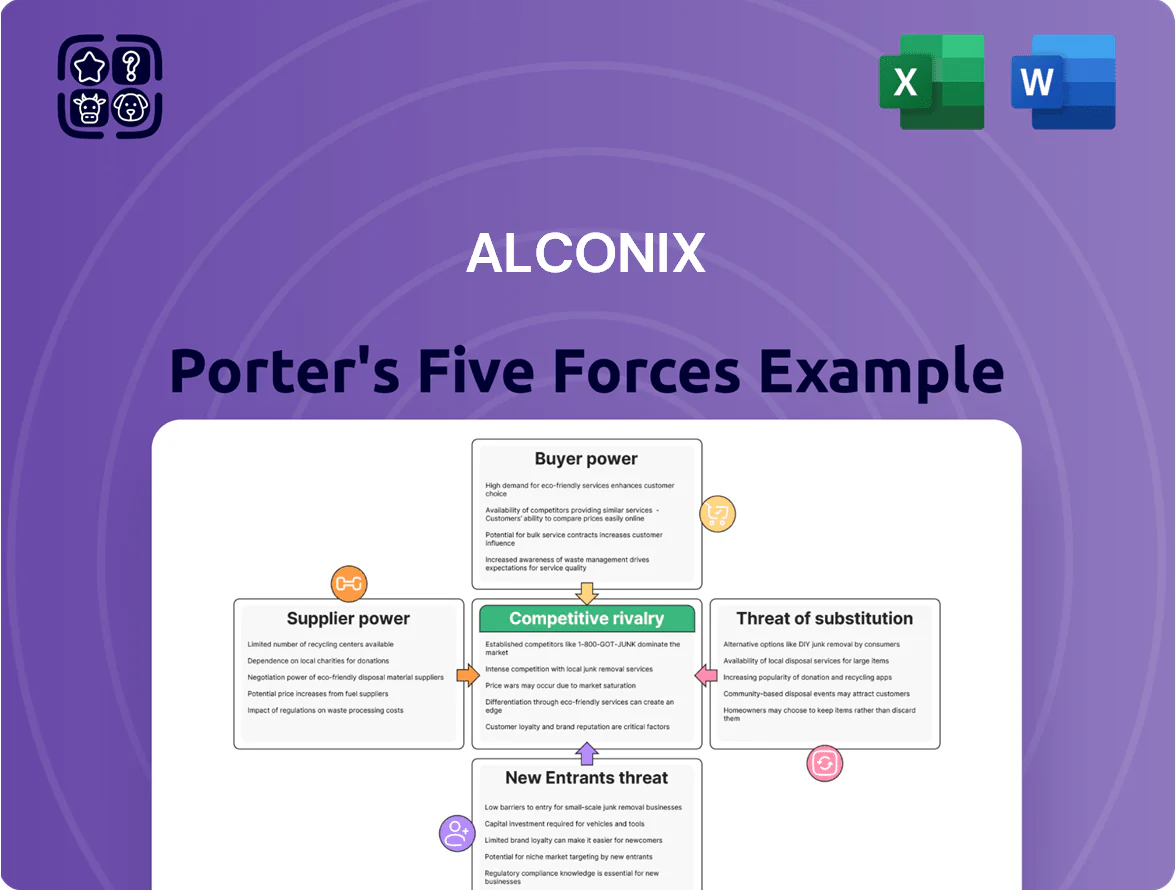

Alconix Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Alconix faces moderate supplier power and intense rivalry from established players, while buyer sensitivity and low switching costs raise pricing pressure—yet niche tech capabilities create a defensible edge.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Alconix’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Primary Metal Producers

The global primary non-ferrous metal supply is concentrated: the top five aluminum producers (including China Hongqiao, Rusal, and Alcoa) accounted for ~45% of 2024 refined output, while BHP, Rio Tinto, and Glencore dominate copper and nickel upstreams, giving suppliers strong leverage over Alconix.

As a specialized trader, Alconix depends on long-term contracts and credit lines with these giants to secure feedstock; limited buyer power forces Alconix to accept supplier-set premiums—copper premium spikes reached 15% in 2024 during tight supply windows.

Geopolitical Control of Rare Earth Elements

Alconix faces high supplier power because rare earths are geopolitically concentrated: China produced ~60% of global rare earth oxides in 2024 and implemented export quotas in 2023–24 that pushed prices up 25–40% for neodymium/praseodymium used in magnets.

Volatility of Global Commodity Pricing

Suppliers of non-ferrous metals peg prices to benchmarks like the London Metal Exchange, so Alconix cannot steer procurement costs; LME copper rose 18% in 2024, showing benchmark-driven swings.

Alconix uses hedges and futures, but price moves follow global supply-demand—world refined copper deficit of ~200 kt in 2024 tightened markets—limiting negotiation leverage.

This market dependence boosts upstream suppliers’ bargaining power over Alconix, squeezing margins during commodity rallies.

Specialized Manufacturing Equipment Providers

Alconix depends on specialized machinery and proprietary tech for metal processing and electronic component production, raising switching costs and supplier power.

These equipment providers charge premium service and parts; industry data shows OEM spare parts margins of 20–40% and average lead times of 12–20 weeks in 2024, increasing Alconix’s operational risk.

The vendors’ technical expertise for maintenance and upgrades gives them leverage over uptime and capital expenditure timing, which can directly affect Alconix’s throughput and margins.

- High switching cost: proprietary tech

- Spare-parts margins: 20–40% (2024)

- Lead times: 12–20 weeks (2024)

- Vendor control over uptime and CAPEX timing

Energy and Logistics Provider Dependency

Alconix relies on global shipping lines and energy-heavy smelting for heavy metals; in 2024 bunker fuel rose ~28% year-over-year, pushing maritime costs and landed material prices higher.

Container shortages and five major carriers controlling ~80% of box capacity limit Alconix’s bargaining power, so transport cost shocks largely pass through to margins.

Supplier squeeze: metals, parts, fuel and shipping margins pinching Alconix

Suppliers hold high bargaining power: top 5 producers ~45% of aluminum, China ~60% of rare earths (2024), LME copper +18% and global refined copper deficit ~200 kt (2024); OEM spare-parts margins 20–40% and lead times 12–20 weeks; bunker fuel +28% and top 5 carriers ≈80% capacity, all squeezing Alconix margins.

| Metric | 2024 |

|---|---|

| Top5 Al output | ~45% |

| China rare earths | ~60% |

| LME copper | +18% |

| Copper deficit | ~200 kt |

| Spare-parts margin | 20–40% |

| Lead times | 12–20 wks |

| Bunker fuel | +28% |

| Top5 carriers | ≈80% |

What is included in the product

Tailored exclusively for Alconix, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry and substitute risks, and identifies disruptive threats to inform strategic positioning and pricing decisions.

Clear, one-sheet Porter's Five Forces summary tailored for Alconix—fast clarity on competitive pressures to streamline strategic decisions and decks.

Customers Bargaining Power

Volume Leverage of Automotive and Electronics Giants

Price Transparency in Metal Markets

Real-time pricing platforms (LME, Fastmarkets, Metal Bulletin) let buyers track non-ferrous metal prices to the minute, so customers can infer Alconix’s likely margins; with LME copper at ~US$9,200/ton in 2025, visible spreads undercut big markups.

That price transparency limits Alconix’s ability to charge premiums on standard alloys, pushing revenue drivers toward value-added services.

Buyers compare quotes across 5–10 trading houses within hours, so Alconix competes on faster delivery, warehousing rates, and inventory-finance terms.

Demand for Integrated Value-Added Services

Low Switching Costs for Standardized Products

For many basic non-ferrous metals Alconix trades, switching costs are low because aluminum and copper ingots are standardized commodities; buyers shift suppliers over price gaps as small as 1–2%, per 2024 trade price elasticity estimates.

This price sensitivity means Alconix must invest in CRM, flexible pricing, and logistics to keep clients; in 2024 Alconix reported 8% higher retention where dedicated account teams handled orders.

- Standardized goods → easy supplier swaps

- Buyers react to ~1–2% price moves

- CRM, pricing, logistics = retention levers

- 2024: dedicated teams → +8% retention

Impact of Customer Vertical Integration

- 2024: customers’ upstream deals ≈ $1.2bn total

- Expected market share loss: 5–12% in 2025–26

- Needed response: focus on niche alloys, traceability, and service contracts

OEMs’ leverage squeezes margins—5% cuts cost 1.8ppt; vertical integration risks 5–12% share

| Metric | Value |

|---|---|

| FY2024 revenue from large OEMs | 45% |

| Price concession impact (5%) | -1.8 ppt gross margin |

| LME copper (2025) | ~US$9,200/t |

| Retention lift (dedicated teams, 2024) | +8% |

| Customer upstream spend (2024) | ~US$1.2bn |

| Expected share loss (2025–26) | 5–12% |

Full Version Awaits

Alconix Porter's Five Forces Analysis

This preview shows the exact Alconix Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; it's fully formatted, professionally written, and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Alconix faces moderate supplier power and intense rivalry from established players, while buyer sensitivity and low switching costs raise pricing pressure—yet niche tech capabilities create a defensible edge.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Alconix’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Primary Metal Producers

The global primary non-ferrous metal supply is concentrated: the top five aluminum producers (including China Hongqiao, Rusal, and Alcoa) accounted for ~45% of 2024 refined output, while BHP, Rio Tinto, and Glencore dominate copper and nickel upstreams, giving suppliers strong leverage over Alconix.

As a specialized trader, Alconix depends on long-term contracts and credit lines with these giants to secure feedstock; limited buyer power forces Alconix to accept supplier-set premiums—copper premium spikes reached 15% in 2024 during tight supply windows.

Geopolitical Control of Rare Earth Elements

Alconix faces high supplier power because rare earths are geopolitically concentrated: China produced ~60% of global rare earth oxides in 2024 and implemented export quotas in 2023–24 that pushed prices up 25–40% for neodymium/praseodymium used in magnets.

Volatility of Global Commodity Pricing

Suppliers of non-ferrous metals peg prices to benchmarks like the London Metal Exchange, so Alconix cannot steer procurement costs; LME copper rose 18% in 2024, showing benchmark-driven swings.

Alconix uses hedges and futures, but price moves follow global supply-demand—world refined copper deficit of ~200 kt in 2024 tightened markets—limiting negotiation leverage.

This market dependence boosts upstream suppliers’ bargaining power over Alconix, squeezing margins during commodity rallies.

Specialized Manufacturing Equipment Providers

Alconix depends on specialized machinery and proprietary tech for metal processing and electronic component production, raising switching costs and supplier power.

These equipment providers charge premium service and parts; industry data shows OEM spare parts margins of 20–40% and average lead times of 12–20 weeks in 2024, increasing Alconix’s operational risk.

The vendors’ technical expertise for maintenance and upgrades gives them leverage over uptime and capital expenditure timing, which can directly affect Alconix’s throughput and margins.

- High switching cost: proprietary tech

- Spare-parts margins: 20–40% (2024)

- Lead times: 12–20 weeks (2024)

- Vendor control over uptime and CAPEX timing

Energy and Logistics Provider Dependency

Alconix relies on global shipping lines and energy-heavy smelting for heavy metals; in 2024 bunker fuel rose ~28% year-over-year, pushing maritime costs and landed material prices higher.

Container shortages and five major carriers controlling ~80% of box capacity limit Alconix’s bargaining power, so transport cost shocks largely pass through to margins.

Supplier squeeze: metals, parts, fuel and shipping margins pinching Alconix

Suppliers hold high bargaining power: top 5 producers ~45% of aluminum, China ~60% of rare earths (2024), LME copper +18% and global refined copper deficit ~200 kt (2024); OEM spare-parts margins 20–40% and lead times 12–20 weeks; bunker fuel +28% and top 5 carriers ≈80% capacity, all squeezing Alconix margins.

| Metric | 2024 |

|---|---|

| Top5 Al output | ~45% |

| China rare earths | ~60% |

| LME copper | +18% |

| Copper deficit | ~200 kt |

| Spare-parts margin | 20–40% |

| Lead times | 12–20 wks |

| Bunker fuel | +28% |

| Top5 carriers | ≈80% |

What is included in the product

Tailored exclusively for Alconix, this Porter's Five Forces analysis uncovers competitive drivers, supplier and buyer power, entry and substitute risks, and identifies disruptive threats to inform strategic positioning and pricing decisions.

Clear, one-sheet Porter's Five Forces summary tailored for Alconix—fast clarity on competitive pressures to streamline strategic decisions and decks.

Customers Bargaining Power

Volume Leverage of Automotive and Electronics Giants

Price Transparency in Metal Markets

Real-time pricing platforms (LME, Fastmarkets, Metal Bulletin) let buyers track non-ferrous metal prices to the minute, so customers can infer Alconix’s likely margins; with LME copper at ~US$9,200/ton in 2025, visible spreads undercut big markups.

That price transparency limits Alconix’s ability to charge premiums on standard alloys, pushing revenue drivers toward value-added services.

Buyers compare quotes across 5–10 trading houses within hours, so Alconix competes on faster delivery, warehousing rates, and inventory-finance terms.

Demand for Integrated Value-Added Services

Low Switching Costs for Standardized Products

For many basic non-ferrous metals Alconix trades, switching costs are low because aluminum and copper ingots are standardized commodities; buyers shift suppliers over price gaps as small as 1–2%, per 2024 trade price elasticity estimates.

This price sensitivity means Alconix must invest in CRM, flexible pricing, and logistics to keep clients; in 2024 Alconix reported 8% higher retention where dedicated account teams handled orders.

- Standardized goods → easy supplier swaps

- Buyers react to ~1–2% price moves

- CRM, pricing, logistics = retention levers

- 2024: dedicated teams → +8% retention

Impact of Customer Vertical Integration

- 2024: customers’ upstream deals ≈ $1.2bn total

- Expected market share loss: 5–12% in 2025–26

- Needed response: focus on niche alloys, traceability, and service contracts

OEMs’ leverage squeezes margins—5% cuts cost 1.8ppt; vertical integration risks 5–12% share

| Metric | Value |

|---|---|

| FY2024 revenue from large OEMs | 45% |

| Price concession impact (5%) | -1.8 ppt gross margin |

| LME copper (2025) | ~US$9,200/t |

| Retention lift (dedicated teams, 2024) | +8% |

| Customer upstream spend (2024) | ~US$1.2bn |

| Expected share loss (2025–26) | 5–12% |

Full Version Awaits

Alconix Porter's Five Forces Analysis

This preview shows the exact Alconix Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; it's fully formatted, professionally written, and ready for download and use the moment you buy.