ALFA Boston Consulting Group Matrix

Actionable Strategy Starts Here

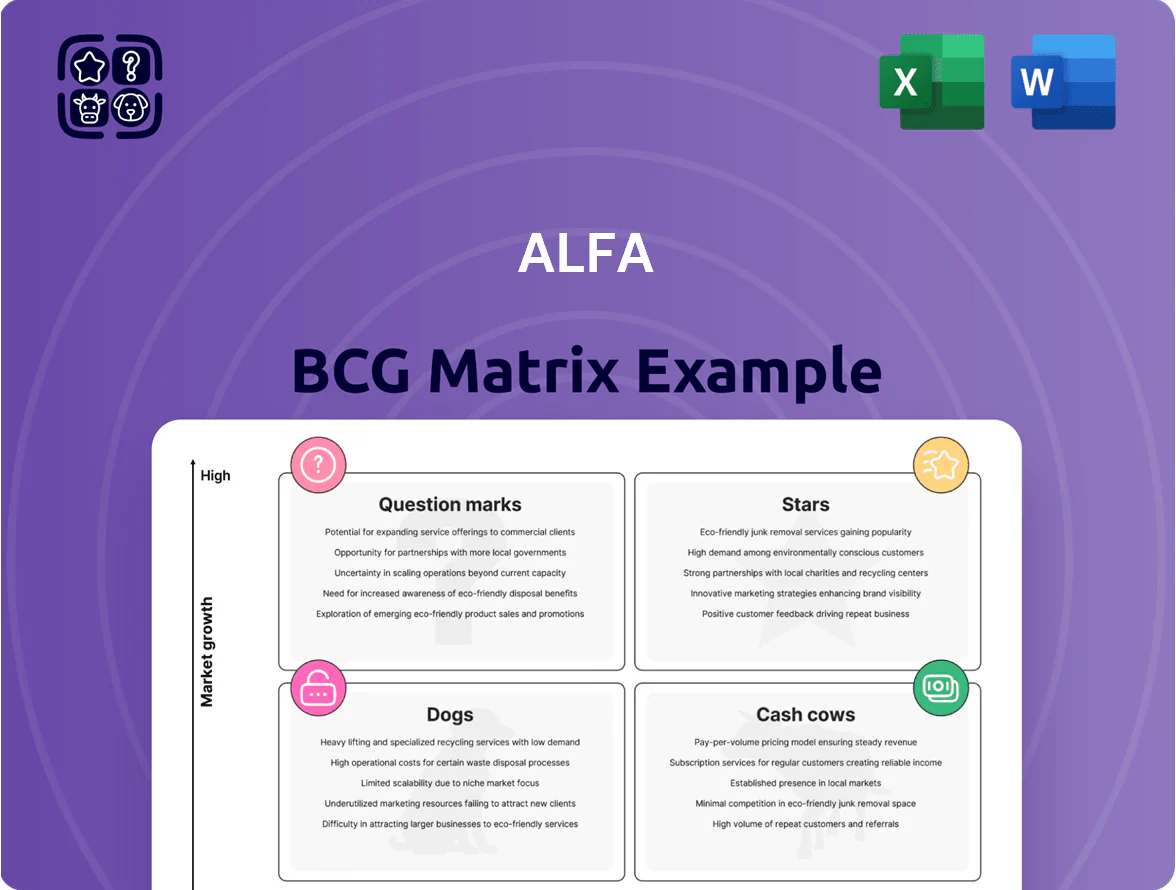

ALFA’s BCG Matrix snapshot highlights where its product lines fall among Stars, Cash Cows, Dogs, and Question Marks, revealing strengths and capital allocation needs at a glance. This preview teases competitive positioning and growth potential, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and strategic next steps. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary—fast, evidence-based guidance to optimize investments and product strategy.

Stars

Sigma Health and Wellness Portfolio

Sigma Health and Wellness sits as a Star in ALFA’s BCG matrix: plant-based and low-sodium lines grew 22% YoY in 2025, capturing ~18% share of ALFA’s FMCG sales as consumers shift to healthier diets.

Maintaining leadership needs heavy marketing—estimated $48M capex and $30M annual SG&A in 2025—to fend off Nestlé and Unilever rivals, but margins are improving toward 14% EBITDA.

ALFA’s distribution reach—3,200 retail partners across the Americas and 14 European countries—cuts time-to-market and supports projected revenue CAGR of 16% through 2028.

Alpek Specialty Polyester and Recycling

Alpek Specialty Polyester and Recycling is a Star: global demand for recycled PET (rPET) grew ~12% in 2024 to ~6.5 million tonnes, and Alpek claims a leading share via 1.1 Mt of installed rPET capacity after 2023–25 expansions.

Heavy capex—about $450M invested 2022–2024—built sorting and depolymerization plants, securing dominant positions in green packaging contracts with Coca-Cola FEMSA and P&G.

Though capital intensive, the unit drives margin resilience; rPET spreads improved 18% in 2024, and the segment is critical to meeting 2025 ESG targets requiring 30–50% recycled content for major beverage clients.

Nemak E-Mobility Components

Nemak E-Mobility Components are Stars: Nemak shifted into EVs, making complex aluminum battery and e-motor housings, with e-mobility revenue rising to ~25% of total sales by 2024 and segment growth >20% CAGR (2021–24).

High growth and market leadership demand ongoing R&D—Nemak spent ≈$85M on R&D in 2024, much aimed at heat management and lightweighting to match shifting EV tech.

This unit is the future of the auto division as ICE volumes fell ~15% from 2019–24, so electrified components will likely dominate Nemak’s portfolio by 2028 given current trends.

Axtel Managed IT and Cloud Services

Axtel Managed IT and Cloud Services sits in the Stars quadrant after Axtel's 2023 pivot: enterprise cloud and cybersecurity serve a Mexican market growing ~18% CAGR in cloud spend 2023–2025, with Axtel reporting 22% YoY revenue growth in enterprise services in 2024 and 30% gross margin, keeping strong share among large corporates.

Significant capex—about MXN 1.2 billion in 2024—was reinvested to expand scalable, secure infrastructure and match competitors like AWS/GCP partners; churn stayed below 6% in 2024.

- Market growth ~18% CAGR (2023–2025)

- Axtel enterprise rev +22% YoY (2024)

- Gross margin ~30% (2024)

- Capex MXN 1.2B (2024)

- Customer churn <6% (2024)

Sigma Snacking and Convenience Brands

Sigma Snacking and Convenience Brands sit as a Star in ALFA’s BCG matrix: premium on-the-go snacks grew 18% in 2024 and hold ~28% market share in Colombia convenience channels, driven by Sigma’s strong brand equity and shelf dominance.

To sustain this high-growth, high-share position ALFA must keep investing in product innovation and packaging—R&D spend rose 12% in 2024—and defend against niche entrants capturing 6–8% annual share in premium segments.

- 2024 growth: 18%

- Market share (convenience): ~28%

- R&D increase in 2024: 12%

- Niche entrant share gain: 6–8% annually

High‑growth portfolio: Sigma, Alpek rPET, Nemak E‑Mobility, Axtel Cloud, Sigma Snacks

Stars: Sigma Health (22% YoY, 18% FMCG share, EBITDA ~14%, 2025 capex $48M/SG&A $30M), Alpek rPET (rPET +12% 2024, 1.1Mt capacity, $450M capex 2022–24), Nemak E‑Mobility (25% rev share 2024, >20% CAGR 2021–24, R&D $85M 2024), Axtel Cloud (22% YoY 2024, 30% gross, MXN1.2B capex 2024), Sigma Snacks (18% 2024, 28% convenience share).

| Unit | Key metrics |

|---|---|

| Sigma Health | 22% YoY; 18% share; EBITDA 14% |

| Alpek rPET | 1.1Mt; +12% demand; $450M capex |

| Nemak | 25% rev; >20% CAGR; $85M R&D |

| Axtel | +22% YoY; 30% gross; MXN1.2B |

| Sigma Snacks | 18% growth; 28% share |

What is included in the product

Comprehensive ALFA BCG Matrix review: quadrant insights, investment recommendations, competitive risks, and trend-driven strategic actions.

One-page ALFA BCG Matrix placing each business unit in a quadrant for instant portfolio clarity

Cash Cows

Sigma Traditional Cold Cuts

Sigma Traditional Cold Cuts dominates Mexico and much of Latin America with ~25–30% market share in processed meats (2024 Euromonitor), delivering steady annual EBITDA margins near 15% and ~MXN 12–15 billion in operating cash flow (2024 Alfa consolidated reports).

As a mature cash cow, it needs little marketing spend and funds Alfa’s bets in petrochemicals, refrigeration, and tech, plus debt reduction—Alfa used ~MXN 8 billion from food-unit cash flow for capex and deleveraging in 2024.

Alpek PTA and PET Commodities

Alpek, a top-five global producer of purified terephthalic acid (PTA) and polyethylene terephthalate (PET) resins, sits in a mature market with global PTA/PET growth ~2% CAGR (2020–2025); scale and feedstock integration drove 2024 EBITDA margin ~18% and free cash flow of ~$450m, delivering steady cash for ALFA’s investments.

Nemak Internal Combustion Engine Castings

Nemak’s Internal Combustion Engine castings (cylinder heads, engine blocks) remain a cash cow, delivering ~€1.1bn revenue and ~18% EBITDA margin in 2024 and representing >40% of group sales; high share, low growth as EV penetration hit 14% globally in 2024.

Production assets are fully depreciated and running at ~85% capacity with unit costs down 12% since 2019, generating free cash flow that funded €220m capex for EV structural programs in 2024.

Sigma Dairy and Cheese Division

Sigma Dairy and Cheese Division holds market-leading brands in Mexico with ~30–40% category share and annual revenues near MXN 22 billion (2024), enjoying high consumer loyalty in a low-growth but stable market.

Household-name status keeps marketing spend under 6% of sales, enabling gross margins above 28% and strong free cash flow that buffers ALFA against petrochemical and telecom volatility.

- Category share: ~30–40%

- 2024 revenue: ~MXN 22 billion

- Marketing spend: <6% of sales

- Gross margin: >28%

- Function: Stable cash generator vs volatile sectors

Alpek Polypropylene Operations

Alpek’s polypropylene unit, serving mature industrial and consumer goods, generated about $1.1 billion EBITDA in 2024 and retains a strong regional market share across North America and Mexico, with stable demand and limited need for transformative capex.

Its predictable cash flow funded ~25% of ALFA’s 2024 free cash flow and underpinned a 2024 dividend payout ratio near 60%, making it a classic cash cow for the group.

- 2024 EBITDA ≈ $1.1B

- Funds ~25% of ALFA FCF 2024

- Dividend support: ~60% payout ratio 2024

- Low capex, stable end markets

ALFA's 2024 Cash Cows: Sigma, Alpek PP & Nemak — MXN20–25bn FCF fueling growth

Sigma processed meats and dairy, Alpek PTA/PET and polypropylene, and Nemak ICE castings are ALFA’s cash cows (2024): steady market shares 25–40%, EBITDA margins ~15–18%, combined FCF ≈ MXN 20–25bn / $1.1bn from polypropylene, funding capex, deleveraging, and dividends.

| Unit | 2024 Rev | EBITDA% | FCF | Role |

|---|---|---|---|---|

| Sigma Foods | MXN 22bn | 15 | MXN 12–15bn | Fund group |

| Alpek PP | - | 18 | $1.1bn | Dividends |

| Nemak ICE | €1.1bn | 18 | — | Stable cash |

Full Transparency, Always

ALFA BCG Matrix

The file you're previewing is the exact ALFA BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document tailored for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

ALFA’s BCG Matrix snapshot highlights where its product lines fall among Stars, Cash Cows, Dogs, and Question Marks, revealing strengths and capital allocation needs at a glance. This preview teases competitive positioning and growth potential, but the full BCG Matrix delivers quadrant-by-quadrant data, actionable recommendations, and strategic next steps. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary—fast, evidence-based guidance to optimize investments and product strategy.

Stars

Sigma Health and Wellness Portfolio

Sigma Health and Wellness sits as a Star in ALFA’s BCG matrix: plant-based and low-sodium lines grew 22% YoY in 2025, capturing ~18% share of ALFA’s FMCG sales as consumers shift to healthier diets.

Maintaining leadership needs heavy marketing—estimated $48M capex and $30M annual SG&A in 2025—to fend off Nestlé and Unilever rivals, but margins are improving toward 14% EBITDA.

ALFA’s distribution reach—3,200 retail partners across the Americas and 14 European countries—cuts time-to-market and supports projected revenue CAGR of 16% through 2028.

Alpek Specialty Polyester and Recycling

Alpek Specialty Polyester and Recycling is a Star: global demand for recycled PET (rPET) grew ~12% in 2024 to ~6.5 million tonnes, and Alpek claims a leading share via 1.1 Mt of installed rPET capacity after 2023–25 expansions.

Heavy capex—about $450M invested 2022–2024—built sorting and depolymerization plants, securing dominant positions in green packaging contracts with Coca-Cola FEMSA and P&G.

Though capital intensive, the unit drives margin resilience; rPET spreads improved 18% in 2024, and the segment is critical to meeting 2025 ESG targets requiring 30–50% recycled content for major beverage clients.

Nemak E-Mobility Components

Nemak E-Mobility Components are Stars: Nemak shifted into EVs, making complex aluminum battery and e-motor housings, with e-mobility revenue rising to ~25% of total sales by 2024 and segment growth >20% CAGR (2021–24).

High growth and market leadership demand ongoing R&D—Nemak spent ≈$85M on R&D in 2024, much aimed at heat management and lightweighting to match shifting EV tech.

This unit is the future of the auto division as ICE volumes fell ~15% from 2019–24, so electrified components will likely dominate Nemak’s portfolio by 2028 given current trends.

Axtel Managed IT and Cloud Services

Axtel Managed IT and Cloud Services sits in the Stars quadrant after Axtel's 2023 pivot: enterprise cloud and cybersecurity serve a Mexican market growing ~18% CAGR in cloud spend 2023–2025, with Axtel reporting 22% YoY revenue growth in enterprise services in 2024 and 30% gross margin, keeping strong share among large corporates.

Significant capex—about MXN 1.2 billion in 2024—was reinvested to expand scalable, secure infrastructure and match competitors like AWS/GCP partners; churn stayed below 6% in 2024.

- Market growth ~18% CAGR (2023–2025)

- Axtel enterprise rev +22% YoY (2024)

- Gross margin ~30% (2024)

- Capex MXN 1.2B (2024)

- Customer churn <6% (2024)

Sigma Snacking and Convenience Brands

Sigma Snacking and Convenience Brands sit as a Star in ALFA’s BCG matrix: premium on-the-go snacks grew 18% in 2024 and hold ~28% market share in Colombia convenience channels, driven by Sigma’s strong brand equity and shelf dominance.

To sustain this high-growth, high-share position ALFA must keep investing in product innovation and packaging—R&D spend rose 12% in 2024—and defend against niche entrants capturing 6–8% annual share in premium segments.

- 2024 growth: 18%

- Market share (convenience): ~28%

- R&D increase in 2024: 12%

- Niche entrant share gain: 6–8% annually

High‑growth portfolio: Sigma, Alpek rPET, Nemak E‑Mobility, Axtel Cloud, Sigma Snacks

Stars: Sigma Health (22% YoY, 18% FMCG share, EBITDA ~14%, 2025 capex $48M/SG&A $30M), Alpek rPET (rPET +12% 2024, 1.1Mt capacity, $450M capex 2022–24), Nemak E‑Mobility (25% rev share 2024, >20% CAGR 2021–24, R&D $85M 2024), Axtel Cloud (22% YoY 2024, 30% gross, MXN1.2B capex 2024), Sigma Snacks (18% 2024, 28% convenience share).

| Unit | Key metrics |

|---|---|

| Sigma Health | 22% YoY; 18% share; EBITDA 14% |

| Alpek rPET | 1.1Mt; +12% demand; $450M capex |

| Nemak | 25% rev; >20% CAGR; $85M R&D |

| Axtel | +22% YoY; 30% gross; MXN1.2B |

| Sigma Snacks | 18% growth; 28% share |

What is included in the product

Comprehensive ALFA BCG Matrix review: quadrant insights, investment recommendations, competitive risks, and trend-driven strategic actions.

One-page ALFA BCG Matrix placing each business unit in a quadrant for instant portfolio clarity

Cash Cows

Sigma Traditional Cold Cuts

Sigma Traditional Cold Cuts dominates Mexico and much of Latin America with ~25–30% market share in processed meats (2024 Euromonitor), delivering steady annual EBITDA margins near 15% and ~MXN 12–15 billion in operating cash flow (2024 Alfa consolidated reports).

As a mature cash cow, it needs little marketing spend and funds Alfa’s bets in petrochemicals, refrigeration, and tech, plus debt reduction—Alfa used ~MXN 8 billion from food-unit cash flow for capex and deleveraging in 2024.

Alpek PTA and PET Commodities

Alpek, a top-five global producer of purified terephthalic acid (PTA) and polyethylene terephthalate (PET) resins, sits in a mature market with global PTA/PET growth ~2% CAGR (2020–2025); scale and feedstock integration drove 2024 EBITDA margin ~18% and free cash flow of ~$450m, delivering steady cash for ALFA’s investments.

Nemak Internal Combustion Engine Castings

Nemak’s Internal Combustion Engine castings (cylinder heads, engine blocks) remain a cash cow, delivering ~€1.1bn revenue and ~18% EBITDA margin in 2024 and representing >40% of group sales; high share, low growth as EV penetration hit 14% globally in 2024.

Production assets are fully depreciated and running at ~85% capacity with unit costs down 12% since 2019, generating free cash flow that funded €220m capex for EV structural programs in 2024.

Sigma Dairy and Cheese Division

Sigma Dairy and Cheese Division holds market-leading brands in Mexico with ~30–40% category share and annual revenues near MXN 22 billion (2024), enjoying high consumer loyalty in a low-growth but stable market.

Household-name status keeps marketing spend under 6% of sales, enabling gross margins above 28% and strong free cash flow that buffers ALFA against petrochemical and telecom volatility.

- Category share: ~30–40%

- 2024 revenue: ~MXN 22 billion

- Marketing spend: <6% of sales

- Gross margin: >28%

- Function: Stable cash generator vs volatile sectors

Alpek Polypropylene Operations

Alpek’s polypropylene unit, serving mature industrial and consumer goods, generated about $1.1 billion EBITDA in 2024 and retains a strong regional market share across North America and Mexico, with stable demand and limited need for transformative capex.

Its predictable cash flow funded ~25% of ALFA’s 2024 free cash flow and underpinned a 2024 dividend payout ratio near 60%, making it a classic cash cow for the group.

- 2024 EBITDA ≈ $1.1B

- Funds ~25% of ALFA FCF 2024

- Dividend support: ~60% payout ratio 2024

- Low capex, stable end markets

ALFA's 2024 Cash Cows: Sigma, Alpek PP & Nemak — MXN20–25bn FCF fueling growth

Sigma processed meats and dairy, Alpek PTA/PET and polypropylene, and Nemak ICE castings are ALFA’s cash cows (2024): steady market shares 25–40%, EBITDA margins ~15–18%, combined FCF ≈ MXN 20–25bn / $1.1bn from polypropylene, funding capex, deleveraging, and dividends.

| Unit | 2024 Rev | EBITDA% | FCF | Role |

|---|---|---|---|---|

| Sigma Foods | MXN 22bn | 15 | MXN 12–15bn | Fund group |

| Alpek PP | - | 18 | $1.1bn | Dividends |

| Nemak ICE | €1.1bn | 18 | — | Stable cash |

Full Transparency, Always

ALFA BCG Matrix

The file you're previewing is the exact ALFA BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document tailored for strategic clarity and professional use.