AIA Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

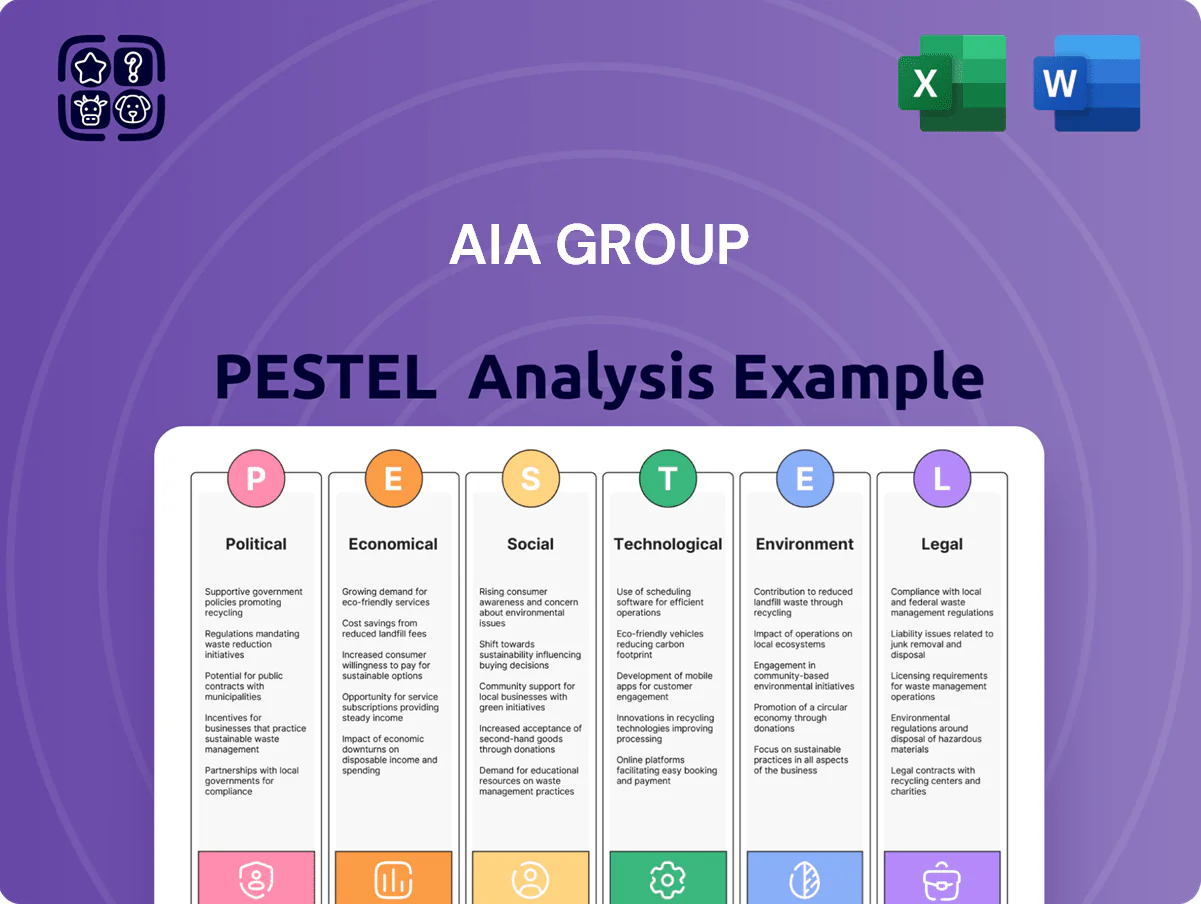

Stay ahead with our PESTLE Analysis of AIA Group—concise, actionable insight into how political, economic, social, technological, legal, and environmental forces shape its strategy and risk profile; ideal for investors, consultants, and executives. Purchase the full report to access detailed trends, forecasts, and ready-to-use slides and spreadsheets that save research time and power smarter decisions.

Political factors

Geopolitical instability and trade friction

AIA Group operates in 18 Asia-Pacific markets, making it highly exposed to US–China strategic tensions; trade frictions and selective sanctions raised compliance costs by an estimated 5–8% for regional insurers in 2024–2025 and lengthened product launch timelines by 3–6 months.

Heightened due diligence requirements have increased operational overhead and slowed cross-border capital repatriation, contributing to capital flow volatility—equity markets in the region showed a 12% average intra‑year swing in 2025.

These political uncertainties have forced AIA to strengthen risk management, increase liquidity buffers (common equity Tier 1‑style targets rising ~2 percentage points) and diversify distribution channels to protect premiums and solvency under stress scenarios.

Mainland China expansion and regulatory facilitation

The company’s growth is tightly linked to Mainland China expansion, supported by political initiatives like the Guangdong-Hong Kong-Macao Greater Bay Area which target deeper regional integration and boosted cross-border financial flows.

Regulatory approvals in Anhui, Shandong and Zhejiang enable AIA to access over 340 million potential customers; China life insurance premiums grew 7.6% in 2024 to RMB 4.2 trillion, signaling market opportunity.

This political facilitation lets AIA scale wealth management and cross-border health solutions via structured platforms, improving distribution efficiency and lifting potential premium and asset-under-management growth across the region.

Governmental focus on financial inclusion

Foreign ownership and capital control policies

AIA faces evolving foreign ownership and capital control regulations across Southeast Asia and Mainland China; tighter rules can curb repatriation and capital mobility, affecting investment and dividend strategies. Changes in insurance capital requirements—e.g., China's Solvency II-like reforms and ASEAN jurisdictions raising RBC ratios—could compress ROE and increase local capital needs. As of late 2025 analysts flag a persistent risk of stricter controls limiting cross-border cash flows.

- Exposure: >60% of AIA premiums from Greater China/Southeast Asia (2024).

- Risk: potential repatriation restrictions—analyst consensus late-2025: medium-high.

- Impact: higher local capital raises could lower ROE by 100–300 bps under stress scenarios.

Political influence on monetary policy

National political shifts, including a hypothetical second Trump term in the U.S., can trigger tariffs and dollar volatility that transmitted to Asia caused FX swings—USD/SGD moved 2.8% during 2018–2024 tariff episodes—affecting insurers' asset returns and liability valuations.

Political pressure on central banks creates 'driving in the fog' uncertainty, producing abrupt rate moves; 2022–2024 saw policy rate volatility where several Asian central banks changed rates by 150–300bps cumulatively.

AIA’s investment yields and product pricing are sensitive to these shocks, so the group keeps strong liquidity and CET1-like buffers; statutory solvency ratios across APAC markets averaged above 180% in 2024, supporting resilience.

- Political shocks → trade/currency transmission (USD swings ~2–3%)

- Central bank uncertainty → sudden rate shifts (150–300bps range 2022–24)

- AIA response → high liquidity, solvency ~180%+ across APAC (2024)

Geopolitical Costs Lift Premiums >60%; Solvency Strong but ROE Faces 100–300bps Hit

Political risks (US–China tensions, capital controls, regulatory reforms) raised compliance costs ~5–8% and delayed launches 3–6 months in 2024–25; Greater China/SEA >60% premiums (2024), China premiums +7.6% (2024). AIA boosted liquidity and CET1‑like buffers ~+2ppt; regional solvency ~180% (2024); potential ROE hit 100–300bps under tighter local capital rules.

| Metric | Value |

|---|---|

| Premiums share (GC/SEA) | >60% (2024) |

| China premiums | RMB 4.2tn, +7.6% (2024) |

| Compliance cost rise | 5–8% (2024–25) |

| Regional solvency | ~180% (2024) |

| ROE risk | -100–300bps |

What is included in the product

Explores how macro-environmental factors — Political, Economic, Social, Technological, Environmental, and Legal — uniquely affect AIA Group, with data-backed trends, region-specific examples, forward-looking insights for scenario planning, and practical implications to inform executives, investors, and strategists.

Concise PESTLE summary tailored to AIA Group that’s visually segmented for quick interpretation, easily dropped into presentations, and editable for region-specific notes to streamline risk discussions and strategic alignment across teams.

Economic factors

Interest rate cycles and investment spreads

In 2025, global central banks including the U.S. Federal Reserve shifted toward monetary easing, compressing yields and narrowing investment spreads, which has put downward pressure on AIA Group’s investment yields after the higher-rate boost in 2022–24.

This easing requires AIA to actively manage asset-liability matching and duration risk; as of FY2024 AIA reported a 4.8% investment yield and duration management remains central to preserving solvency margins.

AIA continues to target 9–11% CAGR in OPAT per share through 2026, leveraging a disciplined investment strategy, diversified fixed-income portfolio and ongoing rebalancing to mitigate spread compression.

Growth of the Asian middle class

The expanding Asian middle class—projected to reach 2.7 billion by 2030—drives premium growth in China, India and Vietnam as rising disposable incomes boost demand for savings, protection and wealth management products.

AIA’s focus on affluent segments delivered double-digit VONB growth in 11 of 18 markets as of late 2025, supporting group operating profit and higher premium inflows amid robust demographic shifts.

Inflation and rising healthcare costs

Persisting inflation across APAC—consumer price rises averaging 3.5–5% in 2024–25 in key markets—has pushed up medical service costs and claim severity, squeezing health product margins for AIA Group. AIA deploys advanced analytics and its Integrated Healthcare Strategy to optimize outpatient clinic networks and provider pricing, cutting claim leakage and lowering per-claim cost growth. Economic headwinds increase reliance on AIA Vitality; studies within AIA show Vitality members have up to 15–20% lower hospital admissions, supporting long-term claim reduction and margin protection.

Capital market volatility and asset valuation

Fluctuations in equity and bond markets, including the market softness in early 2025, directly pressured AIA’s embedded value and shareholder capital positions.

AIA reported a shareholder capital ratio of 219% in mid-2025, providing strong capacity to absorb market volatility and protect solvency.

With 98% of bond holdings rated investment grade, AIA’s stable investment portfolio offers a defensive buffer against broader downturns.

- Market softness early 2025 reduced EV sensitivity to equity returns

- Shareholder capital ratio 219% (mid-2025)

- 98% of bonds investment grade

Currency fluctuations and exchange rate risk

Operating across 18 markets exposes AIA to material FX risk, notably versus the U.S. dollar; a weaker USD in late 2025 lifted non-U.S. equity returns and positively impacted AIA’s reported net profit—Group reported HKD 33.8 billion profit for 9M 2025 with ~4–5% translation tailwind from stronger Asian currencies.

The group employs hedging and constant-exchange-rate (CER) reporting to isolate underlying operating performance: CER growth metrics showed new business value up ~7% YoY in 9M 2025, smoothing volatility for international investors.

- 18 markets exposure increases FX volatility risk

- Late-2025 weaker USD gave ~4–5% translation uplift to reported profit

- Hedging programs and CER reporting used to clarify underlying results

- CER metrics: NBV growth ~7% YoY in 9M 2025

AIA: Strong capital, rising premiums amid yield squeeze and APAC inflation

AIA faces yield compression from 2025 easing, reported 4.8% investment yield (FY2024) and 219% shareholder capital ratio (mid-2025) while 98% of bonds are investment grade; APAC inflation 3.5–5% (2024–25) raises claim costs offset by AIA Vitality and integrated healthcare; expanding Asian middle class (projected 2.7bn by 2030) fuels premium growth and VONB gains (~double-digit in 11/18 markets).

| Metric | Value |

|---|---|

| Investment yield (FY2024) | 4.8% |

| Shareholder capital ratio (mid-2025) | 219% |

| IG bonds | 98% |

| APAC inflation (2024–25) | 3.5–5% |

| Asian middle class (2030) | 2.7 billion |

Same Document Delivered

AIA Group PESTLE Analysis

The preview shown here is the exact AIA Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment work.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Stay ahead with our PESTLE Analysis of AIA Group—concise, actionable insight into how political, economic, social, technological, legal, and environmental forces shape its strategy and risk profile; ideal for investors, consultants, and executives. Purchase the full report to access detailed trends, forecasts, and ready-to-use slides and spreadsheets that save research time and power smarter decisions.

Political factors

Geopolitical instability and trade friction

AIA Group operates in 18 Asia-Pacific markets, making it highly exposed to US–China strategic tensions; trade frictions and selective sanctions raised compliance costs by an estimated 5–8% for regional insurers in 2024–2025 and lengthened product launch timelines by 3–6 months.

Heightened due diligence requirements have increased operational overhead and slowed cross-border capital repatriation, contributing to capital flow volatility—equity markets in the region showed a 12% average intra‑year swing in 2025.

These political uncertainties have forced AIA to strengthen risk management, increase liquidity buffers (common equity Tier 1‑style targets rising ~2 percentage points) and diversify distribution channels to protect premiums and solvency under stress scenarios.

Mainland China expansion and regulatory facilitation

The company’s growth is tightly linked to Mainland China expansion, supported by political initiatives like the Guangdong-Hong Kong-Macao Greater Bay Area which target deeper regional integration and boosted cross-border financial flows.

Regulatory approvals in Anhui, Shandong and Zhejiang enable AIA to access over 340 million potential customers; China life insurance premiums grew 7.6% in 2024 to RMB 4.2 trillion, signaling market opportunity.

This political facilitation lets AIA scale wealth management and cross-border health solutions via structured platforms, improving distribution efficiency and lifting potential premium and asset-under-management growth across the region.

Governmental focus on financial inclusion

Foreign ownership and capital control policies

AIA faces evolving foreign ownership and capital control regulations across Southeast Asia and Mainland China; tighter rules can curb repatriation and capital mobility, affecting investment and dividend strategies. Changes in insurance capital requirements—e.g., China's Solvency II-like reforms and ASEAN jurisdictions raising RBC ratios—could compress ROE and increase local capital needs. As of late 2025 analysts flag a persistent risk of stricter controls limiting cross-border cash flows.

- Exposure: >60% of AIA premiums from Greater China/Southeast Asia (2024).

- Risk: potential repatriation restrictions—analyst consensus late-2025: medium-high.

- Impact: higher local capital raises could lower ROE by 100–300 bps under stress scenarios.

Political influence on monetary policy

National political shifts, including a hypothetical second Trump term in the U.S., can trigger tariffs and dollar volatility that transmitted to Asia caused FX swings—USD/SGD moved 2.8% during 2018–2024 tariff episodes—affecting insurers' asset returns and liability valuations.

Political pressure on central banks creates 'driving in the fog' uncertainty, producing abrupt rate moves; 2022–2024 saw policy rate volatility where several Asian central banks changed rates by 150–300bps cumulatively.

AIA’s investment yields and product pricing are sensitive to these shocks, so the group keeps strong liquidity and CET1-like buffers; statutory solvency ratios across APAC markets averaged above 180% in 2024, supporting resilience.

- Political shocks → trade/currency transmission (USD swings ~2–3%)

- Central bank uncertainty → sudden rate shifts (150–300bps range 2022–24)

- AIA response → high liquidity, solvency ~180%+ across APAC (2024)

Geopolitical Costs Lift Premiums >60%; Solvency Strong but ROE Faces 100–300bps Hit

Political risks (US–China tensions, capital controls, regulatory reforms) raised compliance costs ~5–8% and delayed launches 3–6 months in 2024–25; Greater China/SEA >60% premiums (2024), China premiums +7.6% (2024). AIA boosted liquidity and CET1‑like buffers ~+2ppt; regional solvency ~180% (2024); potential ROE hit 100–300bps under tighter local capital rules.

| Metric | Value |

|---|---|

| Premiums share (GC/SEA) | >60% (2024) |

| China premiums | RMB 4.2tn, +7.6% (2024) |

| Compliance cost rise | 5–8% (2024–25) |

| Regional solvency | ~180% (2024) |

| ROE risk | -100–300bps |

What is included in the product

Explores how macro-environmental factors — Political, Economic, Social, Technological, Environmental, and Legal — uniquely affect AIA Group, with data-backed trends, region-specific examples, forward-looking insights for scenario planning, and practical implications to inform executives, investors, and strategists.

Concise PESTLE summary tailored to AIA Group that’s visually segmented for quick interpretation, easily dropped into presentations, and editable for region-specific notes to streamline risk discussions and strategic alignment across teams.

Economic factors

Interest rate cycles and investment spreads

In 2025, global central banks including the U.S. Federal Reserve shifted toward monetary easing, compressing yields and narrowing investment spreads, which has put downward pressure on AIA Group’s investment yields after the higher-rate boost in 2022–24.

This easing requires AIA to actively manage asset-liability matching and duration risk; as of FY2024 AIA reported a 4.8% investment yield and duration management remains central to preserving solvency margins.

AIA continues to target 9–11% CAGR in OPAT per share through 2026, leveraging a disciplined investment strategy, diversified fixed-income portfolio and ongoing rebalancing to mitigate spread compression.

Growth of the Asian middle class

The expanding Asian middle class—projected to reach 2.7 billion by 2030—drives premium growth in China, India and Vietnam as rising disposable incomes boost demand for savings, protection and wealth management products.

AIA’s focus on affluent segments delivered double-digit VONB growth in 11 of 18 markets as of late 2025, supporting group operating profit and higher premium inflows amid robust demographic shifts.

Inflation and rising healthcare costs

Persisting inflation across APAC—consumer price rises averaging 3.5–5% in 2024–25 in key markets—has pushed up medical service costs and claim severity, squeezing health product margins for AIA Group. AIA deploys advanced analytics and its Integrated Healthcare Strategy to optimize outpatient clinic networks and provider pricing, cutting claim leakage and lowering per-claim cost growth. Economic headwinds increase reliance on AIA Vitality; studies within AIA show Vitality members have up to 15–20% lower hospital admissions, supporting long-term claim reduction and margin protection.

Capital market volatility and asset valuation

Fluctuations in equity and bond markets, including the market softness in early 2025, directly pressured AIA’s embedded value and shareholder capital positions.

AIA reported a shareholder capital ratio of 219% in mid-2025, providing strong capacity to absorb market volatility and protect solvency.

With 98% of bond holdings rated investment grade, AIA’s stable investment portfolio offers a defensive buffer against broader downturns.

- Market softness early 2025 reduced EV sensitivity to equity returns

- Shareholder capital ratio 219% (mid-2025)

- 98% of bonds investment grade

Currency fluctuations and exchange rate risk

Operating across 18 markets exposes AIA to material FX risk, notably versus the U.S. dollar; a weaker USD in late 2025 lifted non-U.S. equity returns and positively impacted AIA’s reported net profit—Group reported HKD 33.8 billion profit for 9M 2025 with ~4–5% translation tailwind from stronger Asian currencies.

The group employs hedging and constant-exchange-rate (CER) reporting to isolate underlying operating performance: CER growth metrics showed new business value up ~7% YoY in 9M 2025, smoothing volatility for international investors.

- 18 markets exposure increases FX volatility risk

- Late-2025 weaker USD gave ~4–5% translation uplift to reported profit

- Hedging programs and CER reporting used to clarify underlying results

- CER metrics: NBV growth ~7% YoY in 9M 2025

AIA: Strong capital, rising premiums amid yield squeeze and APAC inflation

AIA faces yield compression from 2025 easing, reported 4.8% investment yield (FY2024) and 219% shareholder capital ratio (mid-2025) while 98% of bonds are investment grade; APAC inflation 3.5–5% (2024–25) raises claim costs offset by AIA Vitality and integrated healthcare; expanding Asian middle class (projected 2.7bn by 2030) fuels premium growth and VONB gains (~double-digit in 11/18 markets).

| Metric | Value |

|---|---|

| Investment yield (FY2024) | 4.8% |

| Shareholder capital ratio (mid-2025) | 219% |

| IG bonds | 98% |

| APAC inflation (2024–25) | 3.5–5% |

| Asian middle class (2030) | 2.7 billion |

Same Document Delivered

AIA Group PESTLE Analysis

The preview shown here is the exact AIA Group PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment work.