AEON Financial Service Business Model Canvas

AEON Financial Service Business Model Canvas: Customer-Centric Loans & Fintech Insights

Unlock the full strategic blueprint behind AEON Financial Service’s business model — this concise Business Model Canvas reveals how the firm creates customer-centric loan products, leverages retail partnerships and fintech integrations, and monetizes credit services while managing credit risk; ideal for investors, consultants, and founders seeking a ready-to-use, downloadable Word/Excel template to benchmark strategy and accelerate decision-making.

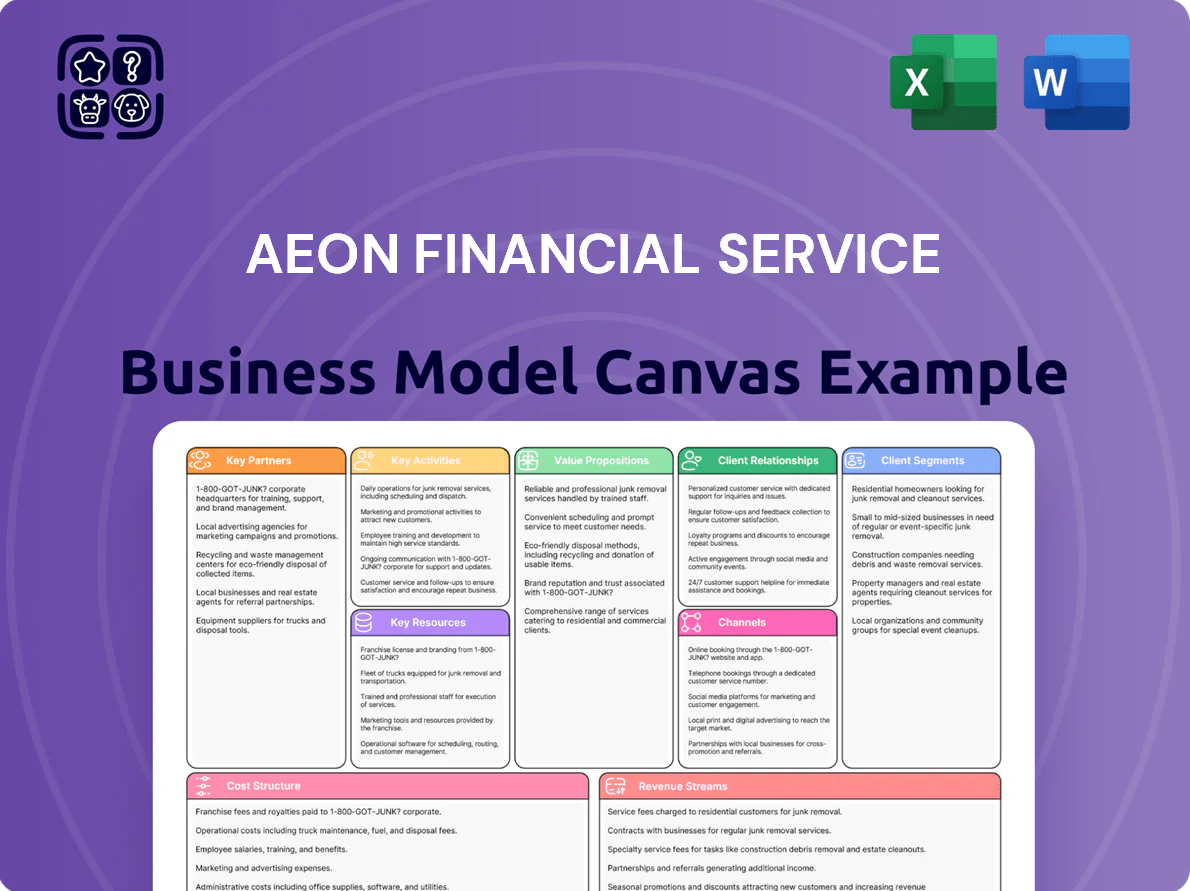

Partnerships

AEON Group Retail Entities

The primary partnership embeds AEON Financial Services within AEON Co., Ltd.’s retail network—including GMS and supermarkets—giving direct access to ~150 million annual mall visits across Japan and Southeast Asia (AEON Group 2024 footfall data) and enabling in-mall service counters for account opening and loans. This deep integration drives low-cost customer acquisition (estimated CAC reduction of 25% vs. digital-only channels) and steady lead flow from high-frequency retail shoppers.

Global Payment Networks

AEON Financial partners with Visa, Mastercard, and JCB to enable global acceptance and clearing; in 2024 these schemes handled over $11.5 trillion in card payments (Visa FY2024 network volume $11.6T), ensuring AEON cards work in 200+ countries and supporting cross-border settlement, which preserves product utility and competitive reach for AEON’s credit portfolio.

Regional Financial Institutions

AEON Financial Service partners with local banks and regulators across Asia to ensure compliance and operational efficiency, securing over JPY 120 billion (≈USD 900M) in local-currency funding in 2024 and rolling out market-specific lending like Vietnam microloans and Thailand auto-finance. These alliances lower cross-border regulatory risk and raised regional loan penetration by 8% y/y in 2024, boosting local market share and collection efficiency.

Fintech and Technology Providers

AEON partners with fintechs and tech firms to roll out mobile payments and AI credit scoring, cutting loan decision time by up to 70% and raising digital loan originations (2024) to ~38% of total book.

These partners supply cloud backend and MFA cybersecurity tools, lowering fraud losses by ~22% year-over-year and helping AEON compete with digital challengers.

- AI credit scoring: faster approvals, 38% digital originations (2024)

- Mobile payments: expanded wallet reach, 70% faster decisions

- Cybersecurity: MFA/cloud tools, 22% cut in fraud losses (YoY)

Insurance Underwriters and Asset Managers

AEON partners with third-party insurance underwriters and asset managers to offer a wider product shelf, acting as intermediary so AEON provides wealth management and protection without taking on full actuarial risk; as of 2025 AEON’s alliances cover products managing ~JPY 120 billion in AUM and insure policies with ~¥18 billion GWP annually.

- Expanded product range via partners

- Intermediary reduces AEON’s actuarial exposure

- ~JPY 120bn assets under management via partners (2025)

- ~¥18bn gross written premium through partner policies (2025)

AEON scales cross‑border payments & products via 150M visits, JPY120bn funding, 38% digital

AEON leverages AEON Co. retail footfall (~150M visits 2024), card networks (Visa FY2024 $11.6T), JPY120bn local funding (2024), 38% digital originations (2024), 22% fraud cut (YoY) and partner AUM ¥120bn/GWP ¥18bn (2025) to lower CAC, scale cross-border acceptance, speed approvals, and expand product shelf via insurers/asset managers.

| Metric | Value |

|---|---|

| Retail visits | ~150M (2024) |

| Visa volume | $11.6T (FY2024) |

| Local funding | JPY120bn (2024) |

| Digital originations | 38% (2024) |

| Fraud reduction | 22% YoY |

| Partner AUM | ¥120bn (2025) |

| Partner GWP | ¥18bn (2025) |

What is included in the product

A concise, pre-written Business Model Canvas for AEON Financial Service detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and governance aligned with real-world operations and strategic priorities.

Quickly identify AEON Financial Service’s customer pain relievers and value propositions in a one-page, editable Business Model Canvas designed to streamline stakeholder alignment and speed decision-making.

Activities

Credit Card Issuance and Management

Retail Banking Operations

AEON Financial Service, via its banking subsidiaries, runs deposit accounts, personal loans, and housing loans—servicing ~6.2 million customers as of 2025 and holding CET1-equivalent capital ratios above local minimums; these lines demand strict regulatory compliance and liquidity management (LCR typically >100%). Efficient ATM networks and online banking, which handle millions of monthly logins (≈12M/month in 2024), are vital to daily customer engagement and retention.

Digital Platform Development

A significant share of AEON Financial’s activity focuses on upgrading the mobile app and integrated digital wallets—supporting 4.2 million active users as of Dec 2025—and building intuitive account-management UIs plus POS-linked wallets. Projects link loyalty points to payments (reducing checkout time by ~18% in 2024 pilots) and prioritize digital innovation to cut customer friction and lift mobile transaction share above 62% of total volume.

Marketing and Loyalty Program Integration

AEON Financial uses AEON Reward Points to drive cross-usage: 2024 campaigns tied to seasonal retail events lifted card transaction volume 11% and loan applications 7% year-over-year, with rewards-funded cashback and bonus points.

Advanced analytics segments 3.2M active cardholders to deliver personalized offers; targeted campaigns show 18% conversion vs 6% for generic promos.

- 11% rise in card transactions (2024)

- 7% increase in loan apps (2024)

- 3.2M active cardholders segmented

- 18% conversion for personalized offers

- 6% conversion for generic campaigns

Risk Management and Compliance

Continuous monitoring of global and Thai regulations keeps AEON Financial Service's licenses valid and reduces fines; in 2024 banks faced $22.8B in regulatory penalties globally, so proactive oversight matters.

We manage interest-rate exposure and credit defaults across ~5 million customers, enforce data privacy (GDPR/PDPA) and maintain compliance frameworks to preserve regulator and consumer trust.

- Monitor regs daily; update policies quarterly

- Hedge rate risk; stress-test monthly

- Limit NPLs to <3% via credit controls

- Encrypt data for 5M+ customers; PDPA/GDPR aligned

AEON Financial: 6.2M customers, ¥250bn receivables, 62% mobile share, 1.8% delinquency

| Metric | Value |

|---|---|

| Customers (2025) | 6.2M |

| Card receivables (FY2024) | ¥250bn |

| App users (Dec 2025) | 4.2M |

| Mobile txn share | 62% |

| Installment share | 38% |

| Delinquency | 1.8% |

| Personalized conv. | 18% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual AEON Financial Service Business Model Canvas you will receive after purchase—not a mockup or sample; upon completing your order you’ll get this same professional, editable file in full, formatted for immediate use and presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

AEON Financial Service Business Model Canvas: Customer-Centric Loans & Fintech Insights

Unlock the full strategic blueprint behind AEON Financial Service’s business model — this concise Business Model Canvas reveals how the firm creates customer-centric loan products, leverages retail partnerships and fintech integrations, and monetizes credit services while managing credit risk; ideal for investors, consultants, and founders seeking a ready-to-use, downloadable Word/Excel template to benchmark strategy and accelerate decision-making.

Partnerships

AEON Group Retail Entities

The primary partnership embeds AEON Financial Services within AEON Co., Ltd.’s retail network—including GMS and supermarkets—giving direct access to ~150 million annual mall visits across Japan and Southeast Asia (AEON Group 2024 footfall data) and enabling in-mall service counters for account opening and loans. This deep integration drives low-cost customer acquisition (estimated CAC reduction of 25% vs. digital-only channels) and steady lead flow from high-frequency retail shoppers.

Global Payment Networks

AEON Financial partners with Visa, Mastercard, and JCB to enable global acceptance and clearing; in 2024 these schemes handled over $11.5 trillion in card payments (Visa FY2024 network volume $11.6T), ensuring AEON cards work in 200+ countries and supporting cross-border settlement, which preserves product utility and competitive reach for AEON’s credit portfolio.

Regional Financial Institutions

AEON Financial Service partners with local banks and regulators across Asia to ensure compliance and operational efficiency, securing over JPY 120 billion (≈USD 900M) in local-currency funding in 2024 and rolling out market-specific lending like Vietnam microloans and Thailand auto-finance. These alliances lower cross-border regulatory risk and raised regional loan penetration by 8% y/y in 2024, boosting local market share and collection efficiency.

Fintech and Technology Providers

AEON partners with fintechs and tech firms to roll out mobile payments and AI credit scoring, cutting loan decision time by up to 70% and raising digital loan originations (2024) to ~38% of total book.

These partners supply cloud backend and MFA cybersecurity tools, lowering fraud losses by ~22% year-over-year and helping AEON compete with digital challengers.

- AI credit scoring: faster approvals, 38% digital originations (2024)

- Mobile payments: expanded wallet reach, 70% faster decisions

- Cybersecurity: MFA/cloud tools, 22% cut in fraud losses (YoY)

Insurance Underwriters and Asset Managers

AEON partners with third-party insurance underwriters and asset managers to offer a wider product shelf, acting as intermediary so AEON provides wealth management and protection without taking on full actuarial risk; as of 2025 AEON’s alliances cover products managing ~JPY 120 billion in AUM and insure policies with ~¥18 billion GWP annually.

- Expanded product range via partners

- Intermediary reduces AEON’s actuarial exposure

- ~JPY 120bn assets under management via partners (2025)

- ~¥18bn gross written premium through partner policies (2025)

AEON scales cross‑border payments & products via 150M visits, JPY120bn funding, 38% digital

AEON leverages AEON Co. retail footfall (~150M visits 2024), card networks (Visa FY2024 $11.6T), JPY120bn local funding (2024), 38% digital originations (2024), 22% fraud cut (YoY) and partner AUM ¥120bn/GWP ¥18bn (2025) to lower CAC, scale cross-border acceptance, speed approvals, and expand product shelf via insurers/asset managers.

| Metric | Value |

|---|---|

| Retail visits | ~150M (2024) |

| Visa volume | $11.6T (FY2024) |

| Local funding | JPY120bn (2024) |

| Digital originations | 38% (2024) |

| Fraud reduction | 22% YoY |

| Partner AUM | ¥120bn (2025) |

| Partner GWP | ¥18bn (2025) |

What is included in the product

A concise, pre-written Business Model Canvas for AEON Financial Service detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and governance aligned with real-world operations and strategic priorities.

Quickly identify AEON Financial Service’s customer pain relievers and value propositions in a one-page, editable Business Model Canvas designed to streamline stakeholder alignment and speed decision-making.

Activities

Credit Card Issuance and Management

Retail Banking Operations

AEON Financial Service, via its banking subsidiaries, runs deposit accounts, personal loans, and housing loans—servicing ~6.2 million customers as of 2025 and holding CET1-equivalent capital ratios above local minimums; these lines demand strict regulatory compliance and liquidity management (LCR typically >100%). Efficient ATM networks and online banking, which handle millions of monthly logins (≈12M/month in 2024), are vital to daily customer engagement and retention.

Digital Platform Development

A significant share of AEON Financial’s activity focuses on upgrading the mobile app and integrated digital wallets—supporting 4.2 million active users as of Dec 2025—and building intuitive account-management UIs plus POS-linked wallets. Projects link loyalty points to payments (reducing checkout time by ~18% in 2024 pilots) and prioritize digital innovation to cut customer friction and lift mobile transaction share above 62% of total volume.

Marketing and Loyalty Program Integration

AEON Financial uses AEON Reward Points to drive cross-usage: 2024 campaigns tied to seasonal retail events lifted card transaction volume 11% and loan applications 7% year-over-year, with rewards-funded cashback and bonus points.

Advanced analytics segments 3.2M active cardholders to deliver personalized offers; targeted campaigns show 18% conversion vs 6% for generic promos.

- 11% rise in card transactions (2024)

- 7% increase in loan apps (2024)

- 3.2M active cardholders segmented

- 18% conversion for personalized offers

- 6% conversion for generic campaigns

Risk Management and Compliance

Continuous monitoring of global and Thai regulations keeps AEON Financial Service's licenses valid and reduces fines; in 2024 banks faced $22.8B in regulatory penalties globally, so proactive oversight matters.

We manage interest-rate exposure and credit defaults across ~5 million customers, enforce data privacy (GDPR/PDPA) and maintain compliance frameworks to preserve regulator and consumer trust.

- Monitor regs daily; update policies quarterly

- Hedge rate risk; stress-test monthly

- Limit NPLs to <3% via credit controls

- Encrypt data for 5M+ customers; PDPA/GDPR aligned

AEON Financial: 6.2M customers, ¥250bn receivables, 62% mobile share, 1.8% delinquency

| Metric | Value |

|---|---|

| Customers (2025) | 6.2M |

| Card receivables (FY2024) | ¥250bn |

| App users (Dec 2025) | 4.2M |

| Mobile txn share | 62% |

| Installment share | 38% |

| Delinquency | 1.8% |

| Personalized conv. | 18% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual AEON Financial Service Business Model Canvas you will receive after purchase—not a mockup or sample; upon completing your order you’ll get this same professional, editable file in full, formatted for immediate use and presentation.