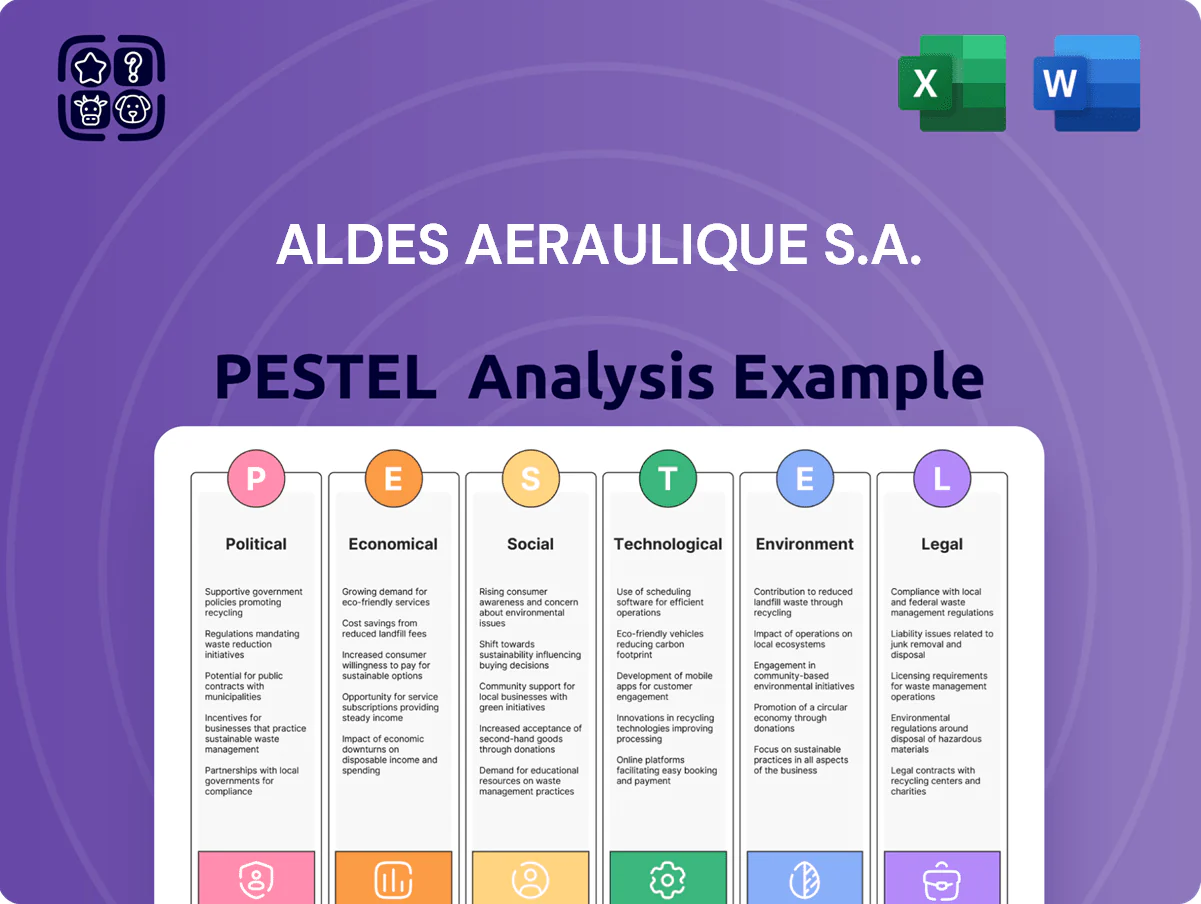

Aldes Aeraulique S.A. PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our PESTLE Analysis for Aldes Aeraulique S.A. highlights how regulatory shifts, energy prices, and technological innovation are reshaping its HVAC market—essential reading for investors and strategists. Gain actionable insights into political risks, environmental obligations, and consumer trends to inform product and market decisions. Purchase the full report to access the complete, editable analysis and immediate strategic recommendations.

Political factors

EU Green Deal and Decarbonization Policies

The EU Green Deal’s target of climate neutrality by 2050 and the Renovation Wave aiming to double renovation rates by 2030 increase demand for high-efficiency ventilation; buildings account for 40% of EU energy consumption and 36% of CO2 emissions, favoring Aldes’ products. New Ecodesign and Energy Performance of Buildings Directive (EPBD) revisions push for heat recovery and low-leak systems, so Aldes must align R&D and capex plans—European HVAC market projected at €90–100bn by 2025—to retain leadership.

French Government Housing Subsidies

Programs like MaPrimeRénov'—which paid out about €6.5 billion from 2020–2023 and supported over 1.2 million renovation projects in 2023—boost demand for energy-efficient ventilation and heat-recovery systems, lowering consumer cost barriers and aiding Aldes' product adoption. Aldes benefits as subsidies accelerate replacement cycles, but remains exposed to shifts in France’s budgetary priorities and political decisions that could reduce aid levels and depress near-term sales.

Geopolitical Supply Chain Stability

Ongoing geopolitical tensions in Eastern Europe and trade disputes in Asia have raised lead times for electronic components by ~18% and pushed global freight costs up 22% in 2024, complicating Aldes Aéraulique S.A.’s sourcing of raw materials.

To mitigate, Aldes is diversifying suppliers and evaluating reshoring for select assemblies; reshoring could cut supply disruption risk by an estimated 30% but may raise unit manufacturing costs by 8–12%.

Political instability in key export markets reduced regional sales growth by up to 6% in 2024 and increased logistics insurance and rerouting costs, pressuring international revenue and operating margins.

Energy Sovereignty and Security Initiatives

Europe's political drive for energy independence is accelerating heat pump and heat-recovery adoption; EU targets aim to cut fossil heating by 55% in buildings by 2030, boosting market demand.

Aldes Aeraulique can align with national energy-security plans by supplying ventilation and heat-recovery systems that lower building gas/electricity use—typical HRV systems reduce heating load by 20–40%.

Mandates for public building upgrades (e.g., EU Renovation Wave targeting 35% renovation rate by 2030) create a predictable institutional project pipeline for Aldes.

- EU target: 55% reduction in building fossil heating by 2030

- HRV systems cut heating load ~20–40%

- Renovation Wave: 35% renovation rate target by 2030

International Trade Regulations and Tariffs

- Exposure: sales in 70+ countries

- Cost risk: component tariff impact 3–7%

- Regulatory change: 2024–25 EU trade updates (Brexit/SPS)

- Logistics shock: container rate volatility (2019–24 +250%)

EU Green Deal Spurs €95B HVAC Boom—Aldes Set to Gain Amid Supply, Reshoring Costs

EU Green Deal and EPBD revisions drive demand for high-efficiency ventilation; buildings = 40% energy use, 36% CO2, favoring Aldes (EU HVAC market €95bn est. 2025). Subsidies (MaPrimeRénov' €6.5bn, 1.2M projects) boost uptake but risk from French budget shifts. Geopolitical/trade tensions raised component lead times ~18% and freight costs +22% in 2024; reshoring cuts disruption risk ~30% but ups costs 8–12%.

| Metric | Value |

|---|---|

| EU HVAC market (2025 est.) | €95bn |

| Buildings energy/CO2 | 40% / 36% |

| MaPrimeRénov' payouts (2020–23) | €6.5bn |

| Component lead time rise (2024) | +18% |

| Freight cost change (2024) | +22% |

| Reshoring cost increase | +8–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Aldes Aéraulique S.A. across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven, region- and industry-specific insights that identify risks, opportunities and forward-looking scenarios to support executives, consultants and investors.

A compact PESTLE summary that highlights regulatory, economic, technological, social, and environmental factors affecting Aldes Aéraulique S.A., designed for quick insertion into presentations and team briefings to streamline external risk discussions and strategic alignment.

Economic factors

Interest Rate Impacts on Construction

Energy Price Volatility

Fluctuating electricity and natural gas prices—up 18% and 22% respectively across EU retail markets in 2022–2024—drive demand for Aldes’ high-efficiency systems; sustained-average EU household energy bills rose ~15% in 2023, improving payback for energy recovery ventilation and heat pumps from >12 years to under 7–8 years in many markets. Aldes positions its IAQ and heat-recovery products around demonstrated energy savings of 30–60% in ventilation-related loads, citing faster ROI as a key sales lever.

Inflation and Raw Material Costs

Persistent inflation raised prices for steel (+15% in EU 2023–24) copper (+12%) and specialty polymers, squeezing Aldes Aéraulique margins and forcing lean manufacturing adoption and selective price increases to preserve gross margin targets near 18–20%.

Rising labor costs—French unit labor cost growth ~6% YoY in 2024—increase installed-system prices, which can depress demand; Aldes must balance automation investments against a 3–5% price sensitivity in HVAC procurement.

Labor Market Shortages in HVAC

A lack of qualified HVAC technicians across Europe—estimated shortages of 100,000+ skilled installers by 2025 in EU countries—creates deployment bottlenecks for Aldes' advanced systems, raising installation costs by 10–20% and extending project timelines by months, which can deter buyers.

Aldes mitigates this through targeted training programs and product designs favoring faster installs, reducing on-site labor time by up to 30% in pilot projects and lowering total installation cost impacts.

- 100,000+ skilled installer shortfall in EU by 2025

- Installation cost increases of 10–20%

- Project delays of several months

- Aldes pilot: up to 30% reduced on-site labor time

Global Market Expansion Opportunities

Economic growth in emerging markets—projected 4.3% GDP growth in 2025 across Asia-Pacific and 3.8% in Sub-Saharan Africa—opens expansion opportunities for Aldes beyond Europe as middle classes and urbanization rise.

Rising pollution and extreme climates boost demand for premium IAQ; WHO estimates 99% of global population breathe air exceeding guidelines, supporting higher ASP potential.

Aldes must assess regional economic stability, FX volatility and projected household disposable income growth (e.g., India real income growth ~5% in 2024–25) to time market entry and CAPEX.

- Target fast-growing markets: Asia-Pacific, MENA, Latin America

- Prioritize countries with rising middle class and GDP growth >3.5%

- Evaluate FX risk, inflation, and regulatory incentives before CAPEX

Aldes pivots to retrofits as EU rates, energy and input costs compress margins

| Metric | Value |

|---|---|

| ECB rate (peak 2024) | 4.25% |

| Electricity price change (2022–24) | +18% |

| Gas price change (2022–24) | +22% |

| Steel price change (EU 2023–24) | +15% |

| Installer shortfall (EU by 2025) | 100,000+ |

Full Version Awaits

Aldes Aeraulique S.A. PESTLE Analysis

The preview shown here is the exact Aldes Aéraulique S.A. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible in this preview are identical to the downloadable file you’ll get immediately after checkout; no placeholders, no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Our PESTLE Analysis for Aldes Aeraulique S.A. highlights how regulatory shifts, energy prices, and technological innovation are reshaping its HVAC market—essential reading for investors and strategists. Gain actionable insights into political risks, environmental obligations, and consumer trends to inform product and market decisions. Purchase the full report to access the complete, editable analysis and immediate strategic recommendations.

Political factors

EU Green Deal and Decarbonization Policies

The EU Green Deal’s target of climate neutrality by 2050 and the Renovation Wave aiming to double renovation rates by 2030 increase demand for high-efficiency ventilation; buildings account for 40% of EU energy consumption and 36% of CO2 emissions, favoring Aldes’ products. New Ecodesign and Energy Performance of Buildings Directive (EPBD) revisions push for heat recovery and low-leak systems, so Aldes must align R&D and capex plans—European HVAC market projected at €90–100bn by 2025—to retain leadership.

French Government Housing Subsidies

Programs like MaPrimeRénov'—which paid out about €6.5 billion from 2020–2023 and supported over 1.2 million renovation projects in 2023—boost demand for energy-efficient ventilation and heat-recovery systems, lowering consumer cost barriers and aiding Aldes' product adoption. Aldes benefits as subsidies accelerate replacement cycles, but remains exposed to shifts in France’s budgetary priorities and political decisions that could reduce aid levels and depress near-term sales.

Geopolitical Supply Chain Stability

Ongoing geopolitical tensions in Eastern Europe and trade disputes in Asia have raised lead times for electronic components by ~18% and pushed global freight costs up 22% in 2024, complicating Aldes Aéraulique S.A.’s sourcing of raw materials.

To mitigate, Aldes is diversifying suppliers and evaluating reshoring for select assemblies; reshoring could cut supply disruption risk by an estimated 30% but may raise unit manufacturing costs by 8–12%.

Political instability in key export markets reduced regional sales growth by up to 6% in 2024 and increased logistics insurance and rerouting costs, pressuring international revenue and operating margins.

Energy Sovereignty and Security Initiatives

Europe's political drive for energy independence is accelerating heat pump and heat-recovery adoption; EU targets aim to cut fossil heating by 55% in buildings by 2030, boosting market demand.

Aldes Aeraulique can align with national energy-security plans by supplying ventilation and heat-recovery systems that lower building gas/electricity use—typical HRV systems reduce heating load by 20–40%.

Mandates for public building upgrades (e.g., EU Renovation Wave targeting 35% renovation rate by 2030) create a predictable institutional project pipeline for Aldes.

- EU target: 55% reduction in building fossil heating by 2030

- HRV systems cut heating load ~20–40%

- Renovation Wave: 35% renovation rate target by 2030

International Trade Regulations and Tariffs

- Exposure: sales in 70+ countries

- Cost risk: component tariff impact 3–7%

- Regulatory change: 2024–25 EU trade updates (Brexit/SPS)

- Logistics shock: container rate volatility (2019–24 +250%)

EU Green Deal Spurs €95B HVAC Boom—Aldes Set to Gain Amid Supply, Reshoring Costs

EU Green Deal and EPBD revisions drive demand for high-efficiency ventilation; buildings = 40% energy use, 36% CO2, favoring Aldes (EU HVAC market €95bn est. 2025). Subsidies (MaPrimeRénov' €6.5bn, 1.2M projects) boost uptake but risk from French budget shifts. Geopolitical/trade tensions raised component lead times ~18% and freight costs +22% in 2024; reshoring cuts disruption risk ~30% but ups costs 8–12%.

| Metric | Value |

|---|---|

| EU HVAC market (2025 est.) | €95bn |

| Buildings energy/CO2 | 40% / 36% |

| MaPrimeRénov' payouts (2020–23) | €6.5bn |

| Component lead time rise (2024) | +18% |

| Freight cost change (2024) | +22% |

| Reshoring cost increase | +8–12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Aldes Aéraulique S.A. across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven, region- and industry-specific insights that identify risks, opportunities and forward-looking scenarios to support executives, consultants and investors.

A compact PESTLE summary that highlights regulatory, economic, technological, social, and environmental factors affecting Aldes Aéraulique S.A., designed for quick insertion into presentations and team briefings to streamline external risk discussions and strategic alignment.

Economic factors

Interest Rate Impacts on Construction

Energy Price Volatility

Fluctuating electricity and natural gas prices—up 18% and 22% respectively across EU retail markets in 2022–2024—drive demand for Aldes’ high-efficiency systems; sustained-average EU household energy bills rose ~15% in 2023, improving payback for energy recovery ventilation and heat pumps from >12 years to under 7–8 years in many markets. Aldes positions its IAQ and heat-recovery products around demonstrated energy savings of 30–60% in ventilation-related loads, citing faster ROI as a key sales lever.

Inflation and Raw Material Costs

Persistent inflation raised prices for steel (+15% in EU 2023–24) copper (+12%) and specialty polymers, squeezing Aldes Aéraulique margins and forcing lean manufacturing adoption and selective price increases to preserve gross margin targets near 18–20%.

Rising labor costs—French unit labor cost growth ~6% YoY in 2024—increase installed-system prices, which can depress demand; Aldes must balance automation investments against a 3–5% price sensitivity in HVAC procurement.

Labor Market Shortages in HVAC

A lack of qualified HVAC technicians across Europe—estimated shortages of 100,000+ skilled installers by 2025 in EU countries—creates deployment bottlenecks for Aldes' advanced systems, raising installation costs by 10–20% and extending project timelines by months, which can deter buyers.

Aldes mitigates this through targeted training programs and product designs favoring faster installs, reducing on-site labor time by up to 30% in pilot projects and lowering total installation cost impacts.

- 100,000+ skilled installer shortfall in EU by 2025

- Installation cost increases of 10–20%

- Project delays of several months

- Aldes pilot: up to 30% reduced on-site labor time

Global Market Expansion Opportunities

Economic growth in emerging markets—projected 4.3% GDP growth in 2025 across Asia-Pacific and 3.8% in Sub-Saharan Africa—opens expansion opportunities for Aldes beyond Europe as middle classes and urbanization rise.

Rising pollution and extreme climates boost demand for premium IAQ; WHO estimates 99% of global population breathe air exceeding guidelines, supporting higher ASP potential.

Aldes must assess regional economic stability, FX volatility and projected household disposable income growth (e.g., India real income growth ~5% in 2024–25) to time market entry and CAPEX.

- Target fast-growing markets: Asia-Pacific, MENA, Latin America

- Prioritize countries with rising middle class and GDP growth >3.5%

- Evaluate FX risk, inflation, and regulatory incentives before CAPEX

Aldes pivots to retrofits as EU rates, energy and input costs compress margins

| Metric | Value |

|---|---|

| ECB rate (peak 2024) | 4.25% |

| Electricity price change (2022–24) | +18% |

| Gas price change (2022–24) | +22% |

| Steel price change (EU 2023–24) | +15% |

| Installer shortfall (EU by 2025) | 100,000+ |

Full Version Awaits

Aldes Aeraulique S.A. PESTLE Analysis

The preview shown here is the exact Aldes Aéraulique S.A. PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and insights visible in this preview are identical to the downloadable file you’ll get immediately after checkout; no placeholders, no surprises.