Alamos Gold Porter's Five Forces Analysis

From Overview to Strategy Blueprint

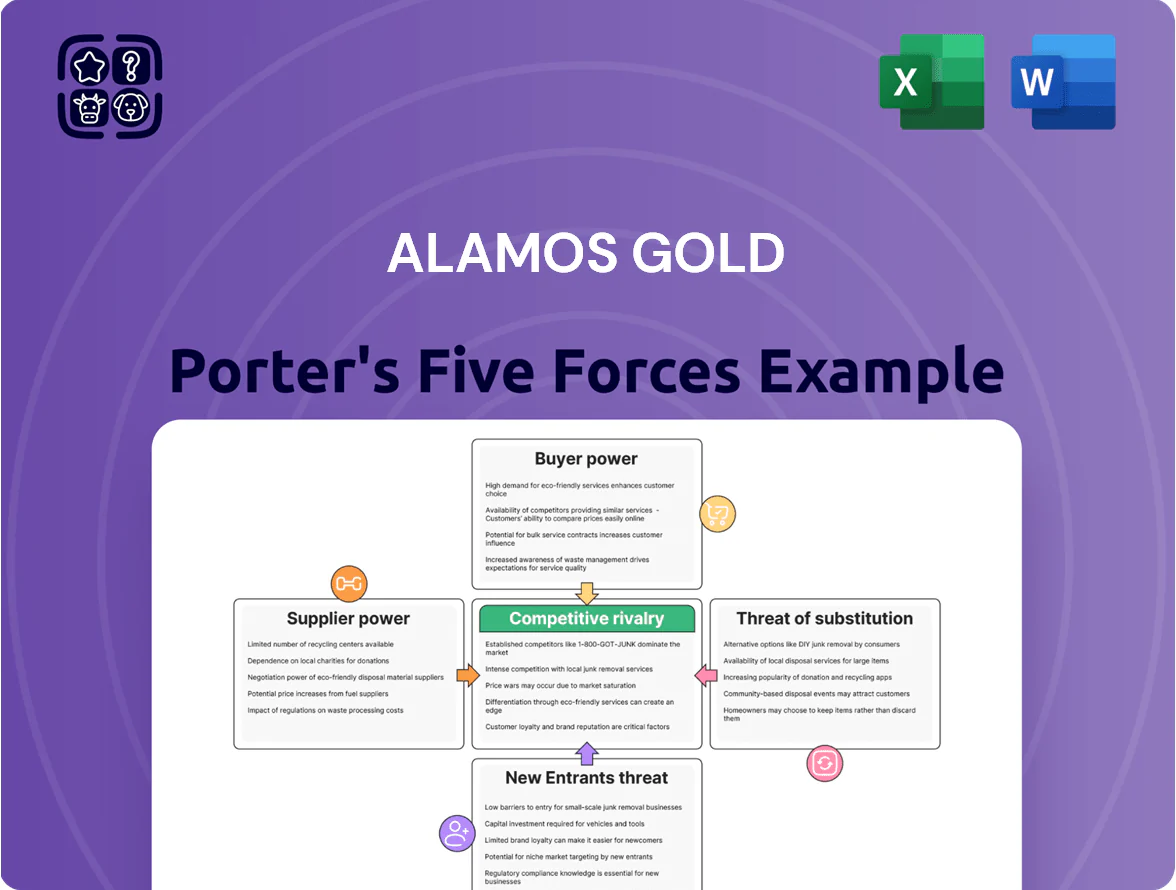

Alamos Gold faces moderate buyer power and manageable supplier influence, while its scale, low-cost assets, and jurisdictional exposure shape competitive dynamics and barriers to entry in the gold mining sector.

Exploration rivals and commodity price volatility raise rivalry and substitute risks, but Alamos’s cash flow profile and project pipeline offer strategic advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Alamos Gold’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Escalating Skilled Labor Costs

The 2025 mining labor shortage pushed technical wages up ~4% across Alamos Gold’s North American sites, giving skilled underground miners and geologists outsized bargaining power during the Phase 3+ Island Gold expansion. This labor premium raises operating costs and project risk because those roles are critical for complex orebody access and grade control. Alamos has responded with automation investments—robotic drilling, remote mucking—and a $12M+ specialized training push to cut reliance on the volatile labor market. These moves aim to cap long‑run wage exposure and protect project IRR.

Specialized Equipment and Maintenance Dependence

Alamos Gold depends on a few global OEMs for high-capacity fleets and specialized mill parts; SAG mill liners needed early replacement in late 2025, costing ~US$8–12m and highlighting supplier influence.

Suppliers have moderate power due to long lead times (6–18 months) and technical specificity, making brand switches cost-prohibitive.

The company offsets risk with strategic spare-part stocks (≈US$25m inventory) and multi-year service agreements to keep operations running.

Energy and Fuel Market Vulnerability

Alamos still faces energy exposure: Canadian sites are shifting to grid power, but open-pit fleets and Mexican mines depend on diesel and natural gas, tying costs to global markets.

Fuel suppliers are highly concentrated, so Alamos has little pricing leverage and must pay near-market rates; energy swings feed directly into all-in sustaining costs.

Energy-driven volatility helped push AISC above 1,500 USD/oz by end-2025, amplifying unit-cost risk.

Chemical Reagents and Consumables

Suppliers of cyanide, grinding media and specialty reagents hold strong leverage over Alamos Gold because a handful of industrial chemical firms dominate global supply; a single-week disruption can cut throughput and revenue immediately.

Alamos reduces this risk via multi-sourcing across North America and Mexico, 12–18 month bulk contracts locked at fixed prices, and on-site inventory covering ~60 days of reagent use as of YE 2025.

- Few global suppliers → high supplier power

- Supply disruption → immediate production loss

- Mitigation: diversification, 12–18 month contracts

- Mitigation: ~60 days on-site reagent stock (YE 2025)

Infrastructure and Construction Contractors

The Phase 3+ shaft expansion needs a few specialist engineering and construction firms skilled in deep-shaft work in cold northern climates; their rarity gives them strong bargaining power and raises risk of cost escalation.

Alamos must tightly manage contracts, use milestone-linked payments, and hold contingency (Alamos set a $75–100M contingency for recent projects) to avoid capital overruns and hit the 2026 completion target.

- Few qualified contractors → high supplier power

- Specialized safety record required → limited competition

- Contingency needed: $75–100M range

- Contract structure: milestones + penalties to protect schedule

Alamos shields Phase‑3 IRR as supplier pressure lifts AISC >$1,500/oz

Suppliers exert moderate–high power: skilled labor, OEMs, energy and reagents are concentrated, raising costs and disruption risk (AISC >1,500 USD/oz YE‑2025). Alamos mitigates via automation, $12M training, $25M spare parts, ~60 days reagent stock, 12–18 month fixed contracts and $75–100M project contingency to protect Phase 3+ timelines and IRR.

| Item | 2025 metric |

|---|---|

| Labor wage uplift | ~4% |

| Spare parts stock | ~US$25M |

| Reagent cover | ~60 days |

| Contingency | US$75–100M |

| AISC | >US$1,500/oz |

What is included in the product

Tailored exclusively for Alamos Gold, this Porter's Five Forces overview uncovers competitive drivers, supplier/buyer leverage, entry barriers, substitutes, and disruptive threats shaping the company’s pricing power and profitability.

Compact Porter's Five Forces snapshot for Alamos Gold—quickly spot competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Global Price-Taker Status

As a producer of a standardized commodity, Alamos Gold is a pure price-taker with no ability to influence the global spot price of gold, which is set by the London Bullion Market Association and major exchanges.

Revenue is fully tied to market rates; in 2025 realized gold prices peaked near $4,000/oz, but Alamos remained a passive participant in the pricing mechanism.

High Liquidity of Gold Markets

The global gold market’s deep liquidity lets Alamos Gold sell its 2024 production (~460 koz consolidated) quickly to bullion banks or refineries at spot prices, so no single buyer can force discounts or special terms. This near-infinite demand at market price cuts bargaining power of customers and supports realized revenue close to LBMA spot levels (gold averaged $1,995/oz in 2024). Instant convertibility reduces inventory risk and removes need for a large sales and marketing function.

Standardized Refining and Smelting Services

Alamos Gold delivers dore bars to accredited refineries meeting LBMA and RJC standards for purity and ethical sourcing; in 2024 the company sent ~400,000 oz of gold for refining, so quality compliance is non-negotiable. Refineries face competition—global refinery capacity exceeded 4,000 t/year in 2023—giving Alamos alternative outlets if terms worsen. That competition keeps average tolling fees stable near historical levels (~0.25–0.50% of metal value), limiting margin erosion.

Institutional Investor Influence

Institutional investors, though not buyers of physical gold, are Alamos Gold’s main customers for equity and push management on ESG and capital discipline; they forced a 60% dividend hike announced in Jan 2026 as proof of returns focus.

Their capacity to reallocate large positions — Alamos’ free float includes ~65% institutional holdings and a 12-month average daily traded value of CAD 18m (2025) — directly constrains strategy and spending.

- 60% dividend increase — Jan 2026

- ~65% institutional ownership — 2025

- CAD 18m average daily traded value — 2025

Central Bank Demand Dynamics

Central banks (major gold holders) added 1,136 tonnes of net gold reserves from 2018–2024, and continued accumulation into 2025 has set a demand floor that supports industry pricing and Alamos Gold’s project economics.

Alamos doesn’t sell to central banks, but their collective buying shapes long-term prices, reducing downside risk for Alamos’ expansion capex and reserve valuation.

- 2018–2024 central bank net purchases: 1,136 tonnes

- EM central bank shift: rising share of purchases to ~60% by 2024

- Effect: lower tail-risk for gold price shocks

Alamos: Price-taker in deep gold market—460koz at $1,995, institutional-led governance

Customers have minimal bargaining power: Alamos is a price-taker in a deep, liquid gold market (LBMA spot), selling ~460 koz in 2024 at average $1,995/oz; refinery capacity >4,000 t/yr keeps tolls ~0.25–0.50% and offers alternative outlets. Institutional shareholders (~65% ownership, CAD 18m ADV in 2025) exert governance pressure (60% dividend hike Jan 2026), while central bank net purchases 2018–2024 totaled 1,136 t, supporting a demand floor.

| Metric | Value |

|---|---|

| 2024 production (consol.) | ~460 koz |

| 2024 gold avg price | $1,995/oz |

| Refinery capacity | >4,000 t/yr |

| Tolling fees | ~0.25–0.50% value |

| Institutional ownership (2025) | ~65% |

| ADV (12m, 2025) | CAD 18m |

| Central bank net buys (2018–24) | 1,136 t |

Preview the Actual Deliverable

Alamos Gold Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Alamos Gold you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is the complete, professionally formatted file ready for download and use the moment you buy.

You're viewing the final version; upon payment you'll get instant access to this identical, ready-to-use analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Alamos Gold faces moderate buyer power and manageable supplier influence, while its scale, low-cost assets, and jurisdictional exposure shape competitive dynamics and barriers to entry in the gold mining sector.

Exploration rivals and commodity price volatility raise rivalry and substitute risks, but Alamos’s cash flow profile and project pipeline offer strategic advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Alamos Gold’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Escalating Skilled Labor Costs

The 2025 mining labor shortage pushed technical wages up ~4% across Alamos Gold’s North American sites, giving skilled underground miners and geologists outsized bargaining power during the Phase 3+ Island Gold expansion. This labor premium raises operating costs and project risk because those roles are critical for complex orebody access and grade control. Alamos has responded with automation investments—robotic drilling, remote mucking—and a $12M+ specialized training push to cut reliance on the volatile labor market. These moves aim to cap long‑run wage exposure and protect project IRR.

Specialized Equipment and Maintenance Dependence

Alamos Gold depends on a few global OEMs for high-capacity fleets and specialized mill parts; SAG mill liners needed early replacement in late 2025, costing ~US$8–12m and highlighting supplier influence.

Suppliers have moderate power due to long lead times (6–18 months) and technical specificity, making brand switches cost-prohibitive.

The company offsets risk with strategic spare-part stocks (≈US$25m inventory) and multi-year service agreements to keep operations running.

Energy and Fuel Market Vulnerability

Alamos still faces energy exposure: Canadian sites are shifting to grid power, but open-pit fleets and Mexican mines depend on diesel and natural gas, tying costs to global markets.

Fuel suppliers are highly concentrated, so Alamos has little pricing leverage and must pay near-market rates; energy swings feed directly into all-in sustaining costs.

Energy-driven volatility helped push AISC above 1,500 USD/oz by end-2025, amplifying unit-cost risk.

Chemical Reagents and Consumables

Suppliers of cyanide, grinding media and specialty reagents hold strong leverage over Alamos Gold because a handful of industrial chemical firms dominate global supply; a single-week disruption can cut throughput and revenue immediately.

Alamos reduces this risk via multi-sourcing across North America and Mexico, 12–18 month bulk contracts locked at fixed prices, and on-site inventory covering ~60 days of reagent use as of YE 2025.

- Few global suppliers → high supplier power

- Supply disruption → immediate production loss

- Mitigation: diversification, 12–18 month contracts

- Mitigation: ~60 days on-site reagent stock (YE 2025)

Infrastructure and Construction Contractors

The Phase 3+ shaft expansion needs a few specialist engineering and construction firms skilled in deep-shaft work in cold northern climates; their rarity gives them strong bargaining power and raises risk of cost escalation.

Alamos must tightly manage contracts, use milestone-linked payments, and hold contingency (Alamos set a $75–100M contingency for recent projects) to avoid capital overruns and hit the 2026 completion target.

- Few qualified contractors → high supplier power

- Specialized safety record required → limited competition

- Contingency needed: $75–100M range

- Contract structure: milestones + penalties to protect schedule

Alamos shields Phase‑3 IRR as supplier pressure lifts AISC >$1,500/oz

Suppliers exert moderate–high power: skilled labor, OEMs, energy and reagents are concentrated, raising costs and disruption risk (AISC >1,500 USD/oz YE‑2025). Alamos mitigates via automation, $12M training, $25M spare parts, ~60 days reagent stock, 12–18 month fixed contracts and $75–100M project contingency to protect Phase 3+ timelines and IRR.

| Item | 2025 metric |

|---|---|

| Labor wage uplift | ~4% |

| Spare parts stock | ~US$25M |

| Reagent cover | ~60 days |

| Contingency | US$75–100M |

| AISC | >US$1,500/oz |

What is included in the product

Tailored exclusively for Alamos Gold, this Porter's Five Forces overview uncovers competitive drivers, supplier/buyer leverage, entry barriers, substitutes, and disruptive threats shaping the company’s pricing power and profitability.

Compact Porter's Five Forces snapshot for Alamos Gold—quickly spot competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Global Price-Taker Status

As a producer of a standardized commodity, Alamos Gold is a pure price-taker with no ability to influence the global spot price of gold, which is set by the London Bullion Market Association and major exchanges.

Revenue is fully tied to market rates; in 2025 realized gold prices peaked near $4,000/oz, but Alamos remained a passive participant in the pricing mechanism.

High Liquidity of Gold Markets

The global gold market’s deep liquidity lets Alamos Gold sell its 2024 production (~460 koz consolidated) quickly to bullion banks or refineries at spot prices, so no single buyer can force discounts or special terms. This near-infinite demand at market price cuts bargaining power of customers and supports realized revenue close to LBMA spot levels (gold averaged $1,995/oz in 2024). Instant convertibility reduces inventory risk and removes need for a large sales and marketing function.

Standardized Refining and Smelting Services

Alamos Gold delivers dore bars to accredited refineries meeting LBMA and RJC standards for purity and ethical sourcing; in 2024 the company sent ~400,000 oz of gold for refining, so quality compliance is non-negotiable. Refineries face competition—global refinery capacity exceeded 4,000 t/year in 2023—giving Alamos alternative outlets if terms worsen. That competition keeps average tolling fees stable near historical levels (~0.25–0.50% of metal value), limiting margin erosion.

Institutional Investor Influence

Institutional investors, though not buyers of physical gold, are Alamos Gold’s main customers for equity and push management on ESG and capital discipline; they forced a 60% dividend hike announced in Jan 2026 as proof of returns focus.

Their capacity to reallocate large positions — Alamos’ free float includes ~65% institutional holdings and a 12-month average daily traded value of CAD 18m (2025) — directly constrains strategy and spending.

- 60% dividend increase — Jan 2026

- ~65% institutional ownership — 2025

- CAD 18m average daily traded value — 2025

Central Bank Demand Dynamics

Central banks (major gold holders) added 1,136 tonnes of net gold reserves from 2018–2024, and continued accumulation into 2025 has set a demand floor that supports industry pricing and Alamos Gold’s project economics.

Alamos doesn’t sell to central banks, but their collective buying shapes long-term prices, reducing downside risk for Alamos’ expansion capex and reserve valuation.

- 2018–2024 central bank net purchases: 1,136 tonnes

- EM central bank shift: rising share of purchases to ~60% by 2024

- Effect: lower tail-risk for gold price shocks

Alamos: Price-taker in deep gold market—460koz at $1,995, institutional-led governance

Customers have minimal bargaining power: Alamos is a price-taker in a deep, liquid gold market (LBMA spot), selling ~460 koz in 2024 at average $1,995/oz; refinery capacity >4,000 t/yr keeps tolls ~0.25–0.50% and offers alternative outlets. Institutional shareholders (~65% ownership, CAD 18m ADV in 2025) exert governance pressure (60% dividend hike Jan 2026), while central bank net purchases 2018–2024 totaled 1,136 t, supporting a demand floor.

| Metric | Value |

|---|---|

| 2024 production (consol.) | ~460 koz |

| 2024 gold avg price | $1,995/oz |

| Refinery capacity | >4,000 t/yr |

| Tolling fees | ~0.25–0.50% value |

| Institutional ownership (2025) | ~65% |

| ADV (12m, 2025) | CAD 18m |

| Central bank net buys (2018–24) | 1,136 t |

Preview the Actual Deliverable

Alamos Gold Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Alamos Gold you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is the complete, professionally formatted file ready for download and use the moment you buy.

You're viewing the final version; upon payment you'll get instant access to this identical, ready-to-use analysis.