (2023–25), sector CAGR ~18% (2020–25).

| Segment | Key metric | Horizon |

|---|---|---|

| SMR | C$3.2bn contracted | to 2030 |

| Transit | C$2–3bn Aecon scope | Ontario Line |

| Utilities | Revenue +18% | FY2024 |

| Telecom | Backlog C$1.2bn | 2024 |

| Industrial | Market share ~25% | 2023–25 |

What is included in the product

Comprehensive BCG review of Aecon’s units with strategic advice for Stars, Cash Cows, Question Marks, and Dogs amid market trends.

One-page Aecon BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Infrastructure Concessions and P3s

Aecon’s infrastructure concessions and P3s, including the Bermuda International Airport concession (20-year term starting 2017), deliver steady, predictable revenues—Aecon reported C$142m in concession-related revenue in FY2024, up 6% year-over-year.

These assets need relatively low capex after handover, yielding high free cash flow; in 2024 concessions produced ~C$78m operating cash, funding riskier growth bets.

Nuclear Maintenance and Refurbishment

The ongoing maintenance of existing CANDU reactors delivers stable, high-margin revenue for Aecon, with Canadian nuclear O&M market growth near 1–2% annually but Aecon holding a dominant share via multi-year master service agreements signed through 2024–2025.

These contracts require little promotional spend and generated roughly CAD 120–150 million annual EBITDA contribution from nuclear services in 2024, providing predictable cash flow.

The segment funds dividends and services debt—nuclear maintenance covered an estimated 25–30% of Aecon’s free cash flow to equity in 2024, acting as the company’s financial bedrock.

Civil Roadbuilding and Bridges

As a mature market leader in Canadian roadwork, Aecon (Aecon Group Inc., ticker ARE.TO) captures recurring government maintenance contracts worth roughly CAD 400–600M annually in road and bridge work, securing predictable revenue.

Growth in traditional asphalt and concrete is low (0–2% CAGR), but Aecon’s scale drives operating margins near 8–10%, yielding strong free cash flow.

These projects need little innovation yet deliver steady volume and cash generation, funding higher-growth bids and capex.

Utilities Maintenance Services

Utilities Maintenance Services delivers steady, high-margin revenue from recurring gas and water repair work, holding a high market share in Canada’s low-growth utility sector; in 2024 Aecon reported ~\$420M in utility services backlog supporting this unit’s cash generation.

Operations run at high efficiency with EBITDA margins near 11–13% in 2023–24, providing free cash flow that funds pilots in smart-pipe tech and sensor-based leak detection.

This classic cash cow relies on multi-decade contracts and long-standing relationships with major Canadian utilities (Enbridge, Fortis, Toronto Water), ensuring predictable cash and low churn.

- Backlog ~\$420M (2024)

- EBITDA margin 11–13% (2023–24)

- Predictable cash flow funds tech pilots

- Long-term contracts with Enbridge, Fortis, Toronto Water

Mining Support and Heavy Industrial

Aecon’s long-standing presence in Canadian mining—notably oil sands and Saskatchewan potash—delivers steady margins: mining & heavy industrial generated ~C$420M revenue in FY2024, with segment EBITDA margins near 8–10%, making it a cash cow despite flat sector growth.

Operational depth and long-term contracts keep Aecon the preferred site services provider, so surplus cash funds green energy projects, including C$75M committed to renewables through 2024–25.

- FY2024 mining revenue ≈ C$420M

- EBITDA margin ~8–10%

- Sustained by long-term contracts

- C$75M allocated to green projects

Aecon’s high‑margin cash cows: concessions, nuclear O&M, roads, utilities, mining

Aecon’s cash cows—concessions/P3s, nuclear O&M, road maintenance, utilities, and mining services—generated steady, high-margin cash in FY2024: concessions revenue C$142m (C$78m operating cash), nuclear EBITDA ~C$120–150m, roadwork revenue C$400–600m, utilities backlog ~$420m (EBITDA 11–13%), mining revenue C$420m (EBITDA 8–10%).

| Segment | FY2024 | EBITDA / Cash |

|---|---|---|

| Concessions/P3s | C$142m rev | C$78m op cash |

| Nuclear O&M | Multi-year MSAs | C$120–150m EBITDA |

| Roads | C$400–600m rev | 8–10% margins |

| Utilities | Backlog ~$420m | 11–13% EBITDA |

| Mining | C$420m rev | 8–10% EBITDA |

What You See Is What You Get

Aecon BCG Matrix

The file you're previewing is the exact Aecon BCG Matrix report you’ll receive after purchase—no watermarks, no demo content, just the final, fully formatted strategic analysis ready for use. This preview mirrors the downloadable document in every detail, crafted with market-backed insights and clear visuals for immediate presentation or decision-making. Upon purchase, the full file is delivered instantly and is editable, printable, and client-ready with no surprises or additional revisions required.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Aecon’s BCG Matrix preview highlights how its business units balance market share and growth — from infrastructure Stars to potential Dogs — offering a snapshot of where capital and strategic focus may be needed. This condensed view signals key strengths and risks but stops short of the granular, quadrant-level data that drives confident decisions. Purchase the full BCG Matrix for a complete breakdown, actionable recommendations, and downloadable Word and Excel formats to present and execute your strategy immediately.

Stars

Energy Transition and Nuclear SMRs

Aecon, via partnerships with Ontario Power Generation, holds a leading SMR pipeline worth ~C$3.2bn in contracted work to 2030, capturing early-mover margins in a sector Canada targets for net-zero by 2050 and net-zero electricity by 2035; SMR market demand is projected at C$20–30bn nationally through 2040.

Major Urban Transit Expansion

Aecon leads multi-billion-dollar transit projects including Toronto’s Ontario Line (budget C$11.6B total; Aecon scope ~C$2–3B) and Montreal REM expansions, key to urban decarbonization and public transit ridership growth of 12% in Toronto 2019–24. These contracts drain cash for equipment and labor but sit in Canada’s fastest-growing infra segment, with light rail market forecast CAGR 6.2% to 2030.

Grid Modernization and Electrification

Aecon’s utilities segment is capturing high-voltage transmission demand driven by EV adoption; Canada’s EV stock rose 55% in 2024, pushing grid upgrade spend—transmission capex in North America hit US$56bn in 2024 (IEA/NEB mix)—and Aecon’s revenues from utilities rose ~18% in FY2024.

Industrial Decarbonization Projects

Aecon is winning ~25% of Canadian heavy-industrial retrofit contracts in 2023–2025, capturing key petrochemical and steel site work as carbon taxes and ESG rules push companies to decarbonize.

Demand grew ~18% CAGR 2020–2025 for industrial decarbonization spending; Aecon’s heavy CAPEX now positions it as preferred contractor for complex green conversions.

- Market share ~25% (2023–2025)

- Sector spend CAGR ~18% (2020–2025)

- Target clients: petrochemical, steel, cement

- Rising compliance costs (carbon tax increases to 2030)

Digital Infrastructure and Connectivity

Aecon’s Digital Infrastructure and Connectivity is a star: the firm is a key contractor in Canada’s 5G and fiber-to-the-home (FTTH) rollout, a market forecasted to grow ~8% CAGR through 2028 with Canadian telecom capex topping CAD 10–12B annually in 2024–25.

High capex needs—tower builds, fiber trenching, equipment—force heavy upfront investment and working-capital cycles; Aecon’s recent telecom backlog of CAD ~1.2B (2024) supports rapid deployment schedules.

Connectivity is essential to GDP growth, so this segment earns premium returns despite execution risk from tech shifts and permitting delays.

- Market growth ~8% CAGR to 2028

- Canadian telco capex CAD 10–12B (2024–25)

- Aecon telecom backlog ~CAD 1.2B (2024)

- High upfront capex, rapid deployment required

Aecon’s C$11.6bn Opportunity: SMR, Transit, Utilities, Telecom & Heavy-Industrial Growth

Aecon’s Stars: SMR pipeline C$3.2bn contracted to 2030; transit scope ~C$2–3bn on Ontario Line (total C$11.6bn); utilities revenue +18% FY2024 amid 55% EV stock rise (2024); telecom backlog C$1.2bn with telco capex C$10–12bn (2024–25); heavy-industrial market share ~25% (2023–25), sector CAGR ~18% (2020–25).

| Segment | Key metric | Horizon |

|---|---|---|

| SMR | C$3.2bn contracted | to 2030 |

| Transit | C$2–3bn Aecon scope | Ontario Line |

| Utilities | Revenue +18% | FY2024 |

| Telecom | Backlog C$1.2bn | 2024 |

| Industrial | Market share ~25% | 2023–25 |

What is included in the product

Comprehensive BCG review of Aecon’s units with strategic advice for Stars, Cash Cows, Question Marks, and Dogs amid market trends.

One-page Aecon BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Infrastructure Concessions and P3s

Aecon’s infrastructure concessions and P3s, including the Bermuda International Airport concession (20-year term starting 2017), deliver steady, predictable revenues—Aecon reported C$142m in concession-related revenue in FY2024, up 6% year-over-year.

These assets need relatively low capex after handover, yielding high free cash flow; in 2024 concessions produced ~C$78m operating cash, funding riskier growth bets.

Nuclear Maintenance and Refurbishment

The ongoing maintenance of existing CANDU reactors delivers stable, high-margin revenue for Aecon, with Canadian nuclear O&M market growth near 1–2% annually but Aecon holding a dominant share via multi-year master service agreements signed through 2024–2025.

These contracts require little promotional spend and generated roughly CAD 120–150 million annual EBITDA contribution from nuclear services in 2024, providing predictable cash flow.

The segment funds dividends and services debt—nuclear maintenance covered an estimated 25–30% of Aecon’s free cash flow to equity in 2024, acting as the company’s financial bedrock.

Civil Roadbuilding and Bridges

As a mature market leader in Canadian roadwork, Aecon (Aecon Group Inc., ticker ARE.TO) captures recurring government maintenance contracts worth roughly CAD 400–600M annually in road and bridge work, securing predictable revenue.

Growth in traditional asphalt and concrete is low (0–2% CAGR), but Aecon’s scale drives operating margins near 8–10%, yielding strong free cash flow.

These projects need little innovation yet deliver steady volume and cash generation, funding higher-growth bids and capex.

Utilities Maintenance Services

Utilities Maintenance Services delivers steady, high-margin revenue from recurring gas and water repair work, holding a high market share in Canada’s low-growth utility sector; in 2024 Aecon reported ~\$420M in utility services backlog supporting this unit’s cash generation.

Operations run at high efficiency with EBITDA margins near 11–13% in 2023–24, providing free cash flow that funds pilots in smart-pipe tech and sensor-based leak detection.

This classic cash cow relies on multi-decade contracts and long-standing relationships with major Canadian utilities (Enbridge, Fortis, Toronto Water), ensuring predictable cash and low churn.

- Backlog ~\$420M (2024)

- EBITDA margin 11–13% (2023–24)

- Predictable cash flow funds tech pilots

- Long-term contracts with Enbridge, Fortis, Toronto Water

Mining Support and Heavy Industrial

Aecon’s long-standing presence in Canadian mining—notably oil sands and Saskatchewan potash—delivers steady margins: mining & heavy industrial generated ~C$420M revenue in FY2024, with segment EBITDA margins near 8–10%, making it a cash cow despite flat sector growth.

Operational depth and long-term contracts keep Aecon the preferred site services provider, so surplus cash funds green energy projects, including C$75M committed to renewables through 2024–25.

- FY2024 mining revenue ≈ C$420M

- EBITDA margin ~8–10%

- Sustained by long-term contracts

- C$75M allocated to green projects

Aecon’s high‑margin cash cows: concessions, nuclear O&M, roads, utilities, mining

Aecon’s cash cows—concessions/P3s, nuclear O&M, road maintenance, utilities, and mining services—generated steady, high-margin cash in FY2024: concessions revenue C$142m (C$78m operating cash), nuclear EBITDA ~C$120–150m, roadwork revenue C$400–600m, utilities backlog ~$420m (EBITDA 11–13%), mining revenue C$420m (EBITDA 8–10%).

| Segment | FY2024 | EBITDA / Cash |

|---|---|---|

| Concessions/P3s | C$142m rev | C$78m op cash |

| Nuclear O&M | Multi-year MSAs | C$120–150m EBITDA |

| Roads | C$400–600m rev | 8–10% margins |

| Utilities | Backlog ~$420m | 11–13% EBITDA |

| Mining | C$420m rev | 8–10% EBITDA |

What You See Is What You Get

Aecon BCG Matrix

The file you're previewing is the exact Aecon BCG Matrix report you’ll receive after purchase—no watermarks, no demo content, just the final, fully formatted strategic analysis ready for use. This preview mirrors the downloadable document in every detail, crafted with market-backed insights and clear visuals for immediate presentation or decision-making. Upon purchase, the full file is delivered instantly and is editable, printable, and client-ready with no surprises or additional revisions required.