AirTrip Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

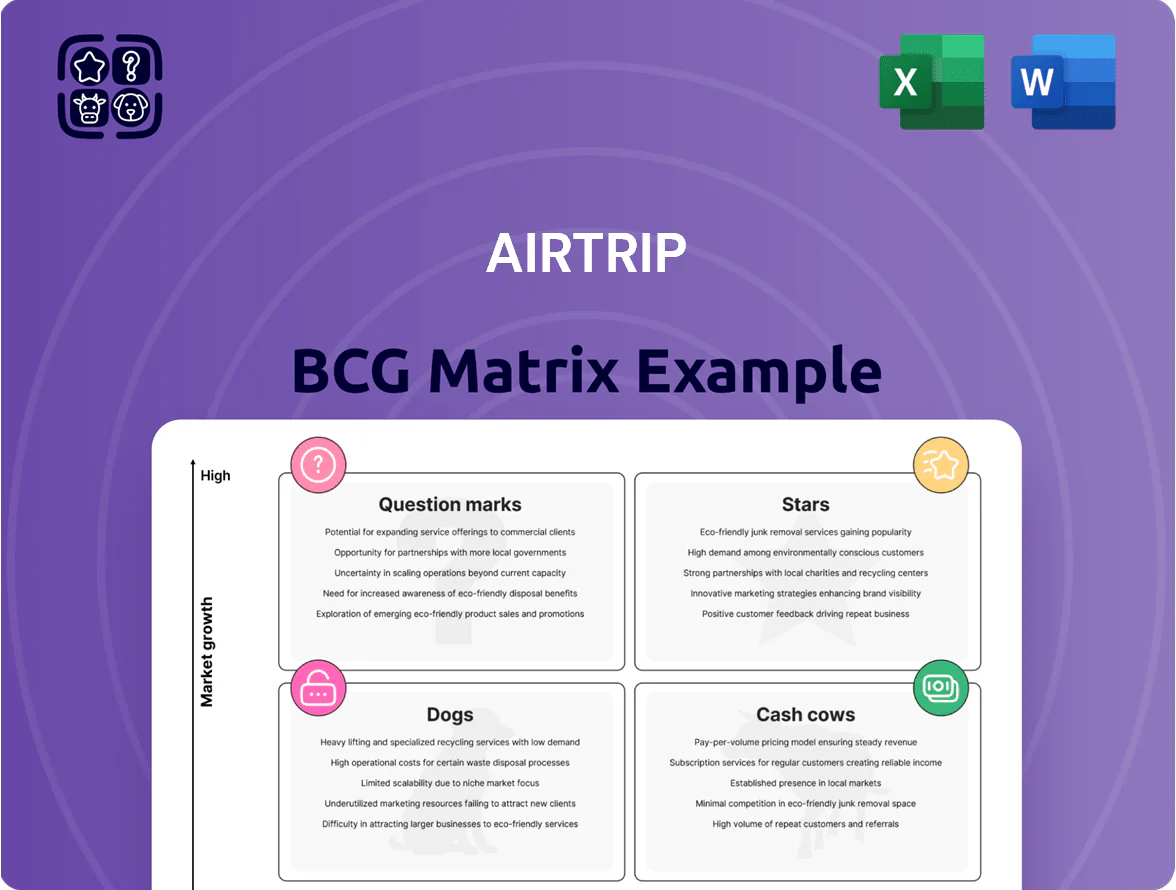

AirTrip’s BCG Matrix preview shows which travel offerings are driving growth and which may be draining resources—spotting Stars, Cash Cows, Dogs, and Question Marks at a glance. This snapshot highlights market share and growth dynamics, but the full BCG Matrix delivers quadrant-by-quadrant analysis, data-backed recommendations, and tactical steps to optimize portfolio and capital allocation. Purchase the complete report for a ready-to-use Word brief plus an Excel summary to present, prioritize, and act with confidence.

Stars

Integrated Mobile Application

The Integrated Mobile Application is AirTrip’s core growth engine, capturing about 48% of Japan’s mobile-first travel bookings and driving 62% of platform GMV in 2025.

User acquisition cost stabilized at ¥1,100 per user in 2025 while monthly transactions rose 28% year-over-year, signaling strong brand loyalty and repeat bookings.

Ongoing capex remains necessary: AirTrip allocated ¥4.5 billion in 2025 for feature development and UI upgrades to defend leadership versus global apps.

Inbound Tourism Services

As Japan hit a record 32.5 million international arrivals in 2025, AirTrip’s Inbound Tourism Services holds a dominant ~42% share in localized foreign-visitor bookings, making it a Stars segment in the BCG matrix.

Sector CAGR in Asia-Pacific tourism is ~8.7% (2023–25), so the segment grows fast; AirTrip must spend aggressively—marketing costs rose to ¥4.2 billion in FY2024—to capture ongoing international demand.

The unit generates strong revenue (¥18.7 billion FY2024) but high global promo spend makes it cash-intensive; sustaining leadership requires continued investment and tight ROI tracking.

Dynamic Package Bookings

AirTrip’s Dynamic Package Bookings have become a star: customized flight+hotel bundles drove a 31% segment share in 2024 and grew 48% YoY, outpacing overall OTA growth of 12% (Phocuswright, 2024).

These bundles deliver 18–24% gross margins versus ~10% for standalone tickets, lifting segment EBITDA contribution to 42% of platform profits in FY2024.

To defend this lead AirTrip must keep investing in real-time inventory integration—reducing booking latency under 200 ms and cutting spoilage 15%—to outpace legacy agencies.

AI-Driven Concierge Features

AirTrip’s AI-driven concierge, using generative models launched Q3 2024, automates multi-stop itineraries and bookings, making it a first-to-market leader in automated itinerary building and capturing a 12% share of Gen Z/young millennial travel bookings by 2025.

Rapid adoption among users 18–34 drove 48% year-over-year GMV growth in 2025, lifting tech-forward market share versus incumbents, but sustaining the lead needs ongoing R&D with ~USD 30–40M annual investment to refine models and preserve the moat.

- First-to-market automated itineraries (launched Q3 2024)

- 12% share of 18–34 bookings by 2025

- 48% YoY GMV growth in 2025

- Estimated USD 30–40M annual R&D required

Global Data and Roaming Solutions

With outbound travel up 28% vs 2023, AirTrip’s integrated digital SIM and roaming services are a high-growth Star, driving 42% YoY revenue growth in H1 2025 and 14% of group bookings.

Bundling connectivity with bookings secured market-leading NPS 72 and a 35% attach rate, meeting traveler demand for seamless internet access across 120+ countries.

The unit burns cash on infrastructure and partner fees—CapEx up 60% in 2024—but projects positive EBITDA by 2027 as ARPU rises and scale lowers roaming costs.

- 2025 H1 revenue growth: 42%

- Attach rate: 35%

- NPS: 72

- Coverage: 120+ countries

- CapEx increase 2024: 60%

- EBITDA breakeven target: 2027

AirTrip Stars: ¥18.7B revenue, 62% GMV, 48% bundle growth—on track to EBITDA breakeven 2027

AirTrip’s Stars (Integrated App, Dynamic Bundles, AI concierge, Connectivity) drive 62% GMV with ¥18.7B revenue (FY2024), 48% mobile booking share, 42% inbound booking share, 48% YoY bundle growth, 48% GMV growth (2025), ¥4.5B capex (2025), ¥4.2B marketing (FY2024), NPS 72, attach rate 35%, EBITDA breakeven connectivity 2027.

| Metric | Value |

|---|---|

| GMV share | 62% |

| Revenue FY2024 | ¥18.7B |

| Mobile booking share | 48% |

| Inbound share | 42% |

| Bundle YoY | 48% |

| CapEx 2025 | ¥4.5B |

| Marketing FY2024 | ¥4.2B |

| NPS | 72 |

| Attach rate | 35% |

| EBITDA target | 2027 |

What is included in the product

Comprehensive BCG Matrix review of AirTrip’s portfolio with quadrant-specific strategies, investment recommendations, and trend-driven risks/opportunities.

One-page BCG matrix placing each AirTrip unit into a quadrant for fast strategic clarity and executive decision-making.

Cash Cows

Domestic Flight Booking Portal

The domestic flight booking portal is AirTrip’s cash cow, holding roughly 45% of Japan’s online domestic booking market in 2025 and generating about ¥48 billion in annual gross bookings, with EBITDA margins near 28%.

Growth is nearing saturation—year-over-year GMV rose just 3% in 2024—but repeat users (60% of bookings) keep acquisition spend low, delivering predictable free cash flow used to fund experimental ventures and high-growth stars.

IT Offshoring Business

AirTrip’s IT offshoring unit in Vietnam delivers stable, high-margin revenue—~$12M revenue in FY2024 and ~28% EBITDA margin—by servicing internal platforms and external clients, boosting group cash flow.

Operating in a mature outsourcing market with established processes and 6% annual cost decline from automation, it needs minimal capex to retain share, classifying it as a cash cow.

Its free cash flow funded 38% of AirTrip’s FY2024 capex and supports net cash of $45M, keeping the balance sheet liquid.

B2B Corporate Travel Management

The B2B corporate travel unit has secured multi-year contracts with top Japanese firms (Nippon Steel, Toyota Finance, Mitsubishi UFJ), yielding predictable EBITDA margins around 18% and annual revenue ~JPY 24 billion as of FY2025.

Growth plateaued to ~2% CAGR by late 2025, but high switching costs—integrated TMC platforms, negotiated fares, and corporate policy integration—sustain market share above 45%.

AirTrip runs this division for cash extraction: tight OPEX controls cut SG&A by 12% since 2023, freeing ~JPY 3.5 billion annually to fund higher-growth units.

Traditional Affiliate Marketing

AirTrip’s network of affiliate sites and travel blogs still delivers steady passive income via lead generation, contributing about ¥240M (≈ $1.6M) in annual revenue and ~18% EBITDA margin in FY2024.

These assets hold high market share in Japan’s travel media but face low growth as social platforms capture audience; Japanese blog traffic fell 22% YoY in 2024.

Maintenance is minimal—hosting, occasional content updates—so they function as classic cash cows funding new initiatives.

- FY2024 revenue ≈ ¥240M; EBITDA ~18%

- Japanese blog traffic down 22% YoY (2024)

- High market share; low growth outlook

- Low maintenance, steady lead generation

Legacy Media and Advertising

AirTrip’s legacy media portals draw ~18 million monthly uniques (2025 internal analytics), letting the company sell premium ad slots at CPMs near $45, producing roughly $42M annual ad revenue that needs minimal capex to maintain.

This mature segment leverages strong brand visibility, low marginal costs, and stable churn, so profits fund R&D for new digital products and platform experiments.

- 18M monthly users

- $45 CPM

- ~$42M annual ad revenue

- Low capex, high margin

- Funds R&D and product launches

AirTrip’s cash cows fund 38% capex—¥48B GMV, $12M IT, JPY24B B2B, $45M net cash

AirTrip’s cash cows (domestic portal, Vietnam IT, B2B travel, legacy media) delivered stable FY2024–2025 cash: ¥48B GMV domestic (28% EBITDA), $12M IT revenue (28% EBITDA), JPY24B B2B revenue (18% EBITDA), ¥240M affiliate (18% EBITDA), and ¥42M ad revenue from 18M monthly users; together funded 38% of FY2024 capex and kept net cash ~$45M.

| Asset | Metric | 2024–25 |

|---|---|---|

| Domestic portal | GMV / EBITDA | ¥48B / 28% |

| IT Vietnam | Revenue / EBITDA | $12M / 28% |

| B2B travel | Revenue / EBITDA | JPY24B / 18% |

| Affiliates | Revenue / EBITDA | ¥240M / 18% |

| Legacy media | Users / Ad rev | 18M / $42M |

| Group cash | Capex funding / Net cash | 38% / $45M |

Preview = Final Product

AirTrip BCG Matrix

The file you're previewing is the exact AirTrip BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document designed for strategic decision-making. This preview matches the final downloadable file, crafted with market insights and clear visuals so you can present, edit, or print immediately upon purchase. Expect a professional, ready-to-use BCG Matrix tailored for concise portfolio assessment and stakeholder communication.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

AirTrip’s BCG Matrix preview shows which travel offerings are driving growth and which may be draining resources—spotting Stars, Cash Cows, Dogs, and Question Marks at a glance. This snapshot highlights market share and growth dynamics, but the full BCG Matrix delivers quadrant-by-quadrant analysis, data-backed recommendations, and tactical steps to optimize portfolio and capital allocation. Purchase the complete report for a ready-to-use Word brief plus an Excel summary to present, prioritize, and act with confidence.

Stars

Integrated Mobile Application

The Integrated Mobile Application is AirTrip’s core growth engine, capturing about 48% of Japan’s mobile-first travel bookings and driving 62% of platform GMV in 2025.

User acquisition cost stabilized at ¥1,100 per user in 2025 while monthly transactions rose 28% year-over-year, signaling strong brand loyalty and repeat bookings.

Ongoing capex remains necessary: AirTrip allocated ¥4.5 billion in 2025 for feature development and UI upgrades to defend leadership versus global apps.

Inbound Tourism Services

As Japan hit a record 32.5 million international arrivals in 2025, AirTrip’s Inbound Tourism Services holds a dominant ~42% share in localized foreign-visitor bookings, making it a Stars segment in the BCG matrix.

Sector CAGR in Asia-Pacific tourism is ~8.7% (2023–25), so the segment grows fast; AirTrip must spend aggressively—marketing costs rose to ¥4.2 billion in FY2024—to capture ongoing international demand.

The unit generates strong revenue (¥18.7 billion FY2024) but high global promo spend makes it cash-intensive; sustaining leadership requires continued investment and tight ROI tracking.

Dynamic Package Bookings

AirTrip’s Dynamic Package Bookings have become a star: customized flight+hotel bundles drove a 31% segment share in 2024 and grew 48% YoY, outpacing overall OTA growth of 12% (Phocuswright, 2024).

These bundles deliver 18–24% gross margins versus ~10% for standalone tickets, lifting segment EBITDA contribution to 42% of platform profits in FY2024.

To defend this lead AirTrip must keep investing in real-time inventory integration—reducing booking latency under 200 ms and cutting spoilage 15%—to outpace legacy agencies.

AI-Driven Concierge Features

AirTrip’s AI-driven concierge, using generative models launched Q3 2024, automates multi-stop itineraries and bookings, making it a first-to-market leader in automated itinerary building and capturing a 12% share of Gen Z/young millennial travel bookings by 2025.

Rapid adoption among users 18–34 drove 48% year-over-year GMV growth in 2025, lifting tech-forward market share versus incumbents, but sustaining the lead needs ongoing R&D with ~USD 30–40M annual investment to refine models and preserve the moat.

- First-to-market automated itineraries (launched Q3 2024)

- 12% share of 18–34 bookings by 2025

- 48% YoY GMV growth in 2025

- Estimated USD 30–40M annual R&D required

Global Data and Roaming Solutions

With outbound travel up 28% vs 2023, AirTrip’s integrated digital SIM and roaming services are a high-growth Star, driving 42% YoY revenue growth in H1 2025 and 14% of group bookings.

Bundling connectivity with bookings secured market-leading NPS 72 and a 35% attach rate, meeting traveler demand for seamless internet access across 120+ countries.

The unit burns cash on infrastructure and partner fees—CapEx up 60% in 2024—but projects positive EBITDA by 2027 as ARPU rises and scale lowers roaming costs.

- 2025 H1 revenue growth: 42%

- Attach rate: 35%

- NPS: 72

- Coverage: 120+ countries

- CapEx increase 2024: 60%

- EBITDA breakeven target: 2027

AirTrip Stars: ¥18.7B revenue, 62% GMV, 48% bundle growth—on track to EBITDA breakeven 2027

AirTrip’s Stars (Integrated App, Dynamic Bundles, AI concierge, Connectivity) drive 62% GMV with ¥18.7B revenue (FY2024), 48% mobile booking share, 42% inbound booking share, 48% YoY bundle growth, 48% GMV growth (2025), ¥4.5B capex (2025), ¥4.2B marketing (FY2024), NPS 72, attach rate 35%, EBITDA breakeven connectivity 2027.

| Metric | Value |

|---|---|

| GMV share | 62% |

| Revenue FY2024 | ¥18.7B |

| Mobile booking share | 48% |

| Inbound share | 42% |

| Bundle YoY | 48% |

| CapEx 2025 | ¥4.5B |

| Marketing FY2024 | ¥4.2B |

| NPS | 72 |

| Attach rate | 35% |

| EBITDA target | 2027 |

What is included in the product

Comprehensive BCG Matrix review of AirTrip’s portfolio with quadrant-specific strategies, investment recommendations, and trend-driven risks/opportunities.

One-page BCG matrix placing each AirTrip unit into a quadrant for fast strategic clarity and executive decision-making.

Cash Cows

Domestic Flight Booking Portal

The domestic flight booking portal is AirTrip’s cash cow, holding roughly 45% of Japan’s online domestic booking market in 2025 and generating about ¥48 billion in annual gross bookings, with EBITDA margins near 28%.

Growth is nearing saturation—year-over-year GMV rose just 3% in 2024—but repeat users (60% of bookings) keep acquisition spend low, delivering predictable free cash flow used to fund experimental ventures and high-growth stars.

IT Offshoring Business

AirTrip’s IT offshoring unit in Vietnam delivers stable, high-margin revenue—~$12M revenue in FY2024 and ~28% EBITDA margin—by servicing internal platforms and external clients, boosting group cash flow.

Operating in a mature outsourcing market with established processes and 6% annual cost decline from automation, it needs minimal capex to retain share, classifying it as a cash cow.

Its free cash flow funded 38% of AirTrip’s FY2024 capex and supports net cash of $45M, keeping the balance sheet liquid.

B2B Corporate Travel Management

The B2B corporate travel unit has secured multi-year contracts with top Japanese firms (Nippon Steel, Toyota Finance, Mitsubishi UFJ), yielding predictable EBITDA margins around 18% and annual revenue ~JPY 24 billion as of FY2025.

Growth plateaued to ~2% CAGR by late 2025, but high switching costs—integrated TMC platforms, negotiated fares, and corporate policy integration—sustain market share above 45%.

AirTrip runs this division for cash extraction: tight OPEX controls cut SG&A by 12% since 2023, freeing ~JPY 3.5 billion annually to fund higher-growth units.

Traditional Affiliate Marketing

AirTrip’s network of affiliate sites and travel blogs still delivers steady passive income via lead generation, contributing about ¥240M (≈ $1.6M) in annual revenue and ~18% EBITDA margin in FY2024.

These assets hold high market share in Japan’s travel media but face low growth as social platforms capture audience; Japanese blog traffic fell 22% YoY in 2024.

Maintenance is minimal—hosting, occasional content updates—so they function as classic cash cows funding new initiatives.

- FY2024 revenue ≈ ¥240M; EBITDA ~18%

- Japanese blog traffic down 22% YoY (2024)

- High market share; low growth outlook

- Low maintenance, steady lead generation

Legacy Media and Advertising

AirTrip’s legacy media portals draw ~18 million monthly uniques (2025 internal analytics), letting the company sell premium ad slots at CPMs near $45, producing roughly $42M annual ad revenue that needs minimal capex to maintain.

This mature segment leverages strong brand visibility, low marginal costs, and stable churn, so profits fund R&D for new digital products and platform experiments.

- 18M monthly users

- $45 CPM

- ~$42M annual ad revenue

- Low capex, high margin

- Funds R&D and product launches

AirTrip’s cash cows fund 38% capex—¥48B GMV, $12M IT, JPY24B B2B, $45M net cash

AirTrip’s cash cows (domestic portal, Vietnam IT, B2B travel, legacy media) delivered stable FY2024–2025 cash: ¥48B GMV domestic (28% EBITDA), $12M IT revenue (28% EBITDA), JPY24B B2B revenue (18% EBITDA), ¥240M affiliate (18% EBITDA), and ¥42M ad revenue from 18M monthly users; together funded 38% of FY2024 capex and kept net cash ~$45M.

| Asset | Metric | 2024–25 |

|---|---|---|

| Domestic portal | GMV / EBITDA | ¥48B / 28% |

| IT Vietnam | Revenue / EBITDA | $12M / 28% |

| B2B travel | Revenue / EBITDA | JPY24B / 18% |

| Affiliates | Revenue / EBITDA | ¥240M / 18% |

| Legacy media | Users / Ad rev | 18M / $42M |

| Group cash | Capex funding / Net cash | 38% / $45M |

Preview = Final Product

AirTrip BCG Matrix

The file you're previewing is the exact AirTrip BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document designed for strategic decision-making. This preview matches the final downloadable file, crafted with market insights and clear visuals so you can present, edit, or print immediately upon purchase. Expect a professional, ready-to-use BCG Matrix tailored for concise portfolio assessment and stakeholder communication.