Albemarle Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

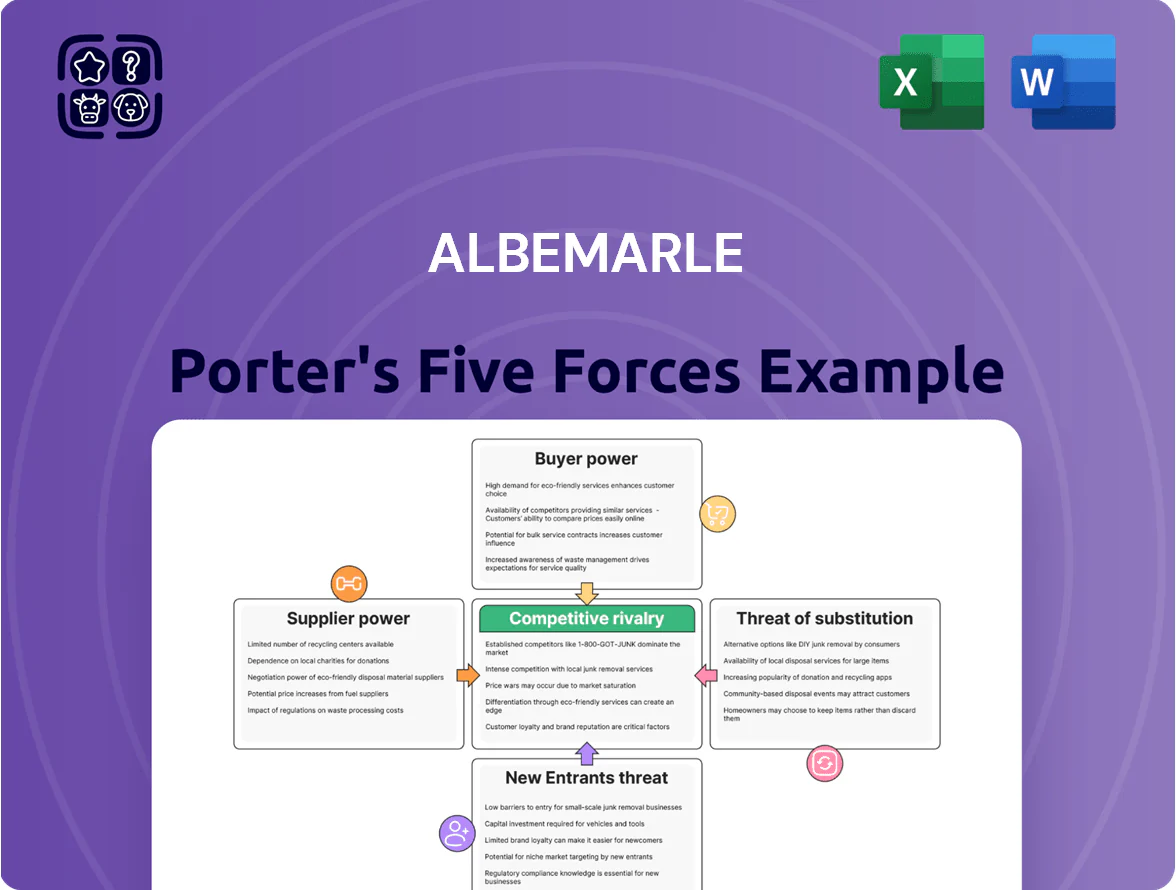

Albemarle faces strong supplier influence from concentrated lithium and specialty chemical inputs, intense rivalry among global battery-materials producers, and moderate buyer power driven by large OEMs—while threats from new entrants and substitutes remain emerging risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Albemarle’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical integration of resource ownership

Albemarle’s ownership stakes in Salar de Atacama and multiple hard-rock mines give it direct control of ~20–25% of global lithium supply (2024 estimate), cutting dependence on external miners and lowering supplier bargaining power.

By internalizing lithium and bromine feedstock, Albemarle stabilizes its cost base—2024 gross margin benefit estimated at +3–5 percentage points versus non-integrated peers—reducing exposure to spot-price spikes.

This vertical integration minimizes disruption risk: company-reported operated production met ~90% of its 2024 lithium needs, so third-party supplier leverage is limited and long-term contract flexibility improves.

Energy and utility dependency

Albemarle’s lithium and bromine production is highly energy-intensive, leaving the company reliant on local electricity and natural gas providers across its global sites, which limits switching options for specific plants. By end-2025 rising energy transition costs and carbon pricing—estimated to add roughly $30–50 per tonne of lithium carbonate equivalent (LCE) in some regions—have boosted supplier influence on margins. Hedging covers fuel price exposure but not grid constraints or regional carbon levies, so energy suppliers retain moderate bargaining leverage.

Specialized chemical and equipment vendors

Albemarle depends on a small set of suppliers for specialized reagents and proprietary equipment to meet battery-grade lithium purity, giving suppliers moderate bargaining power; roughly 60–70% of such niche suppliers are concentrated among a few firms globally.

Long-term contracts and co-development deals—Albemarle reported 5+ active tech partnerships in 2024—limit abrupt price hikes and align supplier incentives with stable supply.

Logistics and global shipping constraints

As a global exporter of hazardous chemicals, Albemarle depends on international carriers and specialized logistics; carrier consolidation raised freight rates by ~30% in 2021–23 and port congestion spiked delays into 2024–25.

Albemarle uses scale to secure long-term charters and optimize routes, cutting logistics cost per tonne by an estimated 8–12% on major lanes in 2024.

Still, few immediate alternatives for bulk hazardous transport keep supplier power materially high, especially during geopolitical or port disruptions.

- Carrier consolidation increased bargaining leverage

- Freight rate surge ~30% (2021–23)

- Albemarle negotiated long-term contracts, saved ~8–12%/tonne

- Limited alternative providers sustain supplier power

Labor market and technical talent

The specialty chemicals sector shows tightening supply of skilled chemical engineers, geologists, and researchers crucial to Albemarle’s innovation; industry hiring for chemical engineers rose ~8% y/y in 2024, boosting pay premiums and supplier bargaining power.

Energy firms shifting to lithium and battery materials increased competition for talent, raising attrition in 2023–24; Albemarle counters with automation and ~$120m in FY2024 training and R&D workforce investments.

By late 2025, attracting and retaining top technical staff remains a key supply risk for maintaining plant uptime and innovation velocity.

- Talent scarcity up ~8% (2024) raises wage pressure

- Energy-to-lithium shift increases competition

- Albemarle spent ~$120m (FY2024) on training/R&D workforce

- Automation reduces but does not eliminate labor risk by 2025

Albemarle’s vertical edge: 90% self-supply, 20–25% global share boosts margins

Albemarle’s vertical integration supplies ~20–25% of global lithium (2024), meeting ~90% of its lithium needs from owned operations and cutting external supplier leverage; long-term contracts and 5+ tech partnerships in 2024 further reduce abrupt price risk. Energy and hazardous-logistics suppliers retain moderate power—energy/carbon costs may add $30–50/tonne LCE and freight rose ~30% (2021–23)—while niche reagent suppliers and talent shortages (chemical-engineer hiring +8% y/y in 2024) keep pockets of supplier influence.

| Metric | Value |

|---|---|

| Owned share of global lithium supply (2024) | 20–25% |

| Self-sourced lithium needs (2024) | ~90% |

| Gross margin benefit vs peers (2024) | +3–5 ppt |

| Energy/carbon cost add | $30–50/tonne LCE |

| Freight increase (2021–23) | ~30% |

| Chemical-engineer hiring (2024) | +8% y/y |

| FY2024 training & R&D spend | $120m |

What is included in the product

Tailored exclusively for Albemarle, this Porter's Five Forces analysis uncovers competitive pressures, supplier and buyer power, substitute threats, and entry barriers, highlighting strategic risks and opportunities that shape its pricing, margins, and market position.

A concise Porter's Five Forces snapshot for Albemarle—clarifies competitive pressures and helps prioritize strategic moves quickly.

Customers Bargaining Power

Concentration of major EV manufacturers

The lithium customer base is concentrated: by 2025 the top 10 EV and battery makers accounted for roughly 65% of global lithium demand, giving Tier 1 buyers strong negotiating leverage.

These large customers push for lower prices and tight specs; Albemarle faces margin pressure and must offer competitive contracts to keep volumes.

In 2025 buyers adopted advanced procurement tactics—long-term offtakes, index-based pricing—forcing Albemarle to boost efficiency and consistency to stay preferred.

Influence of long term supply contracts

A significant share of Albemarle’s revenue comes from multi-year supply contracts with pricing tied to indices or fixed formulas, giving the company ~60–70% volume certainty but capping short-term margin upside; some contracts audited in 2024 showed index links to lithium carbonate prices. By end-2025 many buyers negotiated more flexible clauses—estimated to affect ~15–25% of contracted volumes—to shield against prior extreme price swings, so customers use long-term commitments to extract better economic terms.

Demand for high purity and sustainability standards

Availability of alternative sourcing options

As of 2025, rising output from new lithium projects in Australia, Chile, Argentina, the US, and Africa has given buyers more sourcing choices, boosting their bargaining power versus Albemarle.

Customers now shift volume to emerging producers for price, reliability, and purity, forcing Albemarle to compete on total cost of ownership rather than scarcity.

The supply expansion—global mined and refined lithium capacity up ~40% since 2021—moves leverage toward buyers compared with early-2020s shortages.

- More producers: new projects in Africa, South America, North America

- Capacity +40% since 2021 (global lithium supply, 2025)

- Buyers demand reliability, purity, lifecycle cost

- Albemarle faces pressure on pricing and service

Price sensitivity in bromine and catalyst markets

Customers in Albemarle’s bromine and catalyst segments are highly price-sensitive because many end-uses act like commodities; in 2024 Albemarle’s Specialty Chemicals revenue mix showed ~48% exposure to traditional chemical units, keeping volumes tied to global price benchmarks.

Fire-safety and refining clients treat chemical input costs as key margins—ethylene-oxide and refining catalyst costs can swing plant economics—so buyers push for lower unit prices or long-term indexed contracts.

Albemarle offsets pressure with technical service and superior product performance—R&D spending was about $130m in 2024—but still faces constant pressure to match global benchmark pricing, so customer bargaining power remains high.

- High price sensitivity: commodity-like end-uses

- 2024: ~48% revenue exposure in traditional chemicals

- $130m R&D supports differentiation

- Customers push indexed/long-term pricing

Albemarle squeezed by top OEMs, indexed deals, +40% supply and $300M ESG cost

Large EV/battery OEMs (top 10 ≈65% demand in 2025) and expanded global supply (+40% capacity since 2021) give buyers strong leverage, forcing Albemarle into indexed/multi‑year contracts (~60–70% volume certainty) and ESG investments (~$300m since 2021 raising unit costs ~3–5%) to retain business.

| Metric | Value (2025) |

|---|---|

| Top‑10 OEM share | ≈65% |

| Contracted volume certainty | 60–70% |

| Global capacity change since 2021 | +40% |

| ESG capex since 2021 | $300m |

Preview the Actual Deliverable

Albemarle Porter's Five Forces Analysis

This preview shows the exact Albemarle Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is professionally written and fully formatted, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insights. You’ll get instant access to this same file upon payment, ready for download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Albemarle faces strong supplier influence from concentrated lithium and specialty chemical inputs, intense rivalry among global battery-materials producers, and moderate buyer power driven by large OEMs—while threats from new entrants and substitutes remain emerging risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Albemarle’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical integration of resource ownership

Albemarle’s ownership stakes in Salar de Atacama and multiple hard-rock mines give it direct control of ~20–25% of global lithium supply (2024 estimate), cutting dependence on external miners and lowering supplier bargaining power.

By internalizing lithium and bromine feedstock, Albemarle stabilizes its cost base—2024 gross margin benefit estimated at +3–5 percentage points versus non-integrated peers—reducing exposure to spot-price spikes.

This vertical integration minimizes disruption risk: company-reported operated production met ~90% of its 2024 lithium needs, so third-party supplier leverage is limited and long-term contract flexibility improves.

Energy and utility dependency

Albemarle’s lithium and bromine production is highly energy-intensive, leaving the company reliant on local electricity and natural gas providers across its global sites, which limits switching options for specific plants. By end-2025 rising energy transition costs and carbon pricing—estimated to add roughly $30–50 per tonne of lithium carbonate equivalent (LCE) in some regions—have boosted supplier influence on margins. Hedging covers fuel price exposure but not grid constraints or regional carbon levies, so energy suppliers retain moderate bargaining leverage.

Specialized chemical and equipment vendors

Albemarle depends on a small set of suppliers for specialized reagents and proprietary equipment to meet battery-grade lithium purity, giving suppliers moderate bargaining power; roughly 60–70% of such niche suppliers are concentrated among a few firms globally.

Long-term contracts and co-development deals—Albemarle reported 5+ active tech partnerships in 2024—limit abrupt price hikes and align supplier incentives with stable supply.

Logistics and global shipping constraints

As a global exporter of hazardous chemicals, Albemarle depends on international carriers and specialized logistics; carrier consolidation raised freight rates by ~30% in 2021–23 and port congestion spiked delays into 2024–25.

Albemarle uses scale to secure long-term charters and optimize routes, cutting logistics cost per tonne by an estimated 8–12% on major lanes in 2024.

Still, few immediate alternatives for bulk hazardous transport keep supplier power materially high, especially during geopolitical or port disruptions.

- Carrier consolidation increased bargaining leverage

- Freight rate surge ~30% (2021–23)

- Albemarle negotiated long-term contracts, saved ~8–12%/tonne

- Limited alternative providers sustain supplier power

Labor market and technical talent

The specialty chemicals sector shows tightening supply of skilled chemical engineers, geologists, and researchers crucial to Albemarle’s innovation; industry hiring for chemical engineers rose ~8% y/y in 2024, boosting pay premiums and supplier bargaining power.

Energy firms shifting to lithium and battery materials increased competition for talent, raising attrition in 2023–24; Albemarle counters with automation and ~$120m in FY2024 training and R&D workforce investments.

By late 2025, attracting and retaining top technical staff remains a key supply risk for maintaining plant uptime and innovation velocity.

- Talent scarcity up ~8% (2024) raises wage pressure

- Energy-to-lithium shift increases competition

- Albemarle spent ~$120m (FY2024) on training/R&D workforce

- Automation reduces but does not eliminate labor risk by 2025

Albemarle’s vertical edge: 90% self-supply, 20–25% global share boosts margins

Albemarle’s vertical integration supplies ~20–25% of global lithium (2024), meeting ~90% of its lithium needs from owned operations and cutting external supplier leverage; long-term contracts and 5+ tech partnerships in 2024 further reduce abrupt price risk. Energy and hazardous-logistics suppliers retain moderate power—energy/carbon costs may add $30–50/tonne LCE and freight rose ~30% (2021–23)—while niche reagent suppliers and talent shortages (chemical-engineer hiring +8% y/y in 2024) keep pockets of supplier influence.

| Metric | Value |

|---|---|

| Owned share of global lithium supply (2024) | 20–25% |

| Self-sourced lithium needs (2024) | ~90% |

| Gross margin benefit vs peers (2024) | +3–5 ppt |

| Energy/carbon cost add | $30–50/tonne LCE |

| Freight increase (2021–23) | ~30% |

| Chemical-engineer hiring (2024) | +8% y/y |

| FY2024 training & R&D spend | $120m |

What is included in the product

Tailored exclusively for Albemarle, this Porter's Five Forces analysis uncovers competitive pressures, supplier and buyer power, substitute threats, and entry barriers, highlighting strategic risks and opportunities that shape its pricing, margins, and market position.

A concise Porter's Five Forces snapshot for Albemarle—clarifies competitive pressures and helps prioritize strategic moves quickly.

Customers Bargaining Power

Concentration of major EV manufacturers

The lithium customer base is concentrated: by 2025 the top 10 EV and battery makers accounted for roughly 65% of global lithium demand, giving Tier 1 buyers strong negotiating leverage.

These large customers push for lower prices and tight specs; Albemarle faces margin pressure and must offer competitive contracts to keep volumes.

In 2025 buyers adopted advanced procurement tactics—long-term offtakes, index-based pricing—forcing Albemarle to boost efficiency and consistency to stay preferred.

Influence of long term supply contracts

A significant share of Albemarle’s revenue comes from multi-year supply contracts with pricing tied to indices or fixed formulas, giving the company ~60–70% volume certainty but capping short-term margin upside; some contracts audited in 2024 showed index links to lithium carbonate prices. By end-2025 many buyers negotiated more flexible clauses—estimated to affect ~15–25% of contracted volumes—to shield against prior extreme price swings, so customers use long-term commitments to extract better economic terms.

Demand for high purity and sustainability standards

Availability of alternative sourcing options

As of 2025, rising output from new lithium projects in Australia, Chile, Argentina, the US, and Africa has given buyers more sourcing choices, boosting their bargaining power versus Albemarle.

Customers now shift volume to emerging producers for price, reliability, and purity, forcing Albemarle to compete on total cost of ownership rather than scarcity.

The supply expansion—global mined and refined lithium capacity up ~40% since 2021—moves leverage toward buyers compared with early-2020s shortages.

- More producers: new projects in Africa, South America, North America

- Capacity +40% since 2021 (global lithium supply, 2025)

- Buyers demand reliability, purity, lifecycle cost

- Albemarle faces pressure on pricing and service

Price sensitivity in bromine and catalyst markets

Customers in Albemarle’s bromine and catalyst segments are highly price-sensitive because many end-uses act like commodities; in 2024 Albemarle’s Specialty Chemicals revenue mix showed ~48% exposure to traditional chemical units, keeping volumes tied to global price benchmarks.

Fire-safety and refining clients treat chemical input costs as key margins—ethylene-oxide and refining catalyst costs can swing plant economics—so buyers push for lower unit prices or long-term indexed contracts.

Albemarle offsets pressure with technical service and superior product performance—R&D spending was about $130m in 2024—but still faces constant pressure to match global benchmark pricing, so customer bargaining power remains high.

- High price sensitivity: commodity-like end-uses

- 2024: ~48% revenue exposure in traditional chemicals

- $130m R&D supports differentiation

- Customers push indexed/long-term pricing

Albemarle squeezed by top OEMs, indexed deals, +40% supply and $300M ESG cost

Large EV/battery OEMs (top 10 ≈65% demand in 2025) and expanded global supply (+40% capacity since 2021) give buyers strong leverage, forcing Albemarle into indexed/multi‑year contracts (~60–70% volume certainty) and ESG investments (~$300m since 2021 raising unit costs ~3–5%) to retain business.

| Metric | Value (2025) |

|---|---|

| Top‑10 OEM share | ≈65% |

| Contracted volume certainty | 60–70% |

| Global capacity change since 2021 | +40% |

| ESG capex since 2021 | $300m |

Preview the Actual Deliverable

Albemarle Porter's Five Forces Analysis

This preview shows the exact Albemarle Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document is professionally written and fully formatted, covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry with actionable insights. You’ll get instant access to this same file upon payment, ready for download and use.