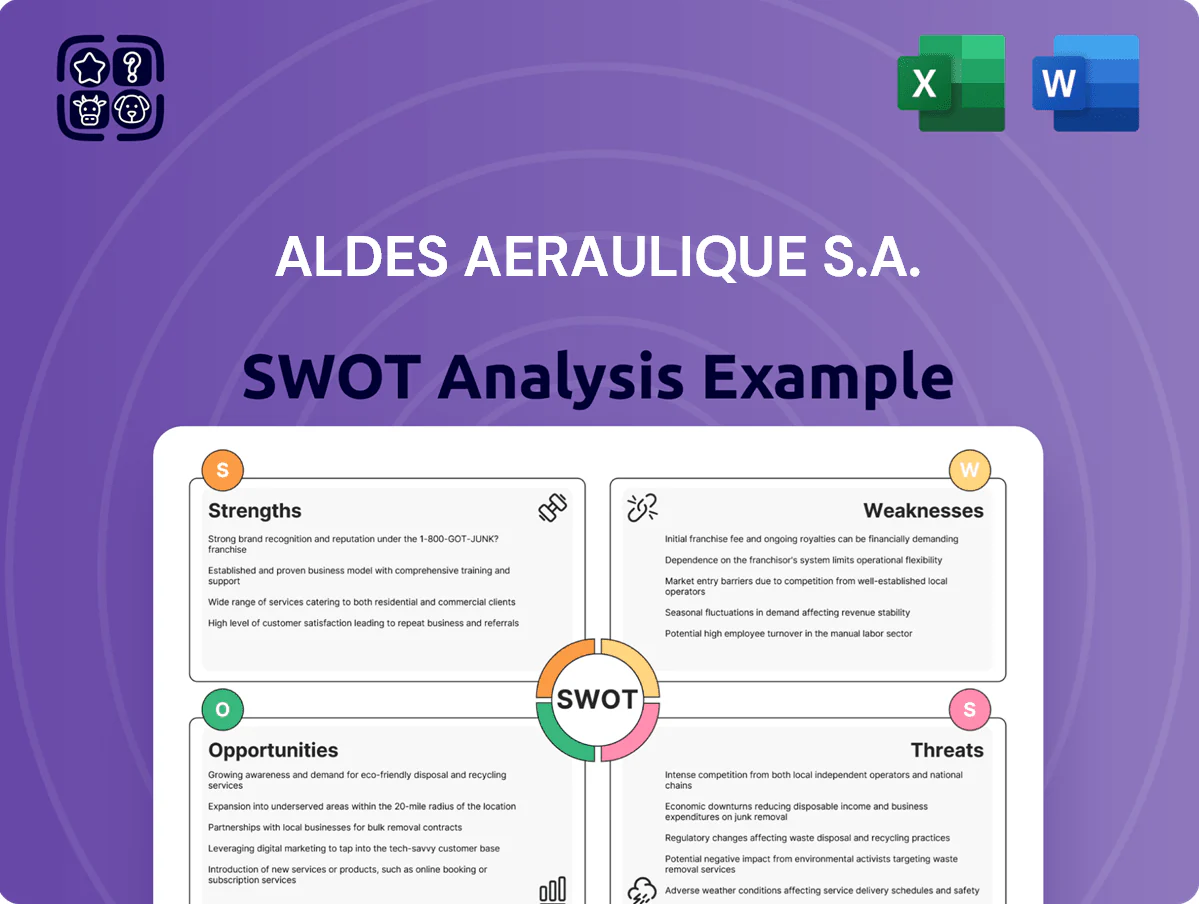

Aldes Aeraulique S.A. SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Aldes Aéraulique S.A. demonstrates engineering strength in HVAC solutions and a solid European footprint but faces competition, regulatory pressures, and supply-chain risks that could impact margins and growth.

Discover the complete picture behind the company’s market position with our full SWOT analysis. This in-depth report reveals actionable insights, financial context, and strategic takeaways—ideal for entrepreneurs, analysts, and investors.

Strengths

Market Leadership in Indoor Air Quality

Aldes holds a dominant spot in the European HVAC market and about 35% share in France’s residential ventilation segment as of Dec 2025, driven by a strict IAQ focus. By end-2025 the brand is widely seen as top for high-performance ventilation and purification, with €420m group revenue in 2024 and sustained installer loyalty. This edge rests on deep local code expertise and a reliability record—installed base exceeding 2.1 million systems in Europe.

Robust Research and Development Pipeline

Diverse Product Portfolio

Aldes Aeraulique S.A. sells a wide ecosystem from residential ventilation to industrial fire protection and central vacuum, letting it serve homes, offices, hospitals and factories and cut dependence on any single category.

In 2024 Aldes reported €520m revenue and 18% of sales from fire-protection/industrial systems, so diversified sales stabilize cash flow and lower segment risk.

By offering end-to-end air management (design, hardware, installation) Aldes captures more project value: aftermarket and services lifted gross margin by ~220 basis points in 2024.

Strong Focus on Energy Efficiency

Aldes’s focus on low-energy products gives it a clear edge as decarbonization drives building demand; energy-efficient HVAC and ventilation reduce operational CO2 and lower life-cycle costs.

Their thermodynamic water heaters and heat-recovery ventilation systems cut energy use by up to 60% versus electric heaters and recover ~70% heat, aligning with HQE, BREEAM, and LEED targets.

- Energy savings: up to 60%

- Heat recovery: ~70%

- Market fit: meets LEED/BREEAM/HQE

- Competitive edge: lower operating CO2

Established International Distribution Network

Aldes Aéraulique S.A. has scaled into Europe, North America and Asia via subsidiaries and partnerships, delivering ~45% of 2024 revenue outside France (€210m group sales in 2024).

This global footprint cushions regional downturns and lets the firm export French HVAC engineering into high-growth markets (EMEA + APAC sales +8% in 2024).

Localized support teams provide on-site service and technical assistance, keeping international NPS above 60 and reducing warranty costs by ~12% vs 2022.

- 45% of 2024 revenue from abroad

- €210m group sales in 2024

- EMEA+APAC sales +8% in 2024

- International NPS >60; warranty costs -12%

Aldes: EU ventilation leader—€520M, 35% France share, energy cuts & 45% export

Aldes leads EU residential ventilation (≈35% France share, ~2.1M installed systems) with €520m revenue in 2024 and €420m group revenue reported for 2024 in prior filing; R&D at 6–8% supports HEPA and enthalpy modules in 70% of core lines, cutting fan energy ~22%; diversified portfolio (18% fire/industrial) and 45% revenue outside France stabilize cash flow; services lift gross margin +220 bp.

| Metric | 2024 / 2025 |

|---|---|

| Group revenue | €520m (2024) |

| France ventil. share | ≈35% (Dec 2025) |

| Installed systems | ≈2.1M (Europe) |

| R&D spend | 6–8% rev |

| HEPA/enthalpy mix | 70% core lines (2025) |

| Energy cut | Fan −22%; heaters −60% |

| Export revenue | 45% (€210m abroad) |

| Fire/industrial | 18% sales |

| Service margin lift | +220 bp |

What is included in the product

Provides a concise SWOT overview of Aldes Aeraulique S.A., highlighting its core strengths in HVAC innovation and market reach, internal weaknesses in scale and diversification, external opportunities from energy-efficiency regulations and smart-building trends, and threats from competitive pressures and raw‑material cost volatility.

Delivers a concise SWOT snapshot of Aldes Aéraulique S.A. for rapid strategic alignment and clear stakeholder communication.

Weaknesses

High Production Costs in Europe

Aldes Aéraulique keeps much manufacturing in France and Italy, where unit labor costs are ~25-40% higher than Eastern Europe (Eurostat 2024), squeezing 2024 adjusted EBIT margin (reported 6.8%) versus low-cost peers.

High-quality output offsets defects, but exposure to Eurozone wage growth (2.5% avg 2023–24) and volatile energy prices raises margin risk; keeping engineering premium while cutting price gaps is an ongoing operational strain.

Heavy Reliance on the Construction Sector

The company’s revenue remains tightly tied to residential and commercial construction: in 2024 Aldes Aéraulique S.A. reported 62% of sales from HVAC for new builds, so a 10% drop in EU building permits (Eurostat H1 2024) cuts near-term demand materially.

When permits fell 8% YoY in 2023–24 in key markets, Aldes’s organic growth slowed to 1.5% in FY2024, showing exposure to cyclical real-estate swings.

That cyclicality forces conservative liquidity planning: Aldes held €120m net cash at end-2024 but needs tight working-capital controls during downturns to avoid margin erosion.

Complexity of Product Installation

Limited Brand Awareness in Consumer Markets

Aldes Aéraulique S.A. is well-known among architects and HVAC professionals but lacks household recognition versus consumer brands like Dyson or Nest, limiting pull in the renovation market.

As smart-home ventilation grows (global smart home market ~US$138B in 2024, CAGR ~14% to 2029), Aldes’ weak consumer equity forces higher marketing spend to win end-users.

Higher CAC and channel investment likely needed for direct-to-consumer moves; FY2024 revenue ~€240M signals room but not scale for mass marketing.

- Strong B2B reputation, weak consumer brand

- Smart-home trend favors consumer-facing brands

- Needs higher marketing spend, raises CAC

- FY2024 revenue ~€240M, limits massive consumer push

Slow Digital Transformation in Legacy Lines

Legacy air distribution lines still lack IoT and BACnet/Modbus support, while Aldes’ new smart products grew revenues 18% in 2024, exposing a product mix gap.

Updating the full catalog to BMS compatibility needs capital and R&D; Aldes’ 2024 R&D spend was ~3.2% of sales, below HVAC peers at ~4–5%.

Delays risk share loss to tech-native startups: global smart HVAC market grew 22% in 2024, favoring fast integrators.

- Legacy lines missing IoT/BMS (BACnet/Modbus)

- Smart products +18% revenue (2024)

- R&D spend ~3.2% of sales (2024) vs peers 4–5%

- Smart HVAC market +22% (2024) — fast movers advantage

High costs, weak R&D squeeze margins as technician shortages threaten HVAC growth

Manufacturing in France/Italy raises unit costs ~25–40% vs Eastern Europe (Eurostat 2024), squeezing 2024 adjusted EBIT margin at 6.8%; wage growth (avg 2.5% 2023–24) and energy volatility add margin risk. Revenue 62% tied to new-build HVAC; a 10% drop in EU permits cuts near-term demand—organic growth slowed to 1.5% in FY2024. Technician shortages (74% of firms, 2024) slow smart-product rollouts; R&D was 3.2% of sales vs peers 4–5%, leaving legacy lines without IoT/BMS support.

| Metric | 2024 Value |

|---|---|

| Adj. EBIT margin | 6.8% |

| Revenue tied to new builds | 62% |

| FY2024 revenue | ≈€240M |

| Net cash end-2024 | €120M |

| R&D spend | 3.2% of sales |

| Smart product growth | +18% |

| EU HVAC firms reporting shortages | 74% |

Preview Before You Purchase

Aldes Aeraulique S.A. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and it reflects the real, structured analysis of Aldes Aéraulique S.A. Once purchased, the complete, editable version with in-depth insights and supporting data will be available for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Aldes Aéraulique S.A. demonstrates engineering strength in HVAC solutions and a solid European footprint but faces competition, regulatory pressures, and supply-chain risks that could impact margins and growth.

Discover the complete picture behind the company’s market position with our full SWOT analysis. This in-depth report reveals actionable insights, financial context, and strategic takeaways—ideal for entrepreneurs, analysts, and investors.

Strengths

Market Leadership in Indoor Air Quality

Aldes holds a dominant spot in the European HVAC market and about 35% share in France’s residential ventilation segment as of Dec 2025, driven by a strict IAQ focus. By end-2025 the brand is widely seen as top for high-performance ventilation and purification, with €420m group revenue in 2024 and sustained installer loyalty. This edge rests on deep local code expertise and a reliability record—installed base exceeding 2.1 million systems in Europe.

Robust Research and Development Pipeline

Diverse Product Portfolio

Aldes Aeraulique S.A. sells a wide ecosystem from residential ventilation to industrial fire protection and central vacuum, letting it serve homes, offices, hospitals and factories and cut dependence on any single category.

In 2024 Aldes reported €520m revenue and 18% of sales from fire-protection/industrial systems, so diversified sales stabilize cash flow and lower segment risk.

By offering end-to-end air management (design, hardware, installation) Aldes captures more project value: aftermarket and services lifted gross margin by ~220 basis points in 2024.

Strong Focus on Energy Efficiency

Aldes’s focus on low-energy products gives it a clear edge as decarbonization drives building demand; energy-efficient HVAC and ventilation reduce operational CO2 and lower life-cycle costs.

Their thermodynamic water heaters and heat-recovery ventilation systems cut energy use by up to 60% versus electric heaters and recover ~70% heat, aligning with HQE, BREEAM, and LEED targets.

- Energy savings: up to 60%

- Heat recovery: ~70%

- Market fit: meets LEED/BREEAM/HQE

- Competitive edge: lower operating CO2

Established International Distribution Network

Aldes Aéraulique S.A. has scaled into Europe, North America and Asia via subsidiaries and partnerships, delivering ~45% of 2024 revenue outside France (€210m group sales in 2024).

This global footprint cushions regional downturns and lets the firm export French HVAC engineering into high-growth markets (EMEA + APAC sales +8% in 2024).

Localized support teams provide on-site service and technical assistance, keeping international NPS above 60 and reducing warranty costs by ~12% vs 2022.

- 45% of 2024 revenue from abroad

- €210m group sales in 2024

- EMEA+APAC sales +8% in 2024

- International NPS >60; warranty costs -12%

Aldes: EU ventilation leader—€520M, 35% France share, energy cuts & 45% export

Aldes leads EU residential ventilation (≈35% France share, ~2.1M installed systems) with €520m revenue in 2024 and €420m group revenue reported for 2024 in prior filing; R&D at 6–8% supports HEPA and enthalpy modules in 70% of core lines, cutting fan energy ~22%; diversified portfolio (18% fire/industrial) and 45% revenue outside France stabilize cash flow; services lift gross margin +220 bp.

| Metric | 2024 / 2025 |

|---|---|

| Group revenue | €520m (2024) |

| France ventil. share | ≈35% (Dec 2025) |

| Installed systems | ≈2.1M (Europe) |

| R&D spend | 6–8% rev |

| HEPA/enthalpy mix | 70% core lines (2025) |

| Energy cut | Fan −22%; heaters −60% |

| Export revenue | 45% (€210m abroad) |

| Fire/industrial | 18% sales |

| Service margin lift | +220 bp |

What is included in the product

Provides a concise SWOT overview of Aldes Aeraulique S.A., highlighting its core strengths in HVAC innovation and market reach, internal weaknesses in scale and diversification, external opportunities from energy-efficiency regulations and smart-building trends, and threats from competitive pressures and raw‑material cost volatility.

Delivers a concise SWOT snapshot of Aldes Aéraulique S.A. for rapid strategic alignment and clear stakeholder communication.

Weaknesses

High Production Costs in Europe

Aldes Aéraulique keeps much manufacturing in France and Italy, where unit labor costs are ~25-40% higher than Eastern Europe (Eurostat 2024), squeezing 2024 adjusted EBIT margin (reported 6.8%) versus low-cost peers.

High-quality output offsets defects, but exposure to Eurozone wage growth (2.5% avg 2023–24) and volatile energy prices raises margin risk; keeping engineering premium while cutting price gaps is an ongoing operational strain.

Heavy Reliance on the Construction Sector

The company’s revenue remains tightly tied to residential and commercial construction: in 2024 Aldes Aéraulique S.A. reported 62% of sales from HVAC for new builds, so a 10% drop in EU building permits (Eurostat H1 2024) cuts near-term demand materially.

When permits fell 8% YoY in 2023–24 in key markets, Aldes’s organic growth slowed to 1.5% in FY2024, showing exposure to cyclical real-estate swings.

That cyclicality forces conservative liquidity planning: Aldes held €120m net cash at end-2024 but needs tight working-capital controls during downturns to avoid margin erosion.

Complexity of Product Installation

Limited Brand Awareness in Consumer Markets

Aldes Aéraulique S.A. is well-known among architects and HVAC professionals but lacks household recognition versus consumer brands like Dyson or Nest, limiting pull in the renovation market.

As smart-home ventilation grows (global smart home market ~US$138B in 2024, CAGR ~14% to 2029), Aldes’ weak consumer equity forces higher marketing spend to win end-users.

Higher CAC and channel investment likely needed for direct-to-consumer moves; FY2024 revenue ~€240M signals room but not scale for mass marketing.

- Strong B2B reputation, weak consumer brand

- Smart-home trend favors consumer-facing brands

- Needs higher marketing spend, raises CAC

- FY2024 revenue ~€240M, limits massive consumer push

Slow Digital Transformation in Legacy Lines

Legacy air distribution lines still lack IoT and BACnet/Modbus support, while Aldes’ new smart products grew revenues 18% in 2024, exposing a product mix gap.

Updating the full catalog to BMS compatibility needs capital and R&D; Aldes’ 2024 R&D spend was ~3.2% of sales, below HVAC peers at ~4–5%.

Delays risk share loss to tech-native startups: global smart HVAC market grew 22% in 2024, favoring fast integrators.

- Legacy lines missing IoT/BMS (BACnet/Modbus)

- Smart products +18% revenue (2024)

- R&D spend ~3.2% of sales (2024) vs peers 4–5%

- Smart HVAC market +22% (2024) — fast movers advantage

High costs, weak R&D squeeze margins as technician shortages threaten HVAC growth

Manufacturing in France/Italy raises unit costs ~25–40% vs Eastern Europe (Eurostat 2024), squeezing 2024 adjusted EBIT margin at 6.8%; wage growth (avg 2.5% 2023–24) and energy volatility add margin risk. Revenue 62% tied to new-build HVAC; a 10% drop in EU permits cuts near-term demand—organic growth slowed to 1.5% in FY2024. Technician shortages (74% of firms, 2024) slow smart-product rollouts; R&D was 3.2% of sales vs peers 4–5%, leaving legacy lines without IoT/BMS support.

| Metric | 2024 Value |

|---|---|

| Adj. EBIT margin | 6.8% |

| Revenue tied to new builds | 62% |

| FY2024 revenue | ≈€240M |

| Net cash end-2024 | €120M |

| R&D spend | 3.2% of sales |

| Smart product growth | +18% |

| EU HVAC firms reporting shortages | 74% |

Preview Before You Purchase

Aldes Aeraulique S.A. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and it reflects the real, structured analysis of Aldes Aéraulique S.A. Once purchased, the complete, editable version with in-depth insights and supporting data will be available for download.