Albertsons Porter's Five Forces Analysis

Don't Miss the Bigger Picture

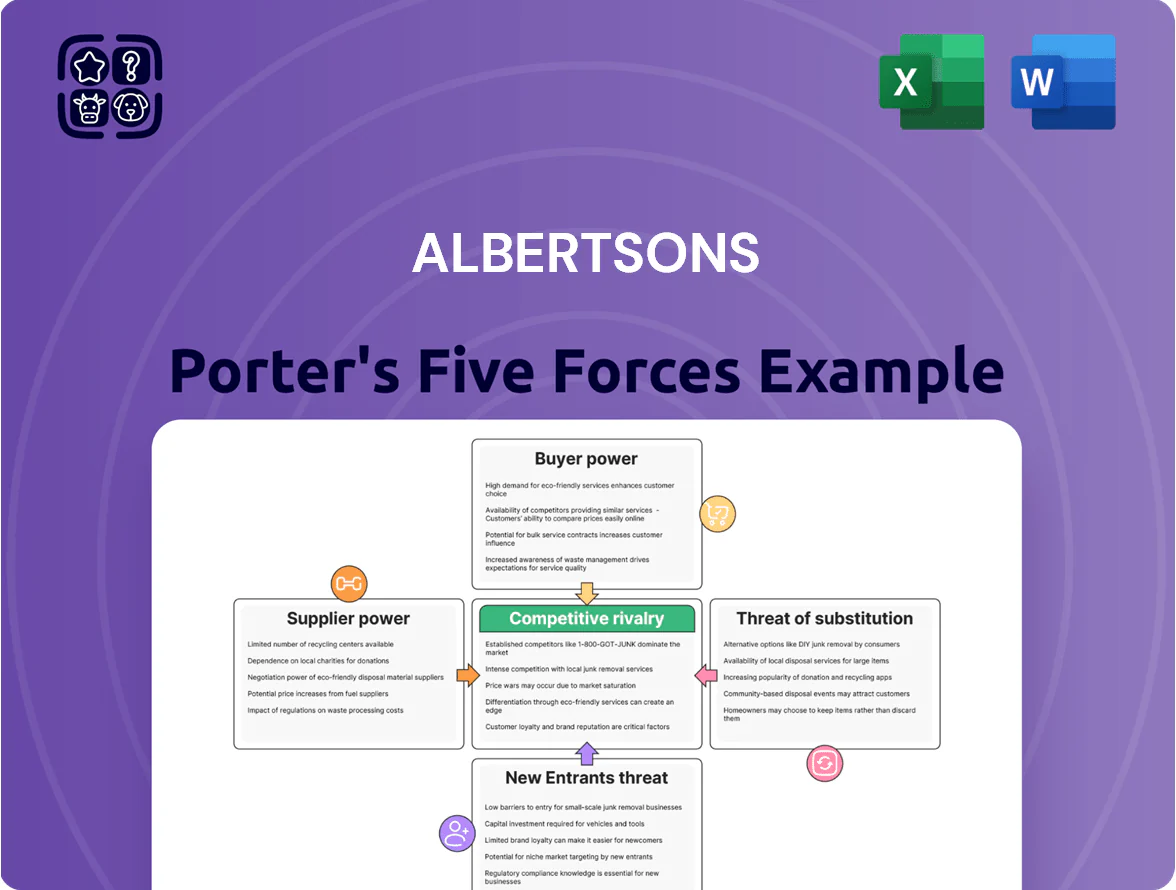

Albertsons faces intense rivalry from national grocers and discounters, moderate supplier power driven by branded goods, and evolving buyer preferences that raise the threat of substitutes and private labels.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Albertsons’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of large CPG brands

Growth of private label brands

Albertsons has grown its Own Brands (Signature Select, O Organics) to ~20% of sales by FY2024, cutting reliance on national vendors and raising private-label gross margins by ~300 basis points vs national brands.

These brands strengthen negotiating leverage—offering credible, lower-cost, high-quality alternatives that enable Albertsons to press suppliers for better pricing and terms, reducing supplier power and protecting EBITDA.

Supply chain and logistics integration

Albertsons operates 38 distribution centers and 33 manufacturing/bakery facilities (2024), which streamline inbound and outbound flows and cut reliance on 3PLs.

Owning this infrastructure lets Albertsons limit inventory carrying costs—company reported a 1.8% improvement in gross margin contribution from supply-chain efficiencies in FY2024.

Controlling logistics reduces bargaining power of mid-tier distributors and transporters, forcing them to accept lower fees or spot contracts.

Impact of commodity price volatility

Suppliers of produce, meat and dairy face rising energy, labor and climate costs; in 2025 many passed price increases to retailers, forcing Albertsons to either cut margins or raise shelf prices—Grocery CPI for food at home rose 3.4% year-over-year in 2025 so far.

The agriculture sector is fragmented, limiting single-supplier leverage, but systemic shocks—droughts, feed-cost spikes—drive volatile contract pricing and strain Albertsons procurement.

- 2025 food-at-home CPI +3.4% Y/Y

- Produce/meat input costs up 8–15% in 2024–25

- Fragmentation lowers supplier concentration

- Systemic shocks increase short-term pass-through risk

Strategic vendor diversification

Albertsons has broadened suppliers to include regional and local producers, reducing reliance on big national brands and answering demand for local goods; by Q4 2025 local SKUs rose ~18% store-wide, cutting national suppliers’ shelf share.

That shift increased sourcing flexibility and created supplier competition for shelf space, helping Albertsons negotiate better terms and lower category supply risk; private-label and local buys reduced COGS pressure by an estimated 40–60 bps in 2025.

- Local SKUs +18% by Q4 2025

- Supplier competition → improved pricing

- Flexibility reduced national supplier leverage

- Estimated COGS relief 40–60 bps (2025)

Albertsons trims COGS via private label/local SKUs but supplier risk stays elevated

| Metric | Value |

|---|---|

| Private-label % of sales (FY2024) | ~20% |

| Local SKUs (Q4 2025) | +18% |

| Input-cost inflation (2024–25) | 8–12% |

| Grocery CPI food-at-home (2025 Y/Y) | +3.4% |

| COGS relief from sourcing shifts (2025) | 40–60 bps |

| Distribution centers / plants (2024) | 38 DCs / 33 plants |

What is included in the product

Provides a concise, Albertsons-specific Porter’s Five Forces assessment that uncovers competitive intensity, buyer and supplier leverage, threat of substitutes, and barriers to entry to inform pricing, strategy, and shareholder value decisions.

One-sheet Porter’s Five Forces for Albertsons—condenses competitive intensity, supplier/buyer leverage, substitution risk, and entry threats into a single view for faster strategic decisions.

Customers Bargaining Power

Low switching costs for shoppers

The grocery sector has near-zero financial barriers for switching, so a shopper can move from Albertsons to Kroger or Walmart after one promo or for convenience; NielsenIQ found 48% of U.S. grocery shoppers switched primary retailers at least once in 2023.

High price sensitivity and transparency

In late 2025 shoppers use apps and digital circulars to compare prices, raising price sensitivity; 68% of US grocery buyers reported switching stores for lower prices in a 2025 NielsenIQ survey. Albertsons faces pressure to match discount chains and warehouse clubs—Costco and Aldi grew same-store sales by mid-single digits in 2025—forcing narrower margins. Customers now split trips across banners, amplifying collective bargaining power and raising promotional frequency.

Influence of digital loyalty programs

The Albertsons for U loyalty program locks customers with personalized rewards and targeted discounts, driving repeat purchases—Albertsons reported over 30 million active members in 2024, accounting for roughly 40% of sales. By using data analytics to tailor offers, the program aims to reduce buyer power and increase basket size (average ticket uplift ~6–8%). Still, rivals like Kroger and Walmart+ offer similar digital perks, so effectiveness depends on continuous engagement and superior value.

Demand for omnichannel flexibility

Modern shoppers expect seamless in-store, curbside, and delivery options, giving customers leverage to demand tech-integrated service; a 2024 McKinsey report found 55% of grocery users now use at least two channels regularly, raising switching risk for laggards.

Albertsons must keep investing in digital platforms—its 2023 $200m+ tech spend and Instacart partnership show this, but competitors like Amazon Fresh and Kroger’s Ocado tie-ups increase pressure on retention.

- 55% of shoppers use 2+ channels (McKinsey 2024)

- Albertsons tech spend ~$200m+ in 2023

- High churn risk if omnichannel lags

Preference for health and sustainability

By end-2025, about 45% of US grocery shoppers prioritize organic/sustainable labels, letting consumers steer Albertsons’ assortment toward certified-organic, fair-trade, and low-carbon products and raising procurement costs by an estimated 2–4% per SKU.

Failure to match these values risks losing younger shoppers: 63% of Gen Z and 52% of millennials say they would stop shopping retailers that ignore sustainability, forcing Albertsons to improve supplier transparency and eco‑certifications.

- 45% of shoppers prefer organic/sustainable (2025)

- Procurement cost +2–4% per SKU

- 63% Gen Z, 52% millennials would abandon retailers

Customers Drive Costs Up: Price, Omnichannel & Sustainability Force Albertsons' Investments

Customers wield strong bargaining power: low switching costs, high price sensitivity (68% switched for lower prices in 2025), omnichannel expectations (55% use 2+ channels), and sustainability preferences (~45% prioritize organic), forcing Albertsons to invest in loyalty, tech, and higher-cost procurement to retain share.

| Metric | Value |

|---|---|

| Switched for price (2025) | 68% |

| Use 2+ channels (2024) | 55% |

| Prefer organic (2025) | 45% |

| Active loyalty members (2024) | 30M |

Preview Before You Purchase

Albertsons Porter's Five Forces Analysis

This preview shows the exact Albertsons Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups, fully written and formatted.

The document displayed here is part of the full, ready-to-download file you’ll get immediately once you buy—prepared for direct use in presentations or reports.

You're viewing the final deliverable: the same comprehensive, professional analysis that will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Albertsons faces intense rivalry from national grocers and discounters, moderate supplier power driven by branded goods, and evolving buyer preferences that raise the threat of substitutes and private labels.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Albertsons’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of large CPG brands

Growth of private label brands

Albertsons has grown its Own Brands (Signature Select, O Organics) to ~20% of sales by FY2024, cutting reliance on national vendors and raising private-label gross margins by ~300 basis points vs national brands.

These brands strengthen negotiating leverage—offering credible, lower-cost, high-quality alternatives that enable Albertsons to press suppliers for better pricing and terms, reducing supplier power and protecting EBITDA.

Supply chain and logistics integration

Albertsons operates 38 distribution centers and 33 manufacturing/bakery facilities (2024), which streamline inbound and outbound flows and cut reliance on 3PLs.

Owning this infrastructure lets Albertsons limit inventory carrying costs—company reported a 1.8% improvement in gross margin contribution from supply-chain efficiencies in FY2024.

Controlling logistics reduces bargaining power of mid-tier distributors and transporters, forcing them to accept lower fees or spot contracts.

Impact of commodity price volatility

Suppliers of produce, meat and dairy face rising energy, labor and climate costs; in 2025 many passed price increases to retailers, forcing Albertsons to either cut margins or raise shelf prices—Grocery CPI for food at home rose 3.4% year-over-year in 2025 so far.

The agriculture sector is fragmented, limiting single-supplier leverage, but systemic shocks—droughts, feed-cost spikes—drive volatile contract pricing and strain Albertsons procurement.

- 2025 food-at-home CPI +3.4% Y/Y

- Produce/meat input costs up 8–15% in 2024–25

- Fragmentation lowers supplier concentration

- Systemic shocks increase short-term pass-through risk

Strategic vendor diversification

Albertsons has broadened suppliers to include regional and local producers, reducing reliance on big national brands and answering demand for local goods; by Q4 2025 local SKUs rose ~18% store-wide, cutting national suppliers’ shelf share.

That shift increased sourcing flexibility and created supplier competition for shelf space, helping Albertsons negotiate better terms and lower category supply risk; private-label and local buys reduced COGS pressure by an estimated 40–60 bps in 2025.

- Local SKUs +18% by Q4 2025

- Supplier competition → improved pricing

- Flexibility reduced national supplier leverage

- Estimated COGS relief 40–60 bps (2025)

Albertsons trims COGS via private label/local SKUs but supplier risk stays elevated

| Metric | Value |

|---|---|

| Private-label % of sales (FY2024) | ~20% |

| Local SKUs (Q4 2025) | +18% |

| Input-cost inflation (2024–25) | 8–12% |

| Grocery CPI food-at-home (2025 Y/Y) | +3.4% |

| COGS relief from sourcing shifts (2025) | 40–60 bps |

| Distribution centers / plants (2024) | 38 DCs / 33 plants |

What is included in the product

Provides a concise, Albertsons-specific Porter’s Five Forces assessment that uncovers competitive intensity, buyer and supplier leverage, threat of substitutes, and barriers to entry to inform pricing, strategy, and shareholder value decisions.

One-sheet Porter’s Five Forces for Albertsons—condenses competitive intensity, supplier/buyer leverage, substitution risk, and entry threats into a single view for faster strategic decisions.

Customers Bargaining Power

Low switching costs for shoppers

The grocery sector has near-zero financial barriers for switching, so a shopper can move from Albertsons to Kroger or Walmart after one promo or for convenience; NielsenIQ found 48% of U.S. grocery shoppers switched primary retailers at least once in 2023.

High price sensitivity and transparency

In late 2025 shoppers use apps and digital circulars to compare prices, raising price sensitivity; 68% of US grocery buyers reported switching stores for lower prices in a 2025 NielsenIQ survey. Albertsons faces pressure to match discount chains and warehouse clubs—Costco and Aldi grew same-store sales by mid-single digits in 2025—forcing narrower margins. Customers now split trips across banners, amplifying collective bargaining power and raising promotional frequency.

Influence of digital loyalty programs

The Albertsons for U loyalty program locks customers with personalized rewards and targeted discounts, driving repeat purchases—Albertsons reported over 30 million active members in 2024, accounting for roughly 40% of sales. By using data analytics to tailor offers, the program aims to reduce buyer power and increase basket size (average ticket uplift ~6–8%). Still, rivals like Kroger and Walmart+ offer similar digital perks, so effectiveness depends on continuous engagement and superior value.

Demand for omnichannel flexibility

Modern shoppers expect seamless in-store, curbside, and delivery options, giving customers leverage to demand tech-integrated service; a 2024 McKinsey report found 55% of grocery users now use at least two channels regularly, raising switching risk for laggards.

Albertsons must keep investing in digital platforms—its 2023 $200m+ tech spend and Instacart partnership show this, but competitors like Amazon Fresh and Kroger’s Ocado tie-ups increase pressure on retention.

- 55% of shoppers use 2+ channels (McKinsey 2024)

- Albertsons tech spend ~$200m+ in 2023

- High churn risk if omnichannel lags

Preference for health and sustainability

By end-2025, about 45% of US grocery shoppers prioritize organic/sustainable labels, letting consumers steer Albertsons’ assortment toward certified-organic, fair-trade, and low-carbon products and raising procurement costs by an estimated 2–4% per SKU.

Failure to match these values risks losing younger shoppers: 63% of Gen Z and 52% of millennials say they would stop shopping retailers that ignore sustainability, forcing Albertsons to improve supplier transparency and eco‑certifications.

- 45% of shoppers prefer organic/sustainable (2025)

- Procurement cost +2–4% per SKU

- 63% Gen Z, 52% millennials would abandon retailers

Customers Drive Costs Up: Price, Omnichannel & Sustainability Force Albertsons' Investments

Customers wield strong bargaining power: low switching costs, high price sensitivity (68% switched for lower prices in 2025), omnichannel expectations (55% use 2+ channels), and sustainability preferences (~45% prioritize organic), forcing Albertsons to invest in loyalty, tech, and higher-cost procurement to retain share.

| Metric | Value |

|---|---|

| Switched for price (2025) | 68% |

| Use 2+ channels (2024) | 55% |

| Prefer organic (2025) | 45% |

| Active loyalty members (2024) | 30M |

Preview Before You Purchase

Albertsons Porter's Five Forces Analysis

This preview shows the exact Albertsons Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups, fully written and formatted.

The document displayed here is part of the full, ready-to-download file you’ll get immediately once you buy—prepared for direct use in presentations or reports.

You're viewing the final deliverable: the same comprehensive, professional analysis that will be available to you instantly after payment.