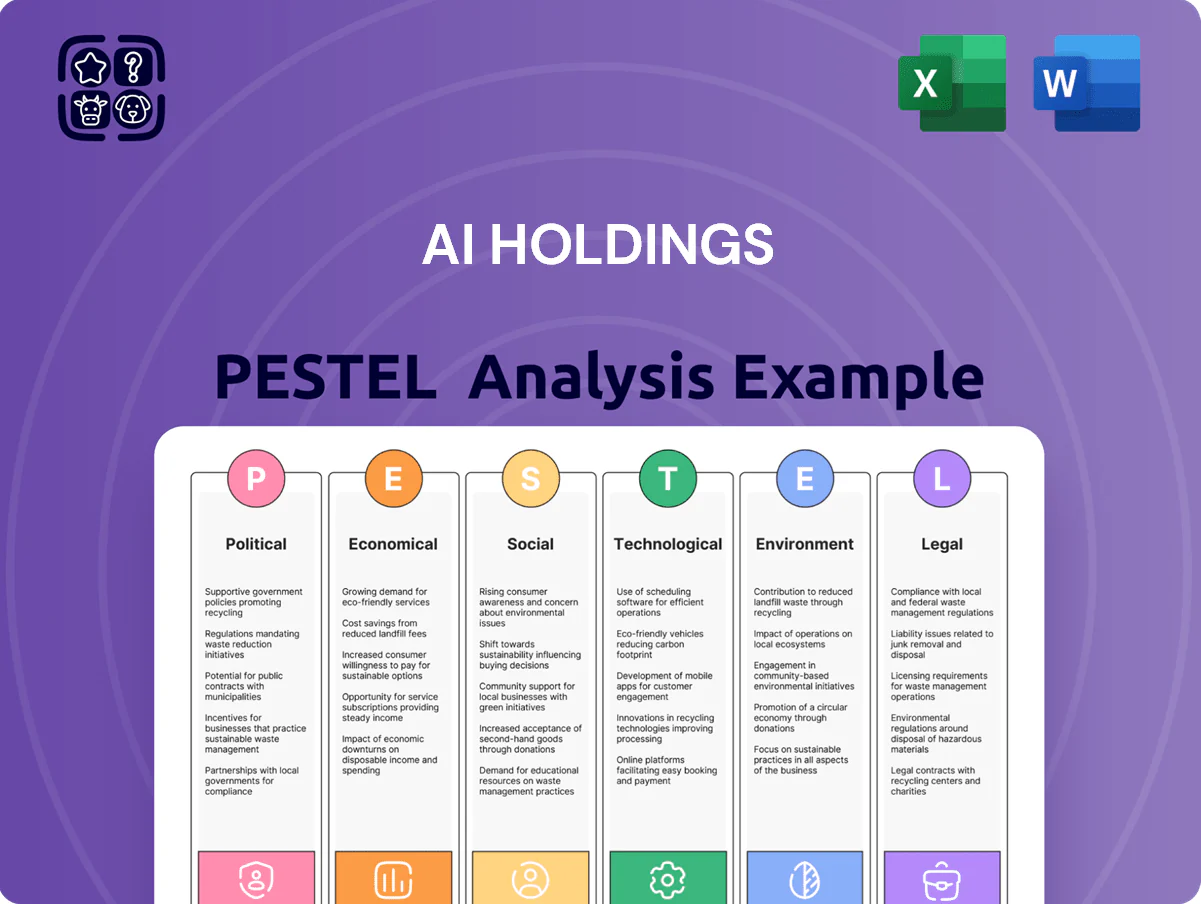

Ai Holdings PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Ai Holdings’ prospects—our concise PESTLE highlights key risks and opportunities to inform smarter decisions. Purchase the full, ready-to-use analysis for detailed insights, data-driven scenarios, and editable charts to fast-track your investment or strategy work.

Political factors

Japanese government stability and policy continuity

As of late 2025 Japan's political agenda emphasizes economic revitalization and structural reform, with the government allocating ¥12.4 trillion in the 2025 budget to digital transformation and urban development initiatives. For AI Holdings, continued public backing for urban redevelopment and smart-city projects—part of a ¥5.6 trillion multi-year infrastructure plan—supports stable long-term planning. Leadership changes within the ruling party could alter the tempo of infrastructure spending or real estate deregulation, affecting project timelines and land-use rules.

Geopolitical tensions affecting supply chains

Ongoing trade frictions and regional instability in East Asia have raised input costs for building maintenance and upgrades by an estimated 6–9% in 2024, disrupting procurement of HVAC parts and raw materials; AI Holdings faces political complexity sourcing electronic components for security and smart-building systems, where semiconductor and sensor shortages pushed prices up 12% YoY in 2024; diversifying suppliers across Southeast Asia and Mexico is now a strategic necessity to mitigate sanctions and trade-barrier risks.

Incentives for regional revitalization

The Japanese government intensified regional revitalization policies in 2024, allocating about ¥1.2 trillion to local revitalization funds and offering tax breaks up to 30% for property investment in secondary cities; AI Holdings can capture these subsidies to lower capex and OPEX for regional projects. Aligning strategy with the 2025 Regional Revitalization Plan enables access to government-backed contracts—municipal procurement in 2024 rose 8.5% year-on-year—opening new market segments outside Tokyo. Leveraging these incentives can improve ROI on regional assets and accelerate expansion into underpenetrated prefectures with aging populations and high vacancy rates.

Inbound tourism promotion policies

Government targets to reach 60 million annual foreign visitors by 2026 boost demand for commercial and hospitality real estate, increasing Japan hotel RevPAR by ~18% from 2022–2024 and benefiting AI Holdings' asset values.

Political support for renovating aging facilities with subsidies and tax incentives aids AI Holdings in upgrading properties to international standards, lowering capex payback periods by an estimated 12%.

Simplified visa rules and infrastructure spending (¥5.5 trillion 2023–2026 pipeline) correlate with higher occupancy—managed-property occupancy rose to ~78% in 2024.

- 60 million visitor target by 2026; RevPAR +18% (2022–24)

- ¥5.5 trillion tourism infrastructure spend (2023–26)

- Occupancy ~78% in 2024; capex payback improvement ~12%

Energy security and national defense alignment

Political pressure to cut imported fossil fuels has driven mandates raising building efficiency standards—EU Fit for 55 and U.S. federal targets aim for 55% emissions cuts by 2030; AI Holdings must retrofit assets to comply.

AI Holdings must align maintenance with national energy-security goals by prioritizing solar PV integration and high-efficiency HVAC—commercial heat pump adoption rose 28% in 2024, lowering energy use by ~30% per site.

Shifts toward domestic energy production change regulatory requirements for managed real estate, with incentives (e.g., 2024 tax credits covering up to 30% of qualifying clean-energy upgrades) affecting CAPEX and ROI models.

- Comply with stricter efficiency mandates tied to national targets (e.g., 55% emissions reduction by 2030).

- Prioritize solar and high-efficiency HVAC; heat pump adoption +28% in 2024, ~30% site energy reduction.

- Leverage incentives—up to 30% tax credits in 2024—when modeling CAPEX and ROI for retrofits.

Japan’s ¥12.4T DX & tourism surge fuels AI Holdings retrofits amid rising input costs

Japan's 2025 pro-DX and regional revitalization policies (¥12.4T DX budget; ¥1.2T local funds) and tourism push (60M visitors target by 2026) boost demand for AI Holdings' smart, retrofitted assets; trade tensions raised 2024 input costs 6–12%, driving supplier diversification; energy mandates (≈55% emissions cut by 2030) and 2024 tax credits up to 30% reshape CAPEX/ROI.

| Metric | Value |

|---|---|

| DX budget 2025 | ¥12.4T |

| Local funds 2024 | ¥1.2T |

| Tourist target | 60M by 2026 |

| Input cost rise 2024 | 6–12% |

| Tax credits 2024 | up to 30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ai Holdings across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current market and regulatory dynamics to identify risks and opportunities relevant to its industry and region.

Concise PESTLE summary tailored for Ai Holdings that highlights external risks and opportunities in plain language, ready to drop into presentations or share across teams for rapid alignment during strategic planning.

Economic factors

Interest rate environment and monetary policy

As the Bank of Japan began tightening in 2024–25,10-year JGB yields rose from near zero to about 0.6% by Jan 2025, raising borrowing costs for real estate acquisitions and pressuring AI Holdings to refinance at higher rates.

Labor shortages and rising wage costs

Japan faces a shortage of 720,000 skilled construction workers in 2024, driving sector wages up about 4.5% year-on-year; AI Holdings must absorb higher operating costs as technician and property manager supply tightens.

Competing for a shrinking talent pool risks service quality and turnover; labor cost increases contributed to a 2–3% gross margin compression across peers in 2023–24.

Economic strategy should prioritize productivity gains and automation: investing in robotics, AI-enabled maintenance and remote monitoring can cut labor hours per site by an estimated 20–30% based on industry pilots in 2024.

Inflationary pressures on maintenance materials

Global and domestic inflation lifted construction material costs by roughly 12–18% in 2023–2024 and energy prices spiked ~20% YoY, raising AI Holdings’ spare-parts and maintenance outlays; with CPI near 4.5% (2025 prelim.), the firm faces pressure to either absorb costs or pass them via lease escalations and service fee increases—a strategy constrained by market rent growth of ~3–5% and tenant affordability, complicating margin management amid ongoing input volatility.

Real estate market valuation trends

The economic health of Japan's commercial real estate shapes AI Holdings' asset strategy; Tokyo office yields compressed to ~2.5% in 2025 while vacancy in secondary cities rose to 8.2% as of Q4 2024, signaling selective reinvestment and repositioning.

Prime urban demand remains strong—average prime rent growth +3.1% YoY in 2024—while secondary markets show rental decline (-1.7% YoY) and higher turnover, affecting cash flow forecasts.

Manufacturing slowdown (industrial output -0.4% in 2024) and service sector growth (+1.8%) shift demand between logistics, office, and retail assets across the portfolio.

- Tokyo prime yields ~2.5% (2025); secondary vacancy 8.2% (Q4 2024)

- Prime rent +3.1% YoY (2024); secondary rent -1.7% YoY

- Industrial output -0.4% (2024); services +1.8% (2024)

Fluctuations in the Japanese Yen

Fluctuations in the Japanese Yen drive costs for imported tech and materials critical to modern building maintenance; a 10% depreciation in 2022–2024 raised import costs by roughly the same magnitude, increasing procurement expenses for IoT sensors and energy-efficient HVAC units for AI Holdings.

A weaker Yen makes high-end security systems and green hardware costlier—overseas security equipment prices rose ~8% YoY in 2024—while concurrently making Japanese real estate more attractive to foreign capital, with non-resident investment into Japan's property sector up about 15% in 2023–2024, potentially boosting AI Holdings’ management and leasing revenue.

- Import cost sensitivity: ≈10% Yen depreciation → ~10% higher tech/material costs

- Security/energy hardware price jump: ≈8% YoY (2024)

- Foreign property inflows: +15% into Japanese real estate (2023–2024)

Inflation, rising yields and costs squeeze margins as prime Tokyo assets diverge

Rising JGB yields (~0.6% Jan 2025) and CPI ~4.5% (2025 prelim.) raise refinancing and operating costs; construction wages +4.5% (2024) and materials +12–18% (2023–24) squeeze margins. Prime rent +3.1% (2024) vs secondary -1.7% and Tokyo prime yield ~2.5% (2025) force selective asset strategies; Yen depreciation (~10% since 2022) lifted imported tech costs ≈10% while foreign property inflows +15% (2023–24).

| Metric | Value |

|---|---|

| JGB 10y | ~0.6% (Jan 2025) |

| CPI | ~4.5% (2025 prelim.) |

| Construction wages | +4.5% (2024) |

| Materials | +12–18% (2023–24) |

| Tokyo prime yield | ~2.5% (2025) |

| Prime/secondary rent | +3.1% / -1.7% (2024) |

| Yen depreciation | ~10% (2022–24) |

| Foreign inflows | +15% (2023–24) |

Same Document Delivered

Ai Holdings PESTLE Analysis

The preview shown here is the exact Ai Holdings PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are reshaping Ai Holdings’ prospects—our concise PESTLE highlights key risks and opportunities to inform smarter decisions. Purchase the full, ready-to-use analysis for detailed insights, data-driven scenarios, and editable charts to fast-track your investment or strategy work.

Political factors

Japanese government stability and policy continuity

As of late 2025 Japan's political agenda emphasizes economic revitalization and structural reform, with the government allocating ¥12.4 trillion in the 2025 budget to digital transformation and urban development initiatives. For AI Holdings, continued public backing for urban redevelopment and smart-city projects—part of a ¥5.6 trillion multi-year infrastructure plan—supports stable long-term planning. Leadership changes within the ruling party could alter the tempo of infrastructure spending or real estate deregulation, affecting project timelines and land-use rules.

Geopolitical tensions affecting supply chains

Ongoing trade frictions and regional instability in East Asia have raised input costs for building maintenance and upgrades by an estimated 6–9% in 2024, disrupting procurement of HVAC parts and raw materials; AI Holdings faces political complexity sourcing electronic components for security and smart-building systems, where semiconductor and sensor shortages pushed prices up 12% YoY in 2024; diversifying suppliers across Southeast Asia and Mexico is now a strategic necessity to mitigate sanctions and trade-barrier risks.

Incentives for regional revitalization

The Japanese government intensified regional revitalization policies in 2024, allocating about ¥1.2 trillion to local revitalization funds and offering tax breaks up to 30% for property investment in secondary cities; AI Holdings can capture these subsidies to lower capex and OPEX for regional projects. Aligning strategy with the 2025 Regional Revitalization Plan enables access to government-backed contracts—municipal procurement in 2024 rose 8.5% year-on-year—opening new market segments outside Tokyo. Leveraging these incentives can improve ROI on regional assets and accelerate expansion into underpenetrated prefectures with aging populations and high vacancy rates.

Inbound tourism promotion policies

Government targets to reach 60 million annual foreign visitors by 2026 boost demand for commercial and hospitality real estate, increasing Japan hotel RevPAR by ~18% from 2022–2024 and benefiting AI Holdings' asset values.

Political support for renovating aging facilities with subsidies and tax incentives aids AI Holdings in upgrading properties to international standards, lowering capex payback periods by an estimated 12%.

Simplified visa rules and infrastructure spending (¥5.5 trillion 2023–2026 pipeline) correlate with higher occupancy—managed-property occupancy rose to ~78% in 2024.

- 60 million visitor target by 2026; RevPAR +18% (2022–24)

- ¥5.5 trillion tourism infrastructure spend (2023–26)

- Occupancy ~78% in 2024; capex payback improvement ~12%

Energy security and national defense alignment

Political pressure to cut imported fossil fuels has driven mandates raising building efficiency standards—EU Fit for 55 and U.S. federal targets aim for 55% emissions cuts by 2030; AI Holdings must retrofit assets to comply.

AI Holdings must align maintenance with national energy-security goals by prioritizing solar PV integration and high-efficiency HVAC—commercial heat pump adoption rose 28% in 2024, lowering energy use by ~30% per site.

Shifts toward domestic energy production change regulatory requirements for managed real estate, with incentives (e.g., 2024 tax credits covering up to 30% of qualifying clean-energy upgrades) affecting CAPEX and ROI models.

- Comply with stricter efficiency mandates tied to national targets (e.g., 55% emissions reduction by 2030).

- Prioritize solar and high-efficiency HVAC; heat pump adoption +28% in 2024, ~30% site energy reduction.

- Leverage incentives—up to 30% tax credits in 2024—when modeling CAPEX and ROI for retrofits.

Japan’s ¥12.4T DX & tourism surge fuels AI Holdings retrofits amid rising input costs

Japan's 2025 pro-DX and regional revitalization policies (¥12.4T DX budget; ¥1.2T local funds) and tourism push (60M visitors target by 2026) boost demand for AI Holdings' smart, retrofitted assets; trade tensions raised 2024 input costs 6–12%, driving supplier diversification; energy mandates (≈55% emissions cut by 2030) and 2024 tax credits up to 30% reshape CAPEX/ROI.

| Metric | Value |

|---|---|

| DX budget 2025 | ¥12.4T |

| Local funds 2024 | ¥1.2T |

| Tourist target | 60M by 2026 |

| Input cost rise 2024 | 6–12% |

| Tax credits 2024 | up to 30% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ai Holdings across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current market and regulatory dynamics to identify risks and opportunities relevant to its industry and region.

Concise PESTLE summary tailored for Ai Holdings that highlights external risks and opportunities in plain language, ready to drop into presentations or share across teams for rapid alignment during strategic planning.

Economic factors

Interest rate environment and monetary policy

As the Bank of Japan began tightening in 2024–25,10-year JGB yields rose from near zero to about 0.6% by Jan 2025, raising borrowing costs for real estate acquisitions and pressuring AI Holdings to refinance at higher rates.

Labor shortages and rising wage costs

Japan faces a shortage of 720,000 skilled construction workers in 2024, driving sector wages up about 4.5% year-on-year; AI Holdings must absorb higher operating costs as technician and property manager supply tightens.

Competing for a shrinking talent pool risks service quality and turnover; labor cost increases contributed to a 2–3% gross margin compression across peers in 2023–24.

Economic strategy should prioritize productivity gains and automation: investing in robotics, AI-enabled maintenance and remote monitoring can cut labor hours per site by an estimated 20–30% based on industry pilots in 2024.

Inflationary pressures on maintenance materials

Global and domestic inflation lifted construction material costs by roughly 12–18% in 2023–2024 and energy prices spiked ~20% YoY, raising AI Holdings’ spare-parts and maintenance outlays; with CPI near 4.5% (2025 prelim.), the firm faces pressure to either absorb costs or pass them via lease escalations and service fee increases—a strategy constrained by market rent growth of ~3–5% and tenant affordability, complicating margin management amid ongoing input volatility.

Real estate market valuation trends

The economic health of Japan's commercial real estate shapes AI Holdings' asset strategy; Tokyo office yields compressed to ~2.5% in 2025 while vacancy in secondary cities rose to 8.2% as of Q4 2024, signaling selective reinvestment and repositioning.

Prime urban demand remains strong—average prime rent growth +3.1% YoY in 2024—while secondary markets show rental decline (-1.7% YoY) and higher turnover, affecting cash flow forecasts.

Manufacturing slowdown (industrial output -0.4% in 2024) and service sector growth (+1.8%) shift demand between logistics, office, and retail assets across the portfolio.

- Tokyo prime yields ~2.5% (2025); secondary vacancy 8.2% (Q4 2024)

- Prime rent +3.1% YoY (2024); secondary rent -1.7% YoY

- Industrial output -0.4% (2024); services +1.8% (2024)

Fluctuations in the Japanese Yen

Fluctuations in the Japanese Yen drive costs for imported tech and materials critical to modern building maintenance; a 10% depreciation in 2022–2024 raised import costs by roughly the same magnitude, increasing procurement expenses for IoT sensors and energy-efficient HVAC units for AI Holdings.

A weaker Yen makes high-end security systems and green hardware costlier—overseas security equipment prices rose ~8% YoY in 2024—while concurrently making Japanese real estate more attractive to foreign capital, with non-resident investment into Japan's property sector up about 15% in 2023–2024, potentially boosting AI Holdings’ management and leasing revenue.

- Import cost sensitivity: ≈10% Yen depreciation → ~10% higher tech/material costs

- Security/energy hardware price jump: ≈8% YoY (2024)

- Foreign property inflows: +15% into Japanese real estate (2023–2024)

Inflation, rising yields and costs squeeze margins as prime Tokyo assets diverge

Rising JGB yields (~0.6% Jan 2025) and CPI ~4.5% (2025 prelim.) raise refinancing and operating costs; construction wages +4.5% (2024) and materials +12–18% (2023–24) squeeze margins. Prime rent +3.1% (2024) vs secondary -1.7% and Tokyo prime yield ~2.5% (2025) force selective asset strategies; Yen depreciation (~10% since 2022) lifted imported tech costs ≈10% while foreign property inflows +15% (2023–24).

| Metric | Value |

|---|---|

| JGB 10y | ~0.6% (Jan 2025) |

| CPI | ~4.5% (2025 prelim.) |

| Construction wages | +4.5% (2024) |

| Materials | +12–18% (2023–24) |

| Tokyo prime yield | ~2.5% (2025) |

| Prime/secondary rent | +3.1% / -1.7% (2024) |

| Yen depreciation | ~10% (2022–24) |

| Foreign inflows | +15% (2023–24) |

Same Document Delivered

Ai Holdings PESTLE Analysis

The preview shown here is the exact Ai Holdings PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without edits.