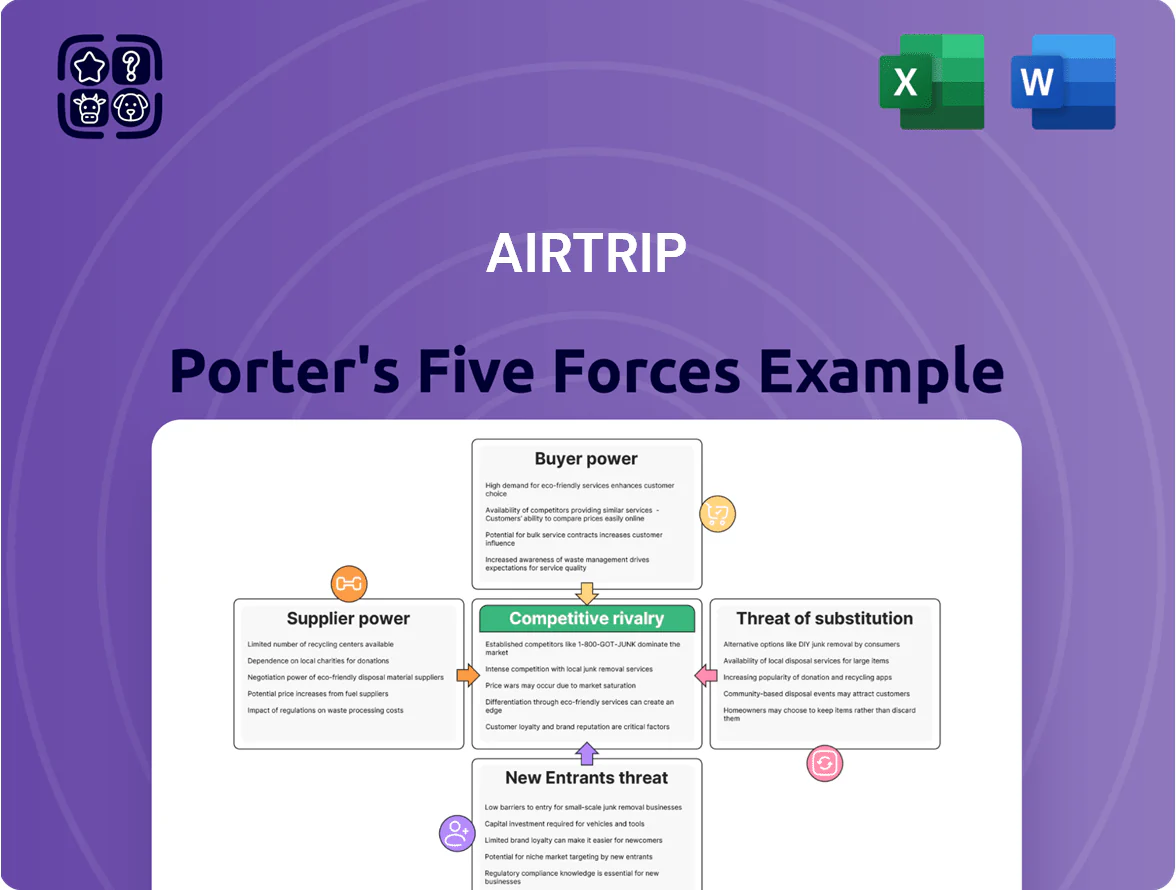

AirTrip Porter's Five Forces Analysis

Don't Miss the Bigger Picture

AirTrip faces intense competitive rivalry from established carriers and nimble low-cost entrants, while buyer power and price sensitivity pressure margins; supplier concentration (aircraft, fuel) and regulatory hurdles further shape strategy.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AirTrip’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Airline Carriers

The Japanese domestic aviation market is concentrated: ANA (All Nippon Airways) and JAL (Japan Airlines) held about 70% of domestic seat capacity in 2024, constraining AirTrip’s commission bargaining power and forcing thinner margins.

These carriers control seat inventory and dynamic pricing—load factors hit ~80% in summer 2024—so AirTrip faces limited leverage during peak seasons.

AirTrip therefore must keep deep API integrations and partnership terms with ANA and JAL to secure timely flight data and booking access.

Direct-to-Consumer Distribution Shifts

Airlines and hotels now push direct booking: in 2024 global airline direct-sales hit 46% of bookings and major chains reported 52% direct hotel bookings in 2024, raising supplier leverage over platforms like AirTrip.

When suppliers offer exclusive loyalty perks or 5–15% cheaper rates on own sites, AirTrip loses price-competitive inventory and margins.

AirTrip faces ongoing risk of inventory cuts—some carriers reduced GDS-supplied seats by 10–20% in 2024—forcing higher acquisition costs or narrower choice for users.

Global Distribution System Dependency

AirTrip depends on Global Distribution Systems (GDS) and API partners for real-time fares and seat inventory; about 60–75% of OTA bookings globally route via GDS as of 2024, so these vendors wield notable leverage.

GDS providers can raise transaction fees or throttle response times; a 10% fee hike on average $25 ticket service fee cuts margin per booking by roughly $2.50, hitting EBITDA on thin-margin routes.

Contract changes on data access or latency can force tech rework or higher costs; in 2023 several GDSs revised API pricing, increasing integration spend by up to 18% for mid-size OTAs.

Hotel Industry Fragmentation

The Japanese hotel and ryokan market remains fragmented: as of 2024 there were over 50,000 accommodation properties, which weakens any single supplier’s bargaining power versus AirTrip.

Still, international chains (Marriott, Hilton) and large domestic groups (Hoshino Resorts, Prince Hotels) control ~20–25% of room inventory in key urban/tourist hubs and can demand preferential placement or commission terms.

AirTrip must balance volume deals with big groups against many independents to keep inventory breadth and margins.

- 50,000+ properties in Japan (2024)

- Top chains ~20–25% inventory share

- Strategy: mix high-volume chain deals + indie listings

IT and Cloud Infrastructure Providers

As a digital-first travel platform, AirTrip relies on cloud providers and cybersecurity vendors for uptime and data integrity; global cloud IaaS spend hit 229 billion USD in 2023, concentrating power among top firms like Amazon Web Services, Microsoft Azure, and Google Cloud.

High migration costs for petabyte-scale travel data and integrations give these suppliers moderate bargaining power; switching a large workload can exceed millions in one-time and recurring expenses.

AirTrip’s continued investment in IT media and solution business increases dependency on specialized tech talent and managed services, keeping supplier power steady unless the firm builds in-house capacity.

- 2023 cloud IaaS market: 229B USD

- Top-3 providers hold ~60% market share

- Migration costs for large workloads: >1M USD

- Cybersecurity breach average cost: 4.45M USD (2023)

Concentrated Suppliers Squeeze Margins: Airlines, Hotels & Cloud Dominate 2023–24

Suppliers exert moderate-to-high power: ANA/JAL control ~70% domestic seats (2024) and peak load factors ~80%, GDS/API fees affect margins (GDS routing 60–75% OTA bookings, 2024), top hotel chains hold ~20–25% urban rooms, cloud IaaS concentrated (229B USD market, top-3 ~60%, 2023), and supplier-driven direct sales (~46% airlines, 2024) shrink OTA leverage.

| Metric | Value |

|---|---|

| ANA+JAL domestic share | ~70% (2024) |

| Peak load factor | ~80% (summer 2024) |

| GDS booking share | 60–75% (2024) |

| Airline direct sales | 46% (2024) |

| Top hotel chain room share | 20–25% (2024) |

| Cloud IaaS market | 229B USD; top-3 ~60% (2023) |

What is included in the product

Tailored Porter’s Five Forces analysis for AirTrip, uncovering competitive dynamics, buyer and supplier power, entry barriers, substitutes, and disruptive threats to inform strategic positioning and investor materials.

Quick, one-sheet Porter’s Five Forces for AirTrip—translate competitive pressures into actionable strategy in seconds.

Customers Bargaining Power

Low Switching Costs for Travelers

Individual travelers can compare fares across OTAs and airlines in minutes, and with global metasearch use up 22% in 2024, brand loyalty is weak; surveys show 68% of leisure flyers hunt for best price each trip. There are no major penalties for booking with competitors or direct carriers, so AirTrip faces high price sensitivity and must refresh its UI and promotions—AirTrip lowered CPA 14% in 2025 after a UX push to counter churn.

Price Transparency Through Meta-Search

Meta-search engines let customers compare AirTrip prices against 30+ OTAs in seconds; 62% of leisure travelers (2024 Phocuswright) check meta-search before booking, pushing AirTrip toward commodity pricing.

Price transparency lets buyers pick the lowest fare, cutting AirTrip’s margin—OTA gross margins fell 3–5 ppt in 2023 as price shopping rose.

To compete AirTrip should sell value: premium 24/7 support, bundled travel insurance (average attachment rate 12% across OTAs in 2024), and loyalty perks to recover €5–15 incremental margin per booking.

Influence of Corporate Clients

Corporate clients give AirTrip strong bargaining power in B2B and IT segments because they provide large, recurring volumes—top 20 accounts supplied ~38% of B2B revenue in 2024; losing one can cut quarterly revenue by 6–10%.

They regularly demand custom booking portals, deferred payment terms, and tailored reporting; implementing these features raises switching costs and operating complexity.

High concentration means churn risk hits market share: a 5% B2B churn in 2024 translated to a 3-point drop in B2B market share that year.

High Volume of Information and Reviews

- User review influence: 92% consult reviews

- Retention boost: 4.2+ ratings → 15–25% more bookings

- Key risk: ratings <4.0 drive user migration

Demand for Integrated Travel Experiences

Customers now favor one-stop travel bundles—flights, hotels, activities—driving AirTrip to sell higher-value packages but also to meet strong price expectations; 2024 OTA data shows 62% of travelers prefer bundled bookings and average bundle basket sizes rose 18% year-over-year.

That demand forces AirTrip to offer dynamic-package discounts; bundles commonly require 10–25% price concessions to match consumer willingness-to-pay, squeezing margins unless offset by higher ancillary take-rates or supplier rebates.

What this estimate hides: supplier contract terms and personalization tech spend can swing net margin by ±6 percentage points, so negotiating allotments and using ML pricing are critical.

- 62% of travelers prefer bundles (2024 OTA survey)

- Bundle basket size +18% YoY (2024)

- Typical bundle discounts 10–25%

- Margin swing ±6 ppt from supplier terms and tech spend

Price-savvy customers squeeze OTA margins as metas, bundles and B2B power rise

Customers hold high bargaining power: price transparency and meta-search use (62% check metas, 22% global metasearch growth 2024) push AirTrip to compete on price; leisure price hunters = 68% (2024), lowering margins (OTA gross margins -3–5 ppt in 2023). B2B concentration (top 20 = 38% B2B revenue 2024) gives corporate clients leverage. Bundles demand (62% prefer bundles, basket +18% YoY) forces 10–25% discounts unless ancillaries rise.

| Metric | Value |

|---|---|

| Meta-search use | 62% (2024) |

| Leisure price hunters | 68% (2024) |

| Meta growth | 22% (2024) |

| OTA margin shift | -3–5 ppt (2023) |

| Top-20 B2B share | 38% (2024) |

| Bundle preference | 62%, basket +18% YoY (2024) |

Full Version Awaits

AirTrip Porter's Five Forces Analysis

This preview shows the exact AirTrip Porter’s Five Forces analysis you'll receive after purchase—no placeholders or samples, fully formatted and ready for immediate download.

You're viewing the same professionally written document delivered instantly upon payment, containing comprehensive assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

AirTrip faces intense competitive rivalry from established carriers and nimble low-cost entrants, while buyer power and price sensitivity pressure margins; supplier concentration (aircraft, fuel) and regulatory hurdles further shape strategy.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AirTrip’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Major Airline Carriers

The Japanese domestic aviation market is concentrated: ANA (All Nippon Airways) and JAL (Japan Airlines) held about 70% of domestic seat capacity in 2024, constraining AirTrip’s commission bargaining power and forcing thinner margins.

These carriers control seat inventory and dynamic pricing—load factors hit ~80% in summer 2024—so AirTrip faces limited leverage during peak seasons.

AirTrip therefore must keep deep API integrations and partnership terms with ANA and JAL to secure timely flight data and booking access.

Direct-to-Consumer Distribution Shifts

Airlines and hotels now push direct booking: in 2024 global airline direct-sales hit 46% of bookings and major chains reported 52% direct hotel bookings in 2024, raising supplier leverage over platforms like AirTrip.

When suppliers offer exclusive loyalty perks or 5–15% cheaper rates on own sites, AirTrip loses price-competitive inventory and margins.

AirTrip faces ongoing risk of inventory cuts—some carriers reduced GDS-supplied seats by 10–20% in 2024—forcing higher acquisition costs or narrower choice for users.

Global Distribution System Dependency

AirTrip depends on Global Distribution Systems (GDS) and API partners for real-time fares and seat inventory; about 60–75% of OTA bookings globally route via GDS as of 2024, so these vendors wield notable leverage.

GDS providers can raise transaction fees or throttle response times; a 10% fee hike on average $25 ticket service fee cuts margin per booking by roughly $2.50, hitting EBITDA on thin-margin routes.

Contract changes on data access or latency can force tech rework or higher costs; in 2023 several GDSs revised API pricing, increasing integration spend by up to 18% for mid-size OTAs.

Hotel Industry Fragmentation

The Japanese hotel and ryokan market remains fragmented: as of 2024 there were over 50,000 accommodation properties, which weakens any single supplier’s bargaining power versus AirTrip.

Still, international chains (Marriott, Hilton) and large domestic groups (Hoshino Resorts, Prince Hotels) control ~20–25% of room inventory in key urban/tourist hubs and can demand preferential placement or commission terms.

AirTrip must balance volume deals with big groups against many independents to keep inventory breadth and margins.

- 50,000+ properties in Japan (2024)

- Top chains ~20–25% inventory share

- Strategy: mix high-volume chain deals + indie listings

IT and Cloud Infrastructure Providers

As a digital-first travel platform, AirTrip relies on cloud providers and cybersecurity vendors for uptime and data integrity; global cloud IaaS spend hit 229 billion USD in 2023, concentrating power among top firms like Amazon Web Services, Microsoft Azure, and Google Cloud.

High migration costs for petabyte-scale travel data and integrations give these suppliers moderate bargaining power; switching a large workload can exceed millions in one-time and recurring expenses.

AirTrip’s continued investment in IT media and solution business increases dependency on specialized tech talent and managed services, keeping supplier power steady unless the firm builds in-house capacity.

- 2023 cloud IaaS market: 229B USD

- Top-3 providers hold ~60% market share

- Migration costs for large workloads: >1M USD

- Cybersecurity breach average cost: 4.45M USD (2023)

Concentrated Suppliers Squeeze Margins: Airlines, Hotels & Cloud Dominate 2023–24

Suppliers exert moderate-to-high power: ANA/JAL control ~70% domestic seats (2024) and peak load factors ~80%, GDS/API fees affect margins (GDS routing 60–75% OTA bookings, 2024), top hotel chains hold ~20–25% urban rooms, cloud IaaS concentrated (229B USD market, top-3 ~60%, 2023), and supplier-driven direct sales (~46% airlines, 2024) shrink OTA leverage.

| Metric | Value |

|---|---|

| ANA+JAL domestic share | ~70% (2024) |

| Peak load factor | ~80% (summer 2024) |

| GDS booking share | 60–75% (2024) |

| Airline direct sales | 46% (2024) |

| Top hotel chain room share | 20–25% (2024) |

| Cloud IaaS market | 229B USD; top-3 ~60% (2023) |

What is included in the product

Tailored Porter’s Five Forces analysis for AirTrip, uncovering competitive dynamics, buyer and supplier power, entry barriers, substitutes, and disruptive threats to inform strategic positioning and investor materials.

Quick, one-sheet Porter’s Five Forces for AirTrip—translate competitive pressures into actionable strategy in seconds.

Customers Bargaining Power

Low Switching Costs for Travelers

Individual travelers can compare fares across OTAs and airlines in minutes, and with global metasearch use up 22% in 2024, brand loyalty is weak; surveys show 68% of leisure flyers hunt for best price each trip. There are no major penalties for booking with competitors or direct carriers, so AirTrip faces high price sensitivity and must refresh its UI and promotions—AirTrip lowered CPA 14% in 2025 after a UX push to counter churn.

Price Transparency Through Meta-Search

Meta-search engines let customers compare AirTrip prices against 30+ OTAs in seconds; 62% of leisure travelers (2024 Phocuswright) check meta-search before booking, pushing AirTrip toward commodity pricing.

Price transparency lets buyers pick the lowest fare, cutting AirTrip’s margin—OTA gross margins fell 3–5 ppt in 2023 as price shopping rose.

To compete AirTrip should sell value: premium 24/7 support, bundled travel insurance (average attachment rate 12% across OTAs in 2024), and loyalty perks to recover €5–15 incremental margin per booking.

Influence of Corporate Clients

Corporate clients give AirTrip strong bargaining power in B2B and IT segments because they provide large, recurring volumes—top 20 accounts supplied ~38% of B2B revenue in 2024; losing one can cut quarterly revenue by 6–10%.

They regularly demand custom booking portals, deferred payment terms, and tailored reporting; implementing these features raises switching costs and operating complexity.

High concentration means churn risk hits market share: a 5% B2B churn in 2024 translated to a 3-point drop in B2B market share that year.

High Volume of Information and Reviews

- User review influence: 92% consult reviews

- Retention boost: 4.2+ ratings → 15–25% more bookings

- Key risk: ratings <4.0 drive user migration

Demand for Integrated Travel Experiences

Customers now favor one-stop travel bundles—flights, hotels, activities—driving AirTrip to sell higher-value packages but also to meet strong price expectations; 2024 OTA data shows 62% of travelers prefer bundled bookings and average bundle basket sizes rose 18% year-over-year.

That demand forces AirTrip to offer dynamic-package discounts; bundles commonly require 10–25% price concessions to match consumer willingness-to-pay, squeezing margins unless offset by higher ancillary take-rates or supplier rebates.

What this estimate hides: supplier contract terms and personalization tech spend can swing net margin by ±6 percentage points, so negotiating allotments and using ML pricing are critical.

- 62% of travelers prefer bundles (2024 OTA survey)

- Bundle basket size +18% YoY (2024)

- Typical bundle discounts 10–25%

- Margin swing ±6 ppt from supplier terms and tech spend

Price-savvy customers squeeze OTA margins as metas, bundles and B2B power rise

Customers hold high bargaining power: price transparency and meta-search use (62% check metas, 22% global metasearch growth 2024) push AirTrip to compete on price; leisure price hunters = 68% (2024), lowering margins (OTA gross margins -3–5 ppt in 2023). B2B concentration (top 20 = 38% B2B revenue 2024) gives corporate clients leverage. Bundles demand (62% prefer bundles, basket +18% YoY) forces 10–25% discounts unless ancillaries rise.

| Metric | Value |

|---|---|

| Meta-search use | 62% (2024) |

| Leisure price hunters | 68% (2024) |

| Meta growth | 22% (2024) |

| OTA margin shift | -3–5 ppt (2023) |

| Top-20 B2B share | 38% (2024) |

| Bundle preference | 62%, basket +18% YoY (2024) |

Full Version Awaits

AirTrip Porter's Five Forces Analysis

This preview shows the exact AirTrip Porter’s Five Forces analysis you'll receive after purchase—no placeholders or samples, fully formatted and ready for immediate download.

You're viewing the same professionally written document delivered instantly upon payment, containing comprehensive assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution.