Advanced Info Service Boston Consulting Group Matrix

Actionable Strategy Starts Here

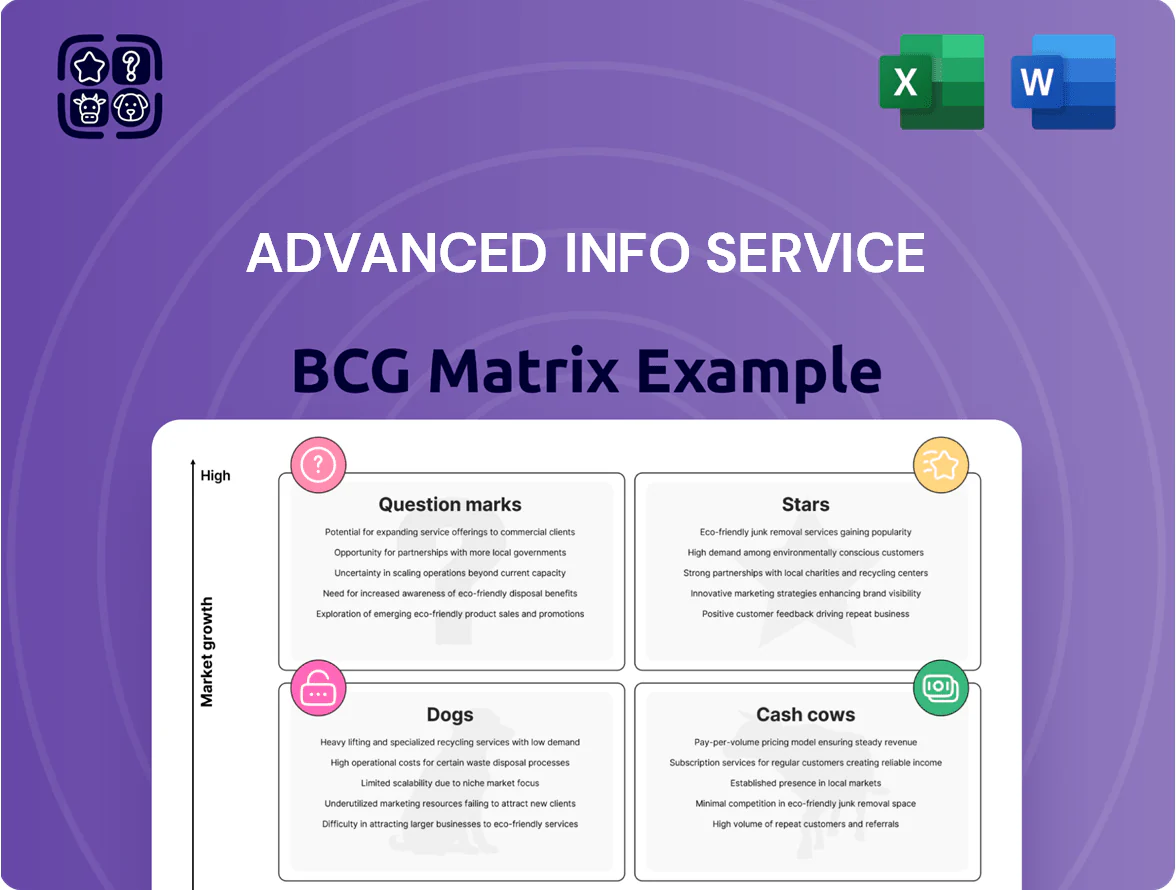

Advanced Info Service’s BCG Matrix snapshot highlights its dominant mobile-market share and cash-generating core services, while flagging growth areas and potential underperformers—essential for strategic capital allocation. This preview teases quadrant placements and high-level implications; purchase the full BCG Matrix to get quadrant-by-quadrant data, actionable recommendations, and deliverables in Word and Excel that let you prioritize investments and operational focus immediately.

Stars

5G Enterprise Solutions

AIS leads Thailand’s industrial 5G rollout, powering smart factories and autonomous logistics with a dominant private-network market share—about 45% of enterprise 5G contracts in 2024 and >THB 7.2bn capex invested since 2022.

AIS Fibre Broadband

The fixed broadband market in Thailand grew ~6–8% in 2024 with household fiber penetration reaching about 46% by end-2024; high-speed home internet is now utility-like for work and entertainment.

AIS Fibre has grabbed share from legacy providers by upselling converged mobile-broadband bundles to its 42.7 million mobile subscribers (AIS group 2024), boosting ARPU and penetration.

Rapid FTTH (fiber-to-the-home) rollout needs continued last-mile capex—AIS reported THB 14.2bn capex for 2024—while traffic per household rose ~35% YoY.

As infrastructure matures and churn falls, AIS Fibre is on track to shift from growth to a primary cash-generating unit within 2–3 years.

Hyperscale Data Centers

Through 2025 AIS, via partnerships with Gulf Energy and Singtel, scaled hyperscale data centers to ~120 MW capacity across Thailand and SEA, targeting cloud and AI workloads and capturing ~28% of domestic enterprise hosting spend.

Regional demand for local data residency and low-latency hosting grew ~34% YoY in 2024–2025; AIS’s hyperscale arm requires heavy capex—estimated THB 15–20 billion 2025–2026—but offers strategic value for cloud revenue and market leadership.

5G Consumer Services

5G Consumer Services is a Star: 4G→5G migration hit critical mass in 2024 with Thailand 5G penetration ~48% (GSMA/NT 2024), lifting AIS ARPU by ~12% YoY in H2 2024; heavy spectrum (largest Thai portfolio) lets AIS offer top speeds and low latency for cloud gaming and AR/VR.

Segment needs sustained promotion and CAPEX to fend off consolidation; as 5G becomes standard by 2027–2028 this Star should transition into a dominant cash cow.

- 2024 5G penetration ~48% Thailand (GSMA/NT)

- AIS ARPU +12% YoY H2 2024 (AIS filings)

- Largest Thai spectrum portfolio — enables high-bandwidth services

- Requires marketing/CAPEX to retain lead; cash cow by 2027–28

Digital Content Ecosystem

The AIS Play platform and exclusive partnerships with Netflix and Disney+ have made digital media a high-growth AIS segment, with video-streaming revenue up ~28% YoY in 2024 and digital services contributing about 12% of group revenue in FY2024.

Bundling premium content with data plans helped AIS capture an estimated 38% share of Thailand’s mobile entertainment market in 2024, boosting ARPU and lowering quarterly churn to ~1.6%.

Ongoing spend on localized shows and app features—AIS reported THB 1.2 billion content investment in 2024—is key to defend against global OTT entrants and sustain stickiness.

- High growth: streaming rev +28% YoY (2024)

- Market share: ~38% mobile entertainment (2024)

- Churn: ~1.6% quarterly

- Content spend: THB 1.2bn (2024)

AIS powerhouse: 48% 5G, ARPU +12%, 120MW DC target, streaming +28% — growth engines aligned

AIS 5G, Fibre, data centers and digital media are Stars: 2024–25 metrics show 48% national 5G penetration, AIS ARPU +12% H2 2024, AIS Fibre capex THB 14.2bn (2024) and 42.7m mobile subs, hyperscale target ~120 MW (2025) with THB 15–20bn capex 2025–26, streaming rev +28% (2024) and 38% mobile entertainment share.

| Metric | Value |

|---|---|

| Thailand 5G pen (2024) | 48% |

| AIS ARPU change H2 2024 | +12% |

| AIS Fibre capex 2024 | THB 14.2bn |

| Mobile subscribers (AIS group 2024) | 42.7m |

| Data center capacity (2025) | ~120 MW |

| Data center capex 2025–26 (est) | THB 15–20bn |

| Streaming rev growth 2024 | +28% |

| Mobile entertainment share 2024 | 38% |

What is included in the product

Comprehensive BCG Matrix review of Advanced Info Service with quadrant strategies, investments, risks, and trend-driven recommendations.

One-page BCG matrix placing Advanced Info Service units in clear quadrants for quick executive decisions and slide-ready export.

Cash Cows

4G LTE Mobile Services

The 4G LTE network remains AIS’s revenue backbone, covering ~85% of Thai mobile subscribers and delivering the largest traffic share with >60% of service revenue as of 2024.

With most 4G capex depreciated, operating cash flow margins exceed 40%, producing massive free cash flow that needs minimal new investment.

These cash flows funded AIS’s 2024–2025 5G rollout (capex ~THB 25bn in 2024) and supported a 2024 dividend yield near 4.5%.

Growth is low, but dominant market share (~45% mobile market in 2024) makes 4G the classic cash cow for AIS.

Prepaid Mobile Segment

AIS holds a commanding lead in Thailand’s prepaid mobile market, with a 2025 prepaid subscriber share around 45% and driving roughly THB 28–30 billion annual EBITDA from the segment; tourism rebound lifted tourist SIM sales by ~22% YoY. The unit needs minimal marketing versus high cash intake, keeping CAC low and gross margins near 55%. Operational costs stay low due to scale and a distribution network of 250,000+ retail points nationwide. It remains a steady cash cow funding AIS’s speculative digital investments.

Traditional Voice and SMS

Despite a 2024-25 mobile data boom—Thai mobile data traffic rose ~35% year-on-year in 2024—Advanced Info Service’s (AIS) traditional voice and SMS still generate high-margin revenue, driven by older consumers and automated corporate alerts, contributing an estimated 8–12% of service EBITDA in 2024.

These services run on legacy PSTN/SMS infrastructure with negligible incremental capex—AIS allocated under 3% of 2024 network capex to circuit/SMS upkeep—so margins remain strong.

The market is mature and declining at roughly 5% CAGR, yet profitability keeps voice/SMS as a stable cash cow that helps cover administrative costs and service debt, supporting AIS’s 2024 net leverage targets.

Enterprise Connectivity Services

Enterprise Connectivity Services (MPLS, leased lines, VPN) are a mature, low-growth cash cow for Advanced Info Service (AIS), generating steady recurring revenue—AIS reported THB 18.2 billion in fixed-data service revenue in 2024, ~24% of group service sales.

Most large Thai corporates and government agencies depend on AIS for foundational connectivity, and high infrastructure and regulation barriers keep market share durable despite saturation.

Limited upside for explosive growth, so AIS can reallocate capital and sales effort toward higher-growth digital transformation and cloud services while harvesting stable margins.

- 2024 fixed-data revenue: THB 18.2B

- Contribution: ~24% of service sales

- Market growth: low to flat; high entry barriers

- Strategy: harvest cash, invest in digital transformation

International Roaming

With Thailand tourism hitting record highs—39.9 million international arrivals in 2025 YTD vs 28.7M in 2023—AIS’s international roaming is a high-margin cash cow, returning strong ARPU uplift as roaming revenue grew ~22% YoY in 2024-25.

AIS uses its 700+ global roaming partners to monetize inbound tourists and outbound Thais with minimal capex, running on spare network capacity and boosting EBITDA margins while stabilizing the corporate portfolio.

- 39.9M arrivals 2025 YTD; roaming rev +22% YoY (2024-25)

- 700+ global partners; negligible capex

- Higher ARPU and margin support corporate EBITDA

AIS cash cows: 4G >60% rev, prepaid THB28–30bn EBITDA, roaming +22% YoY

4G/Prepaid/Fixed-data/roaming are AIS cash cows: 4G drives >60% service revenue with ~45% mobile share (2024); prepaid yields THB 28–30bn EBITDA and ~55% gross margin (2025); fixed-data THB 18.2bn (~24% service sales, 2024); roaming +22% YoY (2024–25) on 700+ partners, tourism 39.9M arrivals (2025 YTD).

| Metric | Value |

|---|---|

| 4G service rev share (2024) | >60% |

| Mobile market share (2024) | ~45% |

| Prepaid EBITDA (annual) | THB 28–30bn (2025) |

| Fixed-data revenue (2024) | THB 18.2bn |

| Roaming rev growth (2024–25) | +22% YoY |

| Tourism arrivals (2025 YTD) | 39.9M |

Preview = Final Product

Advanced Info Service BCG Matrix

The file you're previewing is the final Advanced Info Service BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready report tailored for strategic clarity and professional use.

This preview is identical to the downloadable document sent to your inbox upon purchase, crafted with precise market insights and ready for immediate editing, printing, or presentation to stakeholders.

What you see is the actual BCG Matrix file included with your one-time purchase—professionally designed, plug-and-play for business planning, investor decks, or client deliverables.

There are no mockups or hidden revisions; the report is delivered as-is so you can use it instantly in decision-making, competitive analysis, or strategic reviews.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Advanced Info Service’s BCG Matrix snapshot highlights its dominant mobile-market share and cash-generating core services, while flagging growth areas and potential underperformers—essential for strategic capital allocation. This preview teases quadrant placements and high-level implications; purchase the full BCG Matrix to get quadrant-by-quadrant data, actionable recommendations, and deliverables in Word and Excel that let you prioritize investments and operational focus immediately.

Stars

5G Enterprise Solutions

AIS leads Thailand’s industrial 5G rollout, powering smart factories and autonomous logistics with a dominant private-network market share—about 45% of enterprise 5G contracts in 2024 and >THB 7.2bn capex invested since 2022.

AIS Fibre Broadband

The fixed broadband market in Thailand grew ~6–8% in 2024 with household fiber penetration reaching about 46% by end-2024; high-speed home internet is now utility-like for work and entertainment.

AIS Fibre has grabbed share from legacy providers by upselling converged mobile-broadband bundles to its 42.7 million mobile subscribers (AIS group 2024), boosting ARPU and penetration.

Rapid FTTH (fiber-to-the-home) rollout needs continued last-mile capex—AIS reported THB 14.2bn capex for 2024—while traffic per household rose ~35% YoY.

As infrastructure matures and churn falls, AIS Fibre is on track to shift from growth to a primary cash-generating unit within 2–3 years.

Hyperscale Data Centers

Through 2025 AIS, via partnerships with Gulf Energy and Singtel, scaled hyperscale data centers to ~120 MW capacity across Thailand and SEA, targeting cloud and AI workloads and capturing ~28% of domestic enterprise hosting spend.

Regional demand for local data residency and low-latency hosting grew ~34% YoY in 2024–2025; AIS’s hyperscale arm requires heavy capex—estimated THB 15–20 billion 2025–2026—but offers strategic value for cloud revenue and market leadership.

5G Consumer Services

5G Consumer Services is a Star: 4G→5G migration hit critical mass in 2024 with Thailand 5G penetration ~48% (GSMA/NT 2024), lifting AIS ARPU by ~12% YoY in H2 2024; heavy spectrum (largest Thai portfolio) lets AIS offer top speeds and low latency for cloud gaming and AR/VR.

Segment needs sustained promotion and CAPEX to fend off consolidation; as 5G becomes standard by 2027–2028 this Star should transition into a dominant cash cow.

- 2024 5G penetration ~48% Thailand (GSMA/NT)

- AIS ARPU +12% YoY H2 2024 (AIS filings)

- Largest Thai spectrum portfolio — enables high-bandwidth services

- Requires marketing/CAPEX to retain lead; cash cow by 2027–28

Digital Content Ecosystem

The AIS Play platform and exclusive partnerships with Netflix and Disney+ have made digital media a high-growth AIS segment, with video-streaming revenue up ~28% YoY in 2024 and digital services contributing about 12% of group revenue in FY2024.

Bundling premium content with data plans helped AIS capture an estimated 38% share of Thailand’s mobile entertainment market in 2024, boosting ARPU and lowering quarterly churn to ~1.6%.

Ongoing spend on localized shows and app features—AIS reported THB 1.2 billion content investment in 2024—is key to defend against global OTT entrants and sustain stickiness.

- High growth: streaming rev +28% YoY (2024)

- Market share: ~38% mobile entertainment (2024)

- Churn: ~1.6% quarterly

- Content spend: THB 1.2bn (2024)

AIS powerhouse: 48% 5G, ARPU +12%, 120MW DC target, streaming +28% — growth engines aligned

AIS 5G, Fibre, data centers and digital media are Stars: 2024–25 metrics show 48% national 5G penetration, AIS ARPU +12% H2 2024, AIS Fibre capex THB 14.2bn (2024) and 42.7m mobile subs, hyperscale target ~120 MW (2025) with THB 15–20bn capex 2025–26, streaming rev +28% (2024) and 38% mobile entertainment share.

| Metric | Value |

|---|---|

| Thailand 5G pen (2024) | 48% |

| AIS ARPU change H2 2024 | +12% |

| AIS Fibre capex 2024 | THB 14.2bn |

| Mobile subscribers (AIS group 2024) | 42.7m |

| Data center capacity (2025) | ~120 MW |

| Data center capex 2025–26 (est) | THB 15–20bn |

| Streaming rev growth 2024 | +28% |

| Mobile entertainment share 2024 | 38% |

What is included in the product

Comprehensive BCG Matrix review of Advanced Info Service with quadrant strategies, investments, risks, and trend-driven recommendations.

One-page BCG matrix placing Advanced Info Service units in clear quadrants for quick executive decisions and slide-ready export.

Cash Cows

4G LTE Mobile Services

The 4G LTE network remains AIS’s revenue backbone, covering ~85% of Thai mobile subscribers and delivering the largest traffic share with >60% of service revenue as of 2024.

With most 4G capex depreciated, operating cash flow margins exceed 40%, producing massive free cash flow that needs minimal new investment.

These cash flows funded AIS’s 2024–2025 5G rollout (capex ~THB 25bn in 2024) and supported a 2024 dividend yield near 4.5%.

Growth is low, but dominant market share (~45% mobile market in 2024) makes 4G the classic cash cow for AIS.

Prepaid Mobile Segment

AIS holds a commanding lead in Thailand’s prepaid mobile market, with a 2025 prepaid subscriber share around 45% and driving roughly THB 28–30 billion annual EBITDA from the segment; tourism rebound lifted tourist SIM sales by ~22% YoY. The unit needs minimal marketing versus high cash intake, keeping CAC low and gross margins near 55%. Operational costs stay low due to scale and a distribution network of 250,000+ retail points nationwide. It remains a steady cash cow funding AIS’s speculative digital investments.

Traditional Voice and SMS

Despite a 2024-25 mobile data boom—Thai mobile data traffic rose ~35% year-on-year in 2024—Advanced Info Service’s (AIS) traditional voice and SMS still generate high-margin revenue, driven by older consumers and automated corporate alerts, contributing an estimated 8–12% of service EBITDA in 2024.

These services run on legacy PSTN/SMS infrastructure with negligible incremental capex—AIS allocated under 3% of 2024 network capex to circuit/SMS upkeep—so margins remain strong.

The market is mature and declining at roughly 5% CAGR, yet profitability keeps voice/SMS as a stable cash cow that helps cover administrative costs and service debt, supporting AIS’s 2024 net leverage targets.

Enterprise Connectivity Services

Enterprise Connectivity Services (MPLS, leased lines, VPN) are a mature, low-growth cash cow for Advanced Info Service (AIS), generating steady recurring revenue—AIS reported THB 18.2 billion in fixed-data service revenue in 2024, ~24% of group service sales.

Most large Thai corporates and government agencies depend on AIS for foundational connectivity, and high infrastructure and regulation barriers keep market share durable despite saturation.

Limited upside for explosive growth, so AIS can reallocate capital and sales effort toward higher-growth digital transformation and cloud services while harvesting stable margins.

- 2024 fixed-data revenue: THB 18.2B

- Contribution: ~24% of service sales

- Market growth: low to flat; high entry barriers

- Strategy: harvest cash, invest in digital transformation

International Roaming

With Thailand tourism hitting record highs—39.9 million international arrivals in 2025 YTD vs 28.7M in 2023—AIS’s international roaming is a high-margin cash cow, returning strong ARPU uplift as roaming revenue grew ~22% YoY in 2024-25.

AIS uses its 700+ global roaming partners to monetize inbound tourists and outbound Thais with minimal capex, running on spare network capacity and boosting EBITDA margins while stabilizing the corporate portfolio.

- 39.9M arrivals 2025 YTD; roaming rev +22% YoY (2024-25)

- 700+ global partners; negligible capex

- Higher ARPU and margin support corporate EBITDA

AIS cash cows: 4G >60% rev, prepaid THB28–30bn EBITDA, roaming +22% YoY

4G/Prepaid/Fixed-data/roaming are AIS cash cows: 4G drives >60% service revenue with ~45% mobile share (2024); prepaid yields THB 28–30bn EBITDA and ~55% gross margin (2025); fixed-data THB 18.2bn (~24% service sales, 2024); roaming +22% YoY (2024–25) on 700+ partners, tourism 39.9M arrivals (2025 YTD).

| Metric | Value |

|---|---|

| 4G service rev share (2024) | >60% |

| Mobile market share (2024) | ~45% |

| Prepaid EBITDA (annual) | THB 28–30bn (2025) |

| Fixed-data revenue (2024) | THB 18.2bn |

| Roaming rev growth (2024–25) | +22% YoY |

| Tourism arrivals (2025 YTD) | 39.9M |

Preview = Final Product

Advanced Info Service BCG Matrix

The file you're previewing is the final Advanced Info Service BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready report tailored for strategic clarity and professional use.

This preview is identical to the downloadable document sent to your inbox upon purchase, crafted with precise market insights and ready for immediate editing, printing, or presentation to stakeholders.

What you see is the actual BCG Matrix file included with your one-time purchase—professionally designed, plug-and-play for business planning, investor decks, or client deliverables.

There are no mockups or hidden revisions; the report is delivered as-is so you can use it instantly in decision-making, competitive analysis, or strategic reviews.