Akebia Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

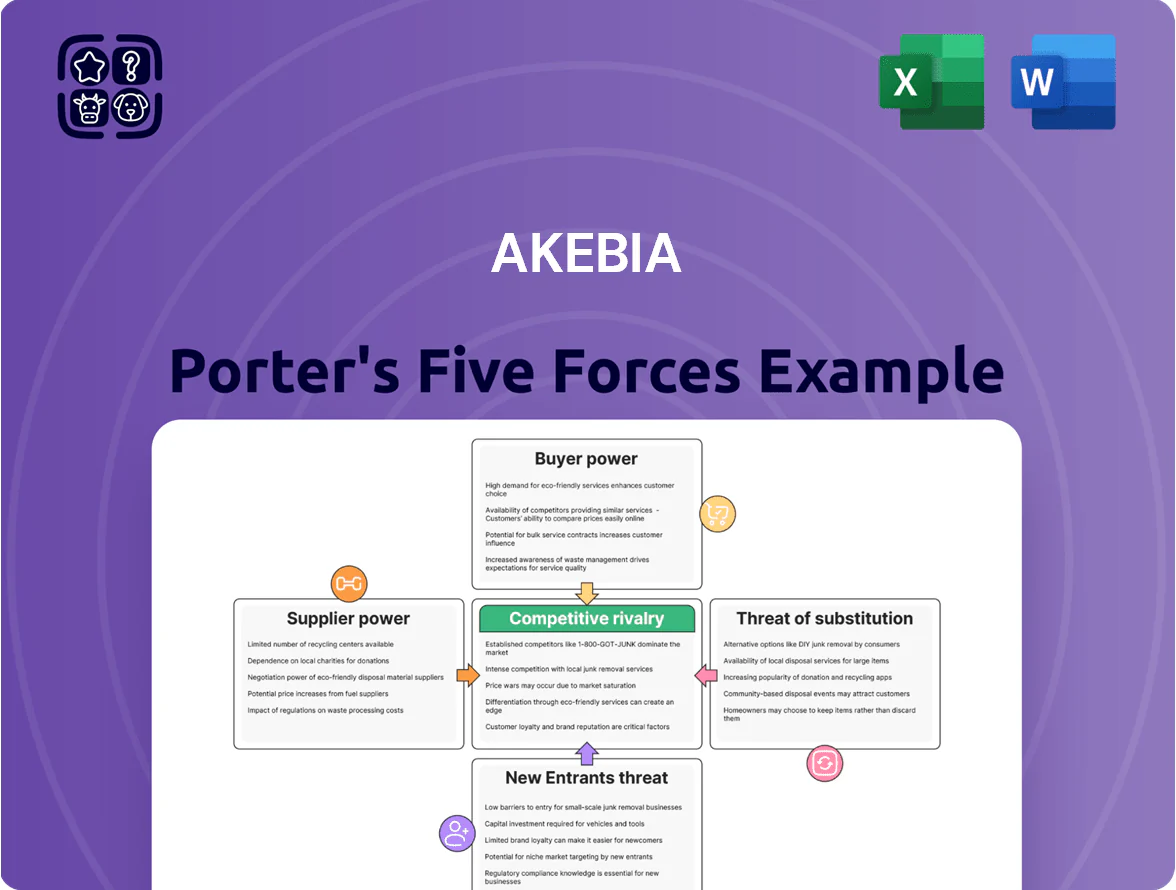

Akebia faces moderate buyer power, specialized supplier influence, and significant competitive rivalry as it navigates reimbursement pressures and patent cliffs in renal care markets.

Regulatory scrutiny and high development costs raise barriers for new entrants but also heighten substitute threats from emerging therapies and generics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Akebia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized API Contract Manufacturers

Clinical Research Organizations

Intellectual Property and Technology Licensors

Akebia relies on licensed HIF-PHI technologies and foundational patents that drive its vadadustat program; licensors wield leverage via royalty rates—industry-standard biopharma royalties range 2–10%—and litigation risk that can halt commercialization.

In 2025 Akebia's freedom to operate hinges on these agreements and milestone payments (recent deals show upfronts $5–50M), so maintaining licenses and defensive patent strategies is critical to avoid injunctions and revenue loss.

Specialized Logistics and Cold Chain Providers

Specialized logistics and cold chain providers hold strong bargaining power for Akebia because only a small pool meet FDA, EU GDP, and FDA Drug Supply Chain Security Act standards required for biopharmaceuticals; in 2024, ~65% of US pharma cold shipments used top-tier certified carriers, concentrating leverage.

Service disruptions—like TempControl carrier outages in Q3 2023—can cause drug shortages and revenue hits; a single-week cold-chain failure can cost a mid-size specialty drug maker $5–10M in lost sales and spoilage.

- Few certified distributors: ~65% market share by top-tier carriers (2024)

- High impact: 1-week failure ≈ $5–10M revenue loss

- Regulatory burden raises switching costs and supplier leverage

Regulatory and Compliance Consultants

Niche regulatory consultants for FDA and EMA kidney-disease approvals command strong supplier power: their specialized expertise is critical to secure and expand labels, and firms pay high fees—consulting rates often range from $300–$800/hour and program fees $250k–$2M per submission in 2024–2025.

The power reflects high stakes of regulatory failure—median FDA nephrology review times were ~10.8 months in 2024—and a small pool of senior experts, concentrating bargaining leverage.

- High fees: $300–$800/hour; $250k–$2M per submission

- Long reviews: median FDA nephrology review ~10.8 months (2024)

- Limited talent: few senior regulatory leads globally

Supplier concentration and service bottlenecks = major cost, delay & royalty risks

Suppliers hold moderate-to-strong power: API/CMO concentration (fewer than 10 global scale suppliers; $5–10M qualification; 8–12 week lead variance), CROs create 8–14 month delays/$5–20M extra, licensors demand 2–10% royalties and $5–50M upfronts, cold-chain/top carriers ~65% share (2024) with 1-week failure ≈ $5–10M loss, regulatory consultants $300–$800/hr.

| Supplier | Key metric | Impact |

|---|---|---|

| API/CMO | <10 suppliers; $5–10M qual | Price/timeline risk |

| CROs | 8–14mo; $5–20M | Trial delay/cost |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants specifically for Akebia, highlighting disruptive forces, pricing pressures, and strategic levers to protect or grow market share.

Concise Porter's Five Forces for Akebia—one-sheet clarity to spot competitive risks and relief strategies fast, ready to drop into decks or stress-test across scenarios.

Customers Bargaining Power

Large Dialysis Organizations

Major providers DaVita Inc. and Fresenius Medical Care control roughly 70% of U.S. in-center dialysis capacity (2024), making them primary gatekeepers for Akebia Therapeutics’ Vafseo (vadadustat).

Their scale lets them demand deep volume discounts and preferred pricing at renewals—contracts often tilt pricing down 20–40% versus list.

Inclusion on these chains’ formularies is make-or-break: winning both could cover an estimated 60–80% of commercial U.S. dialysis demand; losing either sharply limits uptake.

Government Payors and Medicare

A vast majority of end-stage renal disease patients—about 84% in 2023—are covered by Medicare, giving the federal government major leverage over reimbursement rates and making payor policy a key revenue driver for Akebia Therapeutics. Changes to the Medicare bundled payment or the End-Stage Renal Disease Prospective Payment System (ESRD PPS), last updated materially in 2021 with annual adjustments, can shift incentives for using Akebia’s vadadustat by altering clinic margins. Akebia must align pricing to Medicare caps—ESRD PPS base rate was roughly $260 per dialysis treatment in 2024—so reimbursement cuts or bundle expansions could compress uptake and clinic preference. This forces continuous payer engagement, pricing flexibility, and scenario planning to keep therapies economically viable for dialysis providers.

Pharmacy Benefit Managers

PBMs negotiate drug tier placement for private insurers and can demand large rebates; in 2024 the top three PBMs (CVS Caremark, Express Scripts, OptumRx) managed ~80% of commercial lives, giving them outsized leverage over Akebia’s CKD non-dialysis drugs.

Failure to secure preferred formulary status with major PBMs can cut off access to ~60–70% of commercially insured CKD patients, and rebates of 20–50% can materially compress Akebia’s net price and margins.

Group Purchasing Organizations

Integrated Health Systems and Hospital Networks

Large integrated health systems like Kaiser Permanente and CommonSpirit increasingly centralize purchasing using comparative effectiveness and cost-benefit analyses; in 2024, hospital systems drove ~60% of US inpatient drug purchasing decisions, favoring protocols that prioritize lower-cost or established treatments over new branded therapies.

Akebia must supply robust health economic outcomes—real-world evidence, cost-per-QALY models, and budget-impact analyses—showing long-term savings versus ESAs and transfusions to win formulary placement.

- ~60% of inpatient drug buys by systems (2024)

- Protocols favor lower-cost/established care

- Require cost-per-QALY and budget-impact data

- Real-world evidence + long-term safety essential

Buyer oligopoly forces Akebia into 20–50% rebates, deep discounts, and heavy evidence

Large dialysis chains (DaVita, Fresenius ~70% 2024) plus Medicare (covers ~84% ESRD 2023; ESRD PPS ~$260/treatment in 2024), top PBMs (~80% lives) and GPOs (30–40% discounts; 5–15% hospital margin pressure 2024) hold strong leverage, forcing Akebia to accept 20–50% rebates, deep discounts, and produce robust health‑economic evidence to secure formulary access.

| Buyer | 2024 metric | Impact on Akebia |

|---|---|---|

| DaVita/Fresenius | ~70% in‑center capacity | Preferred formulary = 60–80% demand |

| Medicare (ESRD) | ~84% ESRD covered; PPS ~$260 | Sets reimbursement cap, shifts margins |

| Top PBMs | ~80% commercial lives | Rebates 20–50% |

| GPOs | 30–40% discounts | 5–15% hospital margin pressure |

Preview the Actual Deliverable

Akebia Porter's Five Forces Analysis

This preview shows the exact Akebia Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy; what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Akebia faces moderate buyer power, specialized supplier influence, and significant competitive rivalry as it navigates reimbursement pressures and patent cliffs in renal care markets.

Regulatory scrutiny and high development costs raise barriers for new entrants but also heighten substitute threats from emerging therapies and generics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Akebia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized API Contract Manufacturers

Clinical Research Organizations

Intellectual Property and Technology Licensors

Akebia relies on licensed HIF-PHI technologies and foundational patents that drive its vadadustat program; licensors wield leverage via royalty rates—industry-standard biopharma royalties range 2–10%—and litigation risk that can halt commercialization.

In 2025 Akebia's freedom to operate hinges on these agreements and milestone payments (recent deals show upfronts $5–50M), so maintaining licenses and defensive patent strategies is critical to avoid injunctions and revenue loss.

Specialized Logistics and Cold Chain Providers

Specialized logistics and cold chain providers hold strong bargaining power for Akebia because only a small pool meet FDA, EU GDP, and FDA Drug Supply Chain Security Act standards required for biopharmaceuticals; in 2024, ~65% of US pharma cold shipments used top-tier certified carriers, concentrating leverage.

Service disruptions—like TempControl carrier outages in Q3 2023—can cause drug shortages and revenue hits; a single-week cold-chain failure can cost a mid-size specialty drug maker $5–10M in lost sales and spoilage.

- Few certified distributors: ~65% market share by top-tier carriers (2024)

- High impact: 1-week failure ≈ $5–10M revenue loss

- Regulatory burden raises switching costs and supplier leverage

Regulatory and Compliance Consultants

Niche regulatory consultants for FDA and EMA kidney-disease approvals command strong supplier power: their specialized expertise is critical to secure and expand labels, and firms pay high fees—consulting rates often range from $300–$800/hour and program fees $250k–$2M per submission in 2024–2025.

The power reflects high stakes of regulatory failure—median FDA nephrology review times were ~10.8 months in 2024—and a small pool of senior experts, concentrating bargaining leverage.

- High fees: $300–$800/hour; $250k–$2M per submission

- Long reviews: median FDA nephrology review ~10.8 months (2024)

- Limited talent: few senior regulatory leads globally

Supplier concentration and service bottlenecks = major cost, delay & royalty risks

Suppliers hold moderate-to-strong power: API/CMO concentration (fewer than 10 global scale suppliers; $5–10M qualification; 8–12 week lead variance), CROs create 8–14 month delays/$5–20M extra, licensors demand 2–10% royalties and $5–50M upfronts, cold-chain/top carriers ~65% share (2024) with 1-week failure ≈ $5–10M loss, regulatory consultants $300–$800/hr.

| Supplier | Key metric | Impact |

|---|---|---|

| API/CMO | <10 suppliers; $5–10M qual | Price/timeline risk |

| CROs | 8–14mo; $5–20M | Trial delay/cost |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants specifically for Akebia, highlighting disruptive forces, pricing pressures, and strategic levers to protect or grow market share.

Concise Porter's Five Forces for Akebia—one-sheet clarity to spot competitive risks and relief strategies fast, ready to drop into decks or stress-test across scenarios.

Customers Bargaining Power

Large Dialysis Organizations

Major providers DaVita Inc. and Fresenius Medical Care control roughly 70% of U.S. in-center dialysis capacity (2024), making them primary gatekeepers for Akebia Therapeutics’ Vafseo (vadadustat).

Their scale lets them demand deep volume discounts and preferred pricing at renewals—contracts often tilt pricing down 20–40% versus list.

Inclusion on these chains’ formularies is make-or-break: winning both could cover an estimated 60–80% of commercial U.S. dialysis demand; losing either sharply limits uptake.

Government Payors and Medicare

A vast majority of end-stage renal disease patients—about 84% in 2023—are covered by Medicare, giving the federal government major leverage over reimbursement rates and making payor policy a key revenue driver for Akebia Therapeutics. Changes to the Medicare bundled payment or the End-Stage Renal Disease Prospective Payment System (ESRD PPS), last updated materially in 2021 with annual adjustments, can shift incentives for using Akebia’s vadadustat by altering clinic margins. Akebia must align pricing to Medicare caps—ESRD PPS base rate was roughly $260 per dialysis treatment in 2024—so reimbursement cuts or bundle expansions could compress uptake and clinic preference. This forces continuous payer engagement, pricing flexibility, and scenario planning to keep therapies economically viable for dialysis providers.

Pharmacy Benefit Managers

PBMs negotiate drug tier placement for private insurers and can demand large rebates; in 2024 the top three PBMs (CVS Caremark, Express Scripts, OptumRx) managed ~80% of commercial lives, giving them outsized leverage over Akebia’s CKD non-dialysis drugs.

Failure to secure preferred formulary status with major PBMs can cut off access to ~60–70% of commercially insured CKD patients, and rebates of 20–50% can materially compress Akebia’s net price and margins.

Group Purchasing Organizations

Integrated Health Systems and Hospital Networks

Large integrated health systems like Kaiser Permanente and CommonSpirit increasingly centralize purchasing using comparative effectiveness and cost-benefit analyses; in 2024, hospital systems drove ~60% of US inpatient drug purchasing decisions, favoring protocols that prioritize lower-cost or established treatments over new branded therapies.

Akebia must supply robust health economic outcomes—real-world evidence, cost-per-QALY models, and budget-impact analyses—showing long-term savings versus ESAs and transfusions to win formulary placement.

- ~60% of inpatient drug buys by systems (2024)

- Protocols favor lower-cost/established care

- Require cost-per-QALY and budget-impact data

- Real-world evidence + long-term safety essential

Buyer oligopoly forces Akebia into 20–50% rebates, deep discounts, and heavy evidence

Large dialysis chains (DaVita, Fresenius ~70% 2024) plus Medicare (covers ~84% ESRD 2023; ESRD PPS ~$260/treatment in 2024), top PBMs (~80% lives) and GPOs (30–40% discounts; 5–15% hospital margin pressure 2024) hold strong leverage, forcing Akebia to accept 20–50% rebates, deep discounts, and produce robust health‑economic evidence to secure formulary access.

| Buyer | 2024 metric | Impact on Akebia |

|---|---|---|

| DaVita/Fresenius | ~70% in‑center capacity | Preferred formulary = 60–80% demand |

| Medicare (ESRD) | ~84% ESRD covered; PPS ~$260 | Sets reimbursement cap, shifts margins |

| Top PBMs | ~80% commercial lives | Rebates 20–50% |

| GPOs | 30–40% discounts | 5–15% hospital margin pressure |

Preview the Actual Deliverable

Akebia Porter's Five Forces Analysis

This preview shows the exact Akebia Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy; what you see is what you get.