Aemetis PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Uncover how regulatory shifts, feedstock economics, and clean-tech advances are reshaping Aemetis’s growth trajectory and risk profile—our targeted PESTLE highlights the critical external forces investors and strategists must monitor. Purchase the full PESTLE to access actionable insights, scenario-driven implications, and ready-to-use slides for decision-making.

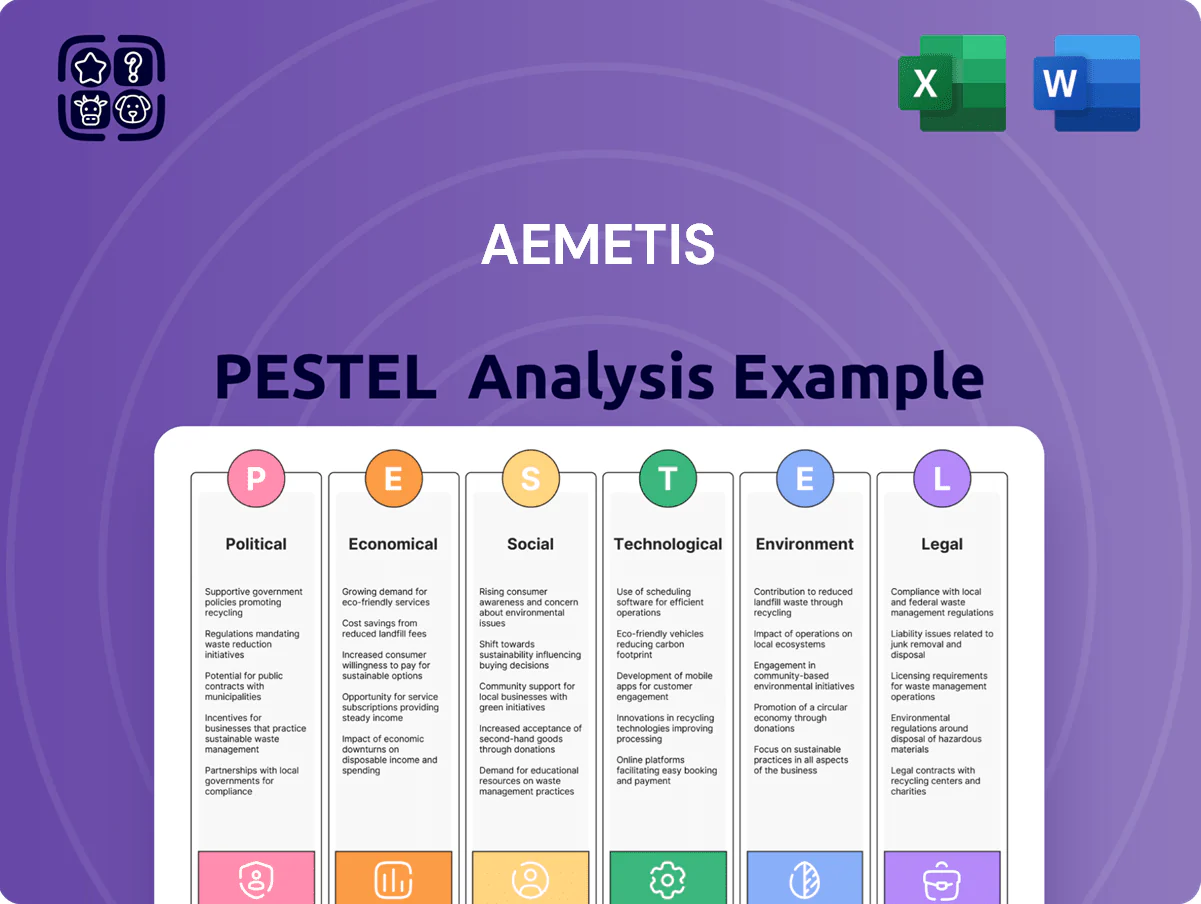

Political factors

Inflation Reduction Act Stability

The 2022 Inflation Reduction Act remains central to Aemetis’s financial planning through 2025, providing production tax credits up to $1.75/gal for Sustainable Aviation Fuel and similar credits for Renewable Diesel that underpin projected revenue streams. These federal incentives help offset Aemetis’s capital intensity—capital expenditures of $220m–$300m estimated for 2023–2025—improving project IRRs by an estimated 200–400 basis points. Management closely monitors Washington: a 2024 midterm-driven policy shift could alter subsidy duration or rates, directly impacting cash flow visibility and valuation.

California Low Carbon Fuel Standard

As a California-based operator, Aemetis benefits from the Low Carbon Fuel Standard where LCFS credit prices averaged about $120/metric ton CO2e in 2024, boosting revenue for its renewable fuels and biomethane projects tied to declining carbon intensity targets through 2030.

State rulemakings to lower carbon intensity by ~20% from 2020 levels by 2030 increase demand for Aemetis’s low‑carbon outputs, supporting project economics and expected LCFS credit generation of several tens of thousands of credits annually at current production scales.

Political pressure over fuel costs has driven short-term LCFS price swings of ±20–30% in 2023–2024, creating credit pricing volatility that can materially affect Aemetis’s quarterly cash flows and valuation sensitivity to LCFS revenue assumptions.

India Biofuel Policy Alignment

The Indian National Policy on Biofuels (2018, updated targets to 2025) supports Aemetis’s Universal Biofuels in Kakinada by enabling feedstock procurement and incentives; India aims for 20% ethanol blending and increased biodiesel mandates for transport/shipping, supporting a predictable domestic market worth an estimated $3–5 billion annually in South Asia; stronger US‑India ties have enabled technology transfer agreements and potential access to $100–200 million in bilateral clean‑energy financing.

Federal Renewable Fuel Standard Mandates

The EPA's Renewable Fuel Standard RVOs remain the primary political lever for Aemetis, with the 2024 RVO setting total conventional ethanol volumes at 15.0 billion gallons and advanced biofuel targets influencing Aemetis' RNG and cellulosic strategies.

Small refinery exemptions granted at 271 petitions in 2023 reduced obligated volumes, creating volatility in demand for Aemetis' ethanol; potential e-RIN inclusion for renewable electricity could raise RNG demand by an estimated 0.2–0.5 billion gallon-equivalent by 2025.

Oil and agriculture lobbying—Oil states spent over $300 million and farm groups $120 million on related lobbying in 2023—drive a political tug-of-war that shapes annual production targets and pricing for Aemetis' fuel outputs.

- EPA RVOs: 15.0 B gal conventional ethanol (2024)

- Small refinery exemptions: 271 petitions (2023)

- Lobbying spend: Oil >$300M, ag ~$120M (2023)

- e-RINs could add 0.2–0.5 B gal-e demand by 2025

International Trade and Tariff Barriers

Trade policies on feedstock and biofuel exports are pivotal for Aemetis’s supply chain; in 2024 EU biodiesel demand growth and US import tariffs on Asian used cooking oil (up to 8–12%) altered feedstock flows, affecting margins.

Tariffs on exports to Europe or duties on imports from Asia can shift competitiveness rapidly; securing political support across jurisdictions helps Aemetis mitigate protectionist risk while scaling internationally.

- 2024: EU biodiesel imports rose ~6% y/y; US tariffs 8–12% on some Asian UCO

Aemetis Boosted by IRA & CA LCFS; RVOs, SREs, Tariffs Drive Feedstock Volatility

Federal incentives (IRA credits up to $1.75/gal) and California LCFS (~$120/t CO2e in 2024) materially support Aemetis cash flows; 2024 RVOs set conventional ethanol at 15.0 B gal while 271 SRE petitions in 2023 and ±20–30% LCFS price swings create volatility; India biofuels targets and $100–200M bilateral financing aid Kakinada; 2024 US tariffs (8–12%) on Asian UCO and EU biodiesel +6% y/y affect feedstock margins.

| Metric | 2023–24 Value |

|---|---|

| IRA SAF/RD credit | $1.75/gal |

| LCFS price | $120/t CO2e |

| RVO conventional | 15.0 B gal (2024) |

| SRE petitions | 271 (2023) |

| US tariffs on UCO | 8–12% |

What is included in the product

Explores how macro-environmental factors uniquely affect Aemetis across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region- and industry-specific insights to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary for Aemetis that’s visually segmented by category, easing meeting references and slide inclusion while allowing quick notes for region- or business-specific context.

Economic factors

Interest Rate Environment and Financing

The cost of capital is critical for Aemetis as it advances the $1.5–$2.0 billion Riverbank jet fuel plant; servicing roughly $300–$400 million of existing debt through 2024–25 depressed net margins and slowed construction pacing.

Volatile Feedstock Commodity Pricing

Profitability at Aemetis is highly sensitive to agricultural waste, corn, and vegetable oil costs; US corn futures rose ~18% in 2024, pressuring margins when renewable fuel prices lag. Global grain volatility from extreme weather and geopolitical tensions—2023–24 crop shocks cut yields in key regions by up to 10%—can compress spreads if fuel prices don’t follow. Hedging and moves to non-food feedstocks (e.g., waste oils, cellulosic) are critical economic risk mitigants.

LCFS and RIN Credit Market Value

Aemetis depends heavily on environmental-credit revenues—LCFS and RINs made up an estimated 40–60% of per-gallon realized value in 2024, boosting margins beyond diesel spot prices.

LCFS credits averaged about $160/credit in California in 2024 while D3 RIN prices traded near $0.55–0.70/gal, so supply-demand swings directly shift Aemetis’s effective fuel revenue.

In 2024–2025, growing renewable diesel capacity created periodic LCFS/RIN price drops—credit crashes of 20–40% in months—highlighting the need for diversified products and feedstocks to hedge earnings volatility.

Energy Market Competition

The 2024 average Brent crude price near $86/barrel and US natural gas around $3.50/MMBtu raise demand for Aemetis renewable fuels as fleets and airlines seek cost-stable alternatives; higher fossil prices improve biofuel margins and ROI.

Sustained low oil (2015–2020 lows ~$30–$40) showed unsubsidized biofuels struggle versus petrofuels, highlighting Aemetis sensitivity to market oil/gas swings and policy support.

- Brent ~$86/barrel (2024)

- US natural gas ~$3.50/MMBtu (2024)

- High fossil prices boost renewable demand and margins

- Low prices reduce competitiveness without subsidies

Labor Market and Construction Costs

Expanding Aemetis production requires skilled engineers and inputs like steel and anaerobic digesters, with 2024 US construction material costs up ~8% YoY and specialty equipment price inflation near 6%, squeezing margins.

Green tech growth tightened labor markets: US clean energy job openings rose 12% in 2024, lifting engineering wages ~7–10%, increasing project OPEX and capital staffing costs.

Controlling these cost drivers is critical to safeguarding projected IRRs on new biogas and RNG projects, where a 5–10% rise in build costs can cut IRR by several hundred basis points.

- 2024 construction material inflation ~8% YoY

- Specialty equipment inflation ~6%

- Clean energy job openings +12% in 2024

- Engineering wage pressure +7–10%

- 5–10% build cost rise can reduce IRR by hundreds of bps

Macro headwinds squeeze Aemetis margins: higher energy, feedstock, LCFS/RINs and build costs

Macro economics drive Aemetis margins: 2024 Brent ~$86/bbl, US natural gas ~$3.50/MMBtu; LCFS ~$160/credit and D3 RINs $0.55–0.70/gal (40–60% of realized value); 2024 corn futures +18% YoY; construction materials +8% and specialty equipment +6%; clean-energy job openings +12% with engineering wages +7–10%, risking IRR erosion from 5–10% build-cost increases.

| Metric | 2024 |

|---|---|

| Brent | $86/bbl |

| NatGas | $3.50/MMBtu |

| LCFS | $160/credit |

| D3 RIN | $0.55–0.70/gal |

| Corn futures | +18% YoY |

| Materials | +8% |

Full Version Awaits

Aemetis PESTLE Analysis

The preview shown here is the exact Aemetis PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Uncover how regulatory shifts, feedstock economics, and clean-tech advances are reshaping Aemetis’s growth trajectory and risk profile—our targeted PESTLE highlights the critical external forces investors and strategists must monitor. Purchase the full PESTLE to access actionable insights, scenario-driven implications, and ready-to-use slides for decision-making.

Political factors

Inflation Reduction Act Stability

The 2022 Inflation Reduction Act remains central to Aemetis’s financial planning through 2025, providing production tax credits up to $1.75/gal for Sustainable Aviation Fuel and similar credits for Renewable Diesel that underpin projected revenue streams. These federal incentives help offset Aemetis’s capital intensity—capital expenditures of $220m–$300m estimated for 2023–2025—improving project IRRs by an estimated 200–400 basis points. Management closely monitors Washington: a 2024 midterm-driven policy shift could alter subsidy duration or rates, directly impacting cash flow visibility and valuation.

California Low Carbon Fuel Standard

As a California-based operator, Aemetis benefits from the Low Carbon Fuel Standard where LCFS credit prices averaged about $120/metric ton CO2e in 2024, boosting revenue for its renewable fuels and biomethane projects tied to declining carbon intensity targets through 2030.

State rulemakings to lower carbon intensity by ~20% from 2020 levels by 2030 increase demand for Aemetis’s low‑carbon outputs, supporting project economics and expected LCFS credit generation of several tens of thousands of credits annually at current production scales.

Political pressure over fuel costs has driven short-term LCFS price swings of ±20–30% in 2023–2024, creating credit pricing volatility that can materially affect Aemetis’s quarterly cash flows and valuation sensitivity to LCFS revenue assumptions.

India Biofuel Policy Alignment

The Indian National Policy on Biofuels (2018, updated targets to 2025) supports Aemetis’s Universal Biofuels in Kakinada by enabling feedstock procurement and incentives; India aims for 20% ethanol blending and increased biodiesel mandates for transport/shipping, supporting a predictable domestic market worth an estimated $3–5 billion annually in South Asia; stronger US‑India ties have enabled technology transfer agreements and potential access to $100–200 million in bilateral clean‑energy financing.

Federal Renewable Fuel Standard Mandates

The EPA's Renewable Fuel Standard RVOs remain the primary political lever for Aemetis, with the 2024 RVO setting total conventional ethanol volumes at 15.0 billion gallons and advanced biofuel targets influencing Aemetis' RNG and cellulosic strategies.

Small refinery exemptions granted at 271 petitions in 2023 reduced obligated volumes, creating volatility in demand for Aemetis' ethanol; potential e-RIN inclusion for renewable electricity could raise RNG demand by an estimated 0.2–0.5 billion gallon-equivalent by 2025.

Oil and agriculture lobbying—Oil states spent over $300 million and farm groups $120 million on related lobbying in 2023—drive a political tug-of-war that shapes annual production targets and pricing for Aemetis' fuel outputs.

- EPA RVOs: 15.0 B gal conventional ethanol (2024)

- Small refinery exemptions: 271 petitions (2023)

- Lobbying spend: Oil >$300M, ag ~$120M (2023)

- e-RINs could add 0.2–0.5 B gal-e demand by 2025

International Trade and Tariff Barriers

Trade policies on feedstock and biofuel exports are pivotal for Aemetis’s supply chain; in 2024 EU biodiesel demand growth and US import tariffs on Asian used cooking oil (up to 8–12%) altered feedstock flows, affecting margins.

Tariffs on exports to Europe or duties on imports from Asia can shift competitiveness rapidly; securing political support across jurisdictions helps Aemetis mitigate protectionist risk while scaling internationally.

- 2024: EU biodiesel imports rose ~6% y/y; US tariffs 8–12% on some Asian UCO

Aemetis Boosted by IRA & CA LCFS; RVOs, SREs, Tariffs Drive Feedstock Volatility

Federal incentives (IRA credits up to $1.75/gal) and California LCFS (~$120/t CO2e in 2024) materially support Aemetis cash flows; 2024 RVOs set conventional ethanol at 15.0 B gal while 271 SRE petitions in 2023 and ±20–30% LCFS price swings create volatility; India biofuels targets and $100–200M bilateral financing aid Kakinada; 2024 US tariffs (8–12%) on Asian UCO and EU biodiesel +6% y/y affect feedstock margins.

| Metric | 2023–24 Value |

|---|---|

| IRA SAF/RD credit | $1.75/gal |

| LCFS price | $120/t CO2e |

| RVO conventional | 15.0 B gal (2024) |

| SRE petitions | 271 (2023) |

| US tariffs on UCO | 8–12% |

What is included in the product

Explores how macro-environmental factors uniquely affect Aemetis across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region- and industry-specific insights to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE summary for Aemetis that’s visually segmented by category, easing meeting references and slide inclusion while allowing quick notes for region- or business-specific context.

Economic factors

Interest Rate Environment and Financing

The cost of capital is critical for Aemetis as it advances the $1.5–$2.0 billion Riverbank jet fuel plant; servicing roughly $300–$400 million of existing debt through 2024–25 depressed net margins and slowed construction pacing.

Volatile Feedstock Commodity Pricing

Profitability at Aemetis is highly sensitive to agricultural waste, corn, and vegetable oil costs; US corn futures rose ~18% in 2024, pressuring margins when renewable fuel prices lag. Global grain volatility from extreme weather and geopolitical tensions—2023–24 crop shocks cut yields in key regions by up to 10%—can compress spreads if fuel prices don’t follow. Hedging and moves to non-food feedstocks (e.g., waste oils, cellulosic) are critical economic risk mitigants.

LCFS and RIN Credit Market Value

Aemetis depends heavily on environmental-credit revenues—LCFS and RINs made up an estimated 40–60% of per-gallon realized value in 2024, boosting margins beyond diesel spot prices.

LCFS credits averaged about $160/credit in California in 2024 while D3 RIN prices traded near $0.55–0.70/gal, so supply-demand swings directly shift Aemetis’s effective fuel revenue.

In 2024–2025, growing renewable diesel capacity created periodic LCFS/RIN price drops—credit crashes of 20–40% in months—highlighting the need for diversified products and feedstocks to hedge earnings volatility.

Energy Market Competition

The 2024 average Brent crude price near $86/barrel and US natural gas around $3.50/MMBtu raise demand for Aemetis renewable fuels as fleets and airlines seek cost-stable alternatives; higher fossil prices improve biofuel margins and ROI.

Sustained low oil (2015–2020 lows ~$30–$40) showed unsubsidized biofuels struggle versus petrofuels, highlighting Aemetis sensitivity to market oil/gas swings and policy support.

- Brent ~$86/barrel (2024)

- US natural gas ~$3.50/MMBtu (2024)

- High fossil prices boost renewable demand and margins

- Low prices reduce competitiveness without subsidies

Labor Market and Construction Costs

Expanding Aemetis production requires skilled engineers and inputs like steel and anaerobic digesters, with 2024 US construction material costs up ~8% YoY and specialty equipment price inflation near 6%, squeezing margins.

Green tech growth tightened labor markets: US clean energy job openings rose 12% in 2024, lifting engineering wages ~7–10%, increasing project OPEX and capital staffing costs.

Controlling these cost drivers is critical to safeguarding projected IRRs on new biogas and RNG projects, where a 5–10% rise in build costs can cut IRR by several hundred basis points.

- 2024 construction material inflation ~8% YoY

- Specialty equipment inflation ~6%

- Clean energy job openings +12% in 2024

- Engineering wage pressure +7–10%

- 5–10% build cost rise can reduce IRR by hundreds of bps

Macro headwinds squeeze Aemetis margins: higher energy, feedstock, LCFS/RINs and build costs

Macro economics drive Aemetis margins: 2024 Brent ~$86/bbl, US natural gas ~$3.50/MMBtu; LCFS ~$160/credit and D3 RINs $0.55–0.70/gal (40–60% of realized value); 2024 corn futures +18% YoY; construction materials +8% and specialty equipment +6%; clean-energy job openings +12% with engineering wages +7–10%, risking IRR erosion from 5–10% build-cost increases.

| Metric | 2024 |

|---|---|

| Brent | $86/bbl |

| NatGas | $3.50/MMBtu |

| LCFS | $160/credit |

| D3 RIN | $0.55–0.70/gal |

| Corn futures | +18% YoY |

| Materials | +8% |

Full Version Awaits

Aemetis PESTLE Analysis

The preview shown here is the exact Aemetis PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.