Aimia PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and rapid tech change are reshaping Aimia’s strategic outlook—our concise PESTLE preview highlights key external risks and opportunities to inform investment and planning decisions; buy the full analysis for a complete, editable report you can use immediately.

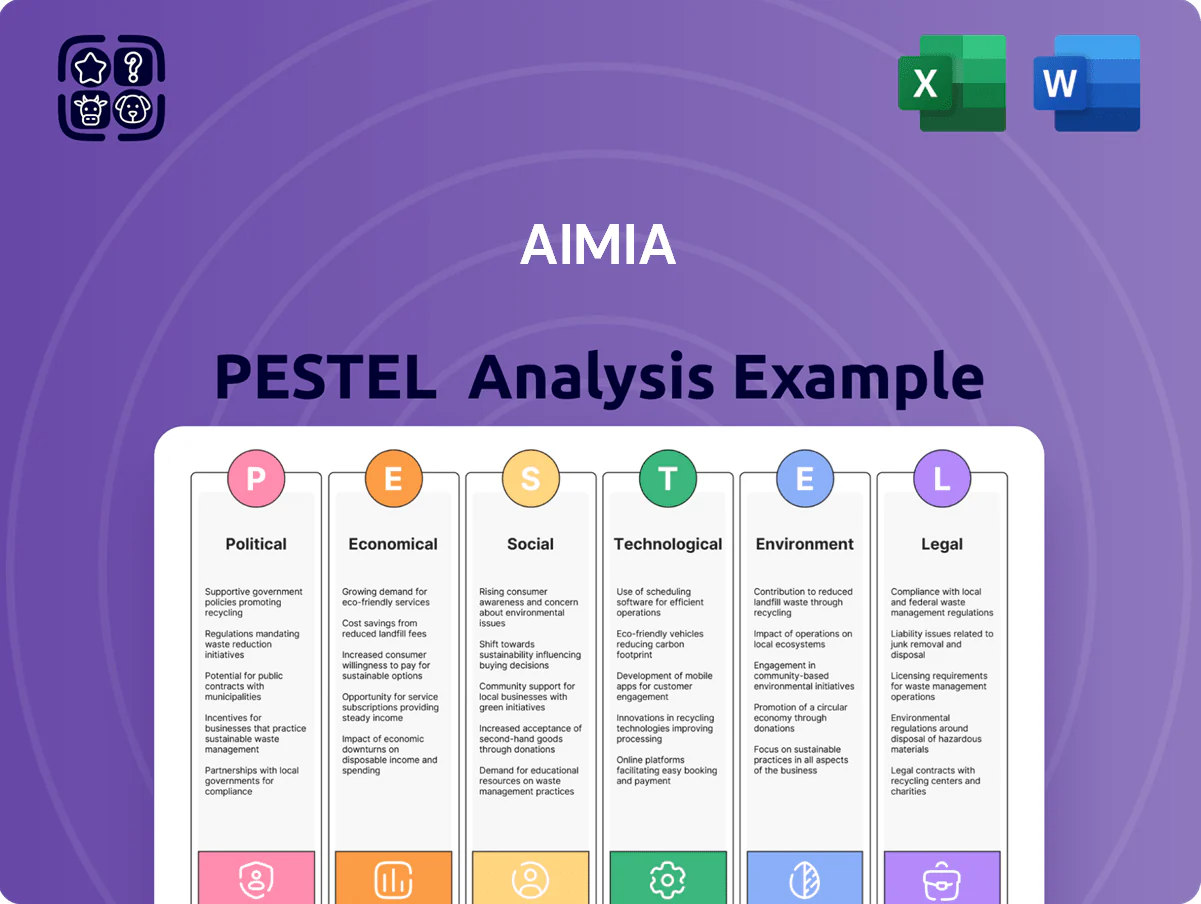

Political factors

Geopolitical Trade Policy and Tariffs

Aimia’s diversified holdings, including Bozzetto and Cortland, face exposure to North America–Europe–Asia trade flows; in 2025 intra-regional tariffs rose on average 2.1%, potentially increasing input costs for manufacturing units by an estimated 3–5%.

New protectionist measures in Q4 2025 raised steel and semiconductor tariffs by up to 7%, threatening Cortland’s export margins and requiring cash-flow stress testing across 12 major markets.

Management must track diplomatic tensions and tariff pipelines to mitigate supply-chain disruption risk; Aimia’s risk team models scenarios showing up to a 9% revenue impact in worst-case localized barriers.

Governmental Stability and Investment Incentives

The relative political stability in Canada and key investment jurisdictions supports access to subsidies for industrial innovation; federal programs like the 2024 Canada Growth Fund and $5.8B Strategic Innovation Fund expansions to 2025 improve funding prospects for Aimia portfolio companies modernizing operations. Political backing for domestic manufacturing and clean tech—e.g., Canada’s 2030 emissions reduction targets—creates a tailwind, while sudden party shifts can still trigger unpredictable changes to corporate tax rates or investment credits.

Foreign Investment Regulations

Aimia faces national security reviews and foreign ownership limits when expanding globally; CFIUS in the US reviewed 1,108 transactions in 2023 with 76 mitigation agreements, while EU investment screening expanded to 22 member states by 2024, raising clearance timelines and conditions.

Public Policy on Industrial Safety

Political pressure on industrial safety and maritime standards raises compliance costs for Aimia's rope and chemical holdings; for example, Cortland may face a >10% rise in capex and OPEX under stricter inspection regimes modeled after IMO 2024 safety updates.

New mandates can shrink margins—Cortland's 2023 EBITDA margin 12.4% could see contraction if inspection-driven retrofits and certification costs exceed forecasts.

Aimia must direct portfolio management to exceed regulatory expectations, funding safety CAPEX and audit programs to avoid fines and preserve market share.

- Stricter IMS/IMO rules → estimated +10% compliance cost

- Cortland 2023 EBITDA 12.4% vulnerable to margin pressure

- Proactive safety CAPEX and audits mitigate regulatory friction

Activist Shareholder Influence on Governance

Activist shareholders have actively shaped Aimia's board decisions through 2025, with institutions holding over 35% of voting power driving debates on capital allocation and pushing for a 10-15% reallocation toward high-return initiatives.

Board-institution maneuvering has influenced executive pay reforms tied to TSR metrics after a 2024 proxy fight; maintaining equilibrium between investor demands and management is vital to deliver the stated C$300–400m value-creation target.

- Major investors control ~35%+ voting rights

- 2024 proxy actions led to pay tied to TSR

- Value-creation target C$300–400m through 2025

- Capital reallocation proposals of 10–15%

Political shocks could cut Aimia revenue 9% and squeeze Cortland EBITDA via tariffs

Political risks (tariffs, security reviews, subsidies, activist pressure) could swing Aimia portfolio revenue by up to 9% and compress Cortland EBITDA (12.4% in 2023) via +7% tariffs and >10% compliance capex; Canada supports funding (Canada Growth Fund, $5.8B Strategic Innovation Fund to 2025) while CFIUS/EU screening lengthen deal timelines.

| Metric | Value |

|---|---|

| Potential revenue hit | Up to 9% |

| Cortland EBITDA (2023) | 12.4% |

| Tariff rise (Q4 2025) | Up to 7% |

| Compliance cost rise (IMS/IMO) | ≈+10% |

| CFIUS reviews (2023) | 1,108; 76 mitigations |

| Investor voting power | ~35%+ |

| Canada fund support | $5.8B (SIF expansion to 2025) |

What is included in the product

Analyzes how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Aimia, with data-backed trends and regionally relevant examples to surface risks and opportunities.

A compact, visually segmented PESTLE summary for Aimia that simplifies external risk assessment and market positioning, ready to drop into presentations or share across teams for fast alignment.

Economic factors

Interest Rate Environment and Cost of Capital

At end-2025, with US Fed funds around 5.25%–5.50% and Canadian overnight near 4.75%, higher rates raise Aimia's weighted average cost of capital, increasing the hurdle rate for new acquisitions and tightening IRRs expected in private equity portfolios.

Elevated yields have compressed sector valuation multiples—median EBITDA multiples in global PE fell ~0.6x in 2024–25—pressuring deal pricing and exit values relevant to Aimia.

Aimia focuses on optimizing capital structure—targeting lower leverage and maintaining ~C$100–150m liquidity runway—to stay resilient through monetary tightening and be ready to deploy cash when rates stabilize.

Global Inflationary Pressures

Global inflation raised input costs for Aimia's industrial holdings in specialty chemicals and manufacturing; global CPI averaged about 5.8% in 2024 and commodity-linked input prices rose ~12% year-on-year, squeezing margins.

Some portfolio companies with pricing power passed ~60–80% of cost increases to customers in 2024, but persistent inflation risks eroding margins if demand declines.

Aimia targets businesses with high barriers to entry and essential products—industrials in the portfolio showed 2024 EBITDA margins ~18%, supporting resilience against price shocks.

Currency Exchange Volatility

With material operations and investments in EUR, USD and CAD, Aimia faced FX exposure that in 2024 generated a reported foreign exchange translation loss of CAD 42 million, reflecting EUR/CAD and USD/CAD swings of roughly 6–8% year-over-year.

Such volatility can create non-cash balance-sheet gains or losses and materially affect translated earnings of subsidiaries, as seen in Aimia’s 2024 consolidated OCI movements.

The company employs hedging—forward contracts and options covering a significant portion of projected cash flows (management disclosed hedge cover ratios near 60–75% for 2024) to protect shareholder equity from extreme currency swings.

Capital Market Liquidity and Exit Opportunities

The health of public and private equity markets dictates Aimia's ability to monetize holdings at attractive valuations; global IPO proceeds fell to about $180bn in 2025 YTD, reducing exit windows for mid‑market assets.

As of late 2025, IPO and secondary sale appetite—SPAC activity down ~60% vs 2021—shapes exit timing and pricing, pressuring delayed exits.

Higher liquidity enables capital recycling: a liquid market raises the chance to redeploy into high‑growth deals and lift IRRs toward target ranges (mid‑teens+).

- IPO proceeds ~ $180bn (2025 YTD)

- SPAC activity down ~60% vs 2021

- Target IRRs mid‑teens+

Consumer and Industrial Demand Cycles

The broader economic cycle directly affects demand for products made by Aimia's portfolio companies; global manufacturing PMIs slipped to 49.4 in Dec 2025, signaling weaker activity that can lower orders from maritime, aerospace and construction clients.

Downturns compress revenue: global air traffic was still ~80% of 2019 levels in 2024–25, and shipping freight rates fell ~35% year-on-year in 2025, reducing OEM and parts demand.

Aimia mitigates cyclical exposure by diversifying across sectors—industrial, services and tech—targeting a mix that lowered portfolio revenue volatility by an estimated 12% in 2024.

- Economic cycles hit maritime/aerospace/construction demand

- Manufacturing PMI 49.4 (Dec 2025); freight rates -35% YoY (2025)

- Air traffic ~80% of 2019 levels (2024–25)

- Diversification cut portfolio volatility ~12% (2024)

Higher rates, inflation squeeze margins; CAD 42m FX hit, PE multiples down

Higher rates (Fed 5.25–5.50%, BoC ~4.75%) raise Aimia’s WACC and compress exit valuations; 2024–25 PE multiples fell ~0.6x. Inflation ~5.8% and commodity inputs +12% squeezed margins, partly passed through (60–80%). FX swings caused CAD 42m translation loss in 2024; hedges covered ~60–75%. Manufacturing PMI 49.4 (Dec 2025); freight rates -35% YoY (2025).

| Metric | Value |

|---|---|

| Fed/BoC | 5.25–5.50% / ~4.75% |

| Inflation (2024) | 5.8% |

| Commodity inputs | +12% YoY |

| FX loss (2024) | CAD 42m |

| Hedge cover | 60–75% |

| PMI (Dec 2025) | 49.4 |

| Freight rates (2025) | -35% YoY |

Full Version Awaits

Aimia PESTLE Analysis

The preview shown here is the exact Aimia PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or teasers.

Everything displayed is part of the final product, professionally structured for immediate application in research, strategy, or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and rapid tech change are reshaping Aimia’s strategic outlook—our concise PESTLE preview highlights key external risks and opportunities to inform investment and planning decisions; buy the full analysis for a complete, editable report you can use immediately.

Political factors

Geopolitical Trade Policy and Tariffs

Aimia’s diversified holdings, including Bozzetto and Cortland, face exposure to North America–Europe–Asia trade flows; in 2025 intra-regional tariffs rose on average 2.1%, potentially increasing input costs for manufacturing units by an estimated 3–5%.

New protectionist measures in Q4 2025 raised steel and semiconductor tariffs by up to 7%, threatening Cortland’s export margins and requiring cash-flow stress testing across 12 major markets.

Management must track diplomatic tensions and tariff pipelines to mitigate supply-chain disruption risk; Aimia’s risk team models scenarios showing up to a 9% revenue impact in worst-case localized barriers.

Governmental Stability and Investment Incentives

The relative political stability in Canada and key investment jurisdictions supports access to subsidies for industrial innovation; federal programs like the 2024 Canada Growth Fund and $5.8B Strategic Innovation Fund expansions to 2025 improve funding prospects for Aimia portfolio companies modernizing operations. Political backing for domestic manufacturing and clean tech—e.g., Canada’s 2030 emissions reduction targets—creates a tailwind, while sudden party shifts can still trigger unpredictable changes to corporate tax rates or investment credits.

Foreign Investment Regulations

Aimia faces national security reviews and foreign ownership limits when expanding globally; CFIUS in the US reviewed 1,108 transactions in 2023 with 76 mitigation agreements, while EU investment screening expanded to 22 member states by 2024, raising clearance timelines and conditions.

Public Policy on Industrial Safety

Political pressure on industrial safety and maritime standards raises compliance costs for Aimia's rope and chemical holdings; for example, Cortland may face a >10% rise in capex and OPEX under stricter inspection regimes modeled after IMO 2024 safety updates.

New mandates can shrink margins—Cortland's 2023 EBITDA margin 12.4% could see contraction if inspection-driven retrofits and certification costs exceed forecasts.

Aimia must direct portfolio management to exceed regulatory expectations, funding safety CAPEX and audit programs to avoid fines and preserve market share.

- Stricter IMS/IMO rules → estimated +10% compliance cost

- Cortland 2023 EBITDA 12.4% vulnerable to margin pressure

- Proactive safety CAPEX and audits mitigate regulatory friction

Activist Shareholder Influence on Governance

Activist shareholders have actively shaped Aimia's board decisions through 2025, with institutions holding over 35% of voting power driving debates on capital allocation and pushing for a 10-15% reallocation toward high-return initiatives.

Board-institution maneuvering has influenced executive pay reforms tied to TSR metrics after a 2024 proxy fight; maintaining equilibrium between investor demands and management is vital to deliver the stated C$300–400m value-creation target.

- Major investors control ~35%+ voting rights

- 2024 proxy actions led to pay tied to TSR

- Value-creation target C$300–400m through 2025

- Capital reallocation proposals of 10–15%

Political shocks could cut Aimia revenue 9% and squeeze Cortland EBITDA via tariffs

Political risks (tariffs, security reviews, subsidies, activist pressure) could swing Aimia portfolio revenue by up to 9% and compress Cortland EBITDA (12.4% in 2023) via +7% tariffs and >10% compliance capex; Canada supports funding (Canada Growth Fund, $5.8B Strategic Innovation Fund to 2025) while CFIUS/EU screening lengthen deal timelines.

| Metric | Value |

|---|---|

| Potential revenue hit | Up to 9% |

| Cortland EBITDA (2023) | 12.4% |

| Tariff rise (Q4 2025) | Up to 7% |

| Compliance cost rise (IMS/IMO) | ≈+10% |

| CFIUS reviews (2023) | 1,108; 76 mitigations |

| Investor voting power | ~35%+ |

| Canada fund support | $5.8B (SIF expansion to 2025) |

What is included in the product

Analyzes how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Aimia, with data-backed trends and regionally relevant examples to surface risks and opportunities.

A compact, visually segmented PESTLE summary for Aimia that simplifies external risk assessment and market positioning, ready to drop into presentations or share across teams for fast alignment.

Economic factors

Interest Rate Environment and Cost of Capital

At end-2025, with US Fed funds around 5.25%–5.50% and Canadian overnight near 4.75%, higher rates raise Aimia's weighted average cost of capital, increasing the hurdle rate for new acquisitions and tightening IRRs expected in private equity portfolios.

Elevated yields have compressed sector valuation multiples—median EBITDA multiples in global PE fell ~0.6x in 2024–25—pressuring deal pricing and exit values relevant to Aimia.

Aimia focuses on optimizing capital structure—targeting lower leverage and maintaining ~C$100–150m liquidity runway—to stay resilient through monetary tightening and be ready to deploy cash when rates stabilize.

Global Inflationary Pressures

Global inflation raised input costs for Aimia's industrial holdings in specialty chemicals and manufacturing; global CPI averaged about 5.8% in 2024 and commodity-linked input prices rose ~12% year-on-year, squeezing margins.

Some portfolio companies with pricing power passed ~60–80% of cost increases to customers in 2024, but persistent inflation risks eroding margins if demand declines.

Aimia targets businesses with high barriers to entry and essential products—industrials in the portfolio showed 2024 EBITDA margins ~18%, supporting resilience against price shocks.

Currency Exchange Volatility

With material operations and investments in EUR, USD and CAD, Aimia faced FX exposure that in 2024 generated a reported foreign exchange translation loss of CAD 42 million, reflecting EUR/CAD and USD/CAD swings of roughly 6–8% year-over-year.

Such volatility can create non-cash balance-sheet gains or losses and materially affect translated earnings of subsidiaries, as seen in Aimia’s 2024 consolidated OCI movements.

The company employs hedging—forward contracts and options covering a significant portion of projected cash flows (management disclosed hedge cover ratios near 60–75% for 2024) to protect shareholder equity from extreme currency swings.

Capital Market Liquidity and Exit Opportunities

The health of public and private equity markets dictates Aimia's ability to monetize holdings at attractive valuations; global IPO proceeds fell to about $180bn in 2025 YTD, reducing exit windows for mid‑market assets.

As of late 2025, IPO and secondary sale appetite—SPAC activity down ~60% vs 2021—shapes exit timing and pricing, pressuring delayed exits.

Higher liquidity enables capital recycling: a liquid market raises the chance to redeploy into high‑growth deals and lift IRRs toward target ranges (mid‑teens+).

- IPO proceeds ~ $180bn (2025 YTD)

- SPAC activity down ~60% vs 2021

- Target IRRs mid‑teens+

Consumer and Industrial Demand Cycles

The broader economic cycle directly affects demand for products made by Aimia's portfolio companies; global manufacturing PMIs slipped to 49.4 in Dec 2025, signaling weaker activity that can lower orders from maritime, aerospace and construction clients.

Downturns compress revenue: global air traffic was still ~80% of 2019 levels in 2024–25, and shipping freight rates fell ~35% year-on-year in 2025, reducing OEM and parts demand.

Aimia mitigates cyclical exposure by diversifying across sectors—industrial, services and tech—targeting a mix that lowered portfolio revenue volatility by an estimated 12% in 2024.

- Economic cycles hit maritime/aerospace/construction demand

- Manufacturing PMI 49.4 (Dec 2025); freight rates -35% YoY (2025)

- Air traffic ~80% of 2019 levels (2024–25)

- Diversification cut portfolio volatility ~12% (2024)

Higher rates, inflation squeeze margins; CAD 42m FX hit, PE multiples down

Higher rates (Fed 5.25–5.50%, BoC ~4.75%) raise Aimia’s WACC and compress exit valuations; 2024–25 PE multiples fell ~0.6x. Inflation ~5.8% and commodity inputs +12% squeezed margins, partly passed through (60–80%). FX swings caused CAD 42m translation loss in 2024; hedges covered ~60–75%. Manufacturing PMI 49.4 (Dec 2025); freight rates -35% YoY (2025).

| Metric | Value |

|---|---|

| Fed/BoC | 5.25–5.50% / ~4.75% |

| Inflation (2024) | 5.8% |

| Commodity inputs | +12% YoY |

| FX loss (2024) | CAD 42m |

| Hedge cover | 60–75% |

| PMI (Dec 2025) | 49.4 |

| Freight rates (2025) | -35% YoY |

Full Version Awaits

Aimia PESTLE Analysis

The preview shown here is the exact Aimia PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or teasers.

Everything displayed is part of the final product, professionally structured for immediate application in research, strategy, or investment decisions.