Aferian Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Aferian faces a dynamic landscape where supplier leverage, buyer concentration, competitive rivalry, potential entrants, and substitutes each shape pricing power and growth prospects; this brief snapshot highlights key pressures and strategic levers to watch. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Aferian—perfect for investment decisions, strategy, or presentations.

Suppliers Bargaining Power

Concentration of System-on-Chip providers

Aferian depends on a small set of SoC suppliers, mainly Broadcom and Synaptics, who together held roughly 60–70% share of the targeted broadband SoC market in 2024; that concentration gives them pricing and lead-time leverage over Amino hardware components.

If either supplier raises prices 5–10% or extends lead times by 8–12 weeks—as industry reports warned could happen during 2024–25 supply tightness—Aferian’s gross margins on devices could compress materially and order fulfillment risk would rise.

Cloud infrastructure dependency

24i’s software division relies on AWS and Microsoft Azure for streaming hosting; in 2025 AWS and Azure held ~62% of global cloud market, giving suppliers strong leverage. Their standardized pricing—often per-hour VM and egress fees—leaves mid-sized firms like Aferian little room to negotiate; average egress fees range $0.05–$0.09/GB. As Aferian scales SaaS, cloud costs (often 20–35% of SaaS COGS) remain a key variable controlled by these giants, directly impacting margins.

Third-party content and metadata providers

Third-party metadata and content discovery providers wield high supplier power for Aferian because their data is essential for Pay-TV features; top providers like Gracenote and TiVo reported combined licensing revenues exceeding $600m in 2024, showing concentrated market value. If licensing fees rise 10–25% Aferian must either absorb margins or raise prices, risking churn among price-sensitive operators where average ARPU pressure is already -3% year-over-year.

Specialized software engineering talent

The market for developers skilled in video engineering, DRM, and embedded software is tight and supply-constrained; Stack Overflow data (2024) shows 25–40% fewer specialists vs generalist roles, increasing competition.

Aferian faces wage inflation and poaching from big tech offering 20–40% higher total comp, so it must invest in hiring, retention, and training to protect its IP and product roadmaps.

- High demand: specialist shortage 25–40%

- Compensation gap: 20–40% vs big tech

- Ongoing costs: recruitment + retention spend rise annually

Logistics and manufacturing outsourcing

Aferian outsources set-top box assembly to contract manufacturers mainly in Asia, exposing it to regional GDP shocks and 2024–25 shipping rate swings—container rates rose ~45% in 2024 on some routes, increasing COGS volatility.

Switching suppliers is possible but slow: requalification and quality audits typically take 4–6 months and can raise unit costs by 5–12% during transition.

- High supplier power from capacity/geopolitics

- Shipping cost sensitivity: +45% peak 2024

- Switch time 4–6 months; transition cost +5–12%

Supply-chain & cloud concentration risk: Broadcom/AWS dominance, rising costs

Aferian faces high supplier power: Broadcom/Synaptics hold ~60–70% broadband SoC share (2024); AWS+Azure ~62% cloud (2025); Gracenote+TiVo licensing >$600m (2024). Risks: 5–10% price rises, 8–12 week lead-time hits, cloud egress $0.05–$0.09/GB, developer shortfall 25–40%, switching 4–6 months (+5–12% cost).

| Metric | Value |

|---|---|

| SoC share | 60–70% |

| Cloud share | ~62% |

| Licensing rev | >$600m |

| Egress | $0.05–$0.09/GB |

What is included in the product

Tailored Porter's Five Forces analysis for Aferian that uncovers competitive intensity, buyer and supplier bargaining power, entry barriers, substitute threats, and strategic levers to protect and grow market position.

Aferian Porter's Five Forces delivers a concise, customizable one-sheet that visualizes competitive pressures with an intuitive radar chart—easy to copy into decks, tweak for scenarios, and integrate into broader reports without needing macros.

Customers Bargaining Power

Consolidation of telecommunications operators

The global Pay-TV and broadband sector saw the top 10 operators capture roughly 60% of revenue in 2024, creating fewer but much larger buyers with outsized leverage over vendors.

These Tier 1 groups routinely secure volume discounts of 20–40% and demand bespoke features, stretching Aferian’s R&D and support budgets.

Losing one major Tier 1 client (≥15% of revenue) could cut Aferian’s annual sales by double-digit percentage points, raising financial and operational risk.

Low switching costs for software solutions

As streaming shifts to software-first models, low switching costs let operators move platforms faster; industry surveys show 42% of pay-TV operators considered vendor changes in 2024. Aferian’s 24i delivers strong feature parity and ROI, but standard APIs and containerized deployments cut migration time by ~30%, so Aferian must innovate product and service to sustain stickiness and target >90% retention.

Demand for flexible OPEX pricing models

By late 2025, >70% of telecom buyers prefer OPEX over CAPEX, shifting upfront costs and churn risk to Aferian; customers now demand pay-per-subscriber and scale-down clauses that can cut revenue 20–40% during downturns.

Customers push for performance-based pricing tied to ARPU (average revenue per user) and churn metrics, forcing Aferian to accept lower margin guarantees and add credit/insurance costs that raise its effective cost of service by ~5–8%.

Availability of open-source alternatives

Technically proficient operators can build in-house video delivery using open-source stacks (e.g., NGINX, HLS/DASH, Janus), making DIY a strong bargaining chip against Aferian during renewals.

Self-build total cost can be 30–60% lower first-year for small teams but scales and support gaps raise long-term TCO; Aferian must prove its features and SLAs beat in-house ROI.

Showcase customer ROI: uptime, latency, and support metrics versus DIY to retain pricing power.

- DIY lowers first-year costs 30–60%

- Long-term TCO rises with scale and support needs

- Aferian must prove superior uptime, latency, and SLA value

High sensitivity to hardware price points

Operators typically bundle set-top boxes free or subsidized, so buyers prioritize unit price over premium specs; Aferian’s Amino faces heavy price sensitivity as operators aim for <$40–$60 hardware EPC (estimated per-device cost) to hit ARPU breakevens seen in 2024–25.

That forces Aferian to cut BOM and manufacturing costs while preserving 4K/HDR performance and firmware reliability to avoid support churn.

- Operators target <$40–$60 EPC

- 4K/HDR adds $8–$15 BOM

- Price wins over niche features

Concentrated Buyers Squeeze Aferian: 20–40% Revenue Hit, 5–8% Margin Drag

Concentrated buyers (top 10 ≈60% revenue in 2024) extract 20–40% volume discounts, push OPEX pricing, and demand ARPU/churn-linked contracts that cut Aferian margins ~5–8% and revenue 20–40% in downturns; 42% considered vendor switches in 2024, DIY first-year costs 30–60% lower, operators target <$40–$60 EPC, 4K/HDR adds $8–$15 BOM.

| Metric | Value |

|---|---|

| Top-10 market share (2024) | ≈60% |

| Volume discounts | 20–40% |

| Buyers considering switch (2024) | 42% |

| DIY first-year cost reduction | 30–60% |

| Operator EPC target | <$40–$60 |

| 4K/HDR BOM uplift | $8–$15 |

| Margin effective rise (credit/insurance) | +5–8% |

What You See Is What You Get

Aferian Porter's Five Forces Analysis

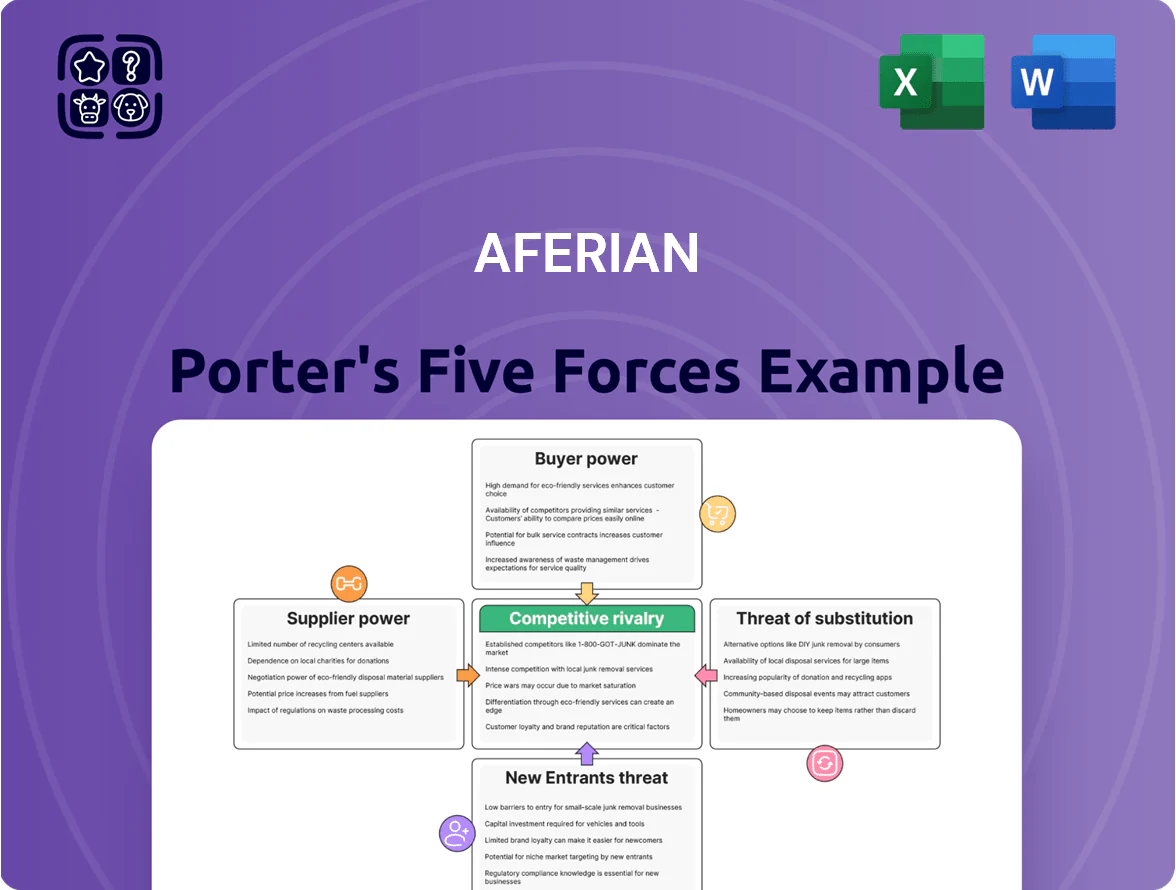

This preview shows the exact Aferian Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document covering industry rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry, ready for download and use the moment you buy. You're viewing the actual deliverable; upon payment you’ll get instant access to this same file.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Aferian faces a dynamic landscape where supplier leverage, buyer concentration, competitive rivalry, potential entrants, and substitutes each shape pricing power and growth prospects; this brief snapshot highlights key pressures and strategic levers to watch. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Aferian—perfect for investment decisions, strategy, or presentations.

Suppliers Bargaining Power

Concentration of System-on-Chip providers

Aferian depends on a small set of SoC suppliers, mainly Broadcom and Synaptics, who together held roughly 60–70% share of the targeted broadband SoC market in 2024; that concentration gives them pricing and lead-time leverage over Amino hardware components.

If either supplier raises prices 5–10% or extends lead times by 8–12 weeks—as industry reports warned could happen during 2024–25 supply tightness—Aferian’s gross margins on devices could compress materially and order fulfillment risk would rise.

Cloud infrastructure dependency

24i’s software division relies on AWS and Microsoft Azure for streaming hosting; in 2025 AWS and Azure held ~62% of global cloud market, giving suppliers strong leverage. Their standardized pricing—often per-hour VM and egress fees—leaves mid-sized firms like Aferian little room to negotiate; average egress fees range $0.05–$0.09/GB. As Aferian scales SaaS, cloud costs (often 20–35% of SaaS COGS) remain a key variable controlled by these giants, directly impacting margins.

Third-party content and metadata providers

Third-party metadata and content discovery providers wield high supplier power for Aferian because their data is essential for Pay-TV features; top providers like Gracenote and TiVo reported combined licensing revenues exceeding $600m in 2024, showing concentrated market value. If licensing fees rise 10–25% Aferian must either absorb margins or raise prices, risking churn among price-sensitive operators where average ARPU pressure is already -3% year-over-year.

Specialized software engineering talent

The market for developers skilled in video engineering, DRM, and embedded software is tight and supply-constrained; Stack Overflow data (2024) shows 25–40% fewer specialists vs generalist roles, increasing competition.

Aferian faces wage inflation and poaching from big tech offering 20–40% higher total comp, so it must invest in hiring, retention, and training to protect its IP and product roadmaps.

- High demand: specialist shortage 25–40%

- Compensation gap: 20–40% vs big tech

- Ongoing costs: recruitment + retention spend rise annually

Logistics and manufacturing outsourcing

Aferian outsources set-top box assembly to contract manufacturers mainly in Asia, exposing it to regional GDP shocks and 2024–25 shipping rate swings—container rates rose ~45% in 2024 on some routes, increasing COGS volatility.

Switching suppliers is possible but slow: requalification and quality audits typically take 4–6 months and can raise unit costs by 5–12% during transition.

- High supplier power from capacity/geopolitics

- Shipping cost sensitivity: +45% peak 2024

- Switch time 4–6 months; transition cost +5–12%

Supply-chain & cloud concentration risk: Broadcom/AWS dominance, rising costs

Aferian faces high supplier power: Broadcom/Synaptics hold ~60–70% broadband SoC share (2024); AWS+Azure ~62% cloud (2025); Gracenote+TiVo licensing >$600m (2024). Risks: 5–10% price rises, 8–12 week lead-time hits, cloud egress $0.05–$0.09/GB, developer shortfall 25–40%, switching 4–6 months (+5–12% cost).

| Metric | Value |

|---|---|

| SoC share | 60–70% |

| Cloud share | ~62% |

| Licensing rev | >$600m |

| Egress | $0.05–$0.09/GB |

What is included in the product

Tailored Porter's Five Forces analysis for Aferian that uncovers competitive intensity, buyer and supplier bargaining power, entry barriers, substitute threats, and strategic levers to protect and grow market position.

Aferian Porter's Five Forces delivers a concise, customizable one-sheet that visualizes competitive pressures with an intuitive radar chart—easy to copy into decks, tweak for scenarios, and integrate into broader reports without needing macros.

Customers Bargaining Power

Consolidation of telecommunications operators

The global Pay-TV and broadband sector saw the top 10 operators capture roughly 60% of revenue in 2024, creating fewer but much larger buyers with outsized leverage over vendors.

These Tier 1 groups routinely secure volume discounts of 20–40% and demand bespoke features, stretching Aferian’s R&D and support budgets.

Losing one major Tier 1 client (≥15% of revenue) could cut Aferian’s annual sales by double-digit percentage points, raising financial and operational risk.

Low switching costs for software solutions

As streaming shifts to software-first models, low switching costs let operators move platforms faster; industry surveys show 42% of pay-TV operators considered vendor changes in 2024. Aferian’s 24i delivers strong feature parity and ROI, but standard APIs and containerized deployments cut migration time by ~30%, so Aferian must innovate product and service to sustain stickiness and target >90% retention.

Demand for flexible OPEX pricing models

By late 2025, >70% of telecom buyers prefer OPEX over CAPEX, shifting upfront costs and churn risk to Aferian; customers now demand pay-per-subscriber and scale-down clauses that can cut revenue 20–40% during downturns.

Customers push for performance-based pricing tied to ARPU (average revenue per user) and churn metrics, forcing Aferian to accept lower margin guarantees and add credit/insurance costs that raise its effective cost of service by ~5–8%.

Availability of open-source alternatives

Technically proficient operators can build in-house video delivery using open-source stacks (e.g., NGINX, HLS/DASH, Janus), making DIY a strong bargaining chip against Aferian during renewals.

Self-build total cost can be 30–60% lower first-year for small teams but scales and support gaps raise long-term TCO; Aferian must prove its features and SLAs beat in-house ROI.

Showcase customer ROI: uptime, latency, and support metrics versus DIY to retain pricing power.

- DIY lowers first-year costs 30–60%

- Long-term TCO rises with scale and support needs

- Aferian must prove superior uptime, latency, and SLA value

High sensitivity to hardware price points

Operators typically bundle set-top boxes free or subsidized, so buyers prioritize unit price over premium specs; Aferian’s Amino faces heavy price sensitivity as operators aim for <$40–$60 hardware EPC (estimated per-device cost) to hit ARPU breakevens seen in 2024–25.

That forces Aferian to cut BOM and manufacturing costs while preserving 4K/HDR performance and firmware reliability to avoid support churn.

- Operators target <$40–$60 EPC

- 4K/HDR adds $8–$15 BOM

- Price wins over niche features

Concentrated Buyers Squeeze Aferian: 20–40% Revenue Hit, 5–8% Margin Drag

Concentrated buyers (top 10 ≈60% revenue in 2024) extract 20–40% volume discounts, push OPEX pricing, and demand ARPU/churn-linked contracts that cut Aferian margins ~5–8% and revenue 20–40% in downturns; 42% considered vendor switches in 2024, DIY first-year costs 30–60% lower, operators target <$40–$60 EPC, 4K/HDR adds $8–$15 BOM.

| Metric | Value |

|---|---|

| Top-10 market share (2024) | ≈60% |

| Volume discounts | 20–40% |

| Buyers considering switch (2024) | 42% |

| DIY first-year cost reduction | 30–60% |

| Operator EPC target | <$40–$60 |

| 4K/HDR BOM uplift | $8–$15 |

| Margin effective rise (credit/insurance) | +5–8% |

What You See Is What You Get

Aferian Porter's Five Forces Analysis

This preview shows the exact Aferian Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It’s the full, professionally formatted document covering industry rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry, ready for download and use the moment you buy. You're viewing the actual deliverable; upon payment you’ll get instant access to this same file.