Aker BP Boston Consulting Group Matrix

Actionable Strategy Starts Here

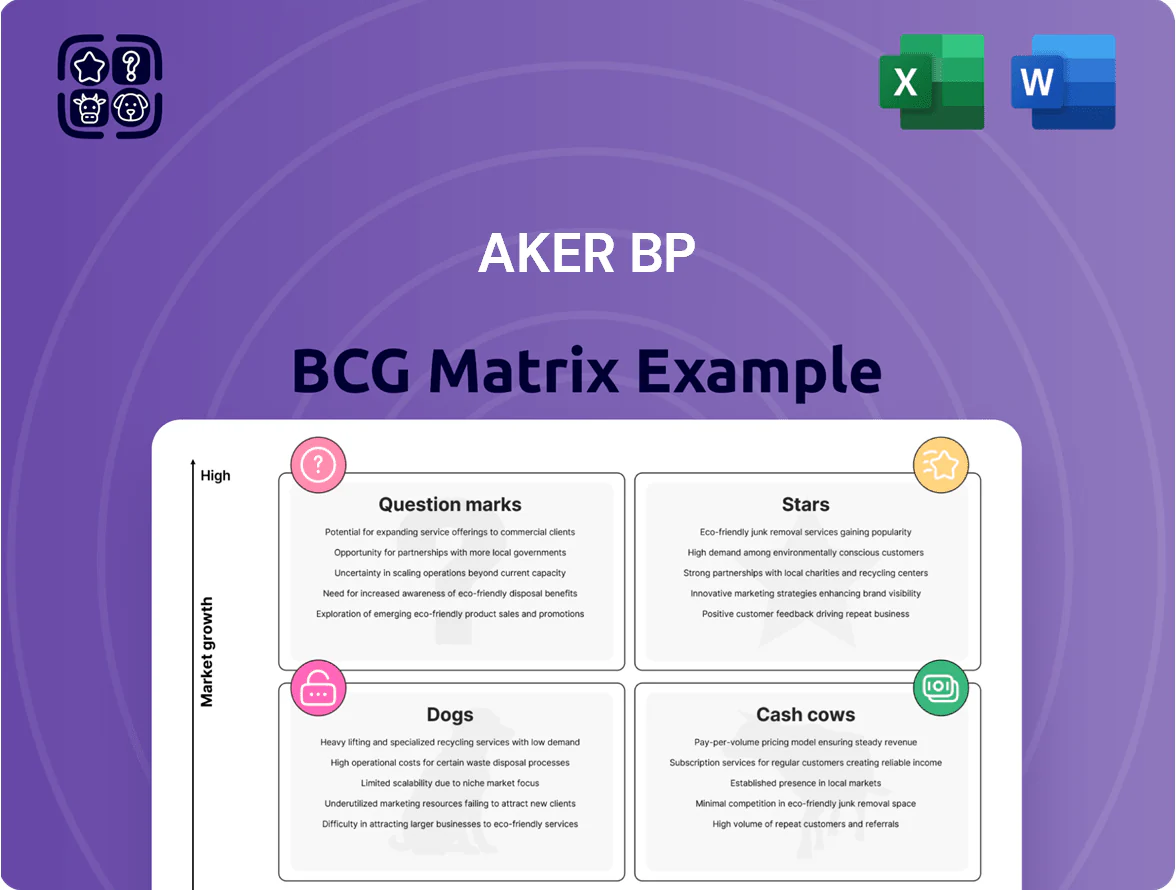

Aker BP's BCG Matrix preview highlights how its core assets and product lines map across market growth and relative share, revealing which fields are driving cash flow and which need strategic attention. This snapshot shows potential Stars in high-growth basins and Cash Cows generating steady returns, but full quadrant placements require deeper data. Purchase the complete BCG Matrix for detailed, data-backed quadrant assignments, actionable recommendations, and ready-to-use Word and Excel deliverables to guide capital allocation and operational strategy.

Stars

Yggdrasil Area Development

The Yggdrasil Area Development is a Stars-tier asset in Aker BP’s BCG Matrix, driving high growth and commanding significant future market share on the Norwegian Continental Shelf.

It is one of the largest ongoing projects, with total capex ~NOK 55–65 billion and peak production guidance ~120–150 kb/d gross, requiring heavy upfront investment but poised for long-term volume growth.

By late 2025, Yggdrasil remains Aker BP’s primary investment focus to secure transition into a future cash-generating leader as basin production shifts toward mid-2030s output.

NOAKA Area Integration

The North of Alvheim, Krafla and Askja integration forms a high-growth hub responsible for ~60% of Aker BP’s 2025 reserve additions (≈350 MMboe) and anchors the company’s growth in the Aker BP BCG Matrix Stars quadrant.

It requires heavy reinvestment—capex guidance of NOK 20–25bn for 2024–26—to build towers, pipelines and processing, pressing margins but enabling volume scale.

Maintaining this hub is critical to Aker BP’s competitive edge as fields target plateau production of ~120 kboe/d combined, offsetting North Sea decline and supporting long‑term value.

Digitalization and Integrated Operations

Aker BP leads in industrial software and data-driven drilling, boosting recovery rates by up to 15% on pilot fields and cutting drilling time by ~20% per Equinor-linked studies in 2024; these initiatives are high-growth stars in the BCG matrix. They demand ongoing capex—Aker BP spent ~USD 120m on digital and automation in 2024—but yield large efficiency gains and lower lifting costs. As tech matures, it scales across the portfolio, raising NPV and extending field life, with digital-led projects contributing ~8–10% of 2025 production upside.

Valhall PWP-Fenris Project

The Valhall PWP-Fenris redevelopment is Aker BP’s star: sanctioned 2021–2024 capex ~NOK 40–50bn, targeting peak production ~150–180 kbopd combined and +0.5–1.0 bcfd gas, securing southern North Sea dominance with 20+ year plateau and reserves >300 mmboe.

It uses low-emission electrification and subsea tiebacks, cutting CO2 intensity toward Aker BP’s 0.6–0.8 kg/boe target, but consumes heavy near-term cash to fund long-life, high-volume output.

- Capex ~NOK 40–50bn (2021–2024)

- Peak ~150–180 kbopd + 0.5–1.0 bcfd

- Reserves >300 mmboe, 20+ year plateau

- CO2 intensity target 0.6–0.8 kg/boe

Low Carbon Production Technologies

Investment in electrification and carbon-capture on offshore platforms is a high-growth area driven by EU and UK 2030/2050 decarbonization targets; global CCS capacity grew 30% in 2024 to 55 MtCO2/year, showing demand for such tech.

Aker BP leads in low-emission production with a 2024 reported upstream emissions intensity ~5 kg CO2/boe, attracting premium capital and lower cost-of-capital for green projects.

Implementation costs are high—electrification and CCS CAPEX can add 15–25% to project costs—but they are essential to keep operating licenses and access to ESG-linked financing.

- High growth: CCS capacity +30% (2024)

- Aker BP emissions ~5 kg CO2/boe (2024)

- CAPEX premium 15–25%

- Drives access to ESG capital, regulatory compliance

Aker BP’s growth trio—Yggdrasil, North hub & Valhall—driving 2025 upside ~300–420 kboe/d

Stars: Yggdrasil, North‑of‑Alvheim/Krafla‑Askja hub, Valhall PWP‑Fenris and digital/low‑emission tech are Aker BP’s high‑growth assets, driving 2024–25 capex ~NOK 95–140bn and anchoring 2025 production upside ~300–420 kboe/d with reserve additions ≈350 MMboe.

| Asset | Capex (NOK) | Peak prod (kboe/d) | Reserves (MMboe) |

|---|---|---|---|

| Yggdrasil | 55–65bn | 120–150 | — |

| North hub | 20–25bn | ≈120 | ≈350 |

| Valhall PWP‑Fenris | 40–50bn | 150–180 | >300 |

What is included in the product

BCG Matrix analysis of Aker BP’s units with strategic guidance—identify Stars, Cash Cows, Question Marks, Dogs, and investment/exit priorities.

One-page Aker BP BCG Matrix mapping assets by growth and share for quick strategic decisions.

Cash Cows

Johan Sverdrup Field Stake

Johan Sverdrup, Norway’s largest oil field, delivers low-cost production of about 470 kbpd gross (2024) and accounted for roughly 15% of Norway’s crude output in 2024, giving Aker BP a commanding market share in the segment.

Now at plateau, operating costs near USD 10–12/boe and capex

That cash cow funds dividends—Aker BP paid NOK 12.5bn in dividends in 2024—and bankrolls exploration and tie‑backs, underpinning growth while keeping balance‑sheet leverage manageable.

Alvheim Area Production

Alvheim Area Production is a mature, high-efficiency hub that has exceeded initial recovery expectations, producing ~60–70 kbbl/d gross in 2024 and lifting cumulative recoveries above original estimates by ~15%.

Its dominant regional position and tie‑back infrastructure keep operating costs low (OPEX ~6–8 USD/boe in 2024) and maintenance capex minimal, yielding EBITDA margins north of 55%.

The asset generated ~USD 1.1–1.3 billion free cash flow in 2024, consistently funding Aker BP’s debt service and supporting ~30–40% of the company’s organic growth budget.

Edvard Grieg Field Operations

Post-merger with Lundin Energy (closed Apr 2024), Edvard Grieg now functions as a cash cow for Aker BP, delivering steady free cash flow—about NOK 6–8 billion annually in 2024–2025—thanks to 50–70 kbpd net production and low unit OPEX (~USD 10–12/boe).

Operating in mature North Sea geology with 85% reservoir recovery confidence, Aker BP targets small tie-backs and optimized waterfloods to raise recovery by ~5–8% and squeeze incremental EUR ~30–50 MMboe from existing infrastructure.

Ivar Aasen Field

Ivar Aasen is a mature, steady producer in Aker BP’s portfolio, delivering ~120–140 kbpd (thousand barrels per day) and contributing roughly NOK 12–18 billion annually in cash flow in 2024 after taxes and operating costs.

The field’s low operational complexity and capex needs free cash for Aker BP’s aggressive exploration and development plan, which saw NOK 30+ billion allocated to new projects in 2024.

- Production: ~120–140 kbpd (2024)

- Cash flow: ~NOK 12–18 bn (2024, net)

- Capex: relatively low maintenance spend

- Funds redeployed: NOK 30+ bn to exploration/development (2024)

Skarv Area Gas Production

The Skarv area is a cash cow for Aker BP, delivering ~1.2–1.5 bcm of gas/year (2024) and using existing 370 km pipeline export links to Nyhamna and Kollsnes, driving high-margin sales in Europe with low incremental capex.

Skarv’s steady EBITDA contribution—roughly NOK 6–8 billion annual run-rate in 2024—supports Aker BP’s dividend (NOK 20.00/share 2024 payout policy) with limited reinvestment need.

It underpins portfolio stability amid mature demand, freeing cash for new growth while preserving shareholder returns.

- 2024 gas output ~1.2–1.5 bcm

- Estimated EBITDA NOK 6–8 bn/year

- Existing export pipelines, low capex

- Supports NOK 20.00/share 2024 dividend

Aker BP’s five cash cows: >$5.5–6.5bn FCF in 2024 funding NOK 12.5bn dividends

Aker BP’s cash cows (Johan Sverdrup, Alvheim, Edvard Grieg, Ivar Aasen, Skarv) delivered ~700–820 kbpd combined oil and ~1.2–1.5 bcm gas in 2024, generating >USD 5.5–6.5bn free cash flow, funding NOK 12.5bn dividends (2024) and NOK 30+bn redeployed to exploration/development.

| Asset | 2024 prod | FCF 2024 |

|---|---|---|

| Johan Sverdrup | 470 kbpd | USD >3bn |

| Alvheim | 60–70 kbpd | USD 1.1–1.3bn |

| Edvard Grieg | 50–70 kbpd | NOK 6–8bn |

| Ivar Aasen | 120–140 kbpd | NOK 12–18bn |

| Skarv | 1.2–1.5 bcm gas | NOK 6–8bn |

Preview = Final Product

Aker BP BCG Matrix

The file you're previewing is the exact Aker BP BCG Matrix report you'll receive after purchase — no watermarks, no sample labels, just the fully formatted, presentation-ready analysis aligned to current market data and strategic frameworks.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Aker BP's BCG Matrix preview highlights how its core assets and product lines map across market growth and relative share, revealing which fields are driving cash flow and which need strategic attention. This snapshot shows potential Stars in high-growth basins and Cash Cows generating steady returns, but full quadrant placements require deeper data. Purchase the complete BCG Matrix for detailed, data-backed quadrant assignments, actionable recommendations, and ready-to-use Word and Excel deliverables to guide capital allocation and operational strategy.

Stars

Yggdrasil Area Development

The Yggdrasil Area Development is a Stars-tier asset in Aker BP’s BCG Matrix, driving high growth and commanding significant future market share on the Norwegian Continental Shelf.

It is one of the largest ongoing projects, with total capex ~NOK 55–65 billion and peak production guidance ~120–150 kb/d gross, requiring heavy upfront investment but poised for long-term volume growth.

By late 2025, Yggdrasil remains Aker BP’s primary investment focus to secure transition into a future cash-generating leader as basin production shifts toward mid-2030s output.

NOAKA Area Integration

The North of Alvheim, Krafla and Askja integration forms a high-growth hub responsible for ~60% of Aker BP’s 2025 reserve additions (≈350 MMboe) and anchors the company’s growth in the Aker BP BCG Matrix Stars quadrant.

It requires heavy reinvestment—capex guidance of NOK 20–25bn for 2024–26—to build towers, pipelines and processing, pressing margins but enabling volume scale.

Maintaining this hub is critical to Aker BP’s competitive edge as fields target plateau production of ~120 kboe/d combined, offsetting North Sea decline and supporting long‑term value.

Digitalization and Integrated Operations

Aker BP leads in industrial software and data-driven drilling, boosting recovery rates by up to 15% on pilot fields and cutting drilling time by ~20% per Equinor-linked studies in 2024; these initiatives are high-growth stars in the BCG matrix. They demand ongoing capex—Aker BP spent ~USD 120m on digital and automation in 2024—but yield large efficiency gains and lower lifting costs. As tech matures, it scales across the portfolio, raising NPV and extending field life, with digital-led projects contributing ~8–10% of 2025 production upside.

Valhall PWP-Fenris Project

The Valhall PWP-Fenris redevelopment is Aker BP’s star: sanctioned 2021–2024 capex ~NOK 40–50bn, targeting peak production ~150–180 kbopd combined and +0.5–1.0 bcfd gas, securing southern North Sea dominance with 20+ year plateau and reserves >300 mmboe.

It uses low-emission electrification and subsea tiebacks, cutting CO2 intensity toward Aker BP’s 0.6–0.8 kg/boe target, but consumes heavy near-term cash to fund long-life, high-volume output.

- Capex ~NOK 40–50bn (2021–2024)

- Peak ~150–180 kbopd + 0.5–1.0 bcfd

- Reserves >300 mmboe, 20+ year plateau

- CO2 intensity target 0.6–0.8 kg/boe

Low Carbon Production Technologies

Investment in electrification and carbon-capture on offshore platforms is a high-growth area driven by EU and UK 2030/2050 decarbonization targets; global CCS capacity grew 30% in 2024 to 55 MtCO2/year, showing demand for such tech.

Aker BP leads in low-emission production with a 2024 reported upstream emissions intensity ~5 kg CO2/boe, attracting premium capital and lower cost-of-capital for green projects.

Implementation costs are high—electrification and CCS CAPEX can add 15–25% to project costs—but they are essential to keep operating licenses and access to ESG-linked financing.

- High growth: CCS capacity +30% (2024)

- Aker BP emissions ~5 kg CO2/boe (2024)

- CAPEX premium 15–25%

- Drives access to ESG capital, regulatory compliance

Aker BP’s growth trio—Yggdrasil, North hub & Valhall—driving 2025 upside ~300–420 kboe/d

Stars: Yggdrasil, North‑of‑Alvheim/Krafla‑Askja hub, Valhall PWP‑Fenris and digital/low‑emission tech are Aker BP’s high‑growth assets, driving 2024–25 capex ~NOK 95–140bn and anchoring 2025 production upside ~300–420 kboe/d with reserve additions ≈350 MMboe.

| Asset | Capex (NOK) | Peak prod (kboe/d) | Reserves (MMboe) |

|---|---|---|---|

| Yggdrasil | 55–65bn | 120–150 | — |

| North hub | 20–25bn | ≈120 | ≈350 |

| Valhall PWP‑Fenris | 40–50bn | 150–180 | >300 |

What is included in the product

BCG Matrix analysis of Aker BP’s units with strategic guidance—identify Stars, Cash Cows, Question Marks, Dogs, and investment/exit priorities.

One-page Aker BP BCG Matrix mapping assets by growth and share for quick strategic decisions.

Cash Cows

Johan Sverdrup Field Stake

Johan Sverdrup, Norway’s largest oil field, delivers low-cost production of about 470 kbpd gross (2024) and accounted for roughly 15% of Norway’s crude output in 2024, giving Aker BP a commanding market share in the segment.

Now at plateau, operating costs near USD 10–12/boe and capex

That cash cow funds dividends—Aker BP paid NOK 12.5bn in dividends in 2024—and bankrolls exploration and tie‑backs, underpinning growth while keeping balance‑sheet leverage manageable.

Alvheim Area Production

Alvheim Area Production is a mature, high-efficiency hub that has exceeded initial recovery expectations, producing ~60–70 kbbl/d gross in 2024 and lifting cumulative recoveries above original estimates by ~15%.

Its dominant regional position and tie‑back infrastructure keep operating costs low (OPEX ~6–8 USD/boe in 2024) and maintenance capex minimal, yielding EBITDA margins north of 55%.

The asset generated ~USD 1.1–1.3 billion free cash flow in 2024, consistently funding Aker BP’s debt service and supporting ~30–40% of the company’s organic growth budget.

Edvard Grieg Field Operations

Post-merger with Lundin Energy (closed Apr 2024), Edvard Grieg now functions as a cash cow for Aker BP, delivering steady free cash flow—about NOK 6–8 billion annually in 2024–2025—thanks to 50–70 kbpd net production and low unit OPEX (~USD 10–12/boe).

Operating in mature North Sea geology with 85% reservoir recovery confidence, Aker BP targets small tie-backs and optimized waterfloods to raise recovery by ~5–8% and squeeze incremental EUR ~30–50 MMboe from existing infrastructure.

Ivar Aasen Field

Ivar Aasen is a mature, steady producer in Aker BP’s portfolio, delivering ~120–140 kbpd (thousand barrels per day) and contributing roughly NOK 12–18 billion annually in cash flow in 2024 after taxes and operating costs.

The field’s low operational complexity and capex needs free cash for Aker BP’s aggressive exploration and development plan, which saw NOK 30+ billion allocated to new projects in 2024.

- Production: ~120–140 kbpd (2024)

- Cash flow: ~NOK 12–18 bn (2024, net)

- Capex: relatively low maintenance spend

- Funds redeployed: NOK 30+ bn to exploration/development (2024)

Skarv Area Gas Production

The Skarv area is a cash cow for Aker BP, delivering ~1.2–1.5 bcm of gas/year (2024) and using existing 370 km pipeline export links to Nyhamna and Kollsnes, driving high-margin sales in Europe with low incremental capex.

Skarv’s steady EBITDA contribution—roughly NOK 6–8 billion annual run-rate in 2024—supports Aker BP’s dividend (NOK 20.00/share 2024 payout policy) with limited reinvestment need.

It underpins portfolio stability amid mature demand, freeing cash for new growth while preserving shareholder returns.

- 2024 gas output ~1.2–1.5 bcm

- Estimated EBITDA NOK 6–8 bn/year

- Existing export pipelines, low capex

- Supports NOK 20.00/share 2024 dividend

Aker BP’s five cash cows: >$5.5–6.5bn FCF in 2024 funding NOK 12.5bn dividends

Aker BP’s cash cows (Johan Sverdrup, Alvheim, Edvard Grieg, Ivar Aasen, Skarv) delivered ~700–820 kbpd combined oil and ~1.2–1.5 bcm gas in 2024, generating >USD 5.5–6.5bn free cash flow, funding NOK 12.5bn dividends (2024) and NOK 30+bn redeployed to exploration/development.

| Asset | 2024 prod | FCF 2024 |

|---|---|---|

| Johan Sverdrup | 470 kbpd | USD >3bn |

| Alvheim | 60–70 kbpd | USD 1.1–1.3bn |

| Edvard Grieg | 50–70 kbpd | NOK 6–8bn |

| Ivar Aasen | 120–140 kbpd | NOK 12–18bn |

| Skarv | 1.2–1.5 bcm gas | NOK 6–8bn |

Preview = Final Product

Aker BP BCG Matrix

The file you're previewing is the exact Aker BP BCG Matrix report you'll receive after purchase — no watermarks, no sample labels, just the fully formatted, presentation-ready analysis aligned to current market data and strategic frameworks.