Akebia PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Spot the external forces shaping Akebia’s prospects—from regulatory scrutiny and biotech funding cycles to shifting healthcare policies and tech-driven R&D advances—and turn those signals into strategy; purchase the full PESTLE for a ready-made, editable deep dive that speeds your analysis and strengthens investment or strategic decisions.

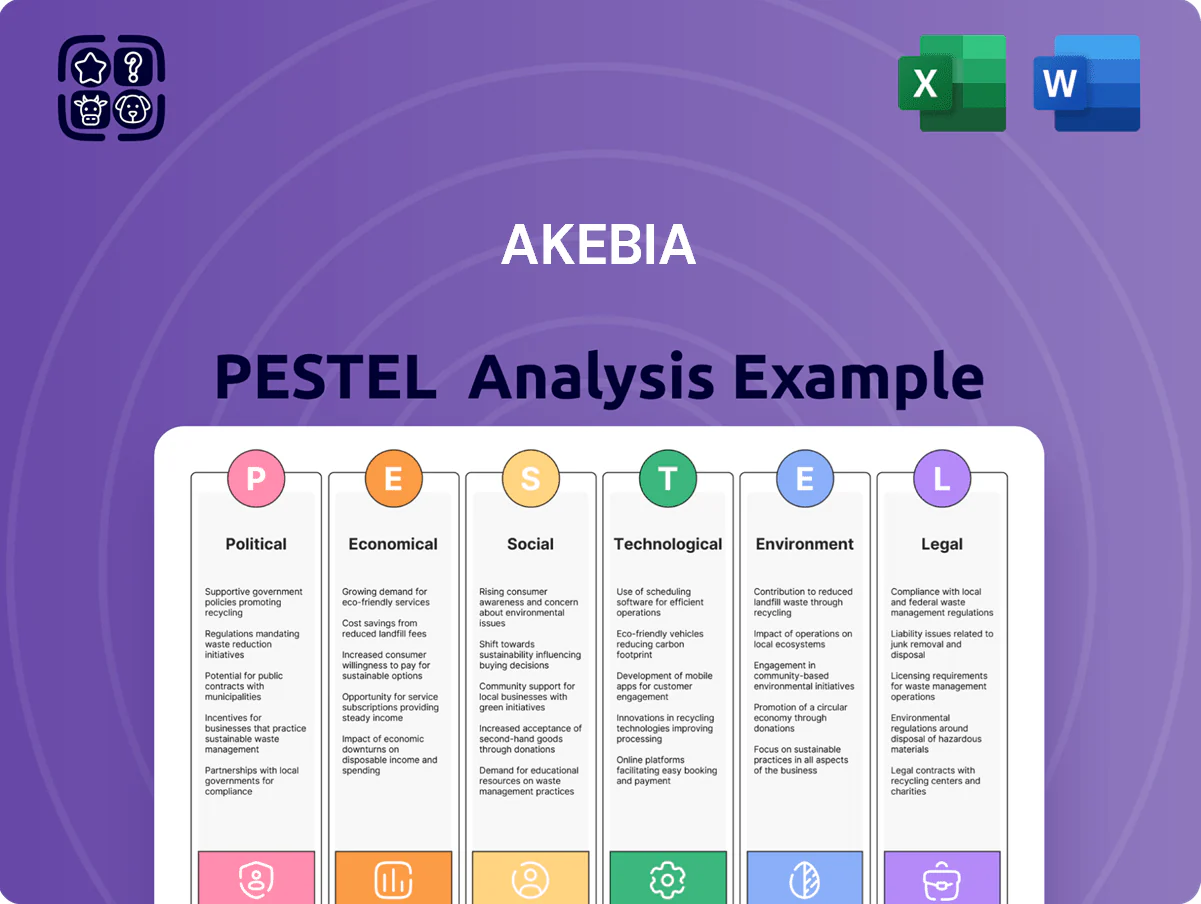

Political factors

Medicare reimbursement policy changes

The Inflation Reduction Act's drug pricing provisions continue to pressure Medicare Part D, with estimated manufacturer rebates and price negotiations projected to reduce net drug revenues by up to 10–15% for some specialty drugs through 2026; for Akebia this heightens pricing scrutiny for Vafseo. Changes to the ESRD bundled payment—affecting roughly 550,000 US dialysis patients—alter incentives for adopting add-on therapies, impacting potential uptake of HIF-PHI treatments. Navigating federal reimbursement, including QIP and ESRD Prospective Payment System adjustments, is critical to secure formulary placement and preserve net present value of Vafseo revenue streams.

FDA regulatory oversight and scrutiny

The FDA maintains stringent oversight of anemia treatments after safety concerns in the HIF-PHI class, with 2024 adverse-event reviews increasing review times by ~20% industry-wide; Akebia must sustain transparent FDA engagement to meet post-marketing requirements and potential label expansions tied to verifiable safety data. Political pressure to balance innovation and patient safety affects approval timelines and costs—median oncology/rare-disease approval costs rose to $300–400M in 2023–24—raising capital needs for Akebia’s pipeline.

International trade and geopolitical stability

As Akebia scales via partnerships in Japan (Kyowa Kirin licensing) and Europe, shifts in tariffs or sanctions could disrupt APIs and finished-product flows; Japan and EU accounted for roughly 30% of ex-US royalties in 2024, exposing revenue to trade risk.

Geopolitical tensions—e.g., 2024 supply-chain reallocations after China export controls—raise procurement costs; a 5-10% tariff swing on APIs could increase COGS materially for small-mid biotech players like Akebia.

Active monitoring of trade policy, customs regimes and diplomatic ties is essential to protect royalty streams and maintain access to contract manufacturing and clinical supply chains across key markets.

Federal funding for kidney disease research

Federal prioritization like the 2019 Advancing American Kidney Health initiative and expanded FY2025 NIH kidney funding (~$575M projected for kidney research in 2024–25) increases screening and early CKD detection, enlarging the treatable patient base and boosting demand for novel therapeutics.

Higher federal support and incentives for home dialysis align with Akebia’s portfolio and could accelerate uptake of partner therapies and supportive care solutions, improving market access and reimbursement prospects.

- Advancing American Kidney Health drives screening/early detection, expanding patient pool

- NIH/kidney funding ~ $575M (2024–25) supports R&D pipeline growth

- Policy emphasis on home dialysis favors Akebia’s market positioning and reimbursement

Healthcare reform and drug pricing legislation

Ongoing proposals to cap seniors' out-of-pocket costs (e.g., Medicare cap bills targeting $2,000–$2,500/year) could increase patient access to Akebia’s anemia and nephrology therapies, potentially expanding addressable market by millions of beneficiaries; CMS drug spending reached $131B in 2024, highlighting fiscal pressure on pricing.

Rebate reform and PBM transparency debates—Congressional proposals in 2024 aimed at eliminating certain rebates—could raise net realized prices for Akebia or compress commercial margins depending on passthrough mechanics and contracting.

Monitoring legislative timelines and modeling scenarios is critical: a 10–20% shift in net price realization would materially affect 2025–2027 revenue forecasts and valuation models.

- Potential Medicare OOP cap: $2,000–$2,500/year

- CMS drug spending: $131B (2024)

- Rebate reform could change net prices by ~10–20%

- Essential to update revenue forecasts with legislative scenarios

Policy, funding, and FDA delays squeeze Vafseo pricing and market opportunity

IRAs drug pricing, ESRD bundle changes, and potential Medicare OOP caps (proposed $2,000–$2,500) pressure Vafseo pricing and uptake; NIH kidney funding (~$575M 2024–25) and home-dialysis incentives expand addressable market; FDA safety scrutiny and longer review times (~+20% in 2024) raise approval costs; trade/tariff risks (5–10% API cost swing) threaten COGS and ex-US royalties (~30% of 2024 ex-US royalties).

| Factor | Key metric |

|---|---|

| Medicare spend | $131B (2024) |

| NIH kidney funding | $575M (2024–25) |

| FDA review delay | +20% (2024) |

| API tariff risk | 5–10% COGS swing |

What is included in the product

Explores how macro-environmental factors uniquely affect Akebia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, industry-specific examples, forward-looking insights, and practical implications to help executives, consultants, and investors identify risks, opportunities, and strategy actions for market and regulatory scenarios.

Concise PESTLE summary tailored to Akebia that highlights regulatory, market, and technological risks for quick inclusion in presentations or strategy sessions.

Economic factors

Cost-benefit analysis of HIF-PHI vs ESAs

Vafseo’s uptake hinges on drug-cost parity with ESAs; 2024 U.S. Medicare Part B reimbursement for injectable ESAs averages about $1,200–$1,800 per patient/month in dialysis settings, so Akebia must price oral HIF-PHI to match or undercut total per-patient costs.

Dialysis centers factor administration savings—oral dosing avoids roughly $150–$300 monthly nursing/infusion costs—and lower monitoring could cut overall cost of care by an estimated 5–15% versus injectables.

To secure share in a cost-sensitive market, Akebia needs real-world pharmacoeconomic data showing Vafseo achieves equal efficacy with net healthcare savings; payers in 2024 increasingly demand value-based contracting and outcomes data.

Inflationary pressures on R&D and manufacturing

Rising costs for lab materials, specialized labor, and clinical trials have pushed biopharma input prices up ~8–12% in 2024, straining Akebia’s cash runway after 2023 net loss of $156M; controlling these inflationary expenses is critical to restore a path toward sustained profitability.

Interest rates and capital market access

Prevailing US federal funds rate at 5.25–5.50% (Dec 2025 target range) raises Akebia’s borrowing costs, increasing interest expense on new debt and potentially reducing available financing for R&D and commercialization.

Higher rates compress valuations by discounting future cash flows, which could lower Akebia’s market cap from 2024–2025 revenue expectations (2025 consensus revenue ~$160–180M among analysts).

Volatile capital markets in 2024–2025 saw biotech IPO and secondary issuance activity decline ~40% year-over-year, so Akebia must preserve liquidity and flexible debt covenants to support commercial scaling.

Global exchange rate fluctuations

- JPY and EUR swings materially affect reported royalties

- 5% currency moves can change revenues by several million USD

- Hedging reduced FX volatility ~40% for peers in 2023

- Geographic revenue diversification mitigates single-currency risk

Market penetration in the dialysis sector

The economic health of major dialysis providers like Fresenius and DaVita, which together serve over 70% of US dialysis patients, directly affects Akebia’s sales and pricing power; Fresenius and DaVita reported combined 2024 dialysis revenues exceeding $30 billion.

Ongoing consolidation has increased buyer leverage, enabling larger rebates—DaVita negotiated estimated formulary discounts up to 20% in recent contracts—pressuring Akebia’s margins.

Therefore, Akebia must analyze providers’ capex, patient growth (~2% annual), and payer mixes to secure formulary placement and favorable protocol inclusion.

- Major providers control >70% market share

- Combined dialysis revenue >$30B (2024)

- Contract rebates/discounts up to ~20%

- Patient growth ≈2% annually

Oral ESA cuts $150–300/mo, may trim care 5–15% as costs, rates, rebates pressure Akebia

Vafseo pricing must match injectable ESA total costs (~$1,200–$1,800/month dialysis); oral dosing saves ~$150–$300/month in admin and may cut care costs 5–15%. Inflation raised biopharma input costs ~8–12% in 2024, aggravating Akebia’s post-2023 $156M net loss; 2024–25 revenue consensus ~$160–180M. Higher rates (Fed 5.25–5.50%) raise borrowing costs; FX moves (5% EUR) can swing revenues $3–5M; major providers (>70% share) drive rebates up to ~20%.

| Metric | 2024–25 Value |

|---|---|

| ESA cost (dialysis) | $1,200–$1,800/mo |

| Admin savings (oral) | $150–$300/mo |

| Input cost inflation | +8–12% |

| Akebia 2023 net loss | $156M |

| 2025 revenue consensus | $160–$180M |

| Fed funds | 5.25–5.50% |

| FX sensitivity (5% EUR) | $3–$5M |

| Dialysis provider market share | >70% |

| Typical rebates | up to ~20% |

Preview the Actual Deliverable

Akebia PESTLE Analysis

The preview shown here is the exact Akebia PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Spot the external forces shaping Akebia’s prospects—from regulatory scrutiny and biotech funding cycles to shifting healthcare policies and tech-driven R&D advances—and turn those signals into strategy; purchase the full PESTLE for a ready-made, editable deep dive that speeds your analysis and strengthens investment or strategic decisions.

Political factors

Medicare reimbursement policy changes

The Inflation Reduction Act's drug pricing provisions continue to pressure Medicare Part D, with estimated manufacturer rebates and price negotiations projected to reduce net drug revenues by up to 10–15% for some specialty drugs through 2026; for Akebia this heightens pricing scrutiny for Vafseo. Changes to the ESRD bundled payment—affecting roughly 550,000 US dialysis patients—alter incentives for adopting add-on therapies, impacting potential uptake of HIF-PHI treatments. Navigating federal reimbursement, including QIP and ESRD Prospective Payment System adjustments, is critical to secure formulary placement and preserve net present value of Vafseo revenue streams.

FDA regulatory oversight and scrutiny

The FDA maintains stringent oversight of anemia treatments after safety concerns in the HIF-PHI class, with 2024 adverse-event reviews increasing review times by ~20% industry-wide; Akebia must sustain transparent FDA engagement to meet post-marketing requirements and potential label expansions tied to verifiable safety data. Political pressure to balance innovation and patient safety affects approval timelines and costs—median oncology/rare-disease approval costs rose to $300–400M in 2023–24—raising capital needs for Akebia’s pipeline.

International trade and geopolitical stability

As Akebia scales via partnerships in Japan (Kyowa Kirin licensing) and Europe, shifts in tariffs or sanctions could disrupt APIs and finished-product flows; Japan and EU accounted for roughly 30% of ex-US royalties in 2024, exposing revenue to trade risk.

Geopolitical tensions—e.g., 2024 supply-chain reallocations after China export controls—raise procurement costs; a 5-10% tariff swing on APIs could increase COGS materially for small-mid biotech players like Akebia.

Active monitoring of trade policy, customs regimes and diplomatic ties is essential to protect royalty streams and maintain access to contract manufacturing and clinical supply chains across key markets.

Federal funding for kidney disease research

Federal prioritization like the 2019 Advancing American Kidney Health initiative and expanded FY2025 NIH kidney funding (~$575M projected for kidney research in 2024–25) increases screening and early CKD detection, enlarging the treatable patient base and boosting demand for novel therapeutics.

Higher federal support and incentives for home dialysis align with Akebia’s portfolio and could accelerate uptake of partner therapies and supportive care solutions, improving market access and reimbursement prospects.

- Advancing American Kidney Health drives screening/early detection, expanding patient pool

- NIH/kidney funding ~ $575M (2024–25) supports R&D pipeline growth

- Policy emphasis on home dialysis favors Akebia’s market positioning and reimbursement

Healthcare reform and drug pricing legislation

Ongoing proposals to cap seniors' out-of-pocket costs (e.g., Medicare cap bills targeting $2,000–$2,500/year) could increase patient access to Akebia’s anemia and nephrology therapies, potentially expanding addressable market by millions of beneficiaries; CMS drug spending reached $131B in 2024, highlighting fiscal pressure on pricing.

Rebate reform and PBM transparency debates—Congressional proposals in 2024 aimed at eliminating certain rebates—could raise net realized prices for Akebia or compress commercial margins depending on passthrough mechanics and contracting.

Monitoring legislative timelines and modeling scenarios is critical: a 10–20% shift in net price realization would materially affect 2025–2027 revenue forecasts and valuation models.

- Potential Medicare OOP cap: $2,000–$2,500/year

- CMS drug spending: $131B (2024)

- Rebate reform could change net prices by ~10–20%

- Essential to update revenue forecasts with legislative scenarios

Policy, funding, and FDA delays squeeze Vafseo pricing and market opportunity

IRAs drug pricing, ESRD bundle changes, and potential Medicare OOP caps (proposed $2,000–$2,500) pressure Vafseo pricing and uptake; NIH kidney funding (~$575M 2024–25) and home-dialysis incentives expand addressable market; FDA safety scrutiny and longer review times (~+20% in 2024) raise approval costs; trade/tariff risks (5–10% API cost swing) threaten COGS and ex-US royalties (~30% of 2024 ex-US royalties).

| Factor | Key metric |

|---|---|

| Medicare spend | $131B (2024) |

| NIH kidney funding | $575M (2024–25) |

| FDA review delay | +20% (2024) |

| API tariff risk | 5–10% COGS swing |

What is included in the product

Explores how macro-environmental factors uniquely affect Akebia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, industry-specific examples, forward-looking insights, and practical implications to help executives, consultants, and investors identify risks, opportunities, and strategy actions for market and regulatory scenarios.

Concise PESTLE summary tailored to Akebia that highlights regulatory, market, and technological risks for quick inclusion in presentations or strategy sessions.

Economic factors

Cost-benefit analysis of HIF-PHI vs ESAs

Vafseo’s uptake hinges on drug-cost parity with ESAs; 2024 U.S. Medicare Part B reimbursement for injectable ESAs averages about $1,200–$1,800 per patient/month in dialysis settings, so Akebia must price oral HIF-PHI to match or undercut total per-patient costs.

Dialysis centers factor administration savings—oral dosing avoids roughly $150–$300 monthly nursing/infusion costs—and lower monitoring could cut overall cost of care by an estimated 5–15% versus injectables.

To secure share in a cost-sensitive market, Akebia needs real-world pharmacoeconomic data showing Vafseo achieves equal efficacy with net healthcare savings; payers in 2024 increasingly demand value-based contracting and outcomes data.

Inflationary pressures on R&D and manufacturing

Rising costs for lab materials, specialized labor, and clinical trials have pushed biopharma input prices up ~8–12% in 2024, straining Akebia’s cash runway after 2023 net loss of $156M; controlling these inflationary expenses is critical to restore a path toward sustained profitability.

Interest rates and capital market access

Prevailing US federal funds rate at 5.25–5.50% (Dec 2025 target range) raises Akebia’s borrowing costs, increasing interest expense on new debt and potentially reducing available financing for R&D and commercialization.

Higher rates compress valuations by discounting future cash flows, which could lower Akebia’s market cap from 2024–2025 revenue expectations (2025 consensus revenue ~$160–180M among analysts).

Volatile capital markets in 2024–2025 saw biotech IPO and secondary issuance activity decline ~40% year-over-year, so Akebia must preserve liquidity and flexible debt covenants to support commercial scaling.

Global exchange rate fluctuations

- JPY and EUR swings materially affect reported royalties

- 5% currency moves can change revenues by several million USD

- Hedging reduced FX volatility ~40% for peers in 2023

- Geographic revenue diversification mitigates single-currency risk

Market penetration in the dialysis sector

The economic health of major dialysis providers like Fresenius and DaVita, which together serve over 70% of US dialysis patients, directly affects Akebia’s sales and pricing power; Fresenius and DaVita reported combined 2024 dialysis revenues exceeding $30 billion.

Ongoing consolidation has increased buyer leverage, enabling larger rebates—DaVita negotiated estimated formulary discounts up to 20% in recent contracts—pressuring Akebia’s margins.

Therefore, Akebia must analyze providers’ capex, patient growth (~2% annual), and payer mixes to secure formulary placement and favorable protocol inclusion.

- Major providers control >70% market share

- Combined dialysis revenue >$30B (2024)

- Contract rebates/discounts up to ~20%

- Patient growth ≈2% annually

Oral ESA cuts $150–300/mo, may trim care 5–15% as costs, rates, rebates pressure Akebia

Vafseo pricing must match injectable ESA total costs (~$1,200–$1,800/month dialysis); oral dosing saves ~$150–$300/month in admin and may cut care costs 5–15%. Inflation raised biopharma input costs ~8–12% in 2024, aggravating Akebia’s post-2023 $156M net loss; 2024–25 revenue consensus ~$160–180M. Higher rates (Fed 5.25–5.50%) raise borrowing costs; FX moves (5% EUR) can swing revenues $3–5M; major providers (>70% share) drive rebates up to ~20%.

| Metric | 2024–25 Value |

|---|---|

| ESA cost (dialysis) | $1,200–$1,800/mo |

| Admin savings (oral) | $150–$300/mo |

| Input cost inflation | +8–12% |

| Akebia 2023 net loss | $156M |

| 2025 revenue consensus | $160–$180M |

| Fed funds | 5.25–5.50% |

| FX sensitivity (5% EUR) | $3–$5M |

| Dialysis provider market share | >70% |

| Typical rebates | up to ~20% |

Preview the Actual Deliverable

Akebia PESTLE Analysis

The preview shown here is the exact Akebia PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.