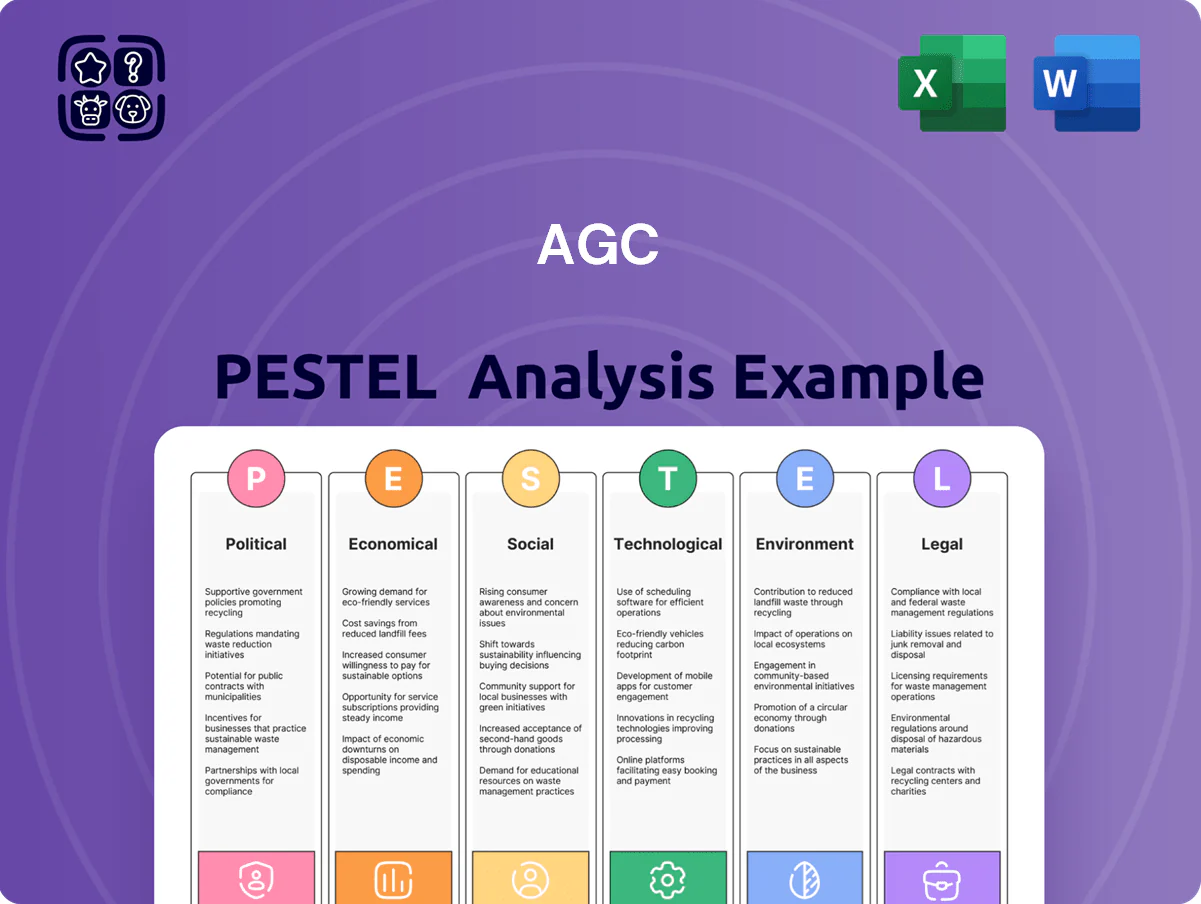

AGC PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political, economic, social, technological, legal, and environmental forces are shaping AGC’s strategic outlook with our concise PESTLE snapshot—perfect for investors and strategists who need immediate, actionable context. Purchase the full PESTLE analysis to unlock detailed risk assessments, trend forecasts, and tailored recommendations you can deploy in boardrooms or investment memos.

Political factors

Geopolitical Trade Tensions

The US-China trade friction through late 2025—including tariffs affecting >$500bn of bilateral goods in prior rounds—forces AGC to plan for tariff volatility; management reports reallocating ~12% of capex to regionalized fabs and inventory buffering to limit cross-border cost exposure. New tariff risks push localized production in US/ASEAN while demand shifts in semiconductors (global capex up ~18% YoY in 2024) directly affect sales of AGC’s high-tech materials.

Energy Security Policies

Instability in European energy markets after the Ukraine conflict has pushed gas prices—peaking at over EUR 120/MWh in 2022 and averaging EUR 60–80/MWh in 2024—raising feedstock and energy costs for AGC’s glass plants and compressing margins.

EU energy security policies and €300+ billion REPowerEU investments are accelerating AGC’s shift to low-carbon fuels; the company is piloting hydrogen and ammonia use to cut scope 1 emissions and reduce gas dependency.

Political stability in key energy-producing regions remains critical: supply disruptions can swing input costs by 20–50%, directly impacting AGC’s cost-competitiveness in energy-intensive glass manufacturing.

Subsidies for Green Technology

Regional Regulatory Alignment

AGC navigates divergent environmental and safety regulations across Japan, Southeast Asia, Europe and the Americas, impacting capex and compliance costs—EU REACH and F-Gas rules can add 1–2% to production costs while Japan’s Green Innovation fund allocated ¥2 trillion through 2025 offers subsidy and partnership opportunities.

Rising political focus on human rights due diligence—EU Corporate Sustainability Due Diligence Directive targets 9,000 companies—drives AGC to expand transparency, traceability and reporting to retain market access and avoid fines or trade restrictions.

Aligning with regional goals, notably Japan’s Green Innovation support, enables AGC to secure subsidies, co-investments and local market leadership in sustainable glass and chemicals, potentially improving ROI on green projects by several percentage points.

- Compliance cost impact: +1–2% production costs (EU rules)

- Japan Green Innovation fund: ¥2 trillion through 2025

- EU due diligence scope: ~9,000 companies (CSDDD)

- Strategic benefit: higher ROI on green projects via subsidies

Infrastructure Development Plans

- Regional infrastructure spend 2024–25: ~$1.2 trillion

- Smart city initiatives tracked: 1,500+

- Target revenue uplift in region: 6–8%

Regionalized fabs & low‑carbon shift: tariffs, energy swings, $1.2T infra boost

US-China tariffs, IRA and EU Green Deal shift AGC to regionalized fabs and low-carbon tech; energy cost volatility (EUR 60–120/MWh) and REPowerEU/¥2T Japan funds alter CAPEX mix; ASEAN/India $1.2T infra pipeline supports 6–8% regional revenue growth; compliance (REACH, F‑Gas, CSDDD) adds ~1–2% production costs while subsidies can offset 30–40% of qualifying green CAPEX.

| Metric | Value |

|---|---|

| Tariff‑exposed trade | >$500bn |

| Energy price range | EUR 60–120/MWh |

| Japan fund | ¥2T (to 2025) |

| ASEAN/India infra | $1.2T |

| Compliance cost | +1–2% |

| Green CAPEX offset | 30–40% |

What is included in the product

Explores how macro-environmental forces uniquely impact AGC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven sections, region- and industry-specific examples, forward-looking insights for scenario planning, and clear formatting to support executives, investors, and strategists in identifying risks, opportunities, and actionable responses.

Condenses AGC's full PESTLE into a clear, shareable summary segmented by category for quick reference in meetings, presentations, or client reports—editable for region- or business-specific notes and optimized for seamless inclusion in slides or planning packs.

Economic factors

Global Inflationary Pressures

By end-2025 AGC managed sustained global inflation that raised raw material and logistics costs ~9–11% year-on-year, with energy surcharges adding €120–€180m in FY2025; pricing actions recovered roughly 60% of cost increases. High ECB rates (peak 4.5% in 2024–25) suppressed European construction and auto demand, reducing volumes ~4–6% in key markets. For FY2026 AGC prioritises margin protection while keeping prices competitive amid elevated input costs.

Recovery in Life Sciences

The biopharmaceutical CDMO market, a core pillar for AGC, showed recovery in late 2025 with global CDMO demand up about 6–8% year-over-year and biotech private funding rising 12% in H2 2025, reversing a 2023–24 slump driven by venture pullback.

Stabilizing interest rates through 2025 spurred renewed capital inflows into biotech R&D, lifting CDMO order books and contract values—AGC reported life-science service bookings growth mid-2025 aligning with industry trends.

This economic pivot supports AGC’s target to restore strategic businesses to high profitability by 2026, with guidance assuming continued biotech funding expansion and improving utilization in CDMO facilities.

Currency Exchange Volatility

As a global entity reporting in JPY, AGC is highly sensitive to USD/JPY and EUR/JPY moves; 2025 saw USD/JPY oscillate roughly 140–160 and EUR/JPY 150–170, which swung reported net sales by an estimated ¥40–60 billion and operating profit by ¥10–20 billion, occasionally masking underlying margin improvements. AGC uses forward hedges, currency swaps and localized production across Asia, Europe and North America to mitigate volatility and protect the bottom line.

Semiconductor Market Growth

The global semiconductor market reached about $680 billion in 2024 and is forecast to grow to roughly $900–1,000 billion by 2027, driven by AI server and edge AI spending; this expansion boosts AGC’s electronics segment via rising demand for EUV photomask blanks and glass core substrates as chipmakers scale capacity for 3nm–2nm nodes.

Sales of EUV-related materials are projected to grow double digits annually, providing a strong economic counterweight to flat-to-slightly-down architectural glass sales in mature markets.

- 2024 semiconductor market ≈ $680B; 2027 est $900–1,000B

- Double-digit CAGR for EUV photomask blanks/glass substrates

- Offsets weaker architectural glass demand

Market Sluggishness in China

The 2023–25 slowdown in China, driven by a stalled property market, cut PVC demand by roughly 12% year-over-year, pressuring AGC’s chemicals segment and prompting a 2024 sales revision of about ¥30–40 billion.

AGC now reallocates volumes toward Southeast Asia, where construction and packaging demand grew ~4–6% in 2024, while expecting China recovery to normalize demand by 2026.

- China PVC demand down ~12% (2023–24)

- AGC 2024 sales revision ~¥30–40bn

- Southeast Asia demand +4–6% (2024)

- China market rebound projected 2026

2025: Inflation, FX swings and energy surcharges squeeze margins as CDMO demand recovers

Global inflation raised AGC input costs ~9–11% in 2025; pricing recouped ~60%, energy surcharges €120–180m. ECB peak rates (~4.5%) cut volumes ~4–6%; CDMO demand rebounded 6–8% in H2 2025. FX swings (USD/JPY 140–160, EUR/JPY 150–170) moved sales ¥40–60bn and OP ¥10–20bn. China PVC down ~12%; SE Asia demand +4–6%.

| Metric | 2024–25 |

|---|---|

| Input cost rise | 9–11% |

| Energy surcharge | €120–180m |

| CDMO demand | +6–8% |

| USD/JPY | 140–160 |

Same Document Delivered

AGC PESTLE Analysis

The preview shown here is the exact AGC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political, economic, social, technological, legal, and environmental forces are shaping AGC’s strategic outlook with our concise PESTLE snapshot—perfect for investors and strategists who need immediate, actionable context. Purchase the full PESTLE analysis to unlock detailed risk assessments, trend forecasts, and tailored recommendations you can deploy in boardrooms or investment memos.

Political factors

Geopolitical Trade Tensions

The US-China trade friction through late 2025—including tariffs affecting >$500bn of bilateral goods in prior rounds—forces AGC to plan for tariff volatility; management reports reallocating ~12% of capex to regionalized fabs and inventory buffering to limit cross-border cost exposure. New tariff risks push localized production in US/ASEAN while demand shifts in semiconductors (global capex up ~18% YoY in 2024) directly affect sales of AGC’s high-tech materials.

Energy Security Policies

Instability in European energy markets after the Ukraine conflict has pushed gas prices—peaking at over EUR 120/MWh in 2022 and averaging EUR 60–80/MWh in 2024—raising feedstock and energy costs for AGC’s glass plants and compressing margins.

EU energy security policies and €300+ billion REPowerEU investments are accelerating AGC’s shift to low-carbon fuels; the company is piloting hydrogen and ammonia use to cut scope 1 emissions and reduce gas dependency.

Political stability in key energy-producing regions remains critical: supply disruptions can swing input costs by 20–50%, directly impacting AGC’s cost-competitiveness in energy-intensive glass manufacturing.

Subsidies for Green Technology

Regional Regulatory Alignment

AGC navigates divergent environmental and safety regulations across Japan, Southeast Asia, Europe and the Americas, impacting capex and compliance costs—EU REACH and F-Gas rules can add 1–2% to production costs while Japan’s Green Innovation fund allocated ¥2 trillion through 2025 offers subsidy and partnership opportunities.

Rising political focus on human rights due diligence—EU Corporate Sustainability Due Diligence Directive targets 9,000 companies—drives AGC to expand transparency, traceability and reporting to retain market access and avoid fines or trade restrictions.

Aligning with regional goals, notably Japan’s Green Innovation support, enables AGC to secure subsidies, co-investments and local market leadership in sustainable glass and chemicals, potentially improving ROI on green projects by several percentage points.

- Compliance cost impact: +1–2% production costs (EU rules)

- Japan Green Innovation fund: ¥2 trillion through 2025

- EU due diligence scope: ~9,000 companies (CSDDD)

- Strategic benefit: higher ROI on green projects via subsidies

Infrastructure Development Plans

- Regional infrastructure spend 2024–25: ~$1.2 trillion

- Smart city initiatives tracked: 1,500+

- Target revenue uplift in region: 6–8%

Regionalized fabs & low‑carbon shift: tariffs, energy swings, $1.2T infra boost

US-China tariffs, IRA and EU Green Deal shift AGC to regionalized fabs and low-carbon tech; energy cost volatility (EUR 60–120/MWh) and REPowerEU/¥2T Japan funds alter CAPEX mix; ASEAN/India $1.2T infra pipeline supports 6–8% regional revenue growth; compliance (REACH, F‑Gas, CSDDD) adds ~1–2% production costs while subsidies can offset 30–40% of qualifying green CAPEX.

| Metric | Value |

|---|---|

| Tariff‑exposed trade | >$500bn |

| Energy price range | EUR 60–120/MWh |

| Japan fund | ¥2T (to 2025) |

| ASEAN/India infra | $1.2T |

| Compliance cost | +1–2% |

| Green CAPEX offset | 30–40% |

What is included in the product

Explores how macro-environmental forces uniquely impact AGC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven sections, region- and industry-specific examples, forward-looking insights for scenario planning, and clear formatting to support executives, investors, and strategists in identifying risks, opportunities, and actionable responses.

Condenses AGC's full PESTLE into a clear, shareable summary segmented by category for quick reference in meetings, presentations, or client reports—editable for region- or business-specific notes and optimized for seamless inclusion in slides or planning packs.

Economic factors

Global Inflationary Pressures

By end-2025 AGC managed sustained global inflation that raised raw material and logistics costs ~9–11% year-on-year, with energy surcharges adding €120–€180m in FY2025; pricing actions recovered roughly 60% of cost increases. High ECB rates (peak 4.5% in 2024–25) suppressed European construction and auto demand, reducing volumes ~4–6% in key markets. For FY2026 AGC prioritises margin protection while keeping prices competitive amid elevated input costs.

Recovery in Life Sciences

The biopharmaceutical CDMO market, a core pillar for AGC, showed recovery in late 2025 with global CDMO demand up about 6–8% year-over-year and biotech private funding rising 12% in H2 2025, reversing a 2023–24 slump driven by venture pullback.

Stabilizing interest rates through 2025 spurred renewed capital inflows into biotech R&D, lifting CDMO order books and contract values—AGC reported life-science service bookings growth mid-2025 aligning with industry trends.

This economic pivot supports AGC’s target to restore strategic businesses to high profitability by 2026, with guidance assuming continued biotech funding expansion and improving utilization in CDMO facilities.

Currency Exchange Volatility

As a global entity reporting in JPY, AGC is highly sensitive to USD/JPY and EUR/JPY moves; 2025 saw USD/JPY oscillate roughly 140–160 and EUR/JPY 150–170, which swung reported net sales by an estimated ¥40–60 billion and operating profit by ¥10–20 billion, occasionally masking underlying margin improvements. AGC uses forward hedges, currency swaps and localized production across Asia, Europe and North America to mitigate volatility and protect the bottom line.

Semiconductor Market Growth

The global semiconductor market reached about $680 billion in 2024 and is forecast to grow to roughly $900–1,000 billion by 2027, driven by AI server and edge AI spending; this expansion boosts AGC’s electronics segment via rising demand for EUV photomask blanks and glass core substrates as chipmakers scale capacity for 3nm–2nm nodes.

Sales of EUV-related materials are projected to grow double digits annually, providing a strong economic counterweight to flat-to-slightly-down architectural glass sales in mature markets.

- 2024 semiconductor market ≈ $680B; 2027 est $900–1,000B

- Double-digit CAGR for EUV photomask blanks/glass substrates

- Offsets weaker architectural glass demand

Market Sluggishness in China

The 2023–25 slowdown in China, driven by a stalled property market, cut PVC demand by roughly 12% year-over-year, pressuring AGC’s chemicals segment and prompting a 2024 sales revision of about ¥30–40 billion.

AGC now reallocates volumes toward Southeast Asia, where construction and packaging demand grew ~4–6% in 2024, while expecting China recovery to normalize demand by 2026.

- China PVC demand down ~12% (2023–24)

- AGC 2024 sales revision ~¥30–40bn

- Southeast Asia demand +4–6% (2024)

- China market rebound projected 2026

2025: Inflation, FX swings and energy surcharges squeeze margins as CDMO demand recovers

Global inflation raised AGC input costs ~9–11% in 2025; pricing recouped ~60%, energy surcharges €120–180m. ECB peak rates (~4.5%) cut volumes ~4–6%; CDMO demand rebounded 6–8% in H2 2025. FX swings (USD/JPY 140–160, EUR/JPY 150–170) moved sales ¥40–60bn and OP ¥10–20bn. China PVC down ~12%; SE Asia demand +4–6%.

| Metric | 2024–25 |

|---|---|

| Input cost rise | 9–11% |

| Energy surcharge | €120–180m |

| CDMO demand | +6–8% |

| USD/JPY | 140–160 |

Same Document Delivered

AGC PESTLE Analysis

The preview shown here is the exact AGC PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.