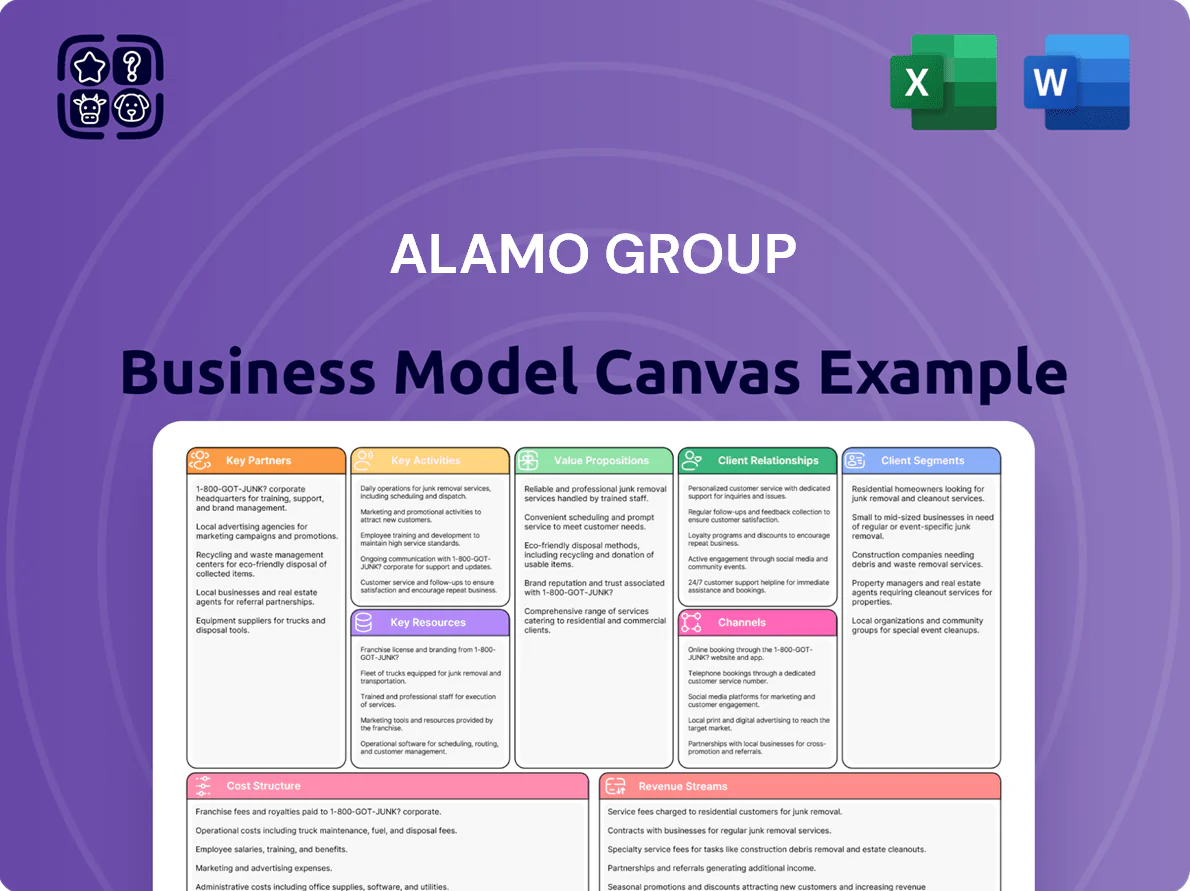

Alamo Group Business Model Canvas

Alamo Group Business Model Canvas: Strategic Blueprint for Investors & Leaders

Unlock the full strategic blueprint behind Alamo Group's business model—this in-depth Business Model Canvas reveals how the company creates value, captures market share, and sustains competitive advantage across segments.

Perfect for investors, consultants, and entrepreneurs, the complete canvas delivers section-by-section insights—from value propositions to revenue streams—ready for benchmarking and strategic planning.

Purchase the full, editable Word and Excel files to accelerate analysis, inform decisions, and adapt proven strategies to your organization.

Partnerships

Independent Dealer Network

Alamo Group depends on a global independent dealer network for localized sales and service, keeping customer proximity and specialized equipment availability across 100+ countries; dealers accounted for roughly 78% of field sales in 2025. By end-2025 Alamo pushed incentives to stock high-margin aftermarket parts, raising parts revenue share by ~4 percentage points and cutting average service lead time from 12 to 7 days. This model scales presence without large retail CapEx.

Tier 1 Component Suppliers

Alamo Group partners with Tier 1 manufacturers for engines, hydraulics, and electronic controllers, keeping supplier lead times under 12 weeks on average and 98% first-pass reliability in assemblies.

By late 2025 Alamo shifted to multi-year sourcing contracts covering ~60% of steel and 45% of advanced electronics spend to curb price swings, letting the company embed new tech while concentrating on final assembly.

Governmental and Municipal Procurement Bodies

Technology and IoT Integration Partners

Alamo partners with telematics firms and software developers to embed GPS tracking, remote diagnostics, and fleet-management software across its mowers and sweepers, delivering real-time uptime gains; pilot integrations cut downtime by up to 18% in 2024 field trials.

These tech partnerships feed a digital ecosystem that yields actionable KPIs for operators and positions Alamo for autonomous and semi-autonomous maintenance rollouts targeted by end-2025.

- 2024 pilot: −18% downtime

- GPS + telematics on 12 product lines (2024)

- Target: semi-autonomy by Q4 2025

Strategic Acquisition Targets

Alamo Group keeps an active M&A pipeline, targeting smaller, specialized manufacturers to expand products and geography; inorganic deals drove ~12% of 2023–2024 revenue growth and remain a priority through 2025.

These ties often begin as distribution agreements and, once proven, convert into full integrations to access niche tech and speed market entry.

- Priority through 2025: add niche OEMs

- 2023–24 inorganic growth ≈12% of revenue gain

- Typical path: distribution → acquisition

- Targets: specialty mowers, hydraulic systems, proprietary controls

Alamo: Global dealer reach, telematics cuts downtime, M&A fuels double‑digit growth

Alamo relies on 100+ country dealers (≈78% field sales in 2025), Tier‑1 suppliers (≤12 week lead, 98% first‑pass), multi‑year contracts covering ~60% steel/45% electronics, public‑sector sales ≈30% (2024) with 25% e/low‑emission sales target, telematics on 12 lines (−18% downtime pilot 2024), and M&A driving ~12% 2023–24 growth.

| Metric | Value |

|---|---|

| Dealer reach | 100+ countries |

| Dealer field sales (2025) | ≈78% |

| Public‑sector revenue (2024) | ≈30% |

| Parts revenue lift (2025) | +4 pp |

| Telematics lines (2024) | 12 |

| Downtime cut (pilot 2024) | −18% |

| M&A revenue contribution (2023–24) | ≈12% |

| Contracted spend—steel | ~60% |

| Contracted spend—electronics | ~45% |

What is included in the product

A concise, ready-made Business Model Canvas for Alamo Group detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams, aligned with real-world operations and strategic priorities.

Condenses Alamo Group’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparisons, team collaboration, and fast executive summaries for boardrooms or internal workshops.

Activities

Precision Manufacturing and Assembly

Alamo Group's core activity is precision fabrication and assembly of heavy machinery across 12 global plants, using advanced welding, CNC, and QA systems so equipment meets harsh agricultural and industrial specs. By end-2025 they added automated assembly lines that raised throughput ~18% and cut defect rates to 0.9%, reinforcing brand differentiation and supporting 2025 revenue of $1.28B.

Research and Development for Innovation

Alamo Group invests continuously in R&D to develop products meeting tightening emissions rules and customer needs; in 2025 it allocates roughly 4–6% of revenue (about $8–12M) toward electrification of mowers and sweepers to capture rising demand for sustainable infrastructure tools.

R&D also upgrades ergonomics and safety on mechanical equipment—reducing operator injury risk and warranty costs—helping Alamo stay ahead of tech shifts and retain niche-market leadership.

Strategic Supply Chain Management

Managing a global supplier network keeps production on schedule while cutting inventory costs; Alamo Group coordinated 120+ suppliers across 15 countries in 2025 to hold working capital at 12.3% of revenue. The company optimized logistics between international hubs and final assembly, cutting lead times 18% and freight costs 7% year-over-year. By late 2025 Alamo rolled out digital tracking across 90% of shipments to spot disruptions and protect margins.

Marketing and Brand Management

Alamo Group manages dozens of distinct brands—each with its own market identity and loyal base—by coordinating marketing to prevent internal cannibalization while maximizing coverage; in 2024 the company reported ~60% of revenue from specialty brands across agriculture and infrastructure segments.

Marketing targets specific channels (ag trade shows for farmers, infrastructure conferences for city planners) so each brand’s value proposition reaches the right decision-makers, driving a higher average order value and repeat rate.

- ~60% revenue from specialty brands (2024)

- Segmented campaigns: trade shows, conferences, dealer programs

- Focus: prevent cannibalization, increase AOV and retention

Aftermarket Support and Training

Aftermarket support keeps Alamo Group equipment running across a 10+ year service life via parts distribution, dealer mechanic training, and onsite fleet support; uptime drives repeat sales and loyalty.

By end-2025 Alamo expanded digital training modules, supporting ~18,000 dealer hours annually and reducing service lead time by ~22%, boosting parts attach rate and aftersales revenue.

- 10+ year service life

- 18,000 dealer training hours (2025)

- 22% lower service lead time

- Higher parts attach rate → recurring revenue

Alamo Group boosts throughput 18%, cuts defects to 0.9% as 2025 revenue hits $1.28B

Alamo Group runs 12 global plants for precision fabrication, added automated lines in 2025 raising throughput ~18% and cutting defects to 0.9%; 2025 revenue $1.28B. R&D spends 4–6% of revenue (~$8–12M) on electrification; aftermarket 10+ year support with 18,000 dealer training hours (2025) and 22% lower service lead time.

| Metric | 2024/2025 |

|---|---|

| Revenue | $1.28B (2025) |

| Plants | 12 |

| Throughput gain | +18% (2025) |

| Defect rate | 0.9% (2025) |

| R&D spend | 4–6% rev (~$8–12M) |

| Dealer training | 18,000 hours (2025) |

| Working capital | 12.3% of rev (2025) |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Alamo Group Business Model Canvas—not a mockup—and it’s the same file you’ll receive after purchase.

When you complete your order, you’ll get full access to this exact, professionally formatted document ready for editing and presenting in Word and Excel.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Alamo Group Business Model Canvas: Strategic Blueprint for Investors & Leaders

Unlock the full strategic blueprint behind Alamo Group's business model—this in-depth Business Model Canvas reveals how the company creates value, captures market share, and sustains competitive advantage across segments.

Perfect for investors, consultants, and entrepreneurs, the complete canvas delivers section-by-section insights—from value propositions to revenue streams—ready for benchmarking and strategic planning.

Purchase the full, editable Word and Excel files to accelerate analysis, inform decisions, and adapt proven strategies to your organization.

Partnerships

Independent Dealer Network

Alamo Group depends on a global independent dealer network for localized sales and service, keeping customer proximity and specialized equipment availability across 100+ countries; dealers accounted for roughly 78% of field sales in 2025. By end-2025 Alamo pushed incentives to stock high-margin aftermarket parts, raising parts revenue share by ~4 percentage points and cutting average service lead time from 12 to 7 days. This model scales presence without large retail CapEx.

Tier 1 Component Suppliers

Alamo Group partners with Tier 1 manufacturers for engines, hydraulics, and electronic controllers, keeping supplier lead times under 12 weeks on average and 98% first-pass reliability in assemblies.

By late 2025 Alamo shifted to multi-year sourcing contracts covering ~60% of steel and 45% of advanced electronics spend to curb price swings, letting the company embed new tech while concentrating on final assembly.

Governmental and Municipal Procurement Bodies

Technology and IoT Integration Partners

Alamo partners with telematics firms and software developers to embed GPS tracking, remote diagnostics, and fleet-management software across its mowers and sweepers, delivering real-time uptime gains; pilot integrations cut downtime by up to 18% in 2024 field trials.

These tech partnerships feed a digital ecosystem that yields actionable KPIs for operators and positions Alamo for autonomous and semi-autonomous maintenance rollouts targeted by end-2025.

- 2024 pilot: −18% downtime

- GPS + telematics on 12 product lines (2024)

- Target: semi-autonomy by Q4 2025

Strategic Acquisition Targets

Alamo Group keeps an active M&A pipeline, targeting smaller, specialized manufacturers to expand products and geography; inorganic deals drove ~12% of 2023–2024 revenue growth and remain a priority through 2025.

These ties often begin as distribution agreements and, once proven, convert into full integrations to access niche tech and speed market entry.

- Priority through 2025: add niche OEMs

- 2023–24 inorganic growth ≈12% of revenue gain

- Typical path: distribution → acquisition

- Targets: specialty mowers, hydraulic systems, proprietary controls

Alamo: Global dealer reach, telematics cuts downtime, M&A fuels double‑digit growth

Alamo relies on 100+ country dealers (≈78% field sales in 2025), Tier‑1 suppliers (≤12 week lead, 98% first‑pass), multi‑year contracts covering ~60% steel/45% electronics, public‑sector sales ≈30% (2024) with 25% e/low‑emission sales target, telematics on 12 lines (−18% downtime pilot 2024), and M&A driving ~12% 2023–24 growth.

| Metric | Value |

|---|---|

| Dealer reach | 100+ countries |

| Dealer field sales (2025) | ≈78% |

| Public‑sector revenue (2024) | ≈30% |

| Parts revenue lift (2025) | +4 pp |

| Telematics lines (2024) | 12 |

| Downtime cut (pilot 2024) | −18% |

| M&A revenue contribution (2023–24) | ≈12% |

| Contracted spend—steel | ~60% |

| Contracted spend—electronics | ~45% |

What is included in the product

A concise, ready-made Business Model Canvas for Alamo Group detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams, aligned with real-world operations and strategic priorities.

Condenses Alamo Group’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparisons, team collaboration, and fast executive summaries for boardrooms or internal workshops.

Activities

Precision Manufacturing and Assembly

Alamo Group's core activity is precision fabrication and assembly of heavy machinery across 12 global plants, using advanced welding, CNC, and QA systems so equipment meets harsh agricultural and industrial specs. By end-2025 they added automated assembly lines that raised throughput ~18% and cut defect rates to 0.9%, reinforcing brand differentiation and supporting 2025 revenue of $1.28B.

Research and Development for Innovation

Alamo Group invests continuously in R&D to develop products meeting tightening emissions rules and customer needs; in 2025 it allocates roughly 4–6% of revenue (about $8–12M) toward electrification of mowers and sweepers to capture rising demand for sustainable infrastructure tools.

R&D also upgrades ergonomics and safety on mechanical equipment—reducing operator injury risk and warranty costs—helping Alamo stay ahead of tech shifts and retain niche-market leadership.

Strategic Supply Chain Management

Managing a global supplier network keeps production on schedule while cutting inventory costs; Alamo Group coordinated 120+ suppliers across 15 countries in 2025 to hold working capital at 12.3% of revenue. The company optimized logistics between international hubs and final assembly, cutting lead times 18% and freight costs 7% year-over-year. By late 2025 Alamo rolled out digital tracking across 90% of shipments to spot disruptions and protect margins.

Marketing and Brand Management

Alamo Group manages dozens of distinct brands—each with its own market identity and loyal base—by coordinating marketing to prevent internal cannibalization while maximizing coverage; in 2024 the company reported ~60% of revenue from specialty brands across agriculture and infrastructure segments.

Marketing targets specific channels (ag trade shows for farmers, infrastructure conferences for city planners) so each brand’s value proposition reaches the right decision-makers, driving a higher average order value and repeat rate.

- ~60% revenue from specialty brands (2024)

- Segmented campaigns: trade shows, conferences, dealer programs

- Focus: prevent cannibalization, increase AOV and retention

Aftermarket Support and Training

Aftermarket support keeps Alamo Group equipment running across a 10+ year service life via parts distribution, dealer mechanic training, and onsite fleet support; uptime drives repeat sales and loyalty.

By end-2025 Alamo expanded digital training modules, supporting ~18,000 dealer hours annually and reducing service lead time by ~22%, boosting parts attach rate and aftersales revenue.

- 10+ year service life

- 18,000 dealer training hours (2025)

- 22% lower service lead time

- Higher parts attach rate → recurring revenue

Alamo Group boosts throughput 18%, cuts defects to 0.9% as 2025 revenue hits $1.28B

Alamo Group runs 12 global plants for precision fabrication, added automated lines in 2025 raising throughput ~18% and cutting defects to 0.9%; 2025 revenue $1.28B. R&D spends 4–6% of revenue (~$8–12M) on electrification; aftermarket 10+ year support with 18,000 dealer training hours (2025) and 22% lower service lead time.

| Metric | 2024/2025 |

|---|---|

| Revenue | $1.28B (2025) |

| Plants | 12 |

| Throughput gain | +18% (2025) |

| Defect rate | 0.9% (2025) |

| R&D spend | 4–6% rev (~$8–12M) |

| Dealer training | 18,000 hours (2025) |

| Working capital | 12.3% of rev (2025) |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the actual Alamo Group Business Model Canvas—not a mockup—and it’s the same file you’ll receive after purchase.

When you complete your order, you’ll get full access to this exact, professionally formatted document ready for editing and presenting in Word and Excel.