AIB Group Business Model Canvas

AIB Group Business Model Canvas: Downloadable Strategic Blueprint for Investors

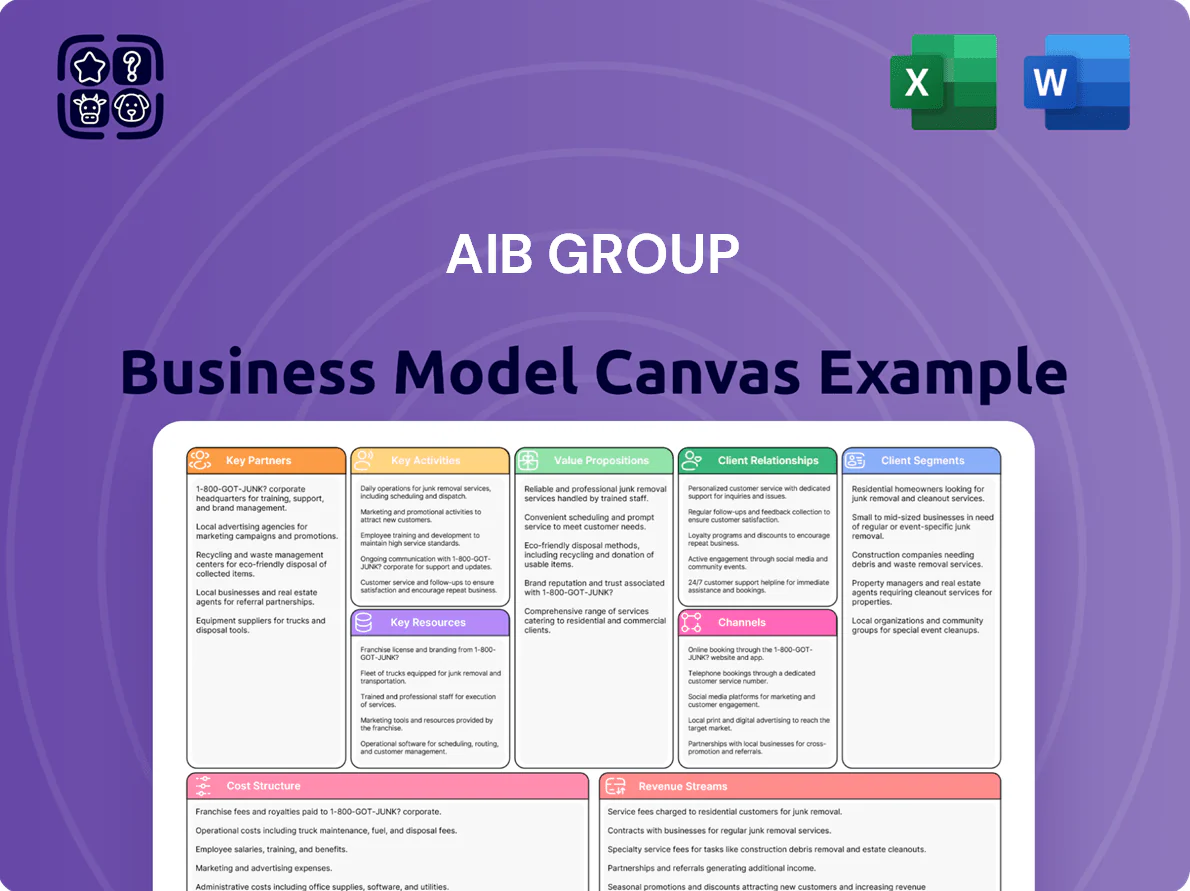

Unlock the full strategic blueprint behind AIB Group’s business model—this in-depth Business Model Canvas reveals customer segments, value propositions, revenue streams, and key partnerships that drive growth and resilience in banking. Ideal for investors, consultants, and founders seeking a ready-to-use, editable analysis to benchmark strategy or inform decisions. Download the complete Word and Excel canvas to apply AIB’s insights directly to your planning.

Partnerships

Strategic Fintech Alliances

AIB partners with fintechs such as Stripe and TransferWise-style providers to add instant payments and advanced analytics, cutting integration time by ~40% and reducing in-house dev costs; these alliances supported AIB’s digital transactions rising 28% in 2024 to ~€95bn. By outsourcing niche tech, AIB keeps pace with UK/Irish neo-banks while preserving core banking control and compliance.

Government and Regulatory Agencies

The group partners with the Strategic Banking Corporation of Ireland and UK state bodies to deliver state-backed SME lending—supporting over €3.2bn in government-backed loans to Irish SMEs since 2019 and participating in UK rollover schemes totaling ~£1.1bn in 2024–25; ongoing engagement with the European Central Bank keeps AIB aligned with evolving capital ratios and monetary policy as of late 2025.

Mortgage and Insurance Brokers

AIB relies heavily on c.40% of new mortgages sourced via independent brokers and intermediaries, who act as an extended sales force to reach customers preferring third‑party advice; in 2024 broker-originated mortgage balances were roughly €18bn. Maintaining competitive commission rates and real‑time digital integration (API feeds, e‑apply portals) with brokers is crucial to defend AIB’s housing finance market share.

Joint Venture with Great-West Lifeco

AIB’s joint venture with Great-West Lifeco through Irish Life lets AIB sell life assurance and pensions, expanding wealth-management under the AIB brand and boosting non-interest income—Irish Life reported €18.3bn assets under management at end-2024, contributing materially to AIB’s fee income.

- Access to Irish Life products

- €18.3bn AUM (2024)

- Higher fee and commission income

- Stronger one-stop financial planning

Outsourced Technology and Cloud Providers

AIB partners with global cloud and cybersecurity providers (AWS, Microsoft Azure, Google Cloud, and specialist security firms) to ensure digital channels handle peak loads—AIB reported 25% YoY growth in digital transactions to ~430m in 2024—keeping systems resilient and secure while freeing internal teams to focus on product innovation and customer service.

- ~430m digital transactions in 2024 (25% YoY)

- Third-party cloud reduces capital IT spend, shifts to Opex

- Scalability for peak payroll/card cycles

- Outsourced security lowers breach risk and compliance costs

AIB scales digital payments (€95bn) & partnerships: SME loans, mortgages, Irish Life AUM

AIB leverages fintechs (Stripe, Wise) and cloud/cyber partners to scale digital payments and security—digital transactions rose ~28% in 2024 to ~€95bn (~430m txns); state partnerships drove €3.2bn+ govt-backed SME loans since 2019 and ~€1.1bn UK schemes (2024–25); ~40% new mortgages via brokers (~€18bn balances 2024); Irish Life JV AUM €18.3bn (2024).

| Partnership | Key metric (2024) |

|---|---|

| Fintech/cloud | €95bn / 430m txns |

| State SME schemes | €3.2bn since 2019 |

| Mortgage brokers | €18bn balances (40%) |

| Irish Life JV | €18.3bn AUM |

What is included in the product

A concise, pre-built Business Model Canvas for AIB Group detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance—linked to competitive advantages, SWOT insights, and realistic operations for presentations, investor discussions, and strategic decision-making.

High-level view of AIB Group’s business model with editable cells, helping teams quickly pinpoint value drivers and regulatory pain points for faster strategic decisions.

Activities

Credit Assessment and Lending Operations

The group’s primary activity is rigorous credit assessment for personal, SME, and corporate clients, using advanced risk models and 10+ years of historical loss data to price loans and set provisions; AIB held EUR 56.3bn in loans to customers and a 0.45% gross non-performing exposure ratio at YE 2024. By allocating capital efficiently across segments, the bank targets return on tangible equity of ~11% while keeping stage 3 loans under tight control to support core markets and economic activity.

Digital Platform Development and Maintenance

Regulatory Compliance and Risk Management

AIB Group allocates about 6% of annual operating costs (≈€360m in 2024) to compliance and risk, continuously auditing processes to meet AML and GDPR rules and feeding robust reporting frameworks into Central Bank of Ireland submissions. Effective risk management preserves its banking licence and institutional trust, reducing capital-at-risk from operational loss events by an estimated 40% year-on-year.

Sustainable Finance and ESG Integration

- 25% new lending → green projects by 2025

- 12.4 MtCO2e FY2024 financed emissions

- Incentive: lower rates for >30% emission cuts

- Target: -50% financed emissions by 2030 (SBTi-aligned)

Customer Relationship and Retention Management

The group runs proactive outreach—personalised financial health checks, targeted campaigns, and omni-channel support—to boost satisfaction and loyalty; AIB reported a 70% digital active customer rate and cut attrition to 6.1% in 2024, improving share of wallet without costly acquisition.

- Personalised checks: quarterly for 1.9m customers

- Targeted campaigns: +12% product cross-sell 2024

- Omni-channel CSAT: 82% in 2024

- Retention focus: 6.1% churn 2024

AIB: Digital-first lender—€56.3bn loans, 0.45% NPE, £300m tech, 25% green targets

AIB’s key activities: credit underwriting (EUR56.3bn loans, 0.45% GNE YE2024), digital delivery (≈£300m FY2024, 80% daily transactions), compliance/risk (~€360m, 6% costs), ESG lending shift (25% new green by 2025; 12.4 MtCO2e FY2024; -50% by 2030), and customer retention (70% digital active, 6.1% churn 2024).

| Metric | 2024/Target |

|---|---|

| Loans to customers | EUR56.3bn |

| Gross NPE | 0.45% |

| Digital spend | £300m |

| Digital transactions | 80% |

| Compliance cost | €360m (6%) |

| Financed emissions | 12.4 MtCO2e |

| Green lending target | 25% new by 2025 |

| ROTE target | ~11% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual AIB Group Business Model Canvas—not a mockup or sample—and it matches the file you’ll receive after purchase; upon completing your order you’ll get this same professional, ready-to-use document in editable Word and Excel formats.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

AIB Group Business Model Canvas: Downloadable Strategic Blueprint for Investors

Unlock the full strategic blueprint behind AIB Group’s business model—this in-depth Business Model Canvas reveals customer segments, value propositions, revenue streams, and key partnerships that drive growth and resilience in banking. Ideal for investors, consultants, and founders seeking a ready-to-use, editable analysis to benchmark strategy or inform decisions. Download the complete Word and Excel canvas to apply AIB’s insights directly to your planning.

Partnerships

Strategic Fintech Alliances

AIB partners with fintechs such as Stripe and TransferWise-style providers to add instant payments and advanced analytics, cutting integration time by ~40% and reducing in-house dev costs; these alliances supported AIB’s digital transactions rising 28% in 2024 to ~€95bn. By outsourcing niche tech, AIB keeps pace with UK/Irish neo-banks while preserving core banking control and compliance.

Government and Regulatory Agencies

The group partners with the Strategic Banking Corporation of Ireland and UK state bodies to deliver state-backed SME lending—supporting over €3.2bn in government-backed loans to Irish SMEs since 2019 and participating in UK rollover schemes totaling ~£1.1bn in 2024–25; ongoing engagement with the European Central Bank keeps AIB aligned with evolving capital ratios and monetary policy as of late 2025.

Mortgage and Insurance Brokers

AIB relies heavily on c.40% of new mortgages sourced via independent brokers and intermediaries, who act as an extended sales force to reach customers preferring third‑party advice; in 2024 broker-originated mortgage balances were roughly €18bn. Maintaining competitive commission rates and real‑time digital integration (API feeds, e‑apply portals) with brokers is crucial to defend AIB’s housing finance market share.

Joint Venture with Great-West Lifeco

AIB’s joint venture with Great-West Lifeco through Irish Life lets AIB sell life assurance and pensions, expanding wealth-management under the AIB brand and boosting non-interest income—Irish Life reported €18.3bn assets under management at end-2024, contributing materially to AIB’s fee income.

- Access to Irish Life products

- €18.3bn AUM (2024)

- Higher fee and commission income

- Stronger one-stop financial planning

Outsourced Technology and Cloud Providers

AIB partners with global cloud and cybersecurity providers (AWS, Microsoft Azure, Google Cloud, and specialist security firms) to ensure digital channels handle peak loads—AIB reported 25% YoY growth in digital transactions to ~430m in 2024—keeping systems resilient and secure while freeing internal teams to focus on product innovation and customer service.

- ~430m digital transactions in 2024 (25% YoY)

- Third-party cloud reduces capital IT spend, shifts to Opex

- Scalability for peak payroll/card cycles

- Outsourced security lowers breach risk and compliance costs

AIB scales digital payments (€95bn) & partnerships: SME loans, mortgages, Irish Life AUM

AIB leverages fintechs (Stripe, Wise) and cloud/cyber partners to scale digital payments and security—digital transactions rose ~28% in 2024 to ~€95bn (~430m txns); state partnerships drove €3.2bn+ govt-backed SME loans since 2019 and ~€1.1bn UK schemes (2024–25); ~40% new mortgages via brokers (~€18bn balances 2024); Irish Life JV AUM €18.3bn (2024).

| Partnership | Key metric (2024) |

|---|---|

| Fintech/cloud | €95bn / 430m txns |

| State SME schemes | €3.2bn since 2019 |

| Mortgage brokers | €18bn balances (40%) |

| Irish Life JV | €18.3bn AUM |

What is included in the product

A concise, pre-built Business Model Canvas for AIB Group detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and governance—linked to competitive advantages, SWOT insights, and realistic operations for presentations, investor discussions, and strategic decision-making.

High-level view of AIB Group’s business model with editable cells, helping teams quickly pinpoint value drivers and regulatory pain points for faster strategic decisions.

Activities

Credit Assessment and Lending Operations

The group’s primary activity is rigorous credit assessment for personal, SME, and corporate clients, using advanced risk models and 10+ years of historical loss data to price loans and set provisions; AIB held EUR 56.3bn in loans to customers and a 0.45% gross non-performing exposure ratio at YE 2024. By allocating capital efficiently across segments, the bank targets return on tangible equity of ~11% while keeping stage 3 loans under tight control to support core markets and economic activity.

Digital Platform Development and Maintenance

Regulatory Compliance and Risk Management

AIB Group allocates about 6% of annual operating costs (≈€360m in 2024) to compliance and risk, continuously auditing processes to meet AML and GDPR rules and feeding robust reporting frameworks into Central Bank of Ireland submissions. Effective risk management preserves its banking licence and institutional trust, reducing capital-at-risk from operational loss events by an estimated 40% year-on-year.

Sustainable Finance and ESG Integration

- 25% new lending → green projects by 2025

- 12.4 MtCO2e FY2024 financed emissions

- Incentive: lower rates for >30% emission cuts

- Target: -50% financed emissions by 2030 (SBTi-aligned)

Customer Relationship and Retention Management

The group runs proactive outreach—personalised financial health checks, targeted campaigns, and omni-channel support—to boost satisfaction and loyalty; AIB reported a 70% digital active customer rate and cut attrition to 6.1% in 2024, improving share of wallet without costly acquisition.

- Personalised checks: quarterly for 1.9m customers

- Targeted campaigns: +12% product cross-sell 2024

- Omni-channel CSAT: 82% in 2024

- Retention focus: 6.1% churn 2024

AIB: Digital-first lender—€56.3bn loans, 0.45% NPE, £300m tech, 25% green targets

AIB’s key activities: credit underwriting (EUR56.3bn loans, 0.45% GNE YE2024), digital delivery (≈£300m FY2024, 80% daily transactions), compliance/risk (~€360m, 6% costs), ESG lending shift (25% new green by 2025; 12.4 MtCO2e FY2024; -50% by 2030), and customer retention (70% digital active, 6.1% churn 2024).

| Metric | 2024/Target |

|---|---|

| Loans to customers | EUR56.3bn |

| Gross NPE | 0.45% |

| Digital spend | £300m |

| Digital transactions | 80% |

| Compliance cost | €360m (6%) |

| Financed emissions | 12.4 MtCO2e |

| Green lending target | 25% new by 2025 |

| ROTE target | ~11% |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual AIB Group Business Model Canvas—not a mockup or sample—and it matches the file you’ll receive after purchase; upon completing your order you’ll get this same professional, ready-to-use document in editable Word and Excel formats.