Afarak Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

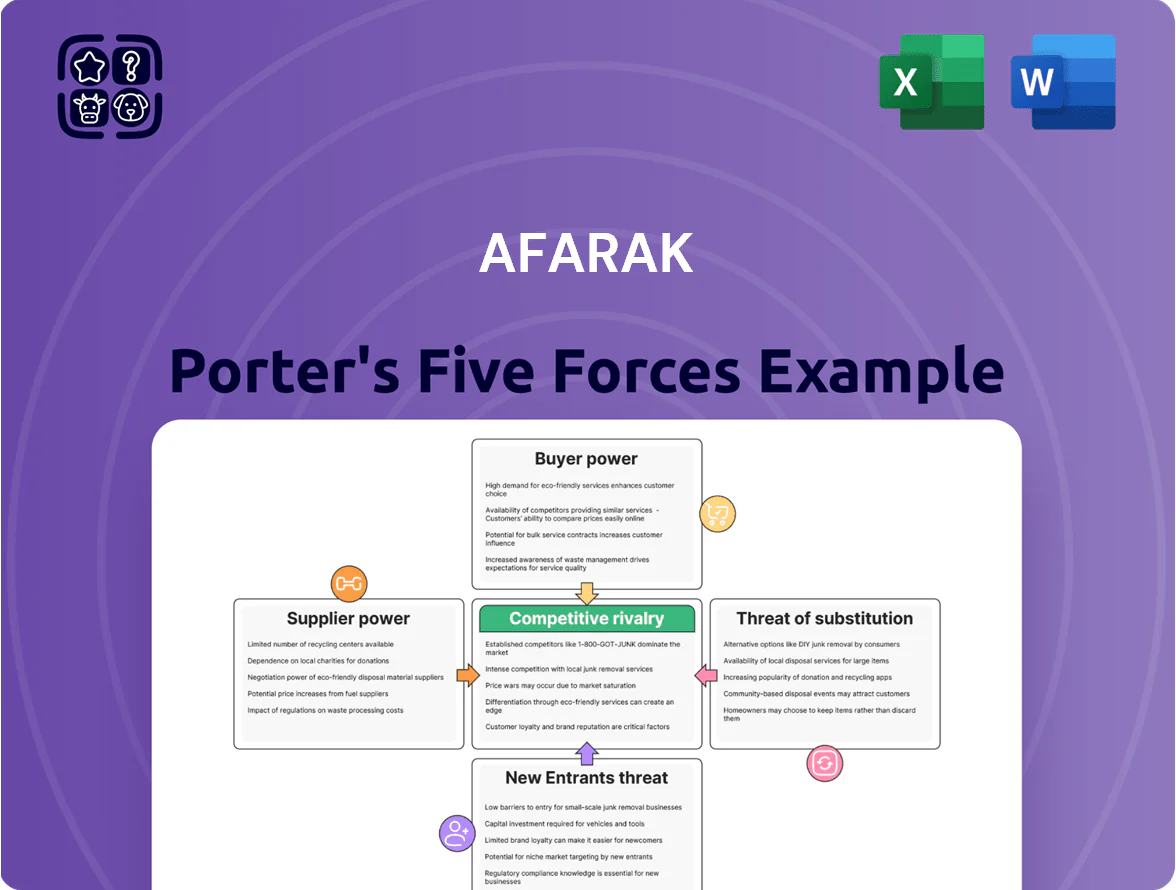

Afarak faces moderate supplier power and concentrated steel markets, while buyer bargaining and substitute threats vary by product segment, creating uneven pricing leverage across its operations.

Competitive rivalry is intense among regional ferroalloy producers, but barriers to entry and Afarak’s niche capabilities offer some defensive advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Afarak’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy Infrastructure and Utility Costs

Ferroalloy smelting uses vast electricity; Afarak reports energy as ~20–30% of cash costs, so tariff shifts matter; in South Africa load-shedding and Eskom tariff increases (average annual hikes ~9% in 2024) raise input cost volatility.

In Europe, industrial electricity prices averaged €120/MWh in 2023–24 for heavy users, pushing margins lower when passed through; long-term contracts are scarce, boosting supplier leverage.

Reliance on national grids and limited on-site generation leaves Afarak exposed: a 10% energy price rise can cut EBITDA margins by roughly 3–5% based on recent plant cost structures.

Labor Union Influence in Mining Regions

Highly organized mining unions in South Africa can halt production; in 2023 strike days in the mining sector rose to 1,250 days nationally, driving real wages up ~8% in affected sites and cutting ore output by an estimated 4–6% for some producers.

Afarak faces risk of wage-driven cost shocks and stoppages that can delay shipments; the company must manage labor contracts and buffer inventory to avoid missed sales and margin compression.

Specialized Mining Equipment and Technology

The procurement of heavy machinery and specialized mining tech is concentrated among a few global OEMs (e.g., Caterpillar, Komatsu, Epiroc), giving suppliers strong leverage; in 2024 the top five manufacturers held ~60% of the market for large mining haul trucks and drills.

Their equipment is critical for safety and extraction efficiency, so Afarak faces high switching costs—new fleets can cost $10–30m per unit—and vendor-specific maintenance contracts, which raised OEM after-sales revenue by ~18% in 2023.

Logistics and Global Freight Services

Afarak relies on rail, ports and shipping to move ore and alloys; in 2024 sea freight rates rose ~18% year‑on‑year and Baltic Dry Index volatility amplified landed costs.

Third‑party logistics and state‑owned port operators hold regional monopolies in key corridors, so rate hikes or port bottlenecks translate to higher COGS and margin pressure.

Logistics firms can exert price and timing leverage: a 10% freight rise can add several dollars per tonne, shifting competitiveness.

- 2024 sea freight +18% YoY

- Baltic Dry Index volatility high in 2023–24

- State ports dominate key corridors

- 10% freight rise → material per‑tonne cost increase

Access to Specialized Chemical Reductants

High-grade reductants like metallurgical coke or anthracite are essential to convert chrome ore into ferrochrome; while broadly commoditized, top-quality grades are limited to regions such as Russia, China, and parts of South Africa, concentrating supply.

During 2024–2025, metallurgical coke premiums rose ~18% YoY amid steel demand recovery, giving specialty reductant suppliers leverage to push prices and squeeze Afarak’s smelting margins.

Here’s the quick math: a 10% input-cost rise can cut ferrochrome gross margin by ~3–5 percentage points, depending on product mix; long-term contracts and vertical sourcing reduce this risk.

- Concentrated supply: Russia, China, South Africa

- 2024–25 premium rise: ~18% YoY

- Estimated margin impact: −3–5 pp per 10% cost rise

- Mitigation: long-term contracts, vertical sourcing, input hedges

Suppliers squeeze Afarak: rising power, freight and coke cut margins; contracts mitigate

Suppliers—power grids, OEMs, fuel/reductant providers, logistics and unions—have high leverage over Afarak: 2024 electricity hikes (~9% ZA), EU power ~€120/MWh, sea freight +18% YoY, coke premiums +18% YoY; a 10% input rise cuts ferrochrome gross margin ~3–5 pp; mitigation: long-term contracts, on-site generation, vertical sourcing.

| Metric | 2024–25 |

|---|---|

| Eskom tariff rise | ~9% pa |

| EU power price | €120/MWh |

| Sea freight | +18% YoY |

| Coke premiums | +18% YoY |

| Margin sensitivity | −3–5 pp per 10% input rise |

What is included in the product

Tailored Porter's Five Forces analysis for Afarak that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share, supported by strategic commentary.

Clear one-sheet Porter’s Five Forces for Afarak—fast insight into competitive pressures and strategic levers to ease decision-making.

Customers Bargaining Power

Concentration of Stainless Steel Producers

The global stainless steel market is concentrated: the top 10 stainless producers accounted for roughly 45% of world melt shop capacity in 2024, giving them huge purchasing clout for ferroalloys.

These giants—like POSCO, Tsingshan, and Aperam—buy volumes that let them secure lower prices and multi-year contracts, pressuring suppliers’ margins.

Afarak depends on a few large buyers for a sizable share of sales; losing one major account could cut revenue by double-digit percentage points, based on 2024 sales mix.

Sensitivity to Global Economic Cycles

The demand for Afarak’s ferroalloys tracks stainless steel usage in construction, automotive and infrastructure; global stainless steel output fell 3.5% year-on-year in 2023, pressuring ferroalloy orders. Buyers cut volumes fast in downturns—OECD construction investment dropped about 2.2% in 2023—letting large steelmakers delay purchases and push for lower prices. This cyclicality raises customer leverage when market demand softens and inventories climb, squeezing Afarak’s margins.

Availability of Alternative Global Suppliers

While Afarak targets specialty alloys, many ferroalloys are commodity-like and buyers can source from global producers; China supplied ~70% of global ferrochrome in 2023 and South Africa ~13% per USGS, so alternatives are ample.

Customers can compare prices and switch to suppliers in South Africa, Kazakhstan, or China with low switching costs for standard grades, pressuring Afarak to match market prices and service.

Increasing Demand for Green and Ethical Sourcing

Modern buyers now prioritize ESG; 78% of global steelmakers surveyed in 2024 required supplier CO2 reporting, raising compliance costs for alloy suppliers like Afarak.

Large producers demand traceable, ethical sourcing and can exclude noncompliant vendors, increasing buyer leverage and forcing Afarak to invest in audits and decarbonisation—estimated CAPEX impact ~€10–25m through 2026 for mid-tier miners.

Transparency of Market Pricing

Real-time market data and index-based ferrochrome pricing (e.g., LME-linked and benchmark indices showing 2024–2025 average prices near 1,900–2,100 USD/t for high-carbon grades) raise pricing transparency and compress producers’ ability to charge large premiums.

Buyers, informed of global trends and estimated production costs (electricity and chrome ore share ~60–70% of cash cost), use information symmetry to push back on increases and demand alignment with indices.

- 2024–25 benchmark: ~1,900–2,100 USD/t

- Index pricing adoption rising, spot liquidity up ~15% YoY

- Producers’ premium window < 5–8% vs benchmark

Concentrated buyers, China supply & ESG pressure squeeze ferroalloy margins

Buyers hold high leverage: top 10 stainless makers = ~45% melt capacity (2024), large buyers force lower prices and multi-year contracts, and Afarak relies on a few major accounts (single-account loss = double-digit revenue hit). Commodity-grade ferroalloys face low switching costs (China ~70% ferrochrome supply 2023), index pricing (~$1,900–2,100/t in 2024–25) and ESG demands (78% steelmakers require CO2 data 2024) that compress margins.

| Metric | Value |

|---|---|

| Top-10 stainless share | ~45% (2024) |

| Ferrochrome price | $1,900–2,100/t (2024–25) |

| China supply | ~70% (2023) |

| ESG buyer req | 78% require CO2 data (2024) |

Full Version Awaits

Afarak Porter's Five Forces Analysis

This preview shows the exact Afarak Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted, professionally written, and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Afarak faces moderate supplier power and concentrated steel markets, while buyer bargaining and substitute threats vary by product segment, creating uneven pricing leverage across its operations.

Competitive rivalry is intense among regional ferroalloy producers, but barriers to entry and Afarak’s niche capabilities offer some defensive advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Afarak’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy Infrastructure and Utility Costs

Ferroalloy smelting uses vast electricity; Afarak reports energy as ~20–30% of cash costs, so tariff shifts matter; in South Africa load-shedding and Eskom tariff increases (average annual hikes ~9% in 2024) raise input cost volatility.

In Europe, industrial electricity prices averaged €120/MWh in 2023–24 for heavy users, pushing margins lower when passed through; long-term contracts are scarce, boosting supplier leverage.

Reliance on national grids and limited on-site generation leaves Afarak exposed: a 10% energy price rise can cut EBITDA margins by roughly 3–5% based on recent plant cost structures.

Labor Union Influence in Mining Regions

Highly organized mining unions in South Africa can halt production; in 2023 strike days in the mining sector rose to 1,250 days nationally, driving real wages up ~8% in affected sites and cutting ore output by an estimated 4–6% for some producers.

Afarak faces risk of wage-driven cost shocks and stoppages that can delay shipments; the company must manage labor contracts and buffer inventory to avoid missed sales and margin compression.

Specialized Mining Equipment and Technology

The procurement of heavy machinery and specialized mining tech is concentrated among a few global OEMs (e.g., Caterpillar, Komatsu, Epiroc), giving suppliers strong leverage; in 2024 the top five manufacturers held ~60% of the market for large mining haul trucks and drills.

Their equipment is critical for safety and extraction efficiency, so Afarak faces high switching costs—new fleets can cost $10–30m per unit—and vendor-specific maintenance contracts, which raised OEM after-sales revenue by ~18% in 2023.

Logistics and Global Freight Services

Afarak relies on rail, ports and shipping to move ore and alloys; in 2024 sea freight rates rose ~18% year‑on‑year and Baltic Dry Index volatility amplified landed costs.

Third‑party logistics and state‑owned port operators hold regional monopolies in key corridors, so rate hikes or port bottlenecks translate to higher COGS and margin pressure.

Logistics firms can exert price and timing leverage: a 10% freight rise can add several dollars per tonne, shifting competitiveness.

- 2024 sea freight +18% YoY

- Baltic Dry Index volatility high in 2023–24

- State ports dominate key corridors

- 10% freight rise → material per‑tonne cost increase

Access to Specialized Chemical Reductants

High-grade reductants like metallurgical coke or anthracite are essential to convert chrome ore into ferrochrome; while broadly commoditized, top-quality grades are limited to regions such as Russia, China, and parts of South Africa, concentrating supply.

During 2024–2025, metallurgical coke premiums rose ~18% YoY amid steel demand recovery, giving specialty reductant suppliers leverage to push prices and squeeze Afarak’s smelting margins.

Here’s the quick math: a 10% input-cost rise can cut ferrochrome gross margin by ~3–5 percentage points, depending on product mix; long-term contracts and vertical sourcing reduce this risk.

- Concentrated supply: Russia, China, South Africa

- 2024–25 premium rise: ~18% YoY

- Estimated margin impact: −3–5 pp per 10% cost rise

- Mitigation: long-term contracts, vertical sourcing, input hedges

Suppliers squeeze Afarak: rising power, freight and coke cut margins; contracts mitigate

Suppliers—power grids, OEMs, fuel/reductant providers, logistics and unions—have high leverage over Afarak: 2024 electricity hikes (~9% ZA), EU power ~€120/MWh, sea freight +18% YoY, coke premiums +18% YoY; a 10% input rise cuts ferrochrome gross margin ~3–5 pp; mitigation: long-term contracts, on-site generation, vertical sourcing.

| Metric | 2024–25 |

|---|---|

| Eskom tariff rise | ~9% pa |

| EU power price | €120/MWh |

| Sea freight | +18% YoY |

| Coke premiums | +18% YoY |

| Margin sensitivity | −3–5 pp per 10% input rise |

What is included in the product

Tailored Porter's Five Forces analysis for Afarak that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share, supported by strategic commentary.

Clear one-sheet Porter’s Five Forces for Afarak—fast insight into competitive pressures and strategic levers to ease decision-making.

Customers Bargaining Power

Concentration of Stainless Steel Producers

The global stainless steel market is concentrated: the top 10 stainless producers accounted for roughly 45% of world melt shop capacity in 2024, giving them huge purchasing clout for ferroalloys.

These giants—like POSCO, Tsingshan, and Aperam—buy volumes that let them secure lower prices and multi-year contracts, pressuring suppliers’ margins.

Afarak depends on a few large buyers for a sizable share of sales; losing one major account could cut revenue by double-digit percentage points, based on 2024 sales mix.

Sensitivity to Global Economic Cycles

The demand for Afarak’s ferroalloys tracks stainless steel usage in construction, automotive and infrastructure; global stainless steel output fell 3.5% year-on-year in 2023, pressuring ferroalloy orders. Buyers cut volumes fast in downturns—OECD construction investment dropped about 2.2% in 2023—letting large steelmakers delay purchases and push for lower prices. This cyclicality raises customer leverage when market demand softens and inventories climb, squeezing Afarak’s margins.

Availability of Alternative Global Suppliers

While Afarak targets specialty alloys, many ferroalloys are commodity-like and buyers can source from global producers; China supplied ~70% of global ferrochrome in 2023 and South Africa ~13% per USGS, so alternatives are ample.

Customers can compare prices and switch to suppliers in South Africa, Kazakhstan, or China with low switching costs for standard grades, pressuring Afarak to match market prices and service.

Increasing Demand for Green and Ethical Sourcing

Modern buyers now prioritize ESG; 78% of global steelmakers surveyed in 2024 required supplier CO2 reporting, raising compliance costs for alloy suppliers like Afarak.

Large producers demand traceable, ethical sourcing and can exclude noncompliant vendors, increasing buyer leverage and forcing Afarak to invest in audits and decarbonisation—estimated CAPEX impact ~€10–25m through 2026 for mid-tier miners.

Transparency of Market Pricing

Real-time market data and index-based ferrochrome pricing (e.g., LME-linked and benchmark indices showing 2024–2025 average prices near 1,900–2,100 USD/t for high-carbon grades) raise pricing transparency and compress producers’ ability to charge large premiums.

Buyers, informed of global trends and estimated production costs (electricity and chrome ore share ~60–70% of cash cost), use information symmetry to push back on increases and demand alignment with indices.

- 2024–25 benchmark: ~1,900–2,100 USD/t

- Index pricing adoption rising, spot liquidity up ~15% YoY

- Producers’ premium window < 5–8% vs benchmark

Concentrated buyers, China supply & ESG pressure squeeze ferroalloy margins

Buyers hold high leverage: top 10 stainless makers = ~45% melt capacity (2024), large buyers force lower prices and multi-year contracts, and Afarak relies on a few major accounts (single-account loss = double-digit revenue hit). Commodity-grade ferroalloys face low switching costs (China ~70% ferrochrome supply 2023), index pricing (~$1,900–2,100/t in 2024–25) and ESG demands (78% steelmakers require CO2 data 2024) that compress margins.

| Metric | Value |

|---|---|

| Top-10 stainless share | ~45% (2024) |

| Ferrochrome price | $1,900–2,100/t (2024–25) |

| China supply | ~70% (2023) |

| ESG buyer req | 78% require CO2 data (2024) |

Full Version Awaits

Afarak Porter's Five Forces Analysis

This preview shows the exact Afarak Porter’s Five Forces analysis you’ll receive upon purchase—fully formatted, professionally written, and ready for immediate download and use.